EMX Royalty (EMX) - Transformative Transaction... At Last

Interview with David Cole, President & CEO of EMX Royalty Corp. (TSX-V, NYSE: EMX)

Last time we spoke to David Cole, CEO of EMX Royalty Corporation, the company had a healthy amount of cash, sitting at $40M, and no debt. Recently they have put this cash to use, announcing an agreement to acquire the Royalty Portfolio from SSR Mining. David goes into more detail about this transaction.

Company Overview

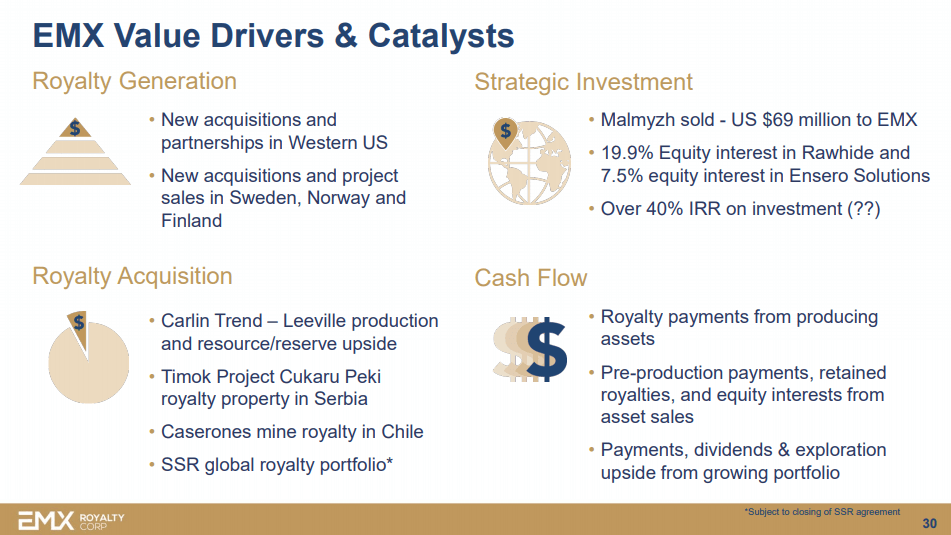

EMX generates royalties utilising the prospects generation business model. They have exposure to 300 mineral property positions around the world. EMX has retained a royalty interest and received pre-production cash payments. They also supplement royalty generation with the careful acquisition of royalty interests in production and advanced development assets. The cash flow from mineral property payments, royalties and advanced royalties generates ongoing revenue for the company’s sustainable growth and value creation. They choose investments in upside mineral exploration opportunities with good exit strategies focused on favouring royalty positions or equity sales.

Royalty: Conversation, discussions & Expenditure

SSR Mining’s Royalty Portfolio comprises 18 geographically diverse royalties, with four of these royalty assets at advanced stages of project development. This also includes $18M in future cash payments to be made to the owner of the Royalty Portfolio.

David confirms that the conversation to acquire this agreement has been occurring for quite some time. Scotiabank was the broker representing SSR Mining. Initially, EMX contacted SSR due to an already established relationship with their Vice President of Exploration, who David has worked with for some time. These talks occurred both inside and outside Turkey, where the mining company is based. It was EMX that suggested they sell their Royalty Portfolio to them and SSR were happy with the idea and hired Scotiabank, who both parties have good relationships with, to ensure a fair price.

100 Million Dollar Deal, Terms, Structure & Assets

When the transaction closes, EMX will pay $33M to SSR in cash and $33M of common shares of EMX, which will be 11-12% pro-rata depending on EMX’s share price during the upcoming VWAP period. The agreement also includes EMX making deferred and contingent payments to SSR of a sequence of $34M payments as the Yenipazar project is fully de-risked. This will bring EMX’s cash value down close to zero. It is for this reason that they put in place the $10M facility from Sprott Global, who has been a long-term supportive capital partner of EMX.

The structure of the Royalty Portfolio comprises some development, resource stage and exploration stage assets. The development stage assets sit within a private company, Xinjiang Mining based in China. They do not meet the 43-101 standards but announce reserves and resources on their website. This is the same for Balya, another private company, which is advancing a very large Lead-Zinc-Silver deposit with a 5000t per day mill. Based in Turkey, they don’t meet 43-101 standards. It is because of this that David can’t talk about the resource and is a reason why he believes EMX remains undervalued. However, this value will be demonstrated when the cash flows are shown. The Gediktepe mine has a 43-101 document by a previous operator. David confirmed EMX is obtaining 10% royalty on the oxide cap, and a 2% royalty in perpetuity on the sulphides.

Obtaining 10% NSR, Parts of Portfolio, NPI Royalties & Greater Interest Rates

SSR was a predecessor company to Lidya, who previously held and operated in Gediktepe. They designed this, which was a key component to the price they sold it to Lidya. The price heavily weighted on the near-term production from the oxide cap, as it holds an enriched Gold-Silver zone with a very high profit margin. The sulphide has a higher cost of production, which brings the royalty to 2% due to its complexity. The oxide has been in production for 3-years with the anticipation that it will bring double digit millions of dollars per year to EMX right away. EMX now has 10% NSR on this asset.

EMX sits on 6% and 10% NPI for Yenipazar, which is part of the same portfolio sold by SSR. It is a Net Profit Interest Royalty (NPI), which is typically subject to greater dispute and variables than can be worked. In a bad year, if metal prices go down for example, there will be no payments. This makes the NPI a greater risk than an NSR. The pay structure for this royalty requires the project to completely de-risk before EMX pays. At construction $2M of EMX stock gets paid to SSR at production, followed by another $2M in stock paid to SSR. After Royalties pay $10M, EMX pays SSR $15M. When it's paid another $10-20M total, EMX pays the balance of $34M. The most EMX would be out of pocket is $14M despite the headline number of $34M, as the de-risking occurs and proves to be a profitable cash flowing operation.

Finances: EMX Royalty & Expected Revenue Timings

Gediktepe will be in production in a month, which really drives early cash flow on this acquisition with an $18M in deferred payments across the portfolio. The portfolio was built in a similar manner to the way EMX builds its portfolio, by selling projects and bringing in payments. Due to not meeting the 43-101 standards on material assets, not much detail on revenue and timings can be said for Yenipazar and Diablilos at the moment. However, right after the close of the deal, more information and public disclosures around these, especially on forecasting cash flows into 2022, will follow after a month.

EMX Royalties 2022-2023: Will There Be an Overhang Over Stock?

There’s a lot of synergies with SSR, especially as they are an incipient shareholder, and this was one of the key catalysts that enabled the transaction to work. In terms of an overhang, David notes it is a free market and SSR are allowed to go down this route if they wish. However, he doesn’t believe that’s their intent at all. In their press release, they publicly announced their desire to be an EMX shareholder.

Supportive Partners, Expectations & Future

EMX has other capital partners who support the company if they need to raise additional money for this deal and future deals. They have a good reputation with capital players, so if SSR starts selling down in blocks, this would not be much of a concern for them. The acquisition will provide a powerful cash flow over the next 3-years with the 10% NSR at Gediktepe, whilst the rest of the portfolio matures. Ultimately, this acquisition is transformative and will change the shape and colour of the EMX.

To find out more, go to the EMX Royalty Website

Analyst's Notes

Subscribe to Our Channel

Stay Informed