Energy & Freight Inflation Are Reshaping the Salt Market: Why Regional Supply Is Becoming a Strategic Advantage

Energy and freight inflation are reshaping the salt market, favoring regional producers with lower delivered costs and stable demand.

- Energy price volatility and freight cost inflation are compressing margins across bulk commodity supply chains. Salt is among the most exposed: its low value-to-weight ratio means freight represents a disproportionately large share of delivered cost, and producers have limited ability to pass those costs through on government and long-term industrial contracts.

- Global supply chains are fragmenting under geopolitical pressure. For bulk commodities where freight is a primary cost variable, that fragmentation favors producers with short routes to end markets over those dependent on long-haul marine supply.

- Salt demand is non-discretionary across its three primary end uses, de-icing, chlor-alkali chemical production, and water treatment, which limits demand-side downside risk even during broader industrial slowdowns.

- Margin differentiation in salt is driven by delivered cost, not commodity price. Operational efficiency and transport proximity are the variables that determine which producers retain contracts and which lose them as freight and energy costs rise.

- Development-stage producers with logistical proximity to import-dependent markets are positioned to displace long-haul supply on cost, not product differentiation. Atlas Salt Inc., advancing the Great Atlantic Salt project on the west coast of Newfoundland, sits in this category.ages that cannot easily be replicated by incumbent long-distance suppliers.

Salt as a Macro-Sensitive Bulk Commodity

Salt generates no speculative inflows, commands no scarcity premium, and attracts limited institutional coverage. Its investment relevance is cost-structural: delivered price, not spot price, determines which producers retain industrial contracts, because salt buyers source on total landed cost and can switch suppliers when a freight differential erodes a competitor's mine-gate advantage.

That cost structure exposes salt directly to two variables currently repricing across industrial supply chains: energy and bulk freight. Energy drives extraction, evaporation, and processing, making it a primary determinant of cash operating costs regardless of production method. Bulk freight determines whether a low-cost mine-gate producer retains that advantage at the point of delivery. A producer that is cheaper to extract from can still be more expensive to buy from.

The investment question in salt is not whether prices will rise. It is which producers can hold delivered-cost competitiveness as energy and freight remain elevated, and which cannot, regardless of extraction efficiency.

Energy Price Volatility and Its Transmission into Bulk Commodity Costs

Energy is the primary cost driver across mining and bulk material supply chains. In salt, energy costs transmit through three channels: diesel-powered extraction, electricity-intensive crushing and handling, and fuel-sensitive marine transport. A significant share of global salt trade moves on Handymax and Panamax vessels, where bunker fuel is a direct and material cost component.

The impact is asymmetric across producers. Salt producers operate on thin margins with limited pricing power: government contracts and long-term industrial agreements constrain cost pass-through. Energy inflation therefore compresses margins rather than triggering price increases, and that compression falls hardest on producers with high energy intensity and long transport routes. Producers with lower energy intensity and shorter routes to end markets gain a structural cost advantage as fuel costs rise, one that widens, rather than closes, under sustained inflation.

The Shift Toward Regional Commodity Supply

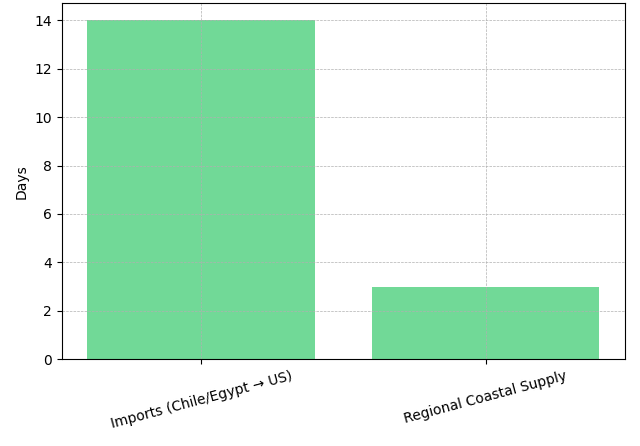

Geopolitical disruption, port bottlenecks, and supply chain dislocations have increased shipping costs and extended delivery times for bulk commodities. For salt, where value-to-weight is low, freight represents a disproportionately large share of delivered cost — and that share grows on long-haul routes. Imported salt can take roughly two weeks to reach North American markets. Regional coastal supply arrives in two to three days. That difference is not just logistical; it affects working capital requirements, inventory planning, and the ability to respond to seasonal demand surges.

In North America, strong de-icing demand contrasts with a constrained domestic supply base: most operating underground mines were developed decades ago, and limited new capacity has entered the market. The region relies heavily on imports from Chile and Egypt, a supply model that becomes less reliable and more costly as freight rates remain elevated. Atlas Salt Inc. is advancing the Great Atlantic Salt project in Newfoundland, leveraging deep-water port access to supply US East Coast markets. Its advantage lies not in product differentiation, but in replacing long-haul imports with shorter, lower-cost supply routes.

As Chief Executive Officer Nolan Peterson describes the supply gap the project is designed to address:

"There's not enough supply. There's quite a bit of demand. There hasn't been a new mine built in 25 years at this point."

Stable Demand, Cost-Driven Margins

Salt demand is structurally resilient because its primary end uses are non-discretionary. De-icing salt applied to road networks is a public safety expenditure procured by municipal and state governments regardless of economic conditions. Chlor-alkali chemical production, which accounts for an estimated 45 to 50 percent of industrial salt demand globally, is an upstream input for PVC, disinfectants, and essential industrial chemicals, with no near-term substitution pathway. Water treatment and food processing represent additional demand segments with similarly limited substitution risk.

That demand profile produces a commodity with low price volatility and high sensitivity to cost-side pressure. Salt prices do not spike during supply disruptions the way battery metals or energy commodities do. The market clears through regional delivered-cost differentials: the producer with the lowest delivered cost does not benefit from a price environment, it holds a persistent margin advantage over higher-cost alternatives.

Salt is not a price-driven commodity. It is a cost-driven margin business where operational efficiency and logistics infrastructure determine long-run contract competitiveness.

Why Logistics Determines the Competitive Hierarchy

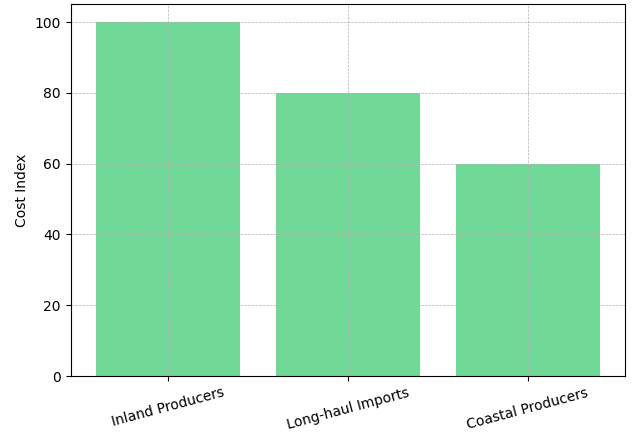

Salt deposits are broadly homogeneous and processing is relatively straightforward. Ore grade does not differentiate producers. Delivered cost does.

Three producer categories exist in salt, each with a distinct cost position. Inland producers carry the highest delivered costs because overland transport is expensive relative to the value of the product. Long-distance importers benefit from shipping scale but absorb high absolute freight costs and supply chain variability. Coastal, near-market producers achieve the lowest delivered costs by combining marine transport efficiency with short route distances.

Atlas Salt's Great Atlantic Salt project sits in the lowest-cost category. Its 2024 feasibility study indicates an operating cost of approximately US$28 per tonne FOB, against a post-tax NPV of approximately US$920 million, an IRR of approximately 21.3 percent, and a payback period of approximately 4.2 years on capital expenditure of approximately US$589 million at 4 million tonnes per annum. The cost advantage over long-haul importers is structural: as fuel costs rise, short-route producers benefit from lower absolute freight exposure, and the delivered-cost gap between them and long-haul competitors widens rather than compresses.

Why New Salt Supply Is Structurally Limited

Salt is not a commodity that attracts meaningful exploration or development capital. The economics are not compelling enough to justify greenfield development unless a project has a specific logistical or scale advantage that justifies the capital outlay. As a result, the North American supply base is dominated by underground mines developed decades ago, with limited new capacity entering the market.

Permitting timelines represents an additional constraint. Environmental assessment processes for underground mining projects typically extend across multiple years. Atlas Salt received its environmental assessment approval from the Government of Newfoundland and Labrador in approximately two months, an outcome the company attributes in part to strong provincial government support and a project design centered on 100 percent battery-electric underground operation, which reduces surface emissions and simplifies environmental review.

The combination of limited new supply entering the market and persistent import dependence along the US East Coast creates the conditions under which a large-scale new development can secure long-term offtake visibility. The Great Atlantic Salt project targets a 25-year mine life based on current reserves, with resource upside that management estimates could support an additional 50 or more years of production.

Project Economics in a Higher-Cost Capital Environment

Rising construction costs and higher financing rates have narrowed the investable universe of bulk commodity development projects. Investors are prioritizing short payback periods, demonstrable cash flow visibility, and project structures that can absorb cost escalation without material deterioration in returns.

Atlas Salt's feasibility study economics are structured for this environment. A post-tax NPV of approximately US$920 million against capital expenditure of approximately US$589 million produces an NPV-to-capex ratio of approximately 1.56, the project generates value above its construction cost before accounting for resource upside. A 4.2-year payback period is competitive within the bulk commodity development pipeline, where payback periods of six to eight years are more common for large-scale underground projects.

Atlas Salt is advancing project financing with Endeavor Financial. That structure separates construction execution risk from equity dilution risk and aligns debt service timing with production cash flows.

Demand Resilience, Weather Risk, and Execution Variables

Weather is the primary demand-side risk. Warmer winters reduce de-icing volumes and create revenue variability for producers with high municipal exposure. Partial diversification into chlor-alkali and industrial markets provides insulation, but seasonal variability cannot be fully offset.

Energy prices introduce a two-directional effect. Higher fuel costs increase mine and processing expenses but also widen the delivered-cost advantage of near-market producers over long-haul importers. For the Great Atlantic Salt project, the net effect under sustained energy inflation is likely positive, though the magnitude depends on the relative scale of operating cost increases versus freight cost increases borne by competing import supply.

Execution risk at the development stage remains: financing, capital costs, and construction timelines are variables that have not yet been resolved. Permitting risk is largely addressed. The demand base, de-icing and chlor-alkali, is non-discretionary, which supports more stable revenue assumptions than most industrial commodities.

The Investment Thesis for Salt

- Salt provides defensive exposure to essential industrial demand across de-icing, water treatment, and chlor-alkali chemical production, segments that do not contract materially during economic downturns, providing a more stable demand floor than most bulk commodities.

- Energy and freight inflation are structurally repricing delivered costs across the bulk commodity supply chain, disproportionately penalizing long-haul import-dependent supply structures and creating durable margin advantages for near-market coastal producers.

- Supply chain fragmentation driven by geopolitical disruption and elevated shipping costs is accelerating the structural value of localized infrastructure assets with direct port access to import-dependent regional markets.

- The near-absence of new underground salt mine development over the past 25 years has created regional supply deficits that cannot be resolved quickly, given permitting timelines and capital requirements, establishing long-term contract visibility for large-scale new entrants.

- Development timelines are aligned with a multi-year structural supply deficit in the US East Coast, where import dependence is high and domestic production alternatives are limited, providing near-term offtake visibility as construction advances.

Salt is not a commodity that rewards price speculation or exploration-stage optionality. It rewards cost discipline, logistics precision, and structural positioning relative to the regional markets it serves. The intersection of energy price volatility and freight cost inflation is not a temporary dislocation, it reflects a fundamental repricing of the assumptions on which long-haul bulk commodity supply chains were built.

The implication is that the competitive hierarchy in salt will be determined not by ore quality or reserve size, but by delivered cost and regional supply proximity. Projects that combine logistical advantage with defensible project economics and a non-discretionary demand base represent a class of infrastructure-adjacent commodity exposure that is increasingly difficult to source in an environment where most new mining development is concentrated in higher-profile critical minerals. As the macroeconomic case for regionalized supply strengthens, the scarcity value of large-scale, near-port salt development assets will continue to increase.

TL;DR

Salt is a cost-driven margin business, not a price-driven commodity. Delivered cost, not spot price, determines which producers retain industrial contracts, and that delivered cost is being repriced upward by energy inflation and elevated bulk freight rates. Salt demand is non-discretionary across its primary end uses, so the market does not clear through price spikes; it clears through producers with higher delivered costs losing contracts to those with lower ones. North America has not seen a new underground salt mine enter production in approximately 25 years, leaving the US East Coast structurally dependent on long-haul imports from Chile and Egypt, a supply model that becomes more expensive and less reliable as freight rates remain elevated. Atlas Salt Inc.'s Great Atlantic Salt project in Newfoundland is positioned to displace that import supply on delivered cost, not product differentiation, by combining a deep-water port with short marine routes to US East Coast markets. Its 2024 feasibility study indicates a post-tax NPV of approximately US$920 million, an IRR of approximately 21.3 percent, and a 4.2-year payback on approximately US$589 million in capital expenditure, project economics structured for an environment where capital is selective and payback period is the primary screen.

FAQs (AI generated)

Salt's investment relevance is not price-based, it is cost-structural. Because salt buyers source on total landed cost and can switch suppliers when delivered-cost differentials make an alternative cheaper, the margin a producer earns is determined entirely by how efficiently it can deliver product to the buyer's door relative to competing sources. That makes salt sensitive to the two variables currently repricing across industrial supply chains, energy and bulk freight, in a way that directly affects which producers retain contracts and which lose them. A commodity where contract retention is mechanically tied to delivered-cost position, and where that cost position is being disrupted by macro forces, is investable precisely because the disruption creates a durable structural advantage for the producers on the right side of the cost divide.

Salt producers operate on thin margins with limited pricing power. Government contracts and long-term industrial agreements constrain cost pass-through, so when freight and energy costs rise, the impact falls on producer margins rather than being absorbed by buyers through higher prices. A long-haul importer facing elevated bunker fuel costs cannot lower its delivered price without compressing margins; it likely does not have room to compress. A near-market coastal producer, by contrast, carries lower absolute freight exposure — its cost base rises more slowly under fuel inflation than a competitor shipping from Chile or Egypt. The competitive gap is therefore not closed by pricing decisions; it widens mechanically as freight costs rise, because the cost disadvantage is structural to the route distance, not addressable through operational efficiency.

Two structural constraints prevent the gap from closing quickly. First, salt does not attract meaningful exploration or development capital, the economics are not compelling enough to justify greenfield investment unless a specific logistical or scale advantage is present, which limits the field of credible new entrants. Second, permitting and construction timelines for underground mining projects are measured in years, not months, meaning even a capital-ready developer cannot bring new supply to market quickly. The result is a North American supply base dominated by underground mines developed decades ago, with no significant new capacity having entered the market in approximately 25 years. Import dependence along the US East Coast is therefore a condition that cannot be resolved by market forces in the near term, which establishes durable offtake visibility for a large-scale new entrant that is already through permitting and advancing toward financing.

The 100 percent battery-electric underground operation removes diesel combustion from the underground environment, which reduces ventilation requirements, lowers surface emissions, and simplifies the environmental assessment process. Atlas Salt received its environmental assessment approval from the Government of Newfoundland and Labrador in approximately two months, an outcome the company attributes in part to the project's emission profile and strong provincial government support. On the cost side, battery-electric equipment eliminates diesel fuel as a direct operating cost underground, which reduces exposure to diesel price volatility, one of the three channels through which energy inflation transmits into salt production costs. The design therefore addresses both the permitting constraint that typically extends development timelines and the energy cost exposure that pressures margins across the broader producer base.

The primary risks are on the execution side: financing, capital costs, and construction timelines have not yet been resolved, and cost escalation in the current environment is a real variable for any development-stage project. Weather introduces demand-side variability, warmer winters reduce de-icing volumes and create revenue pressure for producers with high municipal exposure. On the macro side, the net effect of energy inflation on Atlas Salt is likely positive given its short-route cost structure, but the magnitude depends on how operating cost increases compared to the freight cost increases borne by competing import supply, a balance that is not guaranteed. Offsetting these risks is a demand base that is non-discretionary at its core: de-icing is a public safety expenditure and chlor-alkali is an upstream industrial input with no near-term substitution pathway. That demand profile supports more stable revenue assumptions than most industrial commodities and limits the downside scenario to execution and weather risk rather than demand destruction.

Analyst's Notes

Subscribe to Our Channel

Stay Informed