North America’s 31% Salt Import Reliance & Logistics Failures Create 3x Winter Pricing Spreads for Domestic Supply

North America’s salt import dependence and logistics failures triggered 3x pricing spreads, increasing the value of domestic supply projects.

- US salt production reached 40Mt in 2025 with net import reliance of 31%, while no major new underground salt mine has opened in North America since 2001, increasing exposure to imported supply and logistics disruptions.

- Detroit-area spot salt prices reached approximately $300/t in early 2026 versus contracted pricing near $100/t after trucking shortages stranded imported inventory at Newark and Baltimore ports, demonstrating that delivery capacity now matters more than reserve availability during winter demand spikes.

- The Strait of Hormuz blockade pushed oil prices above $100/bbl and increased marine insurance and freight costs for bulk commodities where transport represents a material share of delivered cost.

- During the 2025-2026 winter season, 61% of sampled Northeast freshwater sites exceeded US EPA chloride thresholds, increasing environmental and compliance pressure on legacy salt operations.

- North America’s 8-10Mtpa salt import gap is increasing the value of domestic salt producers and development-stage projects located close to major end markets, particularly as freight volatility, trucking shortages, and winter supply disruptions expose the risks of long-haul imported supply.

Detroit Spot Salt Prices Reached $300/t in 2026 as Trucking Shortages Stranded Imported Supply at East Coast Ports

The 2026 North American winter produced Detroit-area spot pricing of approximately $300 per tonne against contracted rates near $100 per tonne, while thousands of tonnes of imported material remained stranded at Newark and Baltimore ports because commercial drivers were not available to move bulk corrosive cargo at the wage rates municipalities had budgeted. The USGS Mineral Commodity Summaries 2026 reported US salt production at 40 million tonnes in 2025 with net import reliance of 31% of apparent consumption, and identified Mexico (26%), Chile (23%), Canada (21%), and Egypt (6%) as the leading 2021 to 2024 import sources. The pricing dislocation occurred even though physical salt was available at port, which isolated the bottleneck to inland trucking and municipal stockpiling rather than to mine output or marine supply.

Domestic underground capacity has not expanded since American Rock Salt commissioned its New York operation in 2001, with mining capital over the past two decades flowing to lithium, copper, and gold rather than to rock salt operations averaging $54 per tonne free on board mine and plant in 2025 per USGS data. Municipal procurement operates under statutory lowest-qualified-bid requirements with annual rebidding cycles that penalize suppliers for off-season inventory carry, producing simultaneous spot-market entry by multiple jurisdictions when winter storms cluster across populated corridors. The bottleneck has shifted from reserve ownership to delivery capability, requiring assessment of trucking capacity, port proximity, and seasonal responsiveness rather than reserve size alone.

Atlas Salt Chief Executive Officer Nolan Peterson described how import exposure converts severe winters into a direct pricing tailwind for any incremental domestic supply:

“There’s actually really only upside potential in cold winters, when fuel shortages like we’re seeing now put pressure on pricing and drive prices higher, because a lot of our salt is imported.”

Fuel Shortages During Severe Winters Amplify Pricing Pressure in North America’s Import-Dependent Salt Market

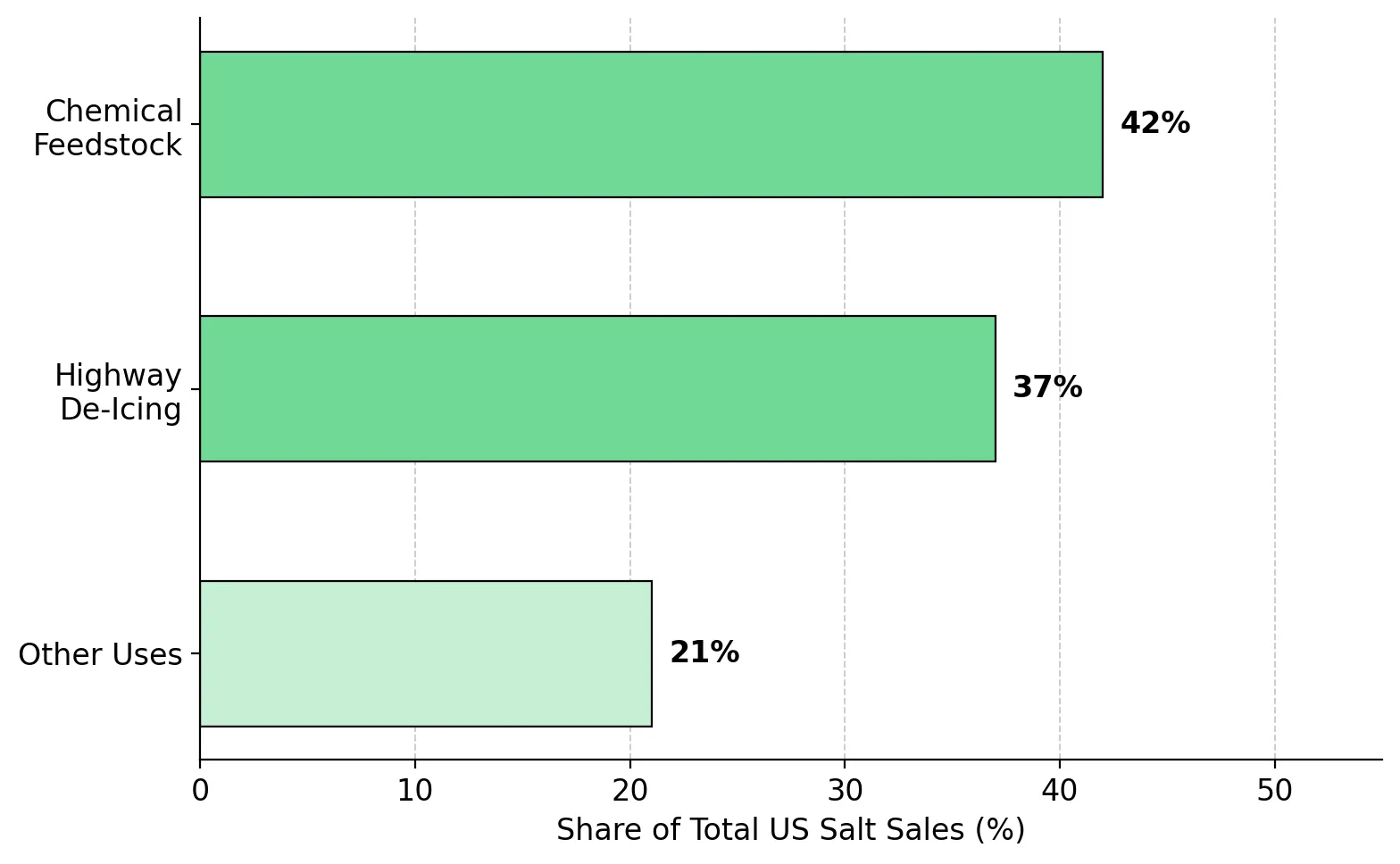

The USGS Mineral Commodity Summaries 2026 reported that chemical feedstock accounted for 42% of total US salt sales in 2025 and highway de-icing for 37%, with chlorine and caustic soda manufacturers as the dominant chemical-industry consumers and salt in brine representing approximately 90% of chemical-feedstock volume.

The chlor-alkali pathway links salt consumption to polyvinyl chloride (PVC), water treatment, paper, textiles, and broader industrial chemistry production, while the highway pathway is anchored to municipal liability exposure that converts winter procurement from a discretionary budget item into a non-discretionary obligation. Salt prices compounded at approximately 4% annually between 2000 and 2024 according to the USGS historical data, sustaining real pricing growth through multiple commodity downcycles in metals and energy.

Peterson framed the demand stability as the feature distinguishing salt from mined commodities rather than as adjacent commentary:

“You have to remember here: the primary customer for our salt is cities and governments. They are, as I’ve said before, in many cases legally obligated to purchase salt to de-ice roads for liability reasons. So this is kind of the best customer anybody could ever ask for, right? They’re forced to buy your product.”

Strait of Hormuz Blockade Increased Marine Freight & Compressed Margins for Low-Value Bulk Commodities

The US naval blockade of Iranian-linked shipping through the Strait of Hormuz pushed oil prices above $100 per barrel and disrupted the corridor that carries 20% of global oil and liquefied natural gas trade, with the International Energy Agency describing the situation as the worst global energy disruption recorded to date. The freight effect is already visible in adjacent bulk markets: S&P Global Platts assessed sulfur free on board US Gulf at $1,060 per tonne in early May 2026 against approximately $650 per tonne when the assessment launched on April 2, and assessed sulfuric acid cost and freight (CFR) US Gulf at $400 per tonne on May 6, up from $155 per tonne on February 25, 2026.

Salt economics remain materially sensitive to fuel costs, trucking rates, marine freight, and port congestion because delivered cost represents a meaningful share of selling price at US bulk rock salt averaging $54 per tonne free on board mine and plant in 2025 per USGS data. Unlike higher-value metals where freight is a rounding item in the cost structure, salt cannot absorb absolute freight inflation without margin compression, and the resulting competitive penalty falls disproportionately on long-haul import corridors. The Great Atlantic Salt Project's location approximately 2 kilometres from the Turf Point deep-water port supports less than three days of shipping to Boston per the 2025 Updated Feasibility Study, against more than 14 days of shipping for cargoes from Egypt or Chile.

The 11-day differential allows weather-responsive delivery during winter demand spikes when municipalities enter spot markets simultaneously, capturing pricing premiums of the magnitude demonstrated by the Detroit $300 per tonne reading in early 2026. Bulk commodity exposures now require regional logistics analysis, shipping-route assessment, and freight sensitivity modelling rather than reserve-based valuation alone.

North America’s 8-10Mtpa Salt Import Gap Is Increasing the Value of Domestic Development-Stage Supply

Delivered-cost economics now favor shorter shipping routes, lower trucking exposure, and cleaner permitting profiles over lowest mine-gate production cost, with the 8 to 10 million tonne annual import gap creating economic space for domestic supply located near North American end markets. Atlas Salt's 2025 Updated Feasibility Study reported probable reserves of 95 million tonnes grading 95.9% sodium chloride (NaCl) at the Great Atlantic Salt Project, with an additional inferred resource of 868 million tonnes grading 95.2% NaCl that extends potential mine life beyond 50 years at planned production rates.

The Updated Feasibility Study estimated an after-tax net present value (NPV8%) of C$920 million and an internal rate of return (IRR) of 21.3%, based on a base salt price of C$81.67 per tonne. The project would require approximately C$589 million in upfront construction capital and is projected to generate average annual free cash flow of C$188 million and average annual EBITDA of C$325 million over a 24.3-year mine life.

Atlas Salt has executed a memorandum of understanding with Scotwood Industries, the largest US distributor of packaged retail de-icing salt, targeting offtake volumes of 1.25 to 1.5 million tonnes per annum, and the Government of Newfoundland and Labrador released the project from provincial environmental assessment in April 2024 after approximately two months of review.

Higher Interest Rates & C$589M Financing Needs Remain the Main Constraint on New North American Salt Supply

The Federal Reserve effective rate reached 3.64% in 2026 with the US 10-year Treasury yield at 4.34%, raising debt cost and equity dilution risk for development-stage project financings that must close prior to construction commitment.

Infrastructure-style lenders evaluate cash flow durability, demand visibility, and reserve life on different criteria from traditional mining lenders, with implications for both cost and structure of any debt package secured. Project financing outcomes function as the principal validation event for whether the lower-risk profile management has described translates into infrastructure-style valuation frameworks rather than continuing to trade at the development-stage NAV discounts typical of cyclical mining assets.

The Investment Thesis for Salt

- North American import dependence of 8 to 10 million tonnes per annum against US 2025 production of 40 million tonnes and net import reliance of 31% per the USGS Mineral Commodity Summaries 2026 creates exposure to freight, trucking, and seasonal supply bottlenecks that can produce spot pricing multiples above contracted rates, as demonstrated by the 3x Detroit-area spread in early 2026.

- Salt demand allocation of 42% to chemical feedstock and 37% to highway de-icing per USGS data anchors consumption to non-discretionary chlor-alkali and municipal demand rather than discretionary industrial cycles, supporting more predictable utilisation and cash flow visibility than most mined commodities.

- Logistics responsiveness has become a pricing variable in its own right, shifting competitive advantage toward producers and developers with shorter shipping distances, port proximity, and integrated trucking access during the precise weather conditions when annual procurement contracts fail to deliver.

- Financing execution remains the principal residual risk variable for development-stage assets in a 3.64% Federal Reserve effective rate environment, requiring investors to monitor debt package structure, construction timelines, offtake conversion, and capex escalation sensitivity before assigning rerating probabilities.

The 2026 North American salt shortage showed that pricing power in industrial minerals can now depend more on logistics resilience than on reserve size. Detroit-area spot prices rising to approximately $300 per tonne against contracted rates near $100 per tonne reflected trucking shortages, port congestion, and import dependence rather than a lack of physical salt supply. With North America still importing 8 to 10 million tonnes annually, marine freight disruptions, higher fuel costs, and tightening environmental standards continue to increase the strategic value of domestic projects located close to end markets. The key variables have shifted toward delivered-cost positioning, shipping distance, infrastructure access, permitting durability, and financing execution, particularly for development-stage assets seeking to capture pricing premiums during seasonal supply disruptions.

TL;DR

North America’s 2026 salt shortage exposed a logistics bottleneck rather than a geological shortage, with Detroit-area spot prices rising to approximately $300/t against contracted rates near $100/t after trucking shortages stranded imported supply at East Coast ports. The region still imports 8–10Mtpa of salt despite producing 40Mt in 2025, leaving the market exposed to freight inflation, fuel disruptions, and seasonal delivery failures. Strait of Hormuz shipping disruptions further increased marine transport costs, while tightening environmental regulations raised compliance pressure on legacy operations. Against this backdrop, domestic development-stage projects with shorter shipping distances, advanced permitting, and lower-emission operations, including Atlas Salt, may gain strategic value as municipalities prioritize supply reliability and delivered-cost security over lowest mine-gate production cost alone.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

%20(1).png)

Stay Informed