Hormuz Energy Shock & 3x Salt Price Spikes Improve Pricing Power for Domestic Producers

Hormuz disruption and rising freight costs drove 3x North American salt price spikes, improving pricing power for domestic suppliers.

- The US Energy Information Administration's May 2026 Short-Term Energy Outlook assumes the Strait of Hormuz remains closed until late May, removing 10.5 million barrels per day of Gulf crude supply and increasing Asian power prices. That directly pressures chlor-alkali producer margins, where electricity accounts for more than 40% of total production cost.

- The World Bank's April 2026 Commodity Markets Outlook forecasts 2026 energy prices to rise 24%, overall commodities 16%, and aluminum 22%, increasing chlor-alkali production costs across Asia. That raises input costs for import-dependent salt consumers and strengthens pricing leverage for domestic salt suppliers.

- The USGS Mineral Commodity Summaries 2026 estimates US salt production at 40 million tons in 2025 against an annual import gap of 8 to 10 million tons, leaving the market 31% reliant on imports. During regional winter shortages, that dependence has driven spot salt prices to as much as three times contracted pricing.

- Salt prices compounded at approximately 4% annually between 2000 and 2024, according to USGS Salt Statistics, maintaining pricing growth through multiple metals and energy downcycles. That stability can cause conventional mining net present value models to undervalue long-life salt assets that assume flat real pricing.

- Development-stage North American salt projects positioned within the US 31% import gap trade at valuations more typical of cyclical mining assets despite stable demand.

The International Monetary Fund's April 2026 World Economic Outlook lowered its 2026 global growth forecast to 3.1% from the Fund's pre-conflict 3.4% projection following the expansion of the Middle East conflict. The IMF projects inflation to rise in 2026 before moderating in 2027, with the strongest price pressures concentrated in emerging-market commodity importers exposed to higher energy and freight costs. The EIA's May 2026 Short-Term Energy Outlook assumes Strait of Hormuz traffic remains below pre-conflict levels through late 2026, sustaining upward pressure on global energy and industrial feedstock costs.

Recent macro commentary has focused primarily on crude oil, natural gas, aluminum, and fertilizer markets because Middle East supply disruptions directly affect their production and transport costs. Salt is exposed to the same energy-driven cost inflation because chlor-alkali production depends heavily on electricity and industrial feedstocks. 42% of US salt demand comes from the chlor-alkali industry, which uses brine electrolysis to produce chlorine and caustic soda, while another 37% comes from highway de-icing. Salt brine represents roughly 90% of chlor-alkali feedstock volume, making salt supply and power costs central to industry margins. PVC is the largest chlorine end-market, linking salt demand to construction and water-infrastructure spending.

The more important difference is between import-dependent salt consumers facing higher energy and freight costs and domestic salt producers that can benefit from tighter regional supply and stronger pricing. Data from the USGS, IMF, World Bank, IEA, and EIA indicate that energy-driven increases in industrial input costs are tightening the salt market faster than current equity valuations imply.

Hormuz Energy Shock Raises Chlor-Alkali Costs & Reshapes Global Salt Demand

The chlor-alkali industry is simultaneously exposed to higher energy costs and tightening regional trade flows. Because electricity represents a major share of chlor-alkali production costs, higher regional power prices are widening the cost advantage of domestic salt supply chains. Higher electricity, freight, and industrial input costs are already increasing chlor-alkali operating costs, creating upward pressure on salt term-contract pricing.

Electricity Represents More Than 40% of Chlor-Alkali Production Cost

According to IEA Electricity 2026, electricity accounts for more than 40% of chlor-alkali production costs. The IEA also reports that 2025 EU electricity prices for energy-intensive industries averaged more than twice US levels and nearly 50% above China, with the gap largely unchanged from 2024. Higher oil and gas prices increase industrial electricity costs, raising chlor-alkali operating expenses and reducing plant utilization rates. Lower utilization reduces brine consumption and weakens salt demand for higher-cost marginal producers. Each ton of caustic soda production consumes approximately 1.4 to 1.8 tons of salt, directly linking chemical-plant operating rates to salt demand.

Higher Energy Costs & Weak PVC Pricing Pressure Asian Chlor-Alkali Margins

Asian chlor-alkali producers are facing margin pressure from higher ethylene costs and weaker downstream PVC pricing. US caustic soda prices fell 21.41% across the four quarters of 2025, indicating chlor-alkali margins were already weakening before the Hormuz disruption increased energy costs. China National Salt Industry and Tata Chemicals Ltd. remain key industrial salt suppliers to Northeast and South Asian chlor-alkali plants. Adani Group's 2,200-ton-per-day Mundra chlor-alkali project and DCM Shriram's Gujarat expansion are expected to increase regional industrial salt demand beginning in 2027. Each ton of PVC production consumes roughly 0.58 tons of chlorine, helping sustain chlor-alkali plant utilization and salt demand even when caustic soda prices weaken.

European Chlor-Alkali Closures Reduce Long-Term Industrial Salt Demand

Europe represents the weakest major regional market for industrial salt demand because high power costs are reducing chlor-alkali operating capacity. European chlor-alkali plant closures in 2025 reduced regional industrial salt demand and may become permanent if elevated electricity costs persist. Each ton of European caustic soda capacity removes approximately 1.4 to 1.8 tons of annual salt demand. K+S Aktiengesellschaft is among the European salt producers most exposed to declining regional chlor-alkali demand, increasing the risk of weaker long-term volume growth.

North America's 31% Salt Import Gap Favors Domestic Producers and Developers

North America provides the clearest example of how higher energy and freight costs can benefit domestic salt developers positioned inside a supply-constrained market. USGS data shows the US remains dependent on imported salt, while new domestic mine supply requires long permitting and construction timelines.

USGS Data Shows the US Salt Market Remains 31% Import Dependent

USGS Mineral Commodity Summaries 2026 reports US salt production of 40 million tons in 2025, 39 million tons of sales, total market value of $2.6 billion, and net import reliance of 31%. North America has added little new underground salt production capacity for decades, limiting supply growth and increasing the risk of sharp regional price spikes during periods of stronger demand or supply disruption. 42% of US salt demand comes from chemical feedstock and 37% from highway de-icing, placing 79% of consumption in essential end markets.

Logistics Bottlenecks Drove North American Salt Spot Prices to 3x Contract Rates

Regional market analysis using USGS data has shown Detroit-area winter salt spot prices reaching approximately three times contracted pricing during periods of supply stress. Freight constraints, trucking shortages, and seasonal port bottlenecks amplify those price spikes in import-dependent markets. Strait of Hormuz disruption, higher bunker fuel costs, and longer shipping routes through the Suez and Panama corridors are increasingly delivering salt import costs ahead of the 2026 North American stocking cycle. Spot prices reflect immediate market purchases, while contract prices are typically negotiated through multi-year supply agreements with committed volumes. A widening gap between spot and contract pricing indicates tightening salt supply conditions, and that spread has increased in recent North American markets.

Atlas Salt's Newfoundland Project Targets North America's 31% Import Gap

Atlas Salt Inc. is advancing the feasibility-stage Great Atlantic Salt Project in St. George's, Newfoundland and Labrador, targeting the North American de-icing salt market. The company completed its 2025 Updated Feasibility Study, secured environmental approval, and began site preparation in February 2026. Final regulatory conditions were cleared on April 30, 2026, and an expanded memorandum of understanding with Sandvik Mining covers approximately $132 million of equipment and services. The project is targeting North American road de-icing salt demand and has not yet entered production.

Nolan Peterson, Chief Executive Officer of Atlas Salt Inc., describes why municipal road-salt procurement creates stable long-term demand for domestic North American suppliers:

“The primary customer for our salt is cities and governments. And they are, in many cases, legally obligated to purchase salt to de-ice roads for liability reasons.”

Because 79% of US salt demand comes from chemical feedstock and highway de-icing, according to the USGS, domestic suppliers positioned within the country's 31% import gap may benefit from more stable long-term demand and pricing.

Salt Prices Compounded at 4% Through Commodity Downcycles

USGS pricing data shows salt prices have remained comparatively stable through multiple commodity downcycles, unlike many bulk mined commodities. That pricing stability can support higher long-term cash-flow assumptions and lower cyclicality risk for salt producers and developers.

A 25-Year USGS Price Series Supports Stable Long-Term Salt Valuations

US salt prices compounded at approximately 4% annually between 2000 and 2024. During the same period, gold, copper, and nickel each experienced multi-year price declines tied to commodity downcycles. Salt prices continued compounding through those commodity downturns. Because the pricing trend is based on a 25-year USGS government data series rather than a forward forecast, it provides a historical basis for using more stable long-term pricing assumptions in salt valuations.

Municipal De-Icing and Chlor-Alkali Demand Support Stable Salt Pricing

State and provincial highway safety requirements make road salt purchases mandatory for many municipalities, supporting stable de-icing demand regardless of economic conditions. Chlor-alkali demand is diversified across PVC, water treatment, paper, textiles, and aluminum refining, reducing the impact of weakness in any single end market. That diversified and non-discretionary demand base has supported sustained salt price growth through multiple metals and energy downturns.

Conventional Mining Valuation Models May Undervalue Salt Developers

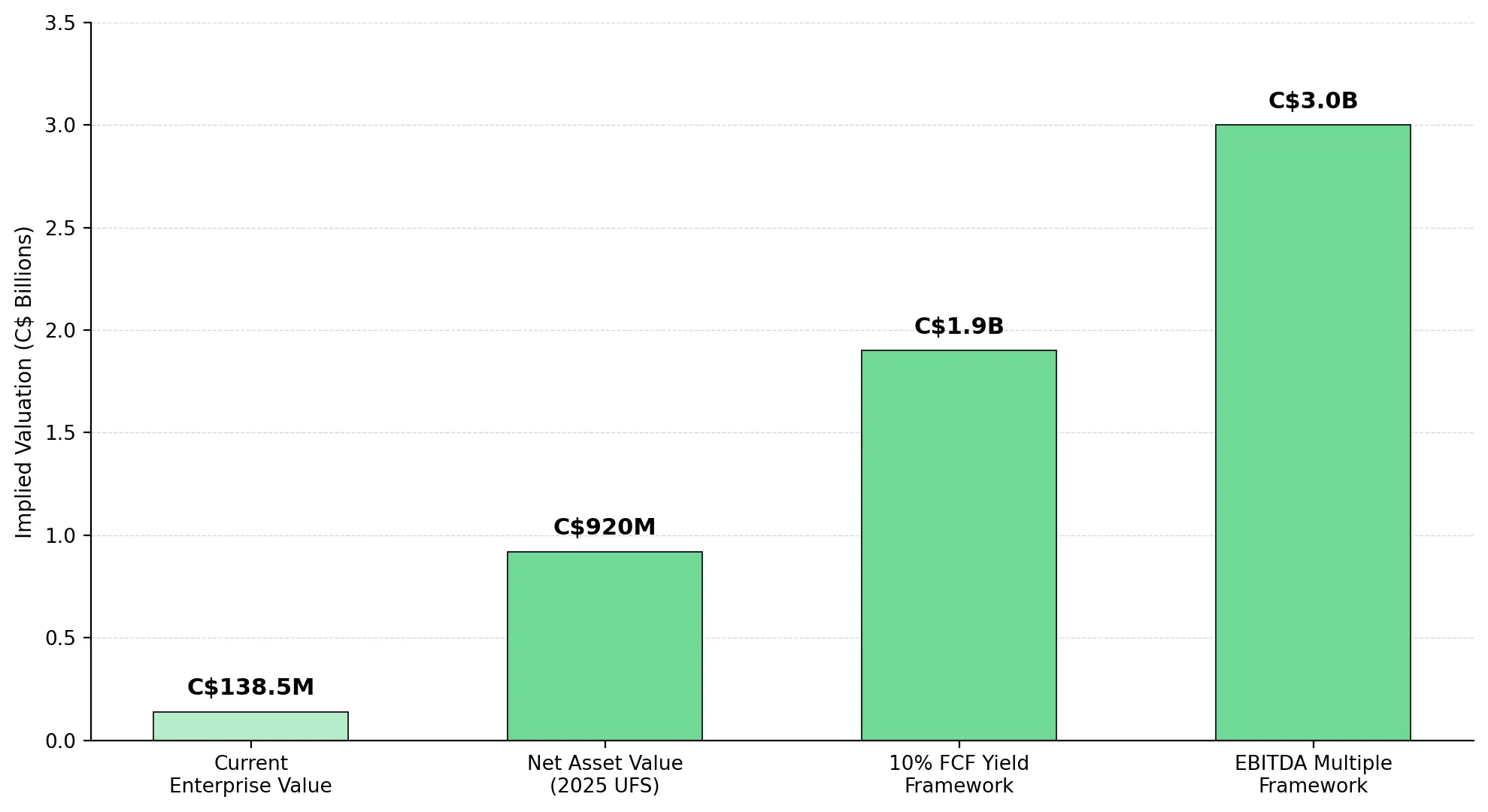

Atlas Salt's 2025 Updated Feasibility Study reports a net asset value of C$920 million, life-of-mine average annual free cash flow of C$188 million at a base salt price of C$81.67 per tonne, average annual EBITDA of C$325 million, and pre-production capital expenditure of C$589 million.

Applying a 10% free cash flow yield implies a valuation of approximately C$1.9 billion. Applying EBITDA multiples in line with publicly traded salt producers implies a valuation of approximately C$3 billion.

India's Pre-Monsoon Export Window Tightens as Asian Chlor-Alkali Demand Expands

Gujarat accounts for approximately 87% of Indian salt output, with Tamil Nadu and Rajasthan producing most of the remainder. India's June monsoon season limits additional solar salt production for roughly three months, forcing many Q3 export volumes to be contracted with Northeast Asian and African buyers before May ends. USGS-validated trade data shows India ranked as the world's largest salt exporter with 14.4 million tons of exports in both 2023 and 2024. Asian salt markets are entering their seasonal June-to-July supply tightening period as Hormuz disruption increases energy costs for regional chlor-alkali producers.

China commissioned 1.9 million tons of new PVC capacity in 2025, lifting fourth-quarter output to 6.54 million tons and increasing chlorine demand by roughly 3.8 million tons. India's 2.8 million-ton PVC supply deficit is driving 1.5 million tons of new chlor-alkali capacity additions at Dahej and Cuddalore. Adani Group's Mundra chlor-alkali project and DCM Shriram's Gujarat expansion are expected to increase industrial salt demand beginning in 2027. Southeast Asian joint ventures are scheduled to add another 1 million tons of PVC capacity by 2027, increasing regional chlorine and salt demand. Each ton of PVC production consumes roughly 0.58 tons of chlorine, supporting chlor-alkali plant utilization and salt demand even when caustic soda prices weaken. These chlor-alkali and PVC capacity additions are increasing long-term industrial salt demand across Asia.

The Investment Thesis for Salt

- Higher energy and shipping costs are increasing the delivered price of imported salt across North America, improving the competitive position of domestic producers and permitted development-stage projects with lower transportation exposure.

- Non-discretionary demand from highway de-icing and chemical feedstock has supported the roughly 4% annual salt price growth reported by the USGS between 2000 and 2024. Investors should evaluate whether salt developers are still being valued using cyclical mining assumptions despite salt's comparatively stable long-term pricing record.

- Permitted feasibility-stage mining projects typically carry lower technical risk than earlier-stage development assets because metallurgical, geological, and permitting work has already been completed. In those cases, project financing and construction execution become the primary remaining risks.

- Asian PVC capacity expansion is increasing long-term industrial salt demand and supporting multi-year supply contracts for Asian and Indian solar-salt producers. Producers in Gujarat benefit because most annual output is generated during the region's dry season before the June monsoon.

- European chlor-alkali and salt producers face rising long-term demand risk because persistent high electricity costs continue to drive capacity closures. Investors with concentrated European exposure should evaluate whether current valuations fully reflect the risk of further plant retirements.

Two near-term catalysts for the salt market are the EIA's mid-month Short-Term Energy Outlook revision on Strait of Hormuz reopening assumptions and the World Bank's June 2, 2026 Commodity Markets update. A Strait of Hormuz reopening delay into July could increase Asian chlor-alkali operating costs by approximately 8% to 12% and reduce Q3 brine demand by an estimated 600 to 900 kilotons. That would further disrupt regional salt trade flows ahead of the Northern Hemisphere winter stocking season. Investors evaluating salt equities should distinguish between cyclical mining valuation models and infrastructure-style cash-flow frameworks supported by salt's long-term pricing history. Development-stage projects still carry financing and construction risk, and salt equities remain exposed to broader mining-sector and macroeconomic conditions.

TL;DR

The Strait of Hormuz disruption is raising global energy, freight, and industrial input costs, increasing chlor-alkali production expenses and tightening salt markets across North America and Asia. Because the US remains structurally dependent on imported salt and domestic supply growth has been limited for decades, regional shortages have already driven spot salt prices to as much as three times contracted pricing. At the same time, USGS data shows salt prices compounded at roughly 4% annually between 2000 and 2024 despite multiple commodity downturns, suggesting long-life salt assets may behave more like infrastructure-style cash-flow businesses than cyclical mining projects.

FAQs (AI Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed