Energy Security Mandates & Digital Power Demand Reprice Uranium Toward Multi-Year Highs

Uranium futures hit $89.25/lb in January 2026 as energy security mandates and AI data center demand drive structural repricing. Policy shifts and supply chain bifurcation favor producers in Tier-1 jurisdictions.

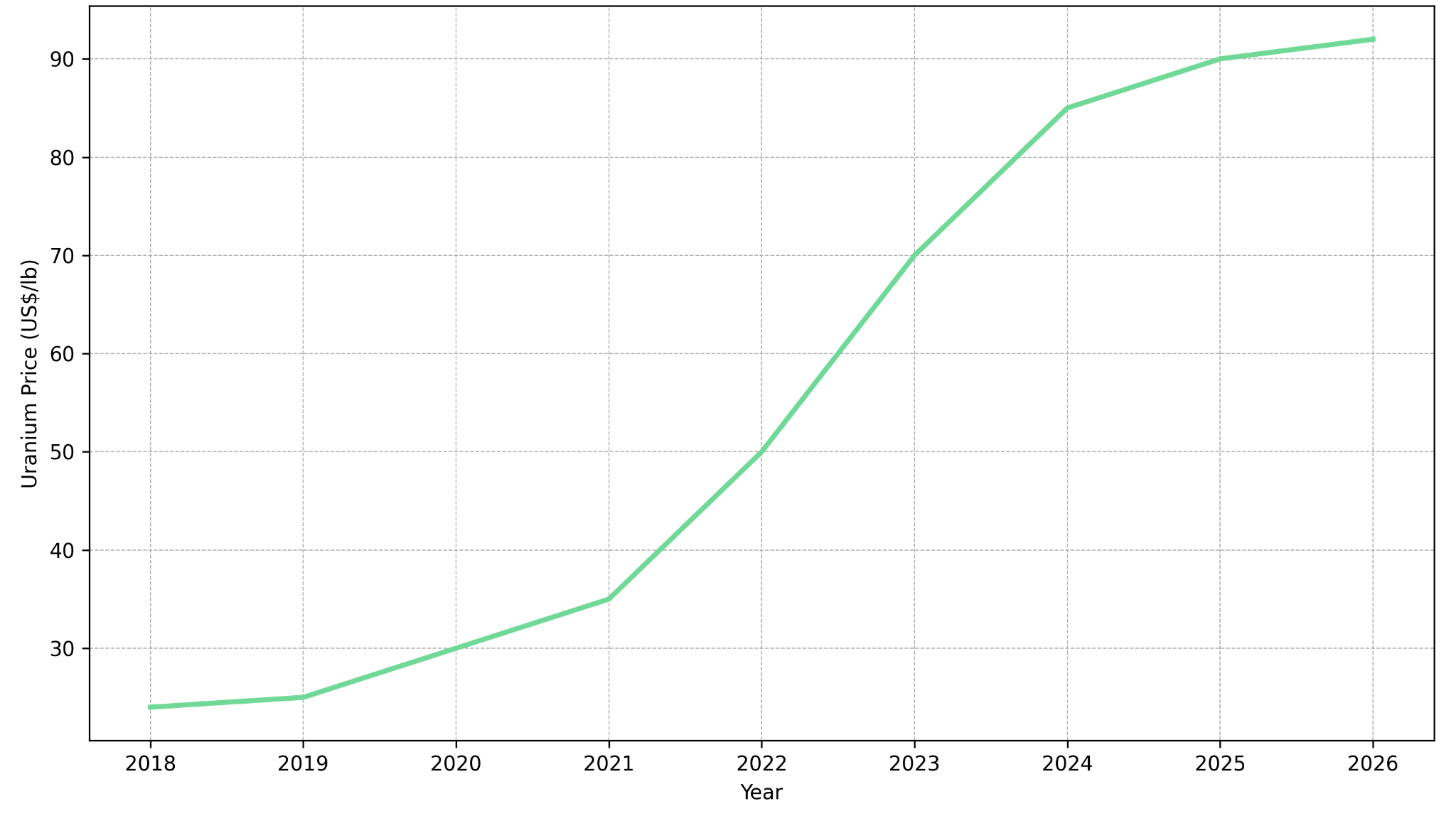

- Uranium futures reached US$89.25/lb in late January 2026, marking a multi-year high and signaling a repricing cycle driven by structural demand rather than cyclical scarcity.

- Energy security policy and AI-driven electricity demand are converging, shifting nuclear power from a legacy baseload solution to a strategic infrastructure asset.

- Sanctions on Russian nuclear fuel have accelerated supply-chain bifurcation, forcing Western governments to fast-track domestic conversion, enrichment, and production capacity through legislation including the Nuclear Fuel Supply Act.

- Institutional capital flows, including physical uranium funds, suggest growing confidence in sustained price support above prior cost-curve thresholds.

- Select uranium producers, developers, and explorers with Tier-1 jurisdictions, permitting visibility, and scalable assets are positioned to benefit from higher long-term incentive pricing.

A Demand Shift Redefines Nuclear's Role in the Energy Space

Uranium's recent move toward US$90/lb reflects more than tightening supply. It marks a structural re-rating of nuclear energy within global power systems. Governments across North America, Europe, and Asia are increasingly prioritizing energy security, grid stability, and decarbonization simultaneously. The confluence of these priorities has elevated nuclear from a legacy baseload option to a central pillar of long-term energy strategy.

The rapid expansion of AI-driven data centers has introduced a parallel demand shock that exposes the limitations of intermittent renewables. Technology companies require consistent, high-capacity electricity supply to power computing infrastructure that operates continuously. Nuclear power, with its baseload reliability and low carbon intensity, is being repositioned as a strategic complement rather than a transitional asset in the global energy transition.

This shift reframes uranium demand from cyclical restocking toward long-duration infrastructure planning. Utilities are extending contract horizons and increasing uncovered demand projections. The implications extend to long-term pricing dynamics, development economics, and capital allocation across the uranium value chain.

Policy, Sanctions & the Bifurcation of Uranium Supply Chains

Geopolitical realignment has become a central driver of uranium pricing dynamics. Sanctions and restrictions on Russian nuclear fuel have disrupted legacy supply chains, forcing Western nations to decouple from state-linked enrichment and conversion services. This bifurcation creates structural inefficiencies that benefit producers operating in allied jurisdictions while raising risk premiums for projects exposed to sanctioned counterparties.

In response to these supply chain vulnerabilities, the United States government has committed substantial capital toward domestic nuclear fuel capacity. The Nuclear Fuel Supply Act represents a bipartisan commitment of US$2.7 billion to fund domestic production of low-enriched uranium and high-assay low-enriched uranium to offset Russian supply dependence. Regulatory reforms aim to reduce permitting friction for converters, enrichers, and uranium producers.

This policy backdrop materially alters project timelines, capital access, and risk premiums. Institutional valuation models increasingly embed regulatory alignment as a primary screening criterion. Producers with permitting visibility and jurisdictional clarity command valuation premiums relative to peers facing extended approval processes or geopolitical exposure.

Federal permitting reforms are accelerating development timelines for domestic producers. William Sheriff, Executive Chairman of enCore Energy, describes the regulatory environment:

"Our South Dakota project got Fast-41 designated by the federal government, which was a welcome sign... It gives you a more certain and more acceptable timeline to get through all of your filings."

enCore's Dewey Burdock ISR Uranium Project received Fast-41 designation in August 2025, exemplifying how policy support is shortening permitting timelines for compliant domestic projects.

Uranium Price Action Signals a Shift in Market Expectations

Uranium futures trading near US$90/lb represents a technical and psychological inflection point. Prices are now at levels that support new mine development economics, particularly for in-situ recovery operations and high-grade conventional deposits. The current price environment sits below the 2007 peak of approximately US$140/lb but substantially above the decade-long trough that constrained development activity through the 2010s.

With macro models forecasting prices toward US$93.75/lb over the next twelve months, investors are reassessing long-term incentive pricing in light of higher capital costs and development constraints. This price environment improves net present value sensitivity for near-production assets while enhancing optionality for high-grade producers and developers.

Producers with low-cost operations are positioned to capture margin expansion at current price levels. Mark Chalmers, Chief Executive Officer of Energy Fuels, quantifies the operating leverage:

"Our costs at Pinyon are between $23 to $30 per pound. If you're selling at $75 a pound plus, you've got a really nice margin... That's a lot of cash coming into the company."

Institutional Capital Flows Reinforce the Uranium Repricing Narrative

Beyond spot price action, capital allocation trends reinforce uranium's structural thesis. Physical uranium funds have accumulated material volumes, signaling confidence in long-term demand rather than short-term trading momentum. These funds remove supply from the spot market while providing transparent inventory data that influences price expectations.

The participation of long-only capital reduces downside volatility and anchors price expectations at levels that support development economics. The growingAllocation to uranium equities and physical holdings may suggest that the commodity is transitioning from a niche allocation to an infrastructure theme within diversified portfolios.

Access to institutional capital at favorable terms reflects growing confidence in the uranium sector. William Sheriff describes the financing environment:

"The cost of capital is something we've never seen before in terms of a five and a half percent coupon on a non-secured note... It really opened an amazing number of doors to a completely new level of capital."

Operational Leverage Across the Uranium Value Chain

The uranium value chain presents differentiated risk-return profiles across production, development, and exploration stages. Each segment offers distinct exposure to the current repricing cycle, with asset quality, jurisdictional alignment, and operational readiness determining relative positioning.

Producers & Near-Term Cash Flow Visibility

United States-based producers utilizing in-situ recovery methods benefit from low all-in sustaining cost profiles and rapid scalability. ISR operations require lower capital than conventional mining while offering flexibility to modulate production in response to price signals. enCore Energy operates three licensed ISR central processing plants in South Texas, with Alta Mesa currently running at 60 percent of its one-million-pound annual configuration and accelerated drilling expected to increase utilization.

Energy Fuels has shown integration advantages through domestic milling capacity and diversified critical minerals positioning. The company operates White Mesa Mill, the only conventional uranium processing facility currently operating in the United States, with licensed capacity exceeding eight million pounds of U3O8 annually.

Vertical integration across the nuclear fuel cycle creates competitive advantages that extend beyond uranium production. Mark Chalmers describes the strategic positioning:

"We are like no other company in the critical mineral space where we're building a critical mineral hub using our longstanding uranium processing capabilities but also the ability to mine and recover rare earths into oxides."

Energy Fuels secured US$700 million through an oversubscribed convertible senior notes offering in October 2025, providing capital for expansion while the company advances commercial production of heavy rare earth oxides targeting later in 2026.

Developers Positioned for Higher Incentive Pricing

Advanced projects with defined internal rates of return and clear permitting pathways gain valuation leverage as long-term price assumptions rise. Policy support shortens development timelines and improves financing conditions for projects in Tier-1 jurisdictions.

IsoEnergy represents the development stage opportunity, with its Tony M project in Utah providing near-term production visibility through toll milling agreements with White Mesa Mill. The company's 2,000-ton bulk sampling program is currently underway with completion expected in April 2026, demonstrating how developers can accelerate cash flow generation by leveraging existing processing capacity.

Philip Williams, Chief Executive Officer of IsoEnergy, describes the strategic advantage:

"We're doing a bulk sample which really just represents a small-scale mining exercise. We're taking about 2,000 tons out of the mine, sending it down the road to the White Mesa Mill for processing... It's the only operable conventional uranium mill in the United States today... It's an asset for us that we can leverage very quickly."

The company is also advancing a winter 2026 drill program of approximately 5,200 meters at its Larocque East project, targeting the high-grade Hurricane deposit in Saskatchewan's Athabasca Basin.

High-Grade Exploration as Strategic Optionality

High-grade discoveries in Tier-1 jurisdictions provide embedded leverage to sustained uranium demand growth. Exploration assets offer asymmetric return potential for investors willing to accept development timeline uncertainty in exchange for exposure to resource expansion and discovery economics.

ATHA Energy exemplifies how grade intensity and district-scale land positions create scarcity value within constrained supply systems. The company's Angilak Project in Nunavut, located within the Angikuni Basin approximately 225 kilometers southwest of Baker Lake, provides exploration optionality across a geological analogue to the Athabasca Basin. The 2024 exploration program achieved a 100 percent hit rate, with all 12 holes testing the unconformity intersecting mineralization and all 13 holes testing parallel structures discovering new uranium lenses.

Troy Boisjoli, Chief Executive Officer of ATHA Energy, describes the asset quality:

"We have full control over the Angikuni basin... I view it as being analogous to exploring in the northeast Athabasca basin circa 1965, pre-major discoveries... We're in control of an entire district that has us in a very good position of strength relative to the market and relative to our strategic opportunities."

Risk Considerations & Market Sensitivities

While the macro backdrop is constructive, uranium equities remain sensitive to factors that could alter the supply-demand trajectory or development economics. Investors should differentiate between price exposure and execution capability, prioritizing balance-sheet strength, jurisdictional alignment, and operational readiness when constructing uranium allocations.

- Policy reversals or permitting delays that extend development timelines beyond current projections

- Commodity price volatility affecting contract timing and margin capture for producers

- Capital cost inflation impacting development economics and project feasibility thresholds

The Investment Thesis for Uranium

The uranium sector presents a differentiated opportunity set characterized by structural demand visibility, policy alignment, and improving price incentives.

- Structural demand visibility derives from energy security mandates and digital infrastructure growth that support long-term baseload electricity requirements independent of short-term commodity cycles.

- Policy alignment through regulatory easing and government funding, including the US$2.7 billion Nuclear Fuel Supply Act, reduces development risk in allied jurisdictions while creating barriers to entry for projects in non-aligned regions.

- Price incentive restoration with futures approaching US$90/lb supports levels required to sanction new supply and enables positive development economics for permitted projects.

- Operational leverage allows producers and ISR operators to benefit from margin expansion while high-grade explorers offer asymmetric upside through discovery potential and resource growth.

- Institutional validation through physical fund accumulation reinforces downside support and improves liquidity across the uranium equity complex.

Uranium prices at multi-year highs reflect changing government policies on nuclear power and growing demand from energy-intensive industries. Multiple factors are converging: renewed support for nuclear energy in climate policy frameworks, increasing electricity requirements from data centers and AI infrastructure, and larger institutional investors entering the sector. These conditions are shifting uranium from a commodity subject primarily to short-term supply-demand cycles toward a material with longer-term strategic importance in energy infrastructure.

For investors evaluating uranium exposure, several factors appear critical to company performance: the quality and size of uranium deposits, political and regulatory stability in operating jurisdictions, and how close projects are to actual production. Companies with these characteristics may be better positioned as the sector continues to evolve.

TL;DR

Uranium prices reached multi-year highs near $90/lb, driven by converging forces: government energy security mandates, AI-driven electricity demand, and sanctions-induced supply chain disruption. The $2.7 billion Nuclear Fuel Supply Act and Fast-41 permitting reforms are accelerating domestic production timelines. Institutional capital flows into physical uranium funds signal confidence in sustained pricing above development cost thresholds. Producers with low-cost ISR operations, developers with permitting visibility, and high-grade explorers in allied jurisdictions are positioned to capture operational leverage as uranium transitions from cyclical commodity to strategic infrastructure asset within long-term energy planning frameworks.

FAQs (AI-Generated)

Uranium futures reached $89.25/lb due to structural demand from energy security policies and AI data center electricity requirements, combined with supply chain disruptions from Russian sanctions. The Nuclear Fuel Supply Act's $2.7 billion commitment to domestic enrichment capacity is accelerating Western supply chain development.

Sanctions have forced supply chain bifurcation, creating inefficiencies that benefit producers in allied jurisdictions while raising risk premiums for projects with sanctioned counterparty exposure. This geopolitical realignment drives policy support for domestic production and accelerates permitting timelines.

Fast-41 is a federal permitting designation that provides uranium projects with more certain approval timelines. enCore Energy's Dewey Burdock project received this designation in August 2025, exemplifying how regulatory reforms are shortening development timelines for domestic producers.

AI-driven data centers require continuous, high-capacity baseload electricity that intermittent renewables cannot reliably provide. Nuclear power's 24/7 reliability positions it as strategic infrastructure for technology companies, creating parallel demand alongside traditional utility requirements.

Producers offer near-term cash flow and margin expansion at current prices; developers provide leverage to higher long-term pricing assumptions with defined project economics; explorers offer asymmetric upside through discovery potential but carry greater development timeline uncertainty.

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed