Fed Policy Favors Funded Uranium Companies as Term Prices Reach US$91.50 per Pound

Fed policy may pressure uranium equities, but term prices at US$91.50/lb continue to reflect utility demand and supply constraints.

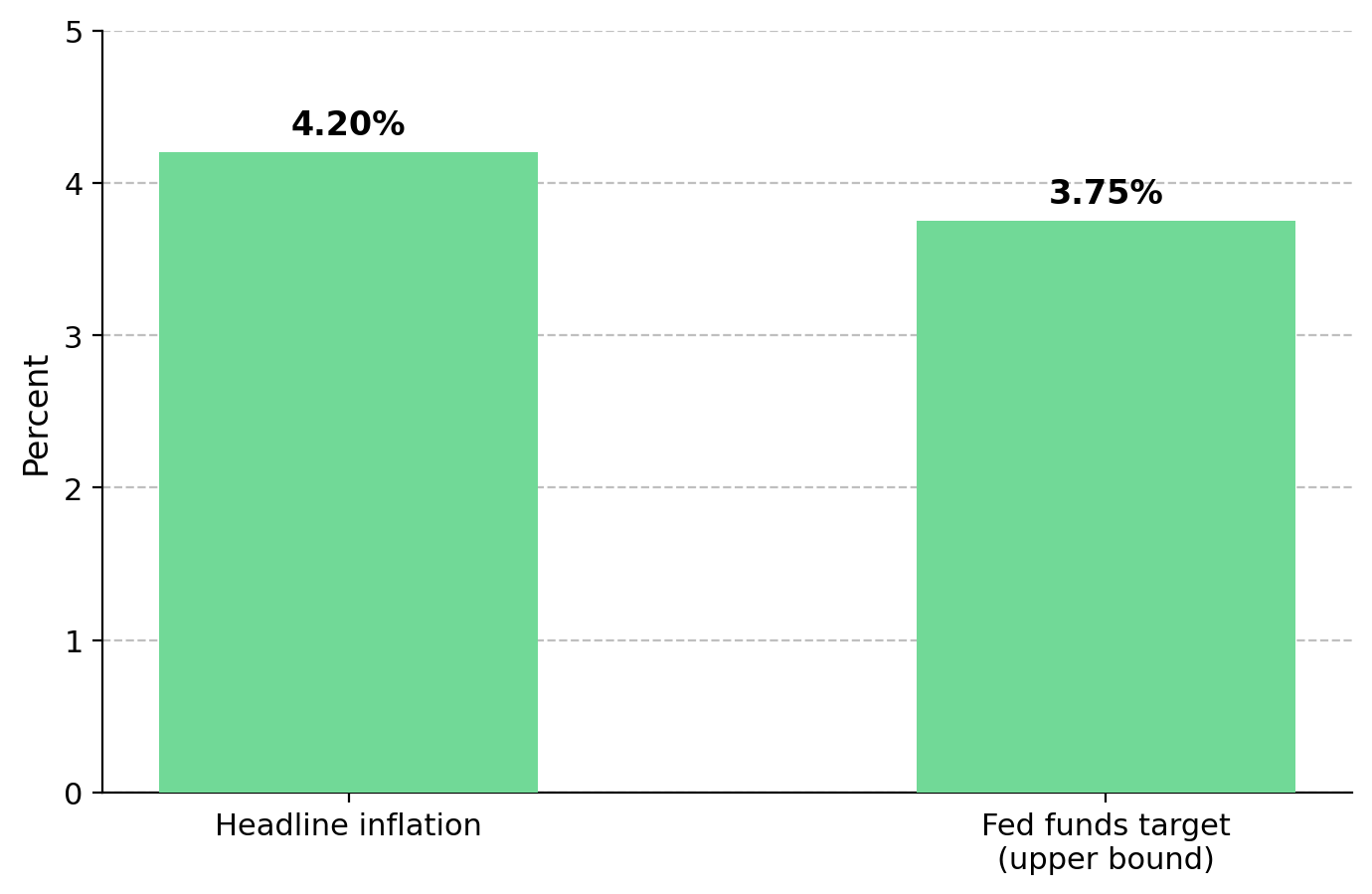

- The June 17 Federal Open Market Committee meeting, the first chaired by Kevin Warsh, is the key macro event for uranium equities, with markets pricing no change to the 3.50-3.75% target range but watching for signals that future rate cuts may be delayed as inflation remains near 4.2%.

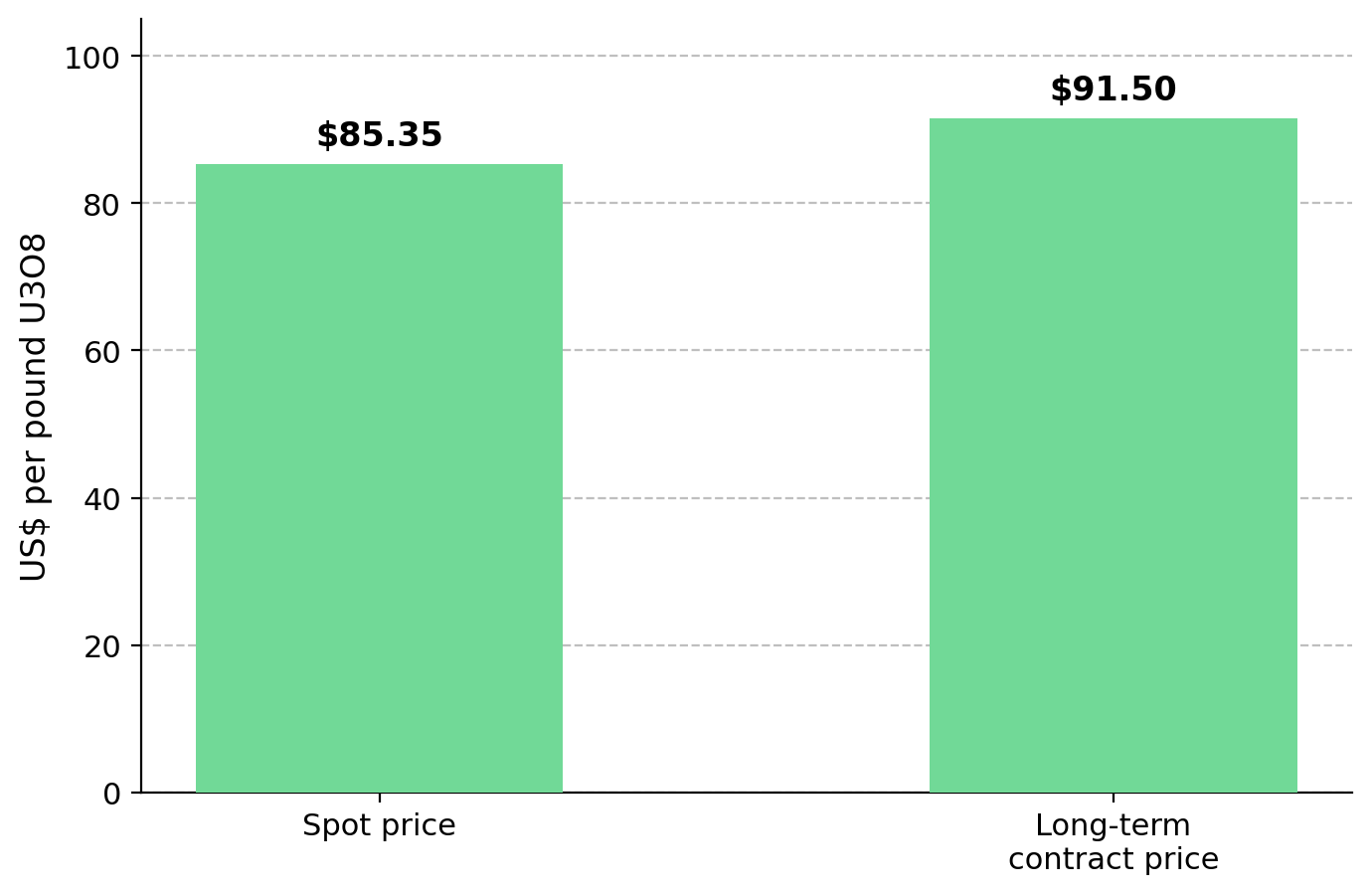

- Uranium's spot price near US$85 to US$86 per pound remains below the long-term contract price of about US$91.50 per pound, the highest level since 2012, indicating utilities are paying more to secure future supply than immediate delivery.

- Monetary policy affects uranium equities and financial buyers through the dollar and real interest rates, while physical uranium supply and utility demand are driven primarily by production and contracting decisions.

- A higher-for-longer rate path raises the cost of capital, giving funded companies an advantage over peers that may need to issue equity or raise debt to advance projects.

- In a higher-rate environment, low-cost producers and companies with funded balance sheets face less financing and margin risk than peers that depend on higher uranium prices or new capital raises.

Fed Policy Drives Uranium Equities More Than Near-Term Supply News

The Federal Open Market Committee meets on June 16 and 17 in its first meeting, chaired by Kevin Warsh. Markets assign little probability to a change in the 3.50 to 3.75% target range, making the committee's projected interest-rate path the key variable for uranium investors. Signals that rates will remain elevated would affect the dollar, real interest rates, and the cost of capital, which are likely to have a greater near-term effect on uranium equities than drilling results.

The uranium spot price was US$85.35 per pound on June 12, up roughly 22% from a year earlier. The long-term contract price reached about US$91.50 per pound, its highest level since 2012. The contract price remaining above the spot price indicates utilities are willing to pay a premium to secure future uranium supply, supporting the physical market despite short-term monetary uncertainty.

Inflation near 4.2% and a still-firm labor market support keeping interest rates elevated, making the committee's guidance as important as its rate decision. Monetary policy affects uranium equities through the dollar, real interest rates, and the cost of capital, while uranium supply and utility contracting are driven primarily by production and procurement decisions. As a result, funded and low-cost companies are better positioned than peers that depend on rising uranium prices or external financing.

The Dollar, Real Rates, & Capital Costs Are the Fed's Transmission Channels

Because uranium is priced in US dollars, expectations for higher US interest rates can strengthen the dollar and raise the effective cost of uranium for non-US utilities. The impact is greater in the spot market because long-term uranium contracts are negotiated years in advance and are less sensitive to short-term currency movements.

Higher real yields raise the opportunity cost of holding physical uranium, reducing the attractiveness of vehicles such as the Sprott Physical Uranium Trust, whose purchases have supported spot uranium prices. Higher real interest rates could reduce demand from financial buyers and pressure uranium equity valuations even if uranium supply and utility demand remain unchanged.

A higher-for-longer rate path raises discount rates and the cost of equity, reducing the value of projects that are years away from generating cash flow. Funded companies gain an advantage because the same drill result or feasibility study creates less shareholder value when capital is expensive and difficult to raise.

Utility Contracting & Producer Discipline Support Long-Term Uranium Prices

While uranium equities react to monetary policy, long-term uranium prices are driven primarily by utility contracting and producer supply decisions. The term price near US$91.50 per pound reflects a multi-year contracting cycle rather than short-term changes in interest-rate expectations. Kazatomprom, the world's largest uranium producer, has guided 2026 output of 27,500 to 29,000 tonnes, or roughly 71.5 to 75.4 million pounds, under a value-over-volume strategy that prioritizes price over production growth. Cameco is maintaining full-year guidance of 29 to 32 million pounds at a realized price of US$85 to US$89 per pound, supported by a contract portfolio of about 230 million pounds. Together, these production and contracting commitments support long-term uranium pricing regardless of short-term changes in monetary policy.

Energy Fuels expects to produce roughly 1.6 million pounds of finished uranium oxide by June 30, placing it within its full-year guidance range of 1.5 to 2.5 million pounds after six months. Production at that scale depends on ore grades, mill availability, and contracts rather than changes in the fed funds rate. Mark Chalmers, Chief Executive Officer of Energy Fuels, highlights the operational scale required to bring new uranium supply to market:

"We processed 350,000 pounds in one month at the mill in December. That's significant when many others in the US are trying to reach 100,000 pounds in a quarter. We know how to produce uranium."

Higher Interest Rates Reward Funded Balance Sheets in Uranium

When capital is expensive, companies that can fund multi-year programs internally face less financing and dilution risk. Financing and dilution risk increase as interest rates remain elevated, making funded companies more resilient than unfunded peers across the development spectrum.

Funded Explorers Face Less Dilution Risk When Capital Tightens

Explorers are the most sensitive to the cost of capital because they are pre-revenue and depend on equity financing to fund drilling. ATHA Energy illustrates how a funded balance sheet can reduce financing risk. A C$63 million financing completed in February 2026 fully funds ATHA's largest program to date at Angilak, including about 20,000 meters of drilling across three mineralized corridors using three rigs. A multi-year cash runway reduces the need to issue shares into a weak market, lowering dilution risk as financing conditions tighten. No resource has yet been defined at Angilak, so the investment case remains tied to exploration success rather than project economics. Troy Boisjoli, Chief Executive Officer of ATHA Energy, explains why uranium supply uncertainty increases the value of large-scale exploration projects:

"We have the ability to execute on a project that has tremendous scale potential at a time in the uranium sector when the vast majority of the risk is on the supply side and there is supply-side uncertainty."

Strong Balance Sheets Allow Developers to Wait for Better Uranium Prices

For developers, a strong balance sheet reduces financing constraints, allowing contracting decisions to be made with greater regard to market conditions. IsoEnergy holds roughly C$130 million and no debt, allowing it to evaluate a restart of the past-producing Tony M mine without committing to contracts required by lenders. Restarting a permitted, past-producing mine requires less upfront capital than a greenfield project, while the absence of debt removes lender requirements that can force pre-sales. Philip Williams, Chief Executive Officer of IsoEnergy, explains why near-term production capacity increases exposure to rising uranium prices:

"There are other producers and companies that are restarting, but generally in our market-cap range there are not many of them. We want to be one of those producers and be able to deliver material into a rapidly rising uranium price environment, which we think is coming in the US."

Lower valuations can reduce downside risk when capital remains expensive. Atomic Eagle trades near A$3 per pound of resource, compared with roughly A$5 to A$7 for Australian-listed uranium peers. Its 2025 feasibility study outlines a post-tax net present value of US$243 million at an 8% discount rate, a 20.8% IRR, and operating costs of about US$32.20 per pound, with the program fully funded. Phil Hoskins, Chief Executive Officer of Atomic Eagle, explains how projected uranium supply deficits could increase the need for new mine development:

"For the first time since the 1960s, reactors are going to be dependent on new supply coming out of the ground toward the end of this decade. That deficit, around 30 million pounds, is going to need to be rectified from uranium coming out of the ground."

These metrics help determine how project valuations change as interest rates remain elevated. A higher-for-longer rate environment raises discount rates, reducing the value of capital-intensive projects and increasing the advantage of companies that can defer financing.

Production Costs Determine Margin Resilience in a Higher-Rate Environment

Low-cost producers are better positioned to maintain margins if higher US interest rates strengthen the dollar. enCore Energy produced uranium at US$46.43 per pound in the first quarter of 2026, compared with US$78.82 per pound for material purchased from third parties, supporting higher margins as self-produced volumes increased. William Sheriff, Executive Chairman of enCore Energy, explains how production delays can tighten uranium supply and support higher prices:

"If they're unable to deliver, that becomes a short. That becomes upward pressure on the market price. It can come back to haunt producers if they can't deliver on time."

Fed Policy Moves Uranium Valuations, Not Uranium Supply

Monetary policy affects uranium valuations, but not uranium supply or utility demand. Interest rates influence the cost of capital, the dollar, and real interest rates, which affect uranium equity valuations. They do not determine reactor construction, utility contracting, or the location of uranium mining and enrichment, which drive long-term uranium demand and supply. A term price near US$91.50 per pound versus a spot price near US$85 to US$86 per pound indicates utilities are paying more to secure future supply than immediate delivery.

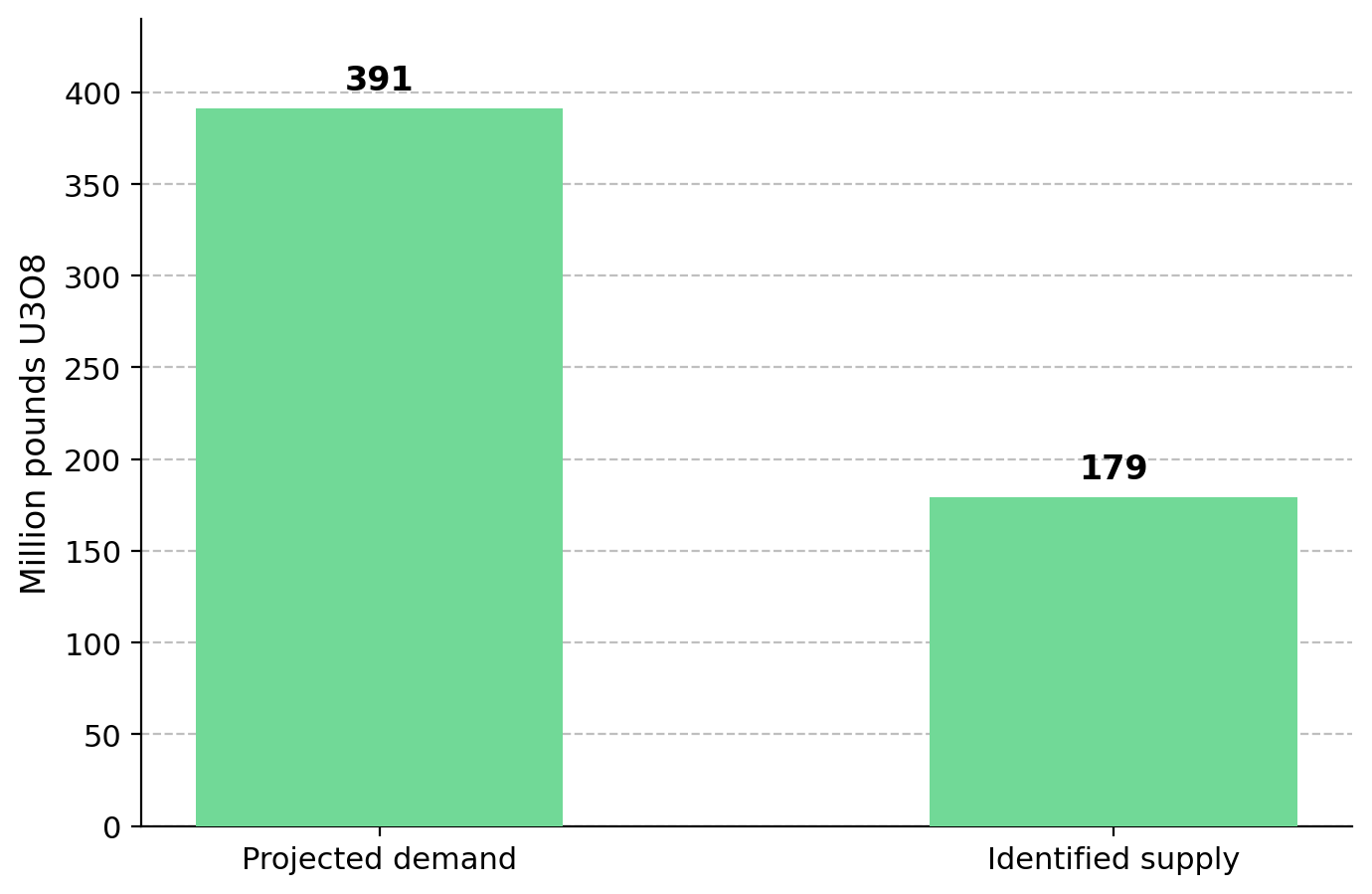

Projected reactor demand exceeds identified supply through 2040, uranium production remains concentrated among a small number of producers, and Western buyers are reducing reliance on Russian enrichment. US policy supports uranium demand through reactor restart programs and domestic enrichment investment. Lower geopolitical risk in the Middle East reduced the energy-security premium but did not change projected uranium supply deficits. Elevated interest rates can pressure uranium valuations, but a term price above spot indicates utilities remain focused on securing future supply, favoring companies with strong balance sheets and credible production plans.

The Investment Thesis for Uranium

- A term price near US$91.50 per pound reflects a multi-year contracting cycle driven by utility procurement and producer supply discipline, making uranium demand less sensitive to a single central bank decision.

- Uranium equities are more sensitive to monetary policy than the physical uranium market because higher expected interest rates can strengthen the dollar, raise real interest rates, and reduce financial demand that supports spot uranium prices.

- Funded explorers carry lower financing risk because a multi-year cash runway allows them to advance drilling programs without issuing equity into a weak market.

- Debt-free developers can time mine restarts and uranium contracts around market conditions rather than lender requirements that can force early sales at lower prices.

- A valuation discount combined with a fully funded development program can reduce downside risk for companies with strong feasibility-stage economics if capital remains expensive.

- Low-cost producers are better positioned to maintain margins if a stronger dollar or higher real interest rates pressure uranium prices.

- Financing costs, dilution risk, and project execution remain the principal risks to uranium equities despite strong balance sheets and low operating costs.

The June 17 Fed decision is likely to influence uranium equity valuations through the dollar, real interest rates, and the cost of capital. It is far less likely to alter the supply and demand balance reflected in a term uranium price near US$91.50 per pound and a contracting cycle that continues to reward new production. The key question is not whether uranium remains necessary, but which companies can advance projects, add production, and avoid dilution if financing conditions remain tight. In a higher-rate environment, funded balance sheets, competitive operating costs, and credible paths to production are likely to matter more than uranium price exposure alone.

TL;DR

The June 17 Fed meeting is the key near-term macro event for uranium investors because changes in policy expectations can affect the dollar, real interest rates, and the cost of capital. While these factors influence uranium equity valuations, the physical uranium market remains supported by utility contracting and constrained supply. A term uranium price of about US$91.50 per pound, the highest since 2012, suggests utilities are still securing long-term supply despite economic uncertainty. The article argues that funded explorers, debt-free developers, and low-cost producers are better positioned to advance projects, avoid dilution, and preserve margins if financing conditions remain restrictive. The central investment question is not whether uranium demand remains intact, but which companies can execute without relying on favorable capital markets.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed