Geopolitical Conflicts and Critical Minerals: Why Supply Security Is Driving Repricing

Critical minerals are being repriced as geopolitics drives supply security, boosting Western projects and reshaping valuations beyond traditional cost curves.

- Geopolitical competition, export controls, and resource nationalism are systematically bifurcating critical mineral markets into Western-aligned and China-aligned supply tracks.

- China's vertically integrated model creates systemic dependency. China controls the majority of global refining capacity for rare earths, lithium, and cobalt, exposing Western industrial supply chains to policy-driven disruption at any point in the value chain.

- Government capital is actively de-risking development-stage assets. Export credit agencies, development finance institutions, and strategic reserve programs are compressing the cost of capital for projects in allied jurisdictions, reshaping project-level return profiles.

- Nickel, uranium, and rare earths are being repriced as strategic instruments. Jurisdictional alignment, carbon intensity, and processing capability have become primary valuation inputs alongside grade and scale.

- Developers with Tier-1 assets and near-term catalysts are positioned for valuation re-rating. Canada Nickel, Lifezone Metals, and Energy Fuels represent distinct but complementary exposure points along this structural shift.

From Globalization to Fragmentation

Global commodity markets are being reshaped by geopolitics rather than traditional demand cycles. Critical minerals, nickel, lithium, rare earths, uranium, and cobalt, now sit at the center of energy transition policy, industrial strategy, and national security. As a result, pricing is no longer driven purely by cost curves or demand, but increasingly by jurisdiction, processing capability, and geopolitical risk.

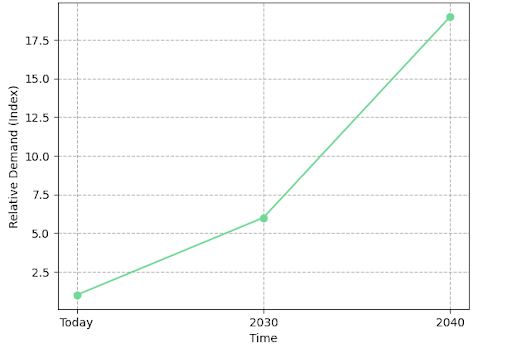

The International Energy Agency forecasts a sixfold increase in demand for critical minerals by 2040, yet supply remains constrained and highly concentrated. This imbalance is creating a structural premium for projects in stable, Western-aligned jurisdictions that offer greater execution certainty.

The market is now bifurcated: low-cost but geopolitically exposed supply (e.g., Indonesia, China, DRC) versus higher-cost but strategically secure supply in North America and allied regions. Investors who focus on cost alone risk mispricing this structural shift.

Supply Chain Concentration & Systemic Vulnerability

Critical mineral supply chains remain highly concentrated. China dominates rare earth processing, the DRC leads cobalt production, and nickel refining is heavily centered in Indonesia and China.

This creates systemic risk: even targeted export controls, like China’s restrictions on gallium and germanium, can disrupt key processing stages. As a result, Western manufacturers are now prioritizing supply security, committing capital to alternative sources that were previously uneconomic.

China's Capital Strategy & the Global Reordering of Resource Control

China's dominance in critical minerals is the result of a multi-decade, state-coordinated capital deployment strategy that integrates resource acquisition, in-country processing, infrastructure development, and long-term offtake agreements into a single industrial model. Since 2023, China has deployed an estimated $120 billion into upstream mining and processing assets globally, with particular concentration in Africa, Southeast Asia, and Latin America.

This model has moved decisively beyond the traditional extract-and-export framework. Chinese state-owned enterprises and affiliated private capital are now building full value chain infrastructure in host nations, often bundling project financing with infrastructure investment to align with host government development priorities. The result is a competitive moat that is difficult to replicate through market mechanisms alone, which is precisely why Western governments have concluded that market mechanisms alone will not be sufficient

The Shift Toward In-Country Processing & Resource Nationalism

Resource nationalism is accelerating the reconfiguration of global supply chains. Zimbabwe banned raw lithium exports in 2022, requiring domestic processing before export. Indonesia extended its nickel ore export ban in 2020, creating a competitive moat for domestic downstream investment that has since attracted hundreds of billions in Chinese-backed smelter and battery precursor capacity. The Democratic Republic of Congo has introduced progressive export taxes on copper and cobalt concentrates, signaling a policy trajectory toward mandatory in-country beneficiation.

Lifezone Metals' Chief Financial Officer Ingo Hofmaier has articulated the strategic exposure that Western governments are seeking to mitigate, framing the dependency risk in terms that institutional investors are increasingly factoring into allocation decisions:

“You wouldn’t want Western governments to end up in a situation where dependency on Indonesia continues to grow unchecked.”

For Western developers, resource nationalism raises costs and complexity, but can reduce competition from Chinese exporters. Those with strong technology or aligned host-country partnerships are best positioned to benefit.

Strategic Capital Replaces Market Capital

Capital allocation in mining is shifting from return-driven investment to strategic funding, as governments and export credit agencies step in to finance development-stage critical mineral projects aligned with supply chain priorities. Institutions like the US Department of Energy, Export Development Canada, and the US EXIM Bank is deploying long-tenor, below-market capital, not as philanthropy, but as industrial policy. A clear example is Canada Nickel’s Crawford Project, where up to $500 million in EDC financing significantly de-risks the asset, lowers the cost of capital, and helps attract broader institutional investment.

Canada Nickel's Chief Executive Officer Mark Selby has been direct about the distinction between this project's policy alignment and the broader pipeline of competing developments:

“We’re the only project in Canada that has both federal and provincial endorsement.”

The broader implication for investors is that cost of capital is becoming jurisdiction-dependent, not just project-dependent. A development-stage nickel sulphide project in Ontario with federal endorsement, permitting clarity, and strategic investor support trades at a fundamentally different cost structure than a comparable asset in a jurisdiction without those attributes, regardless of whether the underlying grade or resource size is similar.

Cost of Capital, Permitting & Timeline Visibility

Projects in Tier-1 jurisdictions benefit from lower financing costs, higher valuation multiples, and stronger institutional interest. In Ontario, the One Project, One Process framework is accelerating permitting timelines, improving development visibility and reducing execution risk. This is reflected in its strong global ranking on the Fraser Institute’s Policy Perception Index.

Investors are increasingly prioritizing execution certainty over grade or scale. Lower-grade projects with clear paths to FID can command higher risk-adjusted valuations than higher-grade assets facing permitting uncertainty, driving multiple expansion for well-positioned developers.

Nickel Markets as a Case Study in Strategic Repricing

Nickel prices have declined since 2023 as Indonesian supply, backed by Chinese capital - expanded faster than demand, increasing availability of lower-cost Class 2 nickel and compressing margins for higher-cost producers. This masks a structural constraint: battery applications require Class 1 nickel, where supply growth is slower due to reliance on sulfide deposits or capital-intensive processing such as HPAL. IEA scenarios indicate strong demand growth from clean energy through 2040, but the imbalance is compositional, Class 2 surplus does not resolve Class 1 scarcity, shifting price formation toward battery-grade availability rather than aggregate supply.

Indonesia has shifted the cost curve by banning ore exports and forcing in-country processing, enabling large-scale, lower-cost integrated supply. In contrast, Western projects face longer permitting timelines, higher capital intensity, and stricter ESG constraints, limiting near-term supply growth. As a result, marginal supply is increasingly determined by jurisdiction and processing capability, concentrating pricing power in producers able to deliver Class 1 nickel at scale. This shifts nickel from a volume-driven trade to a supply-quality and jurisdiction-driven allocation decision.

Large-Scale, Low-Cost Western Supply

Canada Nickel’s Crawford Project in Ontario is one of the largest undeveloped nickel sulphide resources globally, with an NPV of ~$2.8B, IRR of 17.6%, and first-quartile costs (~$0.39/lb Ni), alongside a 40+ year mine life. It has attracted strategic investors including Agnico Eagle, Samsung SDI, and Anglo American, reflecting strong supply chain alignment.

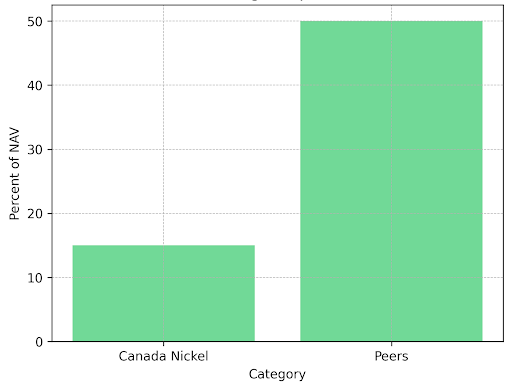

The project is advancing toward a 2026 construction decision, yet the company trades at ~15% of NAV versus ~50% for comparable development-stage peers. This discount reflects execution risk, but also highlights the potential for a significant re-rating as permitting and financing milestones are achieved.

By-Product Economics as Structural Cost Advantage

Sovereign Metals’ Kasiya project demonstrates how deposit characteristics and co-product recovery can structurally compress operating costs and reposition an asset at the low end of the global cost curve. Unlike conventional graphite projects that rely on standalone economics, Kasiya’s graphite is produced as a by-product of a primary rutile operation, materially reducing incremental cost exposure and decoupling margins from prevailing graphite price cycles.

Sovereign Metals’ Chairman Ben Stoikovich has articulated this advantage in terms of cost-curve positioning and margin durability:

“Our incremental cost to produce a ton of graphite as a byproduct will be just $241 per ton, placing us at the very bottom of the global cost curve.”

This cost structure is driven by geology and process design rather than cyclical inputs. Soft, free-dig saprolite mineralization eliminates drilling, blasting, and energy-intensive comminution, while by-product recovery reduces the effective cost allocation to graphite, enabling sustained margins even in oversupplied markets. The investment implication is that cost leadership in critical minerals can be engineered through integrated project design, with assets combining low-energy processing and co-product economics positioned to maintain profitability across cycles and attract long-duration strategic capital.

High-Grade Nickel & Processing Innovation

Lifezone Metals’ Kabanga Project in Tanzania offers a differentiated risk-return profile driven by resource quality and strong economics. With an average grade of ~1.98% nickel, an NPV of $1.58B, IRR of 23.3%, and AISC of ~$3.36/lb, Kabanga is one of the highest-grade undeveloped nickel sulphide deposits globally. Its high-grade nature also supports greater debt capacity, reducing equity dilution risk.

Beyond the resource, Lifezone’s proprietary Hydromet technology enables lower-emission processing by eliminating traditional smelting, producing battery-grade nickel, copper, and cobalt. This positions Kabanga as a clean, vertically integrated supply solution aligned with Western battery supply chains, with a final investment decision targeted for mid-2026.

The Strategic Premium on Domestic Supply

Beyond nickel, uranium and rare earths are also undergoing a structural re-rating driven by energy security, nuclear resurgence, and defense-related demand. Despite geographically diverse mining, downstream processing remains heavily concentrated in China, creating similar supply chain vulnerabilities.

The uranium market is now in a sustained supply deficit, with reactor demand (~180M lbs/year) exceeding primary mine supply (~140M lbs/year). While secondary sources fill part of the gap, utilities are increasingly securing primary supply from allied jurisdictions to reduce reliance on Kazakh and Russian-linked sources.

United States Processing Advantage & Strategic Optionality

Energy Fuels occupies a unique position in the United States critical minerals supply chain. As the largest domestic uranium producer, the company operates the White Mesa Mill in Utah, the only conventional uranium processing mill currently operating in the United States. This infrastructure position is not easily replicated, requires multi-year permitting to establish from scratch, and creates a capital-light expansion platform for adjacent critical mineral processing.

Chief Executive Officer Mark Chalmers has articulated the integration logic that underpins Energy Fuels' strategy, framing the competitive challenge in terms of value chain completeness:

“To truly compete with China, you need every step in place, missing even one in the middle isn’t an option.”

Energy Fuels has extended White Mesa's capabilities into rare earth element processing, accepting monazite sands, a rare earth-bearing mineral, and producing a partially separated rare earth carbonate as an intermediate product for downstream separation. The company is advancing toward fully separated rare earth oxides, which would represent the highest-value processing step currently absent from United States domestic supply chains.

ESG, Jurisdiction & the Emerging Valuation Premium

Investor frameworks for critical minerals are evolving beyond traditional metrics like grade, resource classification, and NPV. Institutional capital now incorporates factors such as jurisdictional risk, carbon intensity, regulatory transparency, and downstream integration alongside financial returns.

This shift is especially important in nickel, rare earths, and uranium, where end-users are imposing strict supply chain standards. Regulations like the EU Battery Regulation are embedding ESG requirements into market access, meaning projects with low emissions, stable jurisdictions, and transparent supply chains are better positioned to secure capital and offtake agreements.

The Investment Thesis for Critical Minerals

- Supply chain security is now a primary pricing driver, with Western governments deploying capital to de-risk projects and lower cost of capital beyond traditional market levels.

- Tier-1 North American jurisdictions command valuation premiums through permitting reform, regulatory clarity, and export credit support.

- High-grade sulphide assets, such as Lifezone’s Kabanga, offer strong debt capacity, reducing dilution risk and enabling FID without relying on higher commodity prices.

- Integrated processing provides defensibility and margin upside independent of raw commodity pricing.

- Near-term catalysts, FID, permitting, and financing, represent key re-rating events for developers trading at deep NAV discounts.

- Producers with existing infrastructure gain immediate leverage to policy-driven demand with capital-light expansion potential.

- ESG alignment and low carbon intensity are becoming required for market access, particularly in Western battery supply chains.

- District-scale upside adds long-term optionality not fully reflected in current valuations.

Western governments have shifted from voluntary offtake preferences to binding procurement policy. The US Inflation Reduction Act, EU Critical Raw Materials Act, and Canada’s Critical Minerals Strategy impose domestic processing and allied-nation sourcing requirements that directly determine project eligibility for government-backed financing. This shift is visible in capital flows: IEA data shows critical mineral investment reached $320 billion in 2023, up 38% year-over-year, with most directed toward IRA- and CRMA-compliant jurisdictions.

Institutional criteria now extend beyond AISC and NPV. Geopolitical alignment, supply chain positioning, and regulatory track record increasingly determine financing access and the discount rate applied to future cash flows. Companies with government endorsement, policy-linked offtake, or proprietary processing capacity secure a lower cost of capital than non-compliant peers.

TL;DR

Geopolitics is reshaping critical mineral markets, shifting pricing from cost-driven fundamentals to supply chain security, jurisdiction, and policy alignment. China’s dominance in processing and resource nationalism has exposed systemic vulnerabilities, prompting Western governments to deploy capital and accelerate permitting to secure alternative supply. This is creating a bifurcated market where Western-aligned projects, such as Canada Nickel, Lifezone Metals, and Energy Fuels, are positioned for structural re-rating as financing, policy support, and ESG requirements increasingly drive valuation.

FAQs (AI generated)

Critical minerals are being repriced because supply security has become as important as cost. Governments now view these commodities as strategic assets tied to energy transition, defense, and industrial policy, shifting valuation toward jurisdiction, ESG compliance, and processing capability rather than just grade or scale.

China dominates refining and downstream processing across key minerals, creating dependency risks for Western supply chains. Its vertically integrated model allows control over multiple stages of production, meaning disruptions can occur even without restricting raw material exports.

Governments are deploying capital through export credit agencies and development finance institutions to fund projects in allied jurisdictions. This lowers the cost of capital, reduces development risk, and accelerates timelines, effectively reshaping project economics beyond traditional market forces.

Projects in stable jurisdictions benefit from clearer permitting, policy support, and access to strategic capital. Investors now prioritize execution certainty and supply chain alignment, leading to higher valuations for projects that meet these criteria despite potentially higher costs.

Investors must shift from cyclical commodity thinking to structural allocation. The key opportunity lies in identifying assets aligned with geopolitical priorities, strong jurisdictional positioning, and near-term catalysts, as these are most likely to benefit from ongoing re-rating.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

%20(1).jpg)

Stay Informed