How ISR Uranium Projects Scale Production 1 Wellfield at a Time

How ISR uranium producers scale output through modular wellfields, satellite IX plants, and phased expansion while managing permitting and growth risks.

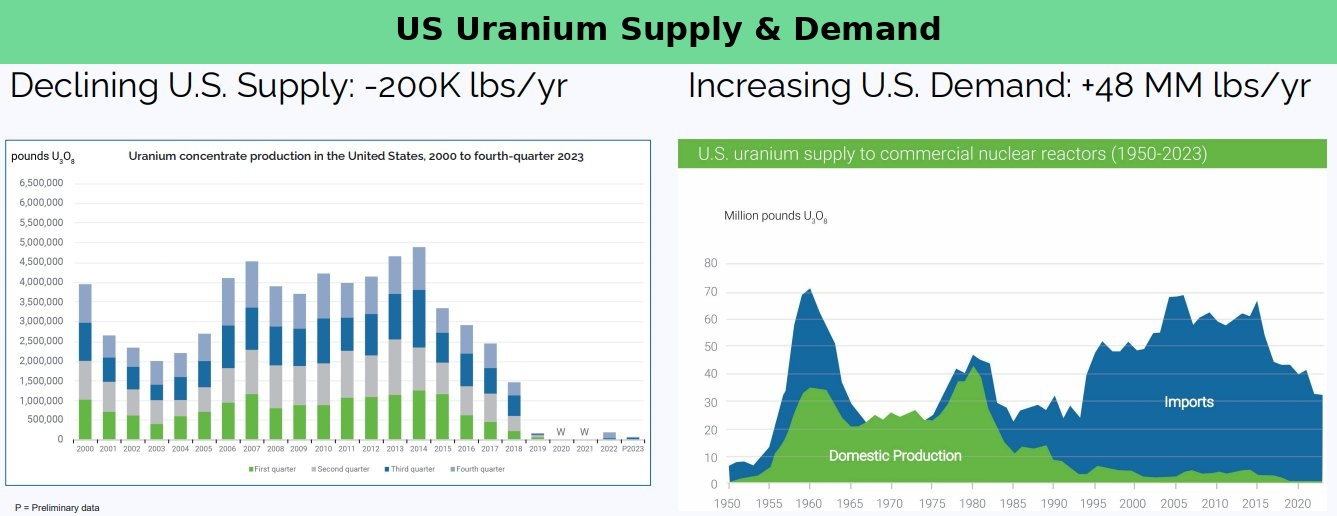

- US uranium demand is increasing at 48 million pounds per year, while domestic supply is declining at approximately 200,000 pounds per year, widening the gap that ISR producers must close, according to US Energy Information Administration (EIA) data through the Fourth Quarter of 2023.

- enCore Energy completed construction of the first phase of the Upper Spring Creek satellite ion exchange (IX) plant in South Texas on June 4, 2026, with a full flow capacity of 3,200 gallons per minute (gpm) targeted by the end of July 2026 across 4 modular wellfield units.

- The satellite IX model allocates fixed processing costs across multiple wellfields that feed a single licensed central processing plant (CPP), allowing producers to add production capacity without constructing new central plant infrastructure at each site.

- The permit gap between construction completion and first production remains the primary risk variable in ISR scaling, with Upper Spring Creek's production start targeted for late 2026 pending final regulatory approvals.

- ISR producers with annual output below approximately 1 million pounds face a structural ceiling on access to institutional capital and utility contract terms, making consolidation a financial necessity rather than an optional strategy.

Why ISR Scales Differently

In conventional hard-rock mining, production capacity is largely determined at the point of construction: a mill is built, a pit is opened, and output is fixed to that infrastructure until the next major capital cycle. In-situ recovery (ISR) uranium production works differently. Its modular wellfield architecture allows operators to add capacity in defined increments, each tied to a discrete unit of infrastructure rather than a single large plant. That structural characteristic, which gives ISR its reputation for capital efficiency and environmental compatibility, also defines its production-scaling logic and constraints.

The distinction matters as US domestic uranium production runs well below historic levels at a time when demand is growing. US uranium demand is increasing at a rate of 48 million pounds per year, while domestic supply is declining at approximately 200,000 pounds per year, based on US Energy Information Administration (EIA) data through the Fourth Quarter of 2023. That divergence places a premium on operators who can bring new production online efficiently.

The completion of construction at enCore Energy Corp.'s (NASDAQ: EU | TSXV: EU) Upper Spring Creek ISR Uranium Project in South Texas, announced June 4, 2026, illustrates both the mechanics of ISR scaling and the regulatory dependencies that govern its pace.

Industry Context

ISR uranium extraction, a process with more than 50 years of commercial history in the US, works by injecting a lixiviant (groundwater mixed with oxygen) into a uranium-bearing sandstone formation, dissolving the uranium in place, and pumping the uranium-bearing solution to the surface for processing. The process eliminates the need for conventional excavation and produces a surface footprint that is a fraction of that required by open-pit or underground operations.

The ion exchange (IX) system is at the heart of the surface infrastructure. In a satellite IX configuration, a modular plant positioned near the wellfield captures uranium onto resin beads, and the loaded resin is then transported to a central processing plant (CPP) for final processing into uranium concentrate, commonly known as yellowcake. The satellite approach allows producers to operate across multiple geographically dispersed wellfields without constructing a full CPP at each site, reducing capital requirements per production unit.

Because each wellfield module represents a discrete increment of flow capacity and uranium output, the actual rate at which a project reaches its nameplate capacity depends on how quickly modules can be drilled, connected, and brought online. Regulatory approvals, including aquifer exemptions and injection permits, govern the timeline at each step, creating a permit-dependent gap between construction completion and production commencement.

Emerging Practices & Industry Progress

The Upper Spring Creek project illustrates the modular approach in concrete terms. As disclosed in enCore's June 4, 2026, news release, the first phase of the satellite IX plant was constructed with a flow capacity of 1,600 gallons per minute (gpm), representing 50% of the facility's planned total throughput. The plant's capacity is being expanded in staged increments: 75% of total flow capacity is targeted for completion before the end of June 2026, with full capacity of 3,200 gpm targeted by the end of July 2026.

The wellfield build-out follows the same modular cadence. Drilling for the first 800-gpm module is complete, and wellfield infrastructure for that module is nearly finished. Drilling for Module 2 is approximately 90% complete, with activities also underway for 2 additional 800-gpm modules. Each module represents a discrete production unit, and the 4-module structure maps directly onto the plant's planned full capacity.

Because each module can be brought into service as soon as its wellfield infrastructure is ready and permits are in hand, operators do not need to fund the full capital cost of the production system before generating any cash flow. The satellite IX plant's short installation time, the ability to relocate the equipment to support additional uranium recovery elsewhere in a district, and the absence of major permanent infrastructure at each satellite site all reduce the per-pound cost of adding production capacity. The company describes the Upper Spring Creek plant as the largest satellite facility it has ever built.

Remaining Challenges

The gap between construction completion and first production is the most consequential operational challenge in ISR scaling. At Upper Spring Creek, construction of the first production wellfield is nearly complete, but uranium extraction cannot begin until final permits are received. The production start is targeted for late 2026, contingent on regulatory clearance.

ISR projects across US jurisdictions face multi-layered permitting processes that include aquifer exemption approvals and wellfield authorisations, each administered on timelines that operators cannot fully control. The Upper Spring Creek project benefits from permits originally issued by a prior operator, Signal Equities LLC, before low uranium prices led that company to halt operations. enCore acquired the project in December 2020 and has built upon those existing permit foundations, but the final production authorisations remain pending.

Scale introduces its own challenges at the corporate level. Executive Chairman of enCore Energy Corp., William M. Sheriff, was direct about the production threshold required to compete for institutional capital:

"In the ISR business, you're going to need to have some producers that produce more than a million pounds a year, or you're going to be essentially running a mom and pop grocery store on the corner. Your credit ratings go up, so your cost of capital goes down. Your ability to deal on more favourable terms with your customers at the nuclear utilities is going to increase as a larger-scale company."

That constraint applies across the ISR sector. Smaller US producers targeting sub-million-pound annual output face a structural ceiling on their access to institutional capital and utility contract terms unless they pursue consolidation.

enCore Energy in South Texas

The Upper Spring Creek ISR Uranium Project is a 100% enCore-owned asset located within the historic Clay West uranium district in South Texas. The uranium-mineralised sands lie within the Oakville Formation at depths between 300 and 450 feet below the surface. The mineralised trend extends approximately 120 miles long by approximately 20 miles wide across South Texas, providing a geologic basis for multiple future potential production units beyond the current project area.

The satellite IX plant at Upper Spring Creek feeds uranium-loaded resin to enCore's Rosita CPP, which is already licensed and operating. The satellite model enables cost-effective operation across multiple sites without constructing full CPP facilities at each one, distributing fixed processing costs across a larger production base as additional satellites are added. The company holds S-K 1300 resources of 30.94 million pounds in the measured and indicated (M&I) category and 20.54 million pounds in the inferred category across its portfolio, as disclosed in the April 2026 corporate presentation.

South Texas as an ISR District

South Texas has been a proving ground for ISR uranium technology for more than 5 decades. enCore's technical advisory committee includes individuals with operational experience on Texas ISR projects through positions at US Steel, Cameco, Rio Algom, and General Atomics, among others, thereby reducing enCore's execution risk on wellfield construction and plant optimisation relative to companies entering ISR production for the first time.

The legacy of open-pit uranium mining in other US jurisdictions continues to shape public and regulatory attitudes nationally. Sheriff drew a sharp distinction between that history and what ISR represents today:

"Uranium mining now, in terms of in-situ, is not your predecessor uranium. It's as different as day and night. Being so environmentally friendly and with a short timeline, short cost to reclaim them, it's a completely different chapter and a new ball game."

The Texas Commission on Environmental Quality (TCEQ) administers ISR permitting in the state, and Texas's 50-year operational record provides a regulatory reference framework that newer ISR jurisdictions, such as South Dakota and Wyoming, are still developing.

Industry Outlook

The modular wellfield approach to ISR uranium production offers a credible path to scaling domestic US output. Still, it requires operators to manage 3 separate timelines simultaneously: construction, regulatory approvals, and production ramp-up. The permit gap between infrastructure-ready and production-authorised is the critical variable that separates projected timelines from realised ones.

For the ISR sector as a whole, the challenge of scale remains unresolved. The modular architecture that makes ISR capital-efficient at the project level can, if left unaddressed at the corporate level, produce a fragmented supply base of small producers, each too modest in output to attract tier-one institutional capital or negotiate competitive utility contracts.

The Upper Spring Creek project, once it receives final permits and enters production, will represent 1 additional wellfield module added to the US domestic uranium supply base. The industry's ability to add many more, quickly, is what the supply-demand arithmetic ultimately demands.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

Stay Informed