Impact Minerals: The HPA Technology Play Valued at a Fraction of A$250–700M Peers

Impact Minerals (ASX:IPT) is developing patented, low-cost high-purity alumina technology targeting battery, sapphire and ceramics markets at a fraction of peer capital costs.

- Impact Minerals (ASX:IPT) is transitioning from a junior mining company into a material science and specialty chemicals business with high-purity alumina as its primary commercial focus built around technology licensing, modular production, and specialty end markets.

- The company holds a 50% stake in Alluminous which owns patented HPA processing technology now protected in the United States, Canada, and Southeast Asia, and has successfully brought a pilot plant into batch production mode capable of delivering kilogram-scale HPA samples to prospective customers.

- A discovery that modifying impeller orientation in the solvent extraction stage increases front-end throughput by up to ten times has the potential to allow the company to achieve production capacity at a projected cost of under A$10 million comparable to peers who spent over A$200 million.

- The Lake Hope clay project in Western Australia adds further commercial optionality through the production of potash and aluminium chlorohydrate as byproducts, both of which have attracted early market interest and could support a joint venture arrangement.

- With listed peers trading at market capitalisations of A$300–700, Impact Minerals' current valuation appears to not yet reflect the potential scale of its cost advantage, with near-term catalysts including the publication of a scoping study for a 2,000-tonne-per-annum commercial plant.

Impact Minerals Limited (ASX:IPT) is in the process of a significant strategic evolution. Under the leadership of Dr. Mike Jones, the company is moving away from conventional junior mining activity toward a material science and industrial technology business. The vehicle for this transition is high-purity alumina,. a niche mineral input used in battery separators, artificial sapphire manufacturing, advanced ceramics, and semiconductor production.

The Strategic Direction

Impact Minerals has three broad areas of activity. The first and most important is the development and commercialisation of high-purity alumina, anchored by the Lake Hope clay project in Western Australia and a 50% stake in Alluminous, a company that holds patented HPA processing technology. The second is potash and hydrochloric acid which are byproducts discovered during HPA process development that management believes could attract a joint venture partner. The third is a portfolio of legacy exploration assets, most notably the Commonwealth gold-silver project in New South Wales, which has been farmed out to Kuniko Limited (ASX:KNI).

Dr. Jones is unambiguous about where the company is heading:

"100% becoming a material science company on the industrial side, the technology side of things, and moving out of the resources sector [...] It is about the technology to produce it and the end product that will go to the customers."

This shift in identity is important for investors to understand. The company is not seeking to be rated on resource multiples but on the revenue and margin potential of a specialty chemicals and technology licensor with a potentially much higher valuation framework.

The Alluminous Technology

The commercial pivot rests heavily on Alluminous, the company in which Impact holds a 50% interest and is described by Dr. Jones as the single largest shareholder by a factor of nearly ten. Alluminous owns a patented solvent extraction process for producing high-purity alumina from chemical feedstock. The intellectual property is now protected in the United States, Canada, and Southeast Asia - geographies that management regards as core to its commercialisation strategy.

The process involves a countercurrent solvent extraction step that leaches aluminium from chemical feedstock, followed by a stripping and precipitation stage to yield hydrated aluminium oxide, which is then calcined to produce HPA. While the chemistry is relatively straightforward at a conceptual level, achieving sufficient purity at scale is where technical differentiation matters.

The company acquired Alluminous and has since brought an approximately 80%-complete pilot plant into operational batch mode. It is now in a position to produce HPA in kilogram quantities, which management says is the entry-level requirement for initial customer qualification processes.

Interview with Dr. Mike Jones, MD of Impact Minerals

The Throughput Breakthrough

The most significant recent development is an engineering discovery that dramatically increased the front-end throughput of the pilot plant. The original design assumed a capacity of around 25 tonnes per annum under standard operating conditions. In attempting to improve mixing efficiency in the solvent extraction stage, the team modified the impeller orientation - and found that this single change increased throughput by up to ten times.

Dr. Jones described the discovery plainly:

"We basically turned the impellers upside down. And guess what? We suddenly got up to 10 times the throughput than was originally planned. That is really almost a global breakthrough in the ability to produce HPA reliably."

When confirmed through scale-up, this implies the pilot plant could potentially produce in excess of 200 tonnes per annum. The claim requires validation through the scoping study currently underway and to note the back-end engineering challenges managing high fluid volumes and ammonium sulfate waste products.

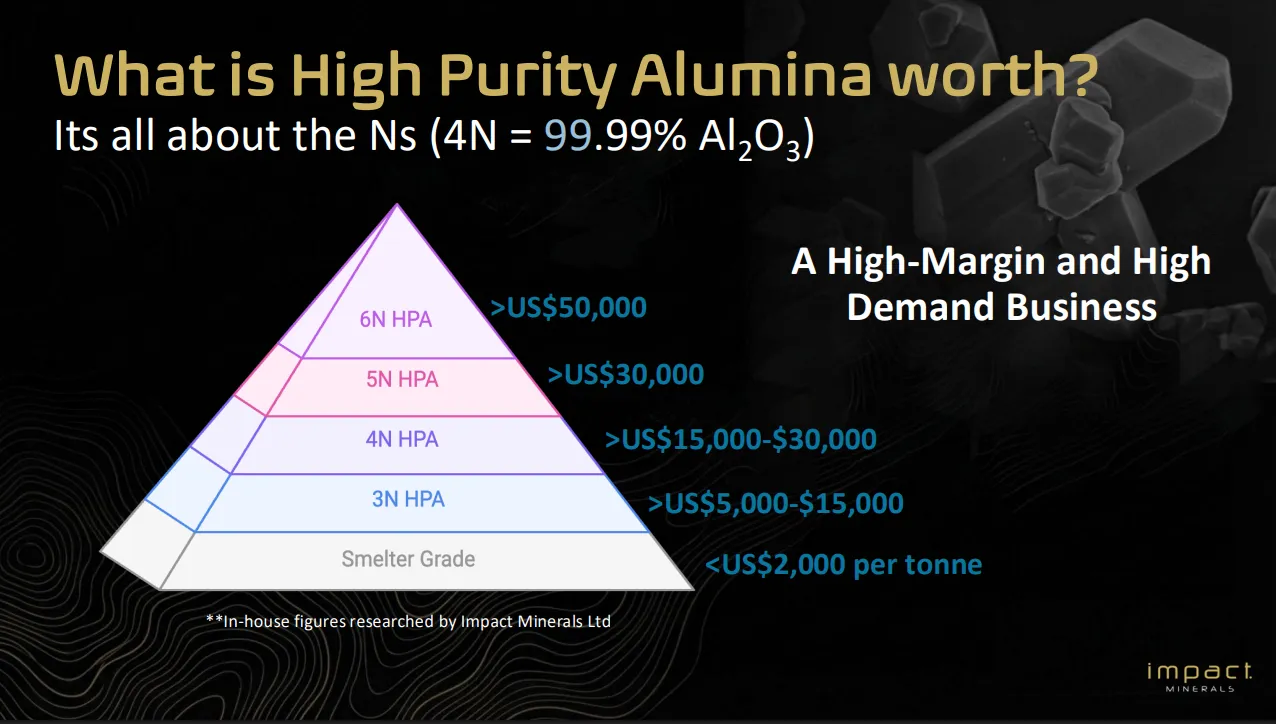

The Market for High-Purity Alumina

HPA is graded by purity level 3N, 4N, 5N (99.99%) being the main commercial categories. The highest volume demand exists in the 3N and 4N segments. The 3N market is predominantly advanced ceramics. The 4N market covers artificial sapphire manufacturing used in LED substrates, watch glass, and semiconductor equipment, and is where Impact has dispatched its first sample inquiries to European customers.

Battery applications are also relevant. Alluminous has completed a technology collaboration with C4V, a battery research company at Binghamton University in New York, the institution historically associated with the development of lithium-ion battery technology. Early physical testing of the company's material for use in battery separator coating has returned positive results.

Management's stated approach is to enter the 3N market first, given the larger addressable volume and lower qualification barrier, then leverage operational credibility to move up what Dr. Jones calls the "pyramid of purity" toward the 5N segment, where price premiums are significantly higher.

The Lake Hope Project and Byproduct Optionality

The Lake Hope project in Western Australia is the company's flagship mineral asset holding clay deposits from which HPA can be produced. The Pre-Feasibility Study (PFS) is complete, and the company is progressing toward a Definitive Feasibility Study (DFS). The production process at Lake Hope generates potash and aluminium chlorohydrate (ACH) as intermediate products both of which have standalone commercial value.

Potash, currently almost entirely imported into Western Australia, has attracted early interest from fertiliser distributors. ACH is used in water treatment and chemical industries. Management is pursuing a separate scoping study on the potash and HCl opportunity and intends to seek a joint venture partner for this stream, which would allow the company to retain focus on HPA without depleting capital across multiple fronts.

The company is also exploring whether the solid residue from the Lake Hope leaching process can be fed directly into the Alluminous process, which would create a natural cost and operational linkage between the two. This integration is not essential to the commercial case but would improve margins if achieved.

The Investment Thesis for Impact Minerals

- Consider the valuation gap to peers. Alpha HPA trades at approximately A$650–700 million and AEM at A$250–300 million. If Impact's technology delivers on its cost claims, the current share price may not reflect the potential scale of the opportunity. Monitor the scoping study results as a near-term catalyst.

- Back-end engineering milestones. The front-end throughput improvement is significant. Although the back-end challenges fluid volume management and ammonium sulfate handling remain unresolved, management updates over the next 6–12 months are worked through.

- Monitor customer sample results. The dispatch of initial 3kg sapphire-grade samples to European customers and the C4V battery collaboration are early commercial indicators. Positive feedback from these engagements would represent a meaningful de-risking event.

- Scoping study for the 2,000-tonne-per-annum commercial plant is imminent. Results are expected shortly and will provide the first independent cost estimates for the modular plant concept. A favourable outcome,where cost per tonne is well below A$100 million per 1,000 tonnes of annual capacity would support the company's cost leadership claims.

- The modular plant model is a structural differentiator. The ability to build multiple smaller plants rather than one large capital-intensive facility reduces financing risk and allows incremental scale-up. This is a genuine competitive advantage if proven out.

- IP protection is in place. US and Canadian patents have been secured. This matters not just for direct commercialisation but for any technology licensing strategy targeting North American customers and government funding programmes for critical minerals.

TL;DR

Impact Minerals holds patented, low-cost HPA processing technology that could reach peer-level production capacity for under A$10 million against the A$200 million-plus spent by comparable listed companies. The pilot plant is operating, IP is protected in the US, Canada, and Southeast Asia, and initial customer samples are being dispatched. A scoping study for the first commercial-scale plant is imminent. Listed peers trade at A$250-700 million, Impact Minerals is currently valued at a fraction of both. The back-end engineering is not yet complete, and the technology has not been demonstrated at full scale. For investors able to assess early-stage technology risk, the gap between current valuation and the potential upside once scale-up is confirmed is among the wider gaps currently visible in the ASX materials sector.

The Global Race for Critical Mineral Supply Chains

High-purity alumina sits at the intersection of several structural demand trends that are unlikely to reverse in the near term. The electrification of transport requires battery separators coated with HPA to improve thermal stability and performance. The semiconductor industry's continued expansion requires sapphire substrates and high-purity ceramic components. Defence and aerospace industries have growing requirements for advanced materials that can only be produced to specification with ultra-pure mineral inputs.

Critically, the global supply of HPA is heavily concentrated in China, which currently produces the majority of the world's output. Western governments particularly in the United States, Australia, Canada, and across the European Union have identified HPA as a critical mineral and are actively funding supply chain diversification programmes. This creates a rare commercial environment where both government grant funding and strategic off-take arrangements from defence and technology buyers are available to credible producers at scale.

The modular plant concept that Impact is pursuing is particularly well-suited to this environment. Dr. Jones summarised the opportunity:

"To get to almost the same levels of production as our competitors, they spent probably over $200 million. And we'll probably get to a similar level of production for less than $10 million. Now, that's an unbelievable number, but that's actually the scale of the breakthrough that we've kind of made."

Rather than requiring a single large plant demanding hundreds of millions of dollars in financing, the company can potentially build and license multiple smaller facilities closer to end customers in North America, Europe, or Southeast Asia thus reducing logistics costs and aligning with supply chain localisation policies. This positions Impact Minerals not just as a producer but as a potential technology platform.

Frequently Asked Questions (FAQs) AI-Generated

Analyst's Notes

Subscribe to Our Channel

Stay Informed