Indonesia Rejects a Broad Nickel Quota Increase, Challenging the Market's Oversupply Outlook for Battery Metals

Indonesia's quota policy and export controls are tightening nickel and lithium supply, making government decisions a bigger price driver than demand.

- Indonesia's Ministry of Energy and Mineral Resources ruled out a broad 2026 nickel mining quota increase on July 10, reversing market expectations of higher supply that had pushed spot nickel to six-month lows.

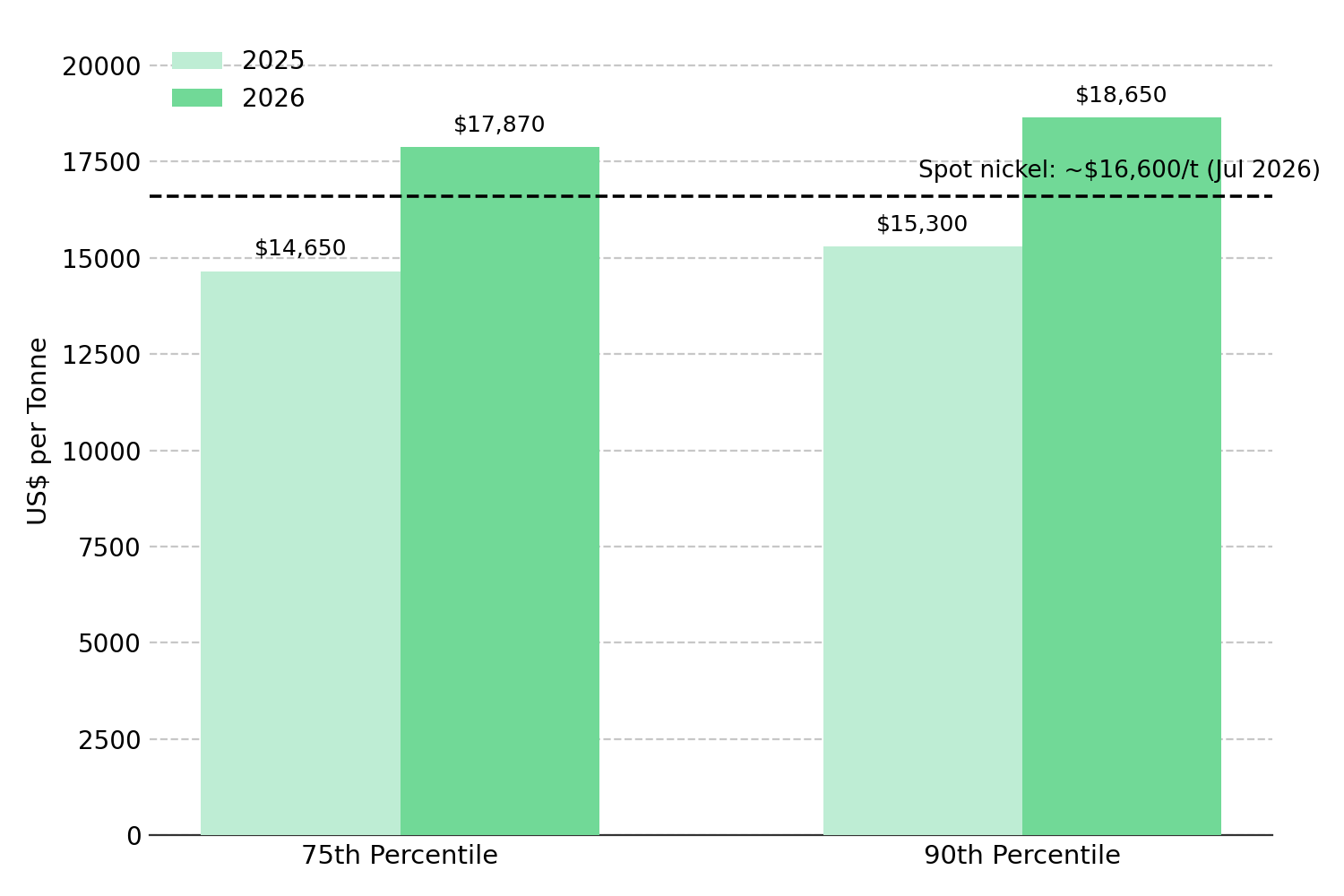

- Bernstein's July 2026 cost curve estimates place C1 cash costs at $17,870 to $18,650 per tonne at the 75th to 90th percentile, while spot nickel trades near $16,500 to $16,700 per tonne, leaving prices below the estimated marginal cost of supply.

- Zimbabwe's lithium export ban and the Democratic Republic of Congo's cobalt quota system show that governments are restricting battery metal supply through export controls and production quotas, extending the same pricing mechanism beyond Indonesia.

- Producing nations are using export controls, licensing requirements, and processing mandates to capture more value from battery metals, increasing the appeal of projects in jurisdictions with more predictable mining and export policies.

- Indonesia's July 31 quota decision is the next major catalyst for determining whether tighter nickel supply supports higher prices or whether additional mine quotas restore expectations of oversupply.

Government Supply Controls Replace Demand as the Primary Driver of Battery Metals Prices

In 2026, nickel and lithium prices are responding more to government supply controls than to changes in end-market demand. Indonesia's Ministry of Energy and Mineral Resources announced on July 10 that it would not broadly increase the 2026 national nickel mining quota, allowing exceptions only for domestic smelters facing immediate feedstock shortages. The decision reversed market expectations that additional supply would enter the market, supporting nickel prices by reducing the risk of oversupply. For much of the past decade, traders relied primarily on London Metal Exchange (LME) inventories and refined supply data to gauge market balance. That relationship has weakened as more global nickel production shifts into Indonesian nickel pig iron and mixed hydroxide precipitate, which are not deliverable into the LME. As a result, Indonesian production policy has become a more important driver of nickel prices than changes in exchange inventories.

Government-led supply controls are now extending beyond Indonesia into the lithium and cobalt markets. Zimbabwe brought forward its ban on raw lithium concentrate exports to February 2026, ten months ahead of the original January 2027 deadline. Because Zimbabwe supplies roughly 8% of global lithium production and nearly 15% of China's spodumene concentrate imports, the policy tightens feedstock availability for Chinese converters.

In the Democratic Republic of Congo (DRC), the state minerals regulator ARECOMS is enforcing a "use it or lose it" cobalt export quota through 2026. Industry estimates indicate that 60% to 75% of exporters could forfeit unused first-half export allocations to a state-controlled strategic reserve. Cobalt prices rose to roughly $26 per pound by mid-2026, up more than 160% from their February 2025 low, demonstrating that government supply controls can influence battery metals prices before additional physical supply reaches the market.

Indonesia's Supply Controls Lift Nickel Costs & Strengthen the Case for New Supply

Indonesia's 2026 Work Plan and Budget (RKAB) capped the nickel ore mining quota at 260 million to 270 million wet metric tonnes, well below the Indonesian Nickel Miners Association's estimate that domestic smelters require roughly 345 million wet metric tonnes of ore. Indonesia reinforced that supply discipline by revising its minimum price benchmark (HPM), which sets the minimum price paid to domestic miners for nickel ore, and by introducing export licensing on ferronickel products containing at least 4% nickel under Finance Minister Regulation No. 32. Together, those measures extend government control from ore production into processed nickel exports. Bernstein's July 2026 cost curve estimates place C1 cash costs at $17,870 and $18,650 per tonne at the 75th and 90th percentiles, compared with $14,650 and $15,300 per tonne in 2025. Even so, spot nickel continues to trade near $16,500 to $16,700 per tonne, leaving prices below the estimated upper end of the industry's cost curve.

Canada Nickel's Crawford Nickel Sulfide Project in Timmins, Ontario, is advancing a sulfide deposit that can be upgraded to roughly 34% nickel before processing. Compared with many Indonesian laterite operations that require more energy-intensive processing, the higher-grade concentrate has the potential to lower operating costs and reduce emissions, improving project economics. Mark Selby, Chief Executive Officer of Canada Nickel, explains Indonesia's influence over global nickel supply:

"There's been a major shift in the nickel market. We're really now one of the only projects that can come online before 2030. There's about three of us that can conceptually get there. They're keen to have that non-Indonesian offtake in place."

Export Restrictions Tighten Lithium Supply & Reward Project Execution

Lithium is now following the same pattern as nickel, with government supply controls playing a larger role in price formation than new mine production. Zimbabwe's accelerated export ban has reduced the availability of spodumene concentrate for Chinese converters. China is attempting to offset part of that shortfall after its Ministry of Natural Resources approved land use for CATL's Jianxiawo lithium mine and the company secured a work safety production permit. However, the company has not confirmed a restart date, leaving uncertainty over when additional supply will reach the market. Fastmarkets raised its lithium carbonate price forecasts to $23.80 per kilogram for 2026 from $17.40 and to $31.40 per kilogram for 2027 from $22.65, reflecting expectations that new lithium supply will continue to lag demand growth. As governments tighten control over battery metal supply, project execution is becoming a more important competitive advantage in jurisdictions with stable mining policies.

Lithium Ionic's 100%-owned Bandeira Lithium Project sits in Minas Gerais, Brazil, in the district the company calls "Lithium Valley," placing Bandeira in a jurisdiction with a proven production track record rather than unproven geology. On July 8, 2026, the company issued requests for quotation to seven contractors for construction of Bandeira's two underground mine portals, the surface access points for personnel, equipment, and development activities, advancing the project's engineering, procurement, and construction-readiness program toward a construction decision. Blake Hylands, Chief Executive Officer of Lithium Ionic, explains the emerging lithium supply deficit:

"We're actually seeing contraction in the production space. These projections of where supply is going to be are way off, and demand continues to grow. That gap is going to be our massive advantage."

Processing Rules Reward Low-Carbon Nickel Supply Outside Indonesia

Indonesia's ferronickel export licensing extends government control beyond nickel ore production to processed nickel exports. The EU is using regulation rather than export controls to influence the battery metals supply chain. Its Battery Regulation, which takes effect in 2026, requires traceability and carbon footprint disclosure for cobalt, lithium, nickel, and graphite imported into the bloc. Those requirements favor processing facilities that can document mineral origin and emissions, increasing the competitiveness of projects in jurisdictions with transparent supply chains.

Lifezone Metals holds a framework agreement with the Tanzanian government for the Kabanga Nickel Project, currently under amendment to settle the staging concept and the split of fiscal benefits between the company and the state. The project's processing route, Hydromet Technology, substitutes chemical leaching for smelting, and an independently reviewed Life Cycle Assessment puts the resulting carbon footprint at 3.7 tonnes of CO2-equivalent per tonne of nickel in concentrate, supporting compliance with the EU Battery Regulation's 2026 carbon-disclosure requirement for imported nickel. The Kabanga Feasibility Study reports an after-tax net present value of $1.58 billion and a 23.3% after-tax internal rate of return, with an all-in sustaining cost of $3.36 per pound of payable nickel net of copper and cobalt credits. Ingo Hofmaier, Chief Financial Officer of Lifezone Metals, discusses concentrated nickel supply risks:

"Nickel is a massive market, but it is very, very concentrated. If the development continues in Indonesia, you will have 75 to 80% of production. Other countries are leaning in, other companies are leaning in, and Indonesia has started playing around with its licensing regime."

Upcoming Policy Decisions Will Test the Battery Metals Supply Outlook

Indonesia's July 31 decision on supplementary RKAB applications is the next major test of whether tighter supply can support higher nickel prices. If the Ministry of Energy and Mineral Resources approves a broad RKAB increase before the application deadline, additional mine supply would weaken support from the industry's cost curve and make nickel prices more likely to remain near current levels. If it maintains the July 10 position, the supply outlook would become more consistent with Bernstein's cost curve estimates, narrowing the gap between spot prices and estimated production costs. The International Nickel Study Group has also revised its 2026 global nickel balance from a projected surplus of 283,000 tonnes to a deficit of 32,000 tonnes, the first deficit forecast since 2021. Together, the revised market balance and Indonesia's production policy point to tighter supply than the market had previously expected.

For lithium, the key near-term catalyst is confirmation of when the Jianxiawo mine will restart production. A restart in the second half of 2026 would introduce additional supply and could limit further gains in lithium prices despite Fastmarkets' higher forecasts. If the restart is delayed, supply is more likely to remain below expected demand, supporting stronger lithium prices into 2027. Because the mine represents roughly 3% of global lithium carbonate equivalent supply, the timing of its return will be an important indicator for both Chinese lithium prices and the broader market balance.

The US Section 232 investigation into processed critical minerals required a negotiation status report to the President by July 13, 2026. If the negotiations are deemed insufficient, the investigation allows tariffs, import restrictions, or price floors on processed lithium, nickel, and cobalt products. Those measures could alter battery metal costs independently of supply controls in Indonesia and Zimbabwe, making the Section 232 review another policy catalyst to monitor alongside Indonesia's July 31 RKAB decision.

The Investment Thesis for Battery Metals

- Indonesia's quota discipline has left spot nickel prices below Bernstein's estimated C1 cash costs, supporting a stronger pricing outlook if additional mine supply is not approved.

- Zimbabwe's lithium export ban and the DRC's cobalt export quotas show that government policy, rather than individual mine restarts, is becoming the larger driver of lithium and cobalt supply.

- Government supply controls are increasing the valuation premium for battery metals projects in jurisdictions with stable mining policies, transparent regulation, and predictable permitting.

- As government policy plays a larger role in battery metals prices, permitting, engineering progress, and procurement milestones provide earlier signals of which projects are most likely to advance.

- The EU's 2026 traceability requirements increase the competitive advantage of processing facilities that can verify mineral origin and carbon emissions.

- Projects with low all-in sustaining costs are better positioned to advance as government supply controls increase pressure on higher-cost producers.

The defining feature of the 2026 battery metals market is that government policy is becoming as important as geology in determining future supply. Quotas, export restrictions, processing rules, and permitting decisions are increasingly shaping where new nickel and lithium production can be developed and how quickly it reaches the market. That places greater emphasis on low-cost projects in stable jurisdictions while making upcoming policy decisions, particularly Indonesia's July 31 RKAB review, the Jianxiawo restart, and the US Section 232 investigation, the key catalysts for the remainder of 2026.

TL;DR

Indonesia's nickel quota policy, Zimbabwe's lithium export ban, and the DRC's cobalt export quotas show that government policy is playing a larger role than demand in shaping battery metals supply. As supply controls tighten, nickel prices remain below estimated production costs while lithium supply growth continues to lag demand. The article argues that low-cost projects in stable jurisdictions with transparent regulation, strong execution, and traceable processing are becoming more competitive. Investors should watch Indonesia's July 31 RKAB decision, the restart timing of China's Jianxiawo lithium mine, and the outcome of the US Section 232 investigation as the key policy catalysts for battery metals through the remainder of 2026.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

%20(1).jpg)

Stay Informed