Interest Rate Expectations Are Rotating Capital Toward High-Grade Producers and Underpriced Developers

Gold stocks shift with interest rates, favoring high-margin producers, strong balance sheets, and scarce exploration assets in a tightening supply environment.

- Gold is increasingly trading as a function of real interest rate expectations and macro liquidity conditions, creating a more volatile price regime with distinct episodic rallies driven by geopolitical risk premiums.

- Elevated real yields are compressing near-term gold price upside, but persistent inflation and structural dollar uncertainty underpin a medium-term bullish case for the metal and its equities.

- Capital is rotating within the gold sector toward developers and producers with high-margin, high-grade assets whose net present values carry significant upside torque at current spot prices above $3,000 per ounce.

- Financing conditions in a higher-rate environment are bifurcating the sector: companies with strong balance sheets and structured financing agreements are advancing projects while undercapitalized peers face dilutive headwinds.

- Exploration assets in scalable, high-grade systems are regaining attention as the global discovery pipeline narrows and scarcity value reasserts itself in institutional portfolio construction.

Gold's Transition From Inflation Hedge to Rate-Sensitive Asset

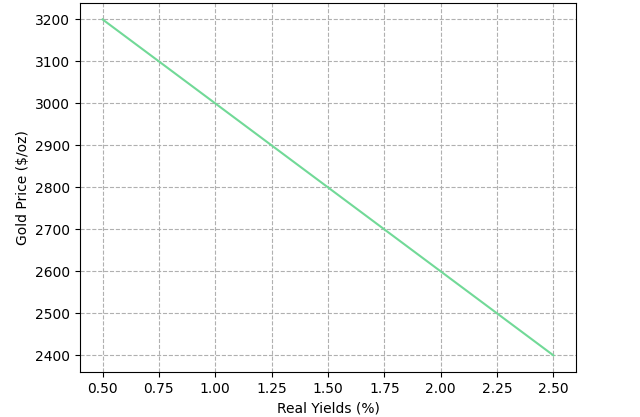

Gold's function in investor portfolios has changed. The metal historically served as a store of value that appreciated alongside consumer prices. That relationship persists, but it now operates beneath a more dominant dynamic: gold's price behavior has become primarily sensitive to real interest rates, the inflation-adjusted return on sovereign debt, rather than nominal inflation alone. According to PIMCO, a 100-basis-point increase in 10-year real yields has historically led to an 18% decline in the inflation-adjusted price of gold.

That sensitivity was stress-tested between 2022 and 2023, when real yields moved from deeply negative territory to above 2%. The World Gold Council notes that while gold was inversely correlated with real rates for roughly a decade prior to 2022, that relationship has since been counterbalanced by structural demand forces, including central bank accumulation, which helped gold rise even as real rates climbed.

When nominal rates rise faster than inflation expectations, real yields increase and the cost of holding a non-yielding asset rises, creating selling pressure on gold. When inflation persists without a commensurate rate response, or when geopolitical risk increases demand for safe-haven assets, sharp episodic rallies follow. The result is a price regime defined by oscillation between these competing forces rather than by a consistent directional trend.

Market behavior over the past 24 months confirms this pattern empirically. Despite persistent inflation and ongoing geopolitical tension, gold has experienced material corrections whenever Federal Reserve communication turned hawkish. When the Fed delivered a hawkish rate cut in December 2024, the World Gold Council documented sizeable intraday losses in gold alongside a 3% drop in the S&P 500 and the largest 10-year Treasury yield move on an FOMC meeting day since 2013. The metal recovered rapidly when rate expectations softened, creating an environment where broad sector rallies are less frequent and asset-specific re-ratings carry more weight."

The Transmission Channels From Macro Conditions to Mining Equity Valuations

Real yields, calculated as nominal treasury yields minus breakeven inflation rates, remain the most reliable leading indicator for gold price direction. When the Federal Reserve signals a prolonged rate hold while inflation stays above target, real yields remain elevated and suppress the gold price even when the nominal inflation argument for gold appears intact. Energy-driven inflation compounds this dynamic: higher oil prices delay central bank easing cycles, keeping real yields elevated and gold range-bound except during geopolitical disruptions.

Currency dynamics introduce a second transmission layer. A stronger US dollar creates a headwind for gold priced in other currencies, reducing purchasing power for non-US investors. Elevated foreign exchange volatility has simultaneously increased cross-border capital flows into gold equities from investors in economies experiencing local currency depreciation, a dynamic that is underweighted in most macro frameworks.

For producing companies, the current spread between all-in sustaining costs averaging $1,200 to $1,500 per ounce across high-margin operators and spot prices above $3,000 is expanding EBITDA at a rate that exceeds revenue growth, the direct expression of operating leverage at current prices.NPV sensitivity for developers: projects modeled at conservative assumptions of $1,800 to $2,000 per ounce carry substantial upside when discounted at current spot prices above $3,000. High-grade discoveries in under-explored systems gain value as the near-development asset pipeline narrows.

Capital Rotation Within the Sector: Grade, Cost Structure, and NPV Sensitivity

The rotation occurring within gold equities is not an exit from the asset class. It is a recalibration of where within the class investors are willing to accept risk and at what valuation. Producers offer cash flow certainty but limited NPV upside, their valuations are anchored to current production rates and near-term reserve life. Developers carry valuations tied to projected future cash flows discounted at assumptions often well below spot prices; incremental gold price increases generate non-linear improvements in project economics.

High-grade deposits carry lower all-in sustaining costs, require less capital per recoverable ounce, and offer faster payback periods. In a higher-rate environment where debt capital costs have risen meaningfully, these grade-driven cost advantages translate into risk-adjusted return differentials.

Leveraging High-Grade Economics for Developer Upside

New Found Gold's Queensway project in Newfoundland illustrates the developer positioning thesis. Keith Boyle, Chief Executive Officer of New Found Gold, outlined the production profile and its financial implications:

“The higher grades in the first couple of years will likely bring us closer to 100,000 ounces annually. At an all-in sustaining cost of $1,300, you're looking at approximately $400 million in Canadian free cash flow.”

The combination of near-term grade advantage and lean cost structure creates a project economics profile whose sensitivity to upward gold price movement is precisely the leverage characteristic institutional investors are seeking in the current environment.

Self-Funded Growth Through High-Grade Production

Serabi Gold's operational trajectory illustrates what sustained self-financing through high-grade production looks like in practice. Mike Hodgson, Chief Executive Officer of Serabi Gold, described the company's record output and its funding implications:

"Cash generation has been exceptional. We're generating so much cash at the moment we can fund it all out of cash flow comfortably. We're not going out looking for more money from investors or raising debt or anything."

Operational self-sufficiency of this kind is a meaningful differentiator when external financing conditions are restrictive and equity markets are selective.

Financing Conditions and Their Differentiated Impact Across the Sector

The rise in debt capital costs is not uniformly negative for gold equities. It is, however, selective in its impact. Companies that secured financing before the rate cycle peaked occupy a materially different risk position than peers that remain dependent on current capital markets.

Gold prepay facilities, streaming agreements, and convertible note structures have become preferred instruments because they reduce near-term dilution risk for equity holders while providing capital certainty for project advancement. Companies that executed structured financing at scale when conditions were favorable can advance through volatile markets without the episodic equity raises that erode per-share value.

Internal Capital Accumulation as a Strategic Buffer

Integra Resources illustrates deliberate internal capital accumulation ahead of a major development commitment. George Salamis, Chief Executive Officer of Integra Resources, described the current year as a strategic build-out period:

"2026 is about building capacity today to deliver more ounces, stronger cash flow, and lower costs tomorrow. We've got $60-70 million to spend on the asset, which still leaves plenty of free cash. The goal is to build as large a cash position as possible to finance Delamar."

The Global Discovery Pipeline and Its Supply Implications

The data underlying the scarcity argument has been building for over a decade. Major gold discoveries, deposits with more than 2 million ounces of measured and indicated resources, have declined in annual frequency since their peak in the early 2000s. The existing development pipeline is aging, and replacement discoveries have not kept pace with depletion rates at operating mines. In this context, large-scale exploration systems in established mining jurisdictions carry a scarcity premium that is beginning to be reflected in valuations.

Resource Expansion Within a Large-Scale Open System

Hycroft Mining's exploration program in Nevada demonstrates how resource expansion within an existing large-scale system can reframe a company's investment narrative. Diane Garrett, President and Chief Executive Officer of Hycroft Mining, described the resource growth outcomes and geological characteristics of the deposit:

"We had a significant overall increase in resources, and recoveries are much higher than we originally contemplated. We are seeing indications that this is a large and, at one time, very powerful system. The system remains open in all directions and at depth, and it continues to grow."

Hycroft's deposit - open in all directions and at depth, with recoveries exceeding original projections - carries resource growth optionality whose value to institutional investors increases directly as the stock of deposits at the feasibility or pre-feasibility stage fails to keep pace with depletion rates at operating mines.

Self-Funding Exploration Through Phased Development

Cabral Gold's staged approach in Brazil illustrates a model many exploration and development companies are employing: generate near-term cash flow from an initial lower-complexity operation to fund exploration of a larger underlying system. Alan Carter, Chief Executive Officer of Cabral Gold, described the strategic logic:

"We are building an initial gold-in-oxide heap leach project that will provide a significant amount of cash. Ultimately, this will demonstrate the economic viability of the much larger phase-two project. We have over 50 peripheral targets where we’ve found gold, and we believe we can increase the company’s value faster by growing the global resource base here."

Cabral's heap leach operation funds exploration across more than 50 peripheral targets from internal cash flow, eliminating the dilutive equity raises that erode per-share value for capital-dependent peers advancing district-scale resource programs in the current financing environment.

The Investment Thesis for Gold

- Companies with low all-in sustaining costs and expanding margins offer direct exposure to the spread between production economics and elevated spot gold prices, generating free cash flow that supports both internal reinvestment and capital return.

- Developers with NPVs modeled at conservative gold price assumptions carry upside that is not yet fully reflected in enterprise value-per-ounce metrics at current spot prices.

- Operators and developers that secured structured financing ahead of the rate cycle peak are advancing projects without equity dilution, creating a differentiated profile relative to capital-dependent peers.

- High-grade deposits in stable jurisdictions carry all-in sustaining cost advantages that maintain margin resilience across a wider range of gold price scenarios, reducing sensitivity to near-term rate-driven price volatility.

- Exploration companies with district-scale systems in active geological provinces carry discovery optionality that is gaining relevance as the global development pipeline narrows and scarcity of near-development assets becomes a more prominent institutional consideration.

- Staged development models that generate near-term cash flow from initial production phases while funding exploration of larger underlying resources represent one approach to managing capital dependency risk in a restrictive financing environment.

The gold equity market in the current macro cycle is defined by the interaction of real yield sensitivity, inflation persistence, and episodic geopolitical risk, forces that have created an environment where broad-based sector performance is less common and asset-specific re-ratings carry greater weight.

Financing structure, production cost profile, and project-level NPV sensitivity to gold price assumptions determine return differentiation more reliably than commodity price direction alone - companies advancing on internal cash generation or pre-arranged structured financing avoid the dilutive equity raises that compress per-share value for capital-dependent peers, a distinction that is measurable at the enterprise value per ounce level across the producers, developers, and exploration assets covered in this analysis.

TL;DR

Gold is no longer behaving purely as an inflation hedge, it is now highly sensitive to real interest rates, creating a more volatile and selective investment environment. In this regime, capital is flowing toward high-margin producers, disciplined developers, and companies with strong balance sheets or pre-secured financing, while weaker, capital-dependent firms face dilution risk. At the same time, a declining global discovery pipeline is reviving interest in exploration assets with scalable, high-grade systems. The result is a market where stock-specific fundamentals, cost structure, financing strategy, and resource quality matter far more than broad gold price direction.

FAQs (AI-generated)

Gold’s pricing is increasingly driven by real yields rather than inflation alone. When interest rates rise faster than inflation, real yields increase, making non-yielding assets like gold less attractive. Conversely, when inflation persists or geopolitical risks rise without a proportional rate response, gold tends to rally. This shift has created a more episodic and volatile pricing pattern compared to its traditional steady inflation-hedge behavior.

Investors are prioritizing producers and developers with high-grade assets, low all-in sustaining costs, and strong margins. These companies benefit most from elevated gold prices through operating leverage and improved project economics. Developers, in particular, offer significant upside because their valuations are often based on conservative gold price assumptions, making them highly sensitive to current spot prices above $3,000 per ounce.

Higher rates are increasing the cost of capital, creating a divide within the sector. Companies with strong balance sheets or pre-arranged financing can continue advancing projects without dilution, while those reliant on external funding face higher borrowing costs or equity issuance. This has made financing structure a key differentiator in determining which companies can execute growth strategies effectively.

The global pipeline of major gold discoveries has been declining for over a decade, and existing mines are depleting faster than new projects are being developed. This supply constraint is driving renewed interest in exploration companies with large, scalable systems, especially in stable jurisdictions. As scarcity becomes more pronounced, these assets are gaining a valuation premium due to their long-term optionality.

A selective, fundamentals-driven approach is essential. Investors should focus on companies with strong cost structures, high-grade resources, and either internal cash generation or secured financing. Broad exposure to gold prices alone is insufficient; instead, identifying companies with favorable project economics and resilience to financing constraints offers better risk-adjusted returns in a rate-sensitive environment.

Analyst's Notes

Subscribe to Our Channel

Stay Informed