IsoEnergy: High-Grade Uranium Asset Positioned for Market Growth

IsoEnergy offers investors exposure to world-class Canadian uranium resources and near-term U.S. production restart amid rising nuclear demand and supply constraints.

- IsoEnergy controls 48.6 million pounds of indicated uranium resources at 34.5% U₃O₈ at its Hurricane deposit in Saskatchewan one of the highest-grade uranium resources globally.

- The company maintains operations across three Tier-1 jurisdictions (Canada, U.S., Australia) with 55.2 million pounds of current measured and indicated resources and 153.8 million pounds historically.

- The fully-permitted Tony M Mine in Utah holds 6.6 million pounds of indicated resources with existing infrastructure and toll milling agreements, targeting restart decisions in 2025.

- Located 40 kilometers from the McClean Lake Mill, Hurricane is positioned to replace depleting Cigar Lake production by 2035, addressing a critical supply gap in the Athabasca Basin.

- With C$84.7 million in cash, C$57.5 million in strategic equity holdings, and analyst price targets ranging from C$17.00 to C$28.60, IsoEnergy maintains financial flexibility to advance multiple development pathways.

The uranium sector is experiencing a fundamental transformation as nuclear energy reemerges as a cornerstone of global decarbonization strategies. Against this backdrop, IsoEnergy Ltd. has positioned itself as a diversified uranium company with assets spanning Canada's prolific Athabasca Basin to the conventional mining districts of Utah. With uranium spot prices reaching $80 per pound in October 2025 up from $48 per pound and mounting concerns over supply constraints following Cigar Lake's anticipated depletion by 2035, IsoEnergy's high-grade Hurricane deposit and near-term production assets warrant investor attention. This analysis examines why IsoEnergy represents a compelling investment opportunity in the evolving nuclear fuel landscape.

Company Overview

IsoEnergy operates as a leading uranium exploration and development company with a market capitalization of C$820 million and an enterprise value of C$688 million as of October 7, 2025. Trading at C$14.99 per share on Canadian exchanges, the company maintains a robust balance sheet with C$84.7 million in cash and C$57.5 million in strategic equity holdings. The shareholder base includes NexGen Energy at 30.1%, reflecting confidence from industry leaders, alongside institutional holders such as the URNM ETF (7.9%) and URA ETF (3.5%).

The company's management team brings extensive uranium sector experience, with CEO Phil Williams, COO Marty Tunney, and VP Exploration Dr. Dan Brisbin drawing from backgrounds at NexGen Energy and Uranium One. This pedigree has translated into a disciplined approach to resource development and strategic asset accumulation. Seven analyst firms currently maintain buy ratings on the stock with price targets spanning C$17.00 to C$28.60, suggesting potential upside from current levels.

IsoEnergy's strategic framework centers on three pillars: exploration upside from Hurricane expansion, near-term production restart at Tony M, and proven leadership with demonstrated uranium development capabilities. This multi-asset approach provides diversification across development timelines and jurisdictional risk profiles, a critical consideration given the extended permitting cycles characteristic of uranium projects.

The Hurricane Deposit: World-Class Canadian Asset

The Hurricane deposit in Saskatchewan's Larocque East Project represents IsoEnergy's flagship asset and a rare high-grade uranium resource. With 48.6 million pounds of indicated resources grading 34.5% U₃O₈ and an additional 2.7 million pounds of inferred resources at 2.2%, Hurricane ranks among the world's highest-grade indicated uranium resources. This exceptional grade compares favorably to the global average for uranium deposits, which typically range between 0.1% and 0.5% U₃O₈.

The deposit's strategic location 40 kilometers from Orano's McClean Lake Mill provides critical infrastructure advantages that could significantly reduce capital requirements and accelerate time to production. The Athabasca Basin hosts several world-class uranium operations, and Hurricane's proximity to established processing facilities positions it as a natural successor to aging deposits. Cigar Lake, currently one of the world's highest-grade producing uranium mines, faces depletion by 2035, creating a supply gap that Hurricane is specifically positioned to address.

IsoEnergy's Summer 2025 exploration program deployed 20 drill holes totaling 7,600 meters targeting resource expansion and regional discoveries. High radioactivity intercepts exceeding 28,000 counts per second in Area D confirmed expansion potential beyond the current resource envelope. Future targets include Areas E, F, and K, along with extensions along the Larocque Trend, suggesting substantial upside to the existing resource base. Technical sensitivity analysis indicates that Hurricane resources retain over 93% metal content at a 10% cut-off grade, demonstrating the robustness of the deposit's economic potential across various operating scenarios.

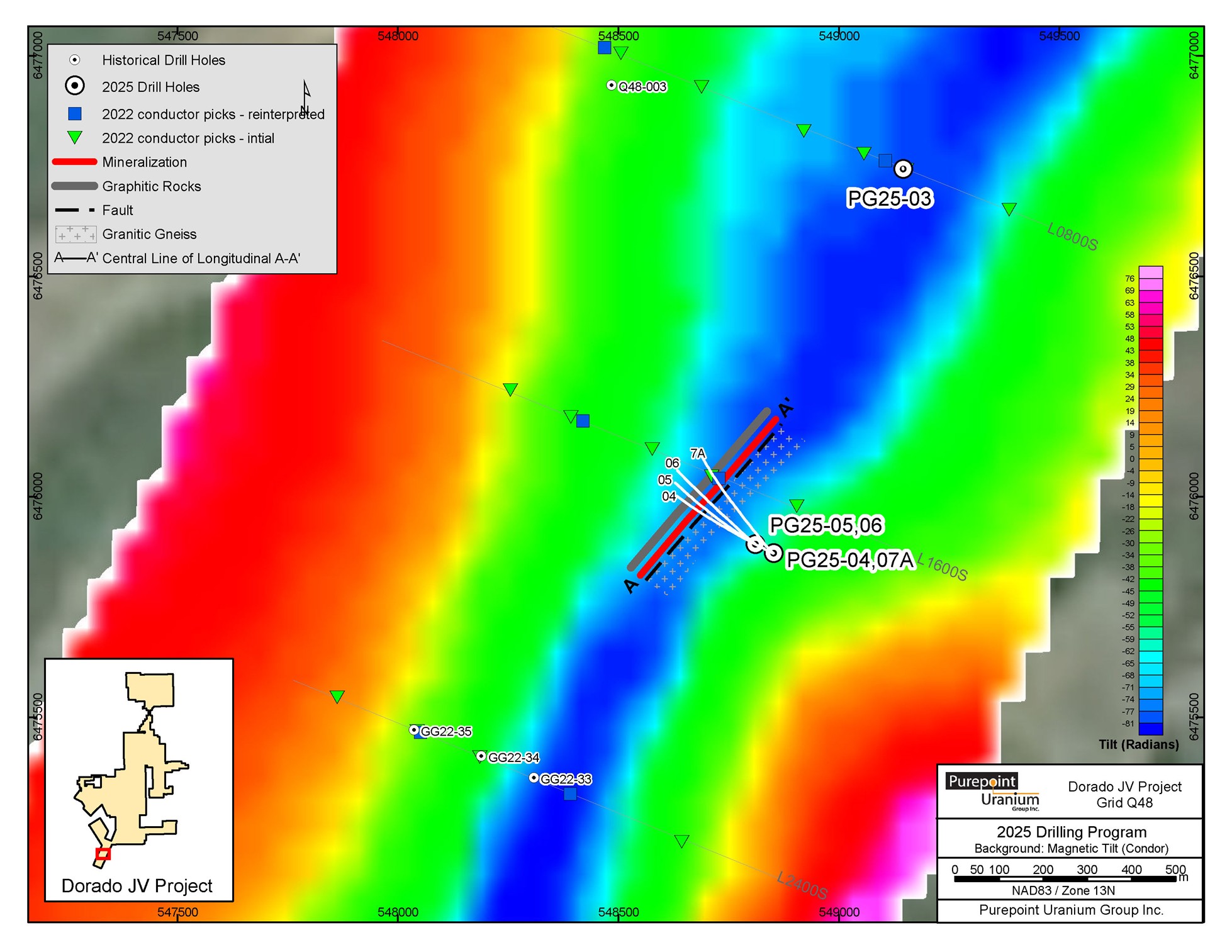

Expanding the Eastern Athabasca Portfolio: Dorado Discovery

Beyond Hurricane, IsoEnergy is advancing exploration through its 50/50 joint venture with Purepoint Uranium at the Dorado Project in the Eastern Athabasca Basin. The Nova Discovery at Dorado has delivered encouraging early-stage results that demonstrate the prospectivity of IsoEnergy's broader Saskatchewan land position. Dr. Dan Brisbin, IsoEnergy's Vice President of Exploration and a qualified person under NI 43-101, emphasized the significance of these findings in the company's broader exploration strategy.

Recent drilling at the Nova Discovery intersected high-grade uranium mineralization, with assay results including 8.1% U₃O₈ over 0.4 meters and 1.5% U₃O₈ over 3.5 meters. These grades, while occurring over narrower intervals than Hurricane's massive high-grade zones, confirm the presence of unconformity-style uranium mineralization similar to deposits that have historically defined the Athabasca Basin as a world-class uranium district. The joint venture structure allows IsoEnergy to advance exploration while sharing costs and technical expertise with Purepoint, an efficient approach for early-stage targets.

Follow-up drilling planned for early 2026 will test the extent and continuity of mineralization at Nova and explore additional targets across the Dorado property. Success at Dorado could add meaningful exploration upside to IsoEnergy's portfolio while validating the company's technical team's ability to make new discoveries in a highly competitive exploration environment. The Eastern Athabasca Basin remains underexplored relative to the southwestern region hosting Hurricane, presenting opportunities for additional discovery value creation.

U.S. Operations: Near-Term Production Pathway

IsoEnergy's Utah portfolio provides a contrasting near-term production opportunity to the longer-term Hurricane development. The Tony M Mine represents the company's most advanced U.S. asset, featuring 6.6 million pounds of indicated resources at 0.28% U₃O₈ and 2.2 million pounds of inferred resources at 0.27%. The mine benefits from 18 miles of existing underground development, ore bays, and a compressor station, significantly reducing the capital required for restart compared to greenfield projects.

Full permitting and proximity to the White Mesa Mill, with toll milling agreements already in place, position Tony M for relatively rapid restart decisions. The company is conducting technical and economic evaluations throughout 2025 to assess optimal restart timing and economics. Unlike the extensive permitting challenges facing many uranium projects, Tony M's existing permits and infrastructure provide a clear pathway to production that could generate cash flow within 18 to 24 months of a positive restart decision.

Complementing Tony M, the Daneros Mine produced approximately one million pounds historically and maintains indicated and inferred resources grading 0.36% and 0.37% U₃O₈ respectively. The Rim Mine, characterized by a high vanadium-to-uranium ratio of 9:1, features 2.7 miles of underground works and exploration potential through ongoing geophysical surveys. All Utah assets hold full operational permits, a significant advantage in an industry where permitting can consume years and substantial capital. This portfolio approach allows IsoEnergy to optimize production timing and capital allocation based on uranium price evolution and operational readiness.

Strategic Call Options & Portfolio Assets

IsoEnergy maintains strategic positions in several significant uranium assets that function as call options on favorable policy developments or market conditions. The Coles Hill project in Virginia contains one of the United States' largest undeveloped uranium deposits, with 132.9 million pounds of indicated resources and 30.4 million pounds of inferred resources. Located near Virginia's "Data Center Alley," a region experiencing explosive growth in electricity demand from technology infrastructure, Coles Hill represents substantial optionality should Virginia lift its uranium mining restrictions.

The Matoush project in Quebec features a high-grade historical resource of 12.3 million pounds indicated at 0.954% and 16.4 million pounds inferred at 0.442%, with approximately C$120 million in historical exploration expenditures. While Quebec maintains restrictive uranium policies, evolving nuclear sentiment across Canada could unlock this asset's value. Similarly, the Australian portfolio comprising Ben Lomond, Milo, and Yarranna projects holds approximately 25 million pounds of combined historical resources, though Queensland's uranium policy currently limits near-term development.

These call option assets required minimal acquisition costs relative to their exploration expenditures and resource bases, providing asymmetric upside potential if regulatory environments evolve. The combined historical expenditure across these assets exceeds C$220 million, yet IsoEnergy acquired them through strategic transactions at fractions of replacement cost. This approach demonstrates management's ability to identify and secure value through contrarian positioning and patient capital deployment.

Financial Strength & Equity Portfolio

IsoEnergy's financial position extends beyond its cash balance through a strategically assembled equity portfolio valued at approximately C$57.5 million. Holdings include positions in NexGen Energy, Premier American Uranium, Atha Energy, Future Fuels, Toro Energy, Purepoint Uranium, Jaguar Uranium, Verdera Resources, and Royal Uranium. These holdings originated from spin-outs, asset sales, and joint venture transactions executed between 2023 and 2025.

This equity portfolio serves multiple strategic purposes. First, it provides financial flexibility to fund exploration and development activities without immediate dilution. Second, it creates leveraged exposure to sector-wide uranium price appreciation, as many portfolio companies control early-stage assets that typically exhibit higher beta to commodity price movements. Third, it maintains relationships and potential strategic optionality with companies controlling adjacent land packages or complementary assets.

The company's enterprise value of C$688 million calculated as market capitalization minus cash and equity holdings represents a relatively modest premium for controlling the Hurricane deposit and fully-permitted U.S. production assets. Compared to uranium sector peers including Uranium Energy Corp., Denison Mines, Paladin Energy, and Energy Fuels, IsoEnergy's valuation metrics appear attractive relative to its resource quality and grade. This financial positioning provides management with multiple levers for value creation without near-term funding pressures that could force suboptimal decisions.

Market Context & Industry Dynamics

The uranium market is experiencing structural tightening driven by supply constraints and accelerating nuclear energy adoption. Uranium spot prices reached $80 per pound in October 2025, reflecting a 67% increase from prior levels and marking the highest prices in over a decade. This price appreciation reflects fundamental supply-demand imbalances as utilities secure long-term contracts while primary production remains constrained.

Cigar Lake's anticipated depletion by 2035 represents a critical inflection point for the Athabasca Basin and global uranium supply. As one of the world's highest-grade producing deposits, Cigar Lake's decline creates a supply gap requiring replacement ounces from new projects. Hurricane's combination of high grade, proximity to processing infrastructure, and location in an established mining jurisdiction positions it as a logical successor project. The lead time required to advance uranium projects from discovery through permitting to production often exceeding ten years means replacement projects must advance now to maintain supply continuity.

Media coverage from outlets including Barron's, Financial Times, and Bloomberg has highlighted global uranium shortages and renewed nuclear momentum as countries pursue decarbonization targets. Small modular reactors, life extensions at existing nuclear facilities, and new large-scale reactor construction across Asia and Eastern Europe are driving structural demand growth. This confluence of constrained supply and growing demand underpins the investment thesis for uranium equities positioned to deliver ounces into a tightening market.

Current Development Activities & Catalysts

IsoEnergy's 2025-2026 catalyst pipeline includes several value-creating milestones that could drive share price appreciation. The Summer 2025 exploration program along the Larocque Trend targeted resource expansion at Hurricane and new discoveries across the broader land package. Assay results from high radioactivity intercepts in Area D and drilling at Areas E, F, and K could materially expand the resource base and extend mine life projections.

The Tony M mine restart decision, anticipated following completion of technical and economic evaluations, represents a near-term production catalyst that would transition IsoEnergy from a pure development company to a producer. This transformation typically triggers valuation re-ratings as investors apply production multiples rather than exploration or development stage multiples. The presence of existing infrastructure and permits reduces execution risk relative to greenfield developments.

Additional catalysts include potential monetization of secondary projects through joint ventures or asset sales, advancement of U.S. portfolio exploration programs, and strategic mergers and acquisitions. The company's management team has demonstrated capability in executing value-accretive transactions, as evidenced by the equity portfolio assembled through strategic deals. The Dorado joint venture results, including the high-grade intersections at Nova, validate the exploration team's targeting methodologies and could generate additional value if follow-up drilling planned for early 2026 expands the discovery footprint.

The Investment Thesis for IsoEnergy Ltd.

- Hurricane's 34.5% grade provides operating leverage and potential margin expansion as uranium prices rise, justifying premium valuations relative to lower-grade peers.

- Diversify uranium exposure by adding producers with near-term cash flow potential; Tony M restart could trigger valuation re-rating within 12-18 months.

- Prioritize companies operating in stable, mining-friendly jurisdictions (Canada, U.S., Australia) where permitting risk is minimized and infrastructure exists.

- Position in projects capable of replacing depleting Tier-1 assets like Cigar Lake; Hurricane's proximity to McClean Lake Mill reduces development capital requirements.

- Evaluate teams with proven uranium development experience; IsoEnergy's leadership demonstrated value creation at NexGen and execution capability through strategic transactions.

- Target companies with cash positions and strategic assets providing funding optionality; IsoEnergy's C$84.7 million cash and C$57.5 million equity holdings support development without immediate dilution pressure.

IsoEnergy Ltd. presents a differentiated investment opportunity in the uranium sector through its combination of world-class Canadian resources, near-term U.S. production potential, and strategic call options across multiple jurisdictions. The Hurricane deposit's exceptional 34.5% grade positions it among the world's premier undeveloped uranium assets, while its proximity to existing infrastructure provides a clear development pathway as Cigar Lake faces depletion by 2035. The Tony M mine restart opportunity offers near-term production catalysts that could accelerate cash flow generation and valuation re-rating.

The company's C$820 million market capitalization appears attractive relative to its 55.2 million pounds of current measured and indicated resources and 153.8 million pounds of historical resources across its diversified portfolio. With uranium prices reaching $80 per pound and structural supply constraints tightening, IsoEnergy's combination of high-grade resources, near-term production optionality, and financial flexibility positions it to capitalize on favorable sector dynamics. Investors seeking exposure to uranium's supply-demand fundamentals with diversification across development timelines and geographies should evaluate IsoEnergy as a core holding in a nuclear energy-focused portfolio.

TL;DR

IsoEnergy controls one of the world's highest-grade uranium deposits (Hurricane: 48.6 Mlbs @ 34.5% U₃O₈) in Saskatchewan's Athabasca Basin, strategically located 40 kilometers from processing infrastructure. The company offers diversified exposure through near-term production restart potential at the fully-permitted Tony M Mine in Utah (6.6 Mlbs indicated), strategic call options on U.S. and Australian assets totaling over 150 million pounds of historical resources, and a strong balance sheet with C$84.7 million cash plus C$57.5 million in equity holdings. With uranium prices at $80/lb and Cigar Lake depleting by 2035, IsoEnergy is positioned to benefit from structural supply tightening while advancing multiple value-creation pathways.

FAQs (AI-Generated)

Hurricane contains 48.6 million pounds at 34.5% U₃O₈ grade, ranking among the world's highest-grade indicated uranium resources and providing significant operating margin potential.

Tony M could restart within 18-24 months following a positive development decision, as it maintains full permits, existing infrastructure, and toll milling agreements with White Mesa Mill.

At C$820 million market cap with high-grade resources and near-term production potential, IsoEnergy trades at attractive metrics relative to Uranium Energy Corp., Denison Mines, and Paladin Energy.

Primary risks include uranium price volatility, permitting delays, capital cost inflation, operational execution challenges, and potential regulatory changes in operating jurisdictions.

Cigar Lake's anticipated 2035 depletion creates a supply gap in the Athabasca Basin that Hurricane is positioned to fill given its proximity to McClean Lake Mill and comparable high-grade profile.

Analyst's Notes

Subscribe to Our Channel

Stay Informed