Uranium Price Volatility in 2025 & the Nuclear Fuel Supply Gap: Why Structural Deficits Still Support a Higher-For-Longer Cycle

Uranium's 2025 volatility masks structural deficits as production lags demand by 130M lbs annually. Energy Fuels, enCore, IsoEnergy & ATHA offer exposure.

- Uranium spot prices experienced volatility in early 2025, reflecting inventory adjustments and speculative unwinding, but term contracting activity remains robust as utilities secure supply for long-term fuel requirements.

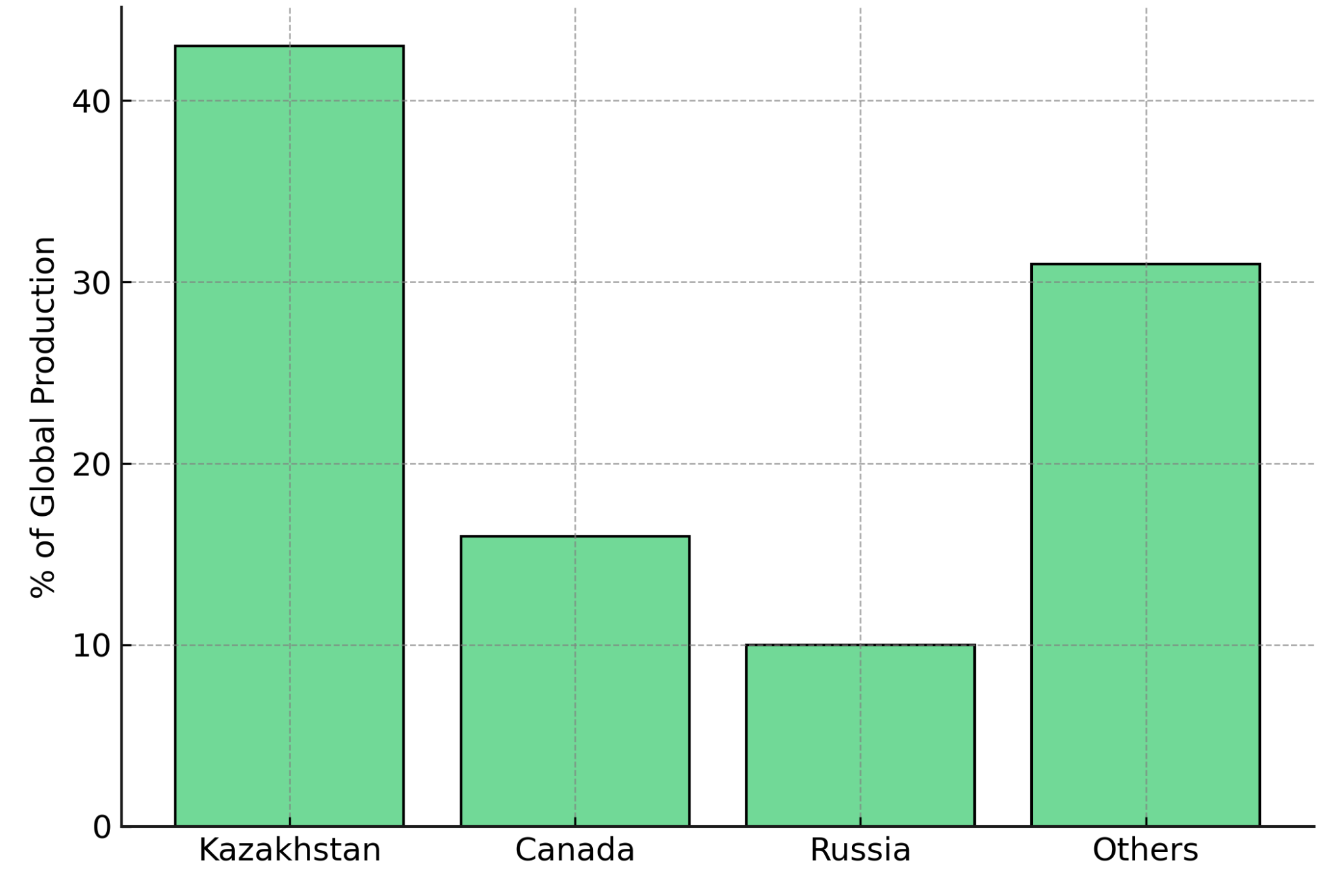

- Supply constraints persist across the nuclear fuel cycle, with North American production capacity reaching only 10-15% of domestic consumption while global primary supply remains concentrated in Kazakhstan, Canada, and Russia.

- Demand visibility has strengthened materially through legislative support, nuclear capacity additions, and data center partnerships, creating multi-year demand growth that outpaces credible supply additions.

- The cost curve for new uranium production has shifted higher due to inflationary pressures, regulatory complexity, and extended permitting timelines, supporting elevated long-term price expectations.

- Investment opportunities span the risk spectrum from established producers with processing infrastructure to restart-ready development assets and high-grade exploration plays positioned in Tier-1 jurisdictions.

Framing 2025's Uranium Volatility in a Structurally Tight Market

Uranium markets entered 2025 confronting a familiar paradox: short-term price volatility occurring within a structurally undersupplied market. Spot prices, which reached approximately $106 per pound in early 2024, have experienced corrections as speculative positioning unwound and secondary supply entered the market. This volatility represents normal cyclical behavior within a commodity market transitioning from surplus to deficit.

The underlying fundamentals supporting higher uranium prices remain intact. According to the World Nuclear Association's 2025 Nuclear Fuel Report, global reactor requirements for 2025 are estimated at approximately 68,920 tonnes of uranium (equivalent to 179 million pounds U₃O₈), while primary mine production is projected to reach approximately 140-150 million pounds annually. This creates an annual supply gap of roughly 30-40 million pounds that has been temporarily masked by secondary supply sources including underfeeding at enrichment facilities, inventory drawdowns, and material sales from government stockpiles. However, these secondary sources are finite and declining, with their contribution expected to fall from approximately 14% of total supply in 2025 to as little as 4% by 2050, creating an inevitable convergence point where primary production must expand materially to meet demand.

What distinguishes the current cycle from previous uranium bull markets is the quality and durability of demand drivers. Legislative frameworks such as the ADVANCE Act in the United States, the European Union's taxonomy inclusion of nuclear energy, and national energy security mandates across Asia have created policy certainty that extends beyond electoral cycles. Simultaneously, the emergence of small modular reactor technology and nuclear partnerships with hyperscale data center operators represents genuinely incremental demand rather than displacement of existing consumption.

The investment implication is straightforward: volatility in spot pricing creates entry points for exposure to companies positioned along the uranium supply curve, particularly those with near-term production capability, jurisdictional advantages, or high-grade resource endowments. The structural deficit remains the dominant long-term driver, and companies capable of delivering pounds into a supply-constrained market trade at valuations reflecting scarcity premiums rather than commodity price leverage alone.

Supply Constraints, Geographic Concentration & the Security-of-Supply Premium

The uranium supply complex faces structural constraints that extend beyond simple production volume deficits. Geographic concentration represents a critical vulnerability, with Kazakhstan, Canada, and Russia collectively accounting for the majority of global primary production. This concentration becomes particularly acute when evaluating conversion and enrichment capacity, where Russian entities control significant portions of global services.

Western utilities and governments have responded to this concentration risk by prioritizing supply chain diversification and domestic production capability. The United States enacted legislation prohibiting Russian uranium imports, with implementation beginning in 2024. This policy shift eliminates a material portion of historical US uranium supply, creating an immediate gap that must be filled through expanded domestic production, allied nation imports, or demand destruction through reactor retirements.

North American Processing & Critical Minerals Leverage – Energy Fuels

Energy Fuels operates the White Mesa Mill in Utah, the only operating conventional uranium processing facility in the United States. This asset provides the company with operational flexibility unavailable to competitors, enabling processing of uranium from multiple mine sites while maintaining cost control through blending of feed materials. The facility commenced processing operations in 2024 and is processing material from the Pinyon Plain Mine, with operations planned to continue into 2025.

Mark Chalmers, President and Chief Executive Officer of Energy Fuels, positions the company's strategy around integration and critical minerals diversification:

"Energy Fuels is a company that is unique from all others that you'd look at because we are focused on building a critical mineral hub that is built around our uranium business but also includes the rare earth suite of elements including the ND (Neodymium) and the PR (Praseodymium) and the DY (Dysprosium) and the TB (Terbium) and potentially samarium and also the heavy mineral sands which is the ilmanite routile and zircon."

This diversification strategy addresses a fundamental reality in rare earth markets: China controls the overwhelming majority of global rare earth processing capacity, creating supply chain vulnerabilities similar to those in uranium. Energy Fuels has positioned itself to process monazite, which contains uranium alongside significant concentrations of neodymium, praseodymium, dysprosium, and terbium—the magnetic rare earths critical for defense systems, electric vehicle motors, and wind turbine generators. The White Mesa Mill is the only US facility with commercial capacity to process monazite for production of high-purity light and heavy rare earth element oxides.

The company's existing solvent extraction circuit is producing neodymium-praseodymium oxide in 2024, with Phase 1A capacity of up to 1,000 tonnes per annum. The planned Phase 2 rare earth element expansion is expected to process up to 60,000 tonnes per annum of monazite to produce up to 6,000 tonnes per annum of neodymium-praseodymium oxide plus other oxides, with commissioning targeted for 2028.

Energy Fuels projects contract deliveries of 300,000 pounds in 2025, increasing to 620,000-880,000 pounds in 2026, with a production run-rate approaching 2 million pounds of uranium oxide per year. The Pinyon Plain Mine is expected to have costs of approximately $23-30 per pound of uranium oxide, supporting the company's competitive cost positioning.

ISR Cost Curve Advantage & Flexible Contracting – enCore Energy (Producer/Ramp-Up)

In-situ recovery uranium production offers distinct advantages relative to conventional mining: lower capital intensity, faster development timelines, reduced environmental footprint, and operational flexibility to adjust production rates based on market conditions. enCore Energy operates three licensed South Texas in-situ recovery uranium processing plants, with two currently processing uranium. The company positions itself as the largest ISR uranium extractor in the United States.

William Sheriff, Founder and Executive Chairman of enCore Energy, emphasizes the scarcity value of actual uranium production capability:

"There's a real shortage… some of those certainly will be in the near future but I think the last year or two we've seen a lot of hurdles to that production. It's a lot easier to talk about than to actually do."

The company's Alta Mesa processing plant commenced operations in the second quarter of 2024, complementing the Rosita processing plant, which has 800,000 pounds of uranium oxide annual capacity. Sheriff quantifies the financial impact of dual-plant operations:

enCore's Dewey Burdock ISR Uranium Project in South Dakota was approved for US Government Fast Track Permitting on August 28, 2024. The project holds an approved Nuclear Regulatory Commission license currently in timely renewal, with Environmental Protection Agency approval and aquifer exemption held in abeyance. This positions the company for production growth beyond its current Texas operations, creating optionality to expand output as market conditions warrant.

Positioning Along the Risk Curve – From High-Grade Development to Exploration Torque

IsoEnergy has constructed a portfolio spanning development assets, restart-ready projects, and exploration targets across Canada, the United States, and Australia. This diversification provides multiple pathways to value creation while managing jurisdictional and development risk across geographies.

The company's acquisition of Toro Energy, announced on October 13, 2024, provides a flagship Australian asset. The transaction is structured as a scheme of arrangement expected to be implemented on April 1, 2026.

IsoEnergy's United States asset base positions the company to participate in domestic supply chain reconstruction. The company holds a portfolio of permitted past-producing mines including Tony M, Daneros, Rim, and Sage Plain. These assets were previously in production during prior periods of strong uranium prices, have uranium resources in place, and possess key state and federal operating permits, which saves an estimated 3-5 years relative to greenfield development.

Philip Williams, Chief Executive Officer of IsoEnergy assesses the US market opportunity:

"What's happening in the United States today is a massive change in the favorability towards nuclear power, the growth of nuclear power, and ultimately what's got to come with it rebuilding the supply chain beneath the reactors."

Exploration Scale & Carried Interest Leverage – ATHA Energy (Exploration)

High-grade uranium exploration in proven districts offers asymmetric risk-reward profiles for investors willing to accept development timeline uncertainty in exchange for discovery leverage. ATHA Energy is conducting exploration programs in the Athabasca Basin of Saskatchewan, targeting basement-hosted uranium deposits analogous to historical discoveries that have produced some of the highest-grade uranium mines globally.

Troy Boisjoli, Chief Executive Officer of ATHA Energy, characterizes drilling results with technical specificity:

"We're seeing very thick grade thicknesses of mineralization, over 26 meters of continuous mineralization downhole with 13 meters of continuous with about 1.9 meters of high grade within it."

ATHA Energy's exploration strategy focuses on outlining deposit scale. Boisjoli articulates this approach:

"The reason they’re aggressive [the step-outs] is that our intention is to outline the scale that we see here on this system."

The company completed a 10,000-meter diamond drilling program at its Angilak Project in 2024, with the Mineralized Rib Corridor discovered in 2025. ATHA holds the largest land package in the Basin at 3.8 million acres and the largest uranium exploration portfolio in Canada at over 7 million acres. Bojlis emphasizes this advantage:

The Investment Thesis for Uranium

The structural case for uranium investment rests on supply-demand fundamentals that have materially improved and are projected to tighten further through the remainder of the decade:

- Structural supply deficits persist through 2030 even under aggressive supply expansion scenarios, with secondary supply sources declining as enrichment underfeeding becomes uneconomic and government stockpiles are depleted or reserved for strategic security purposes.

- Policy-driven demand visibility has strengthened through legislative support for nuclear energy, reactor life extensions, and small modular reactor deployment commitments, creating multi-year demand growth insulated from economic cyclicality.

- Security-of-supply premiums are emerging as Western utilities and governments prioritize supply chain diversification, creating valuation premiums for companies operating in stable jurisdictions with transparent regulatory frameworks.

- Operational leverage and cost curve positioning favor companies with existing processing infrastructure, restart-ready assets, or high-grade resource endowments that can deliver production at competitive costs.

- Exploration and optionality provide asymmetric return potential through resource expansion at existing projects or new discoveries in proven uranium districts.

- Diversification across the uranium value chain enables portfolio construction that captures near-term cash flow from producers, development optionality from restart-ready projects, and exploration leverage from high-grade targets.

Volatility as an Entry Point into a Long-Duration Energy Security Theme

Uranium price volatility in 2025 has created entry points for investors seeking exposure to the nuclear fuel supply gap. The structural deficit between primary uranium supply and reactor requirements persists despite short-term price corrections, with supply response constrained by capital intensity, permitting complexity, and cost inflation. The companies highlighted represent differentiated approaches to capturing value: Energy Fuels leverages North American processing infrastructure and critical minerals diversification, enCore Energy provides operational ISR production with expansion optionality, IsoEnergy offers geographic diversification and restart-ready assets, and ATHA Energy delivers exploration leverage in proven uranium districts. For institutional and sophisticated retail investors, these companies provide exposure to near-term production, development optionality, and exploration upside while operating in jurisdictions with regulatory stability. The structural supply deficit remains the dominant fundamental driver, and volatility represents opportunity rather than deterioration of the long-term investment case.

TL;DR

Uranium spot prices corrected in early 2025 after speculation unwound, but structural supply deficits remain intact. Global reactor demand of 179 million pounds exceeds primary mine production by 30-40 million pounds annually, with secondary supplies declining. Western utilities prioritize supply chain diversification following Russian import restrictions, creating premiums for North American producers. Energy Fuels operates the only US conventional processing mill while diversifying into rare earths. enCore Energy provides low-cost ISR production with expansion capacity. IsoEnergy holds restart-ready permitted mines across multiple jurisdictions. ATHA Energy targets high-grade Athabasca Basin discoveries. Legislative support, SMR technology, and data center partnerships drive durable demand growth, making price volatility an entry opportunity into a multi-year supply-constrained cycle.

FAQs (AI-Generated)

Short-term volatility resulted from speculative unwinding and secondary supply (inventory drawdowns, enrichment underfeeding) entering the market. However, these secondary sources are finite and declining, while the structural 30-40 million pound annual deficit between primary production and reactor demand remains unchanged.

US legislation prohibiting Russian uranium imports eliminates a material portion of historical supply, creating an immediate gap that must be filled through expanded domestic production or allied nation imports. This policy shift increases the security-of-supply premium for North American producers.

ISR offers lower capital intensity, faster development timelines, reduced environmental footprint, and operational flexibility to adjust production rates based on market conditions compared to conventional mining methods.

It's the only operating conventional uranium processing facility in the United States and the only US facility with commercial capacity to process monazite for rare earth production, addressing supply chain vulnerabilities in both uranium and critical minerals for defense and clean energy technologies.

This cycle features higher-quality, more durable demand drivers including legislative frameworks (ADVANCE Act, EU taxonomy inclusion), energy security mandates, small modular reactor technology, and genuinely incremental demand from data center partnerships—creating policy certainty that extends beyond electoral cycles.

Analyst's Notes

Subscribe to Our Channel

Stay Informed