K92 Mining (KNT) - 350,000oz Gold Production in 2026

Matthew Gordon spoke with John Lewins the CEO of K92 Mining Inc. (TSX:KNT) to discuss the company’s recent activities and record past financial year.

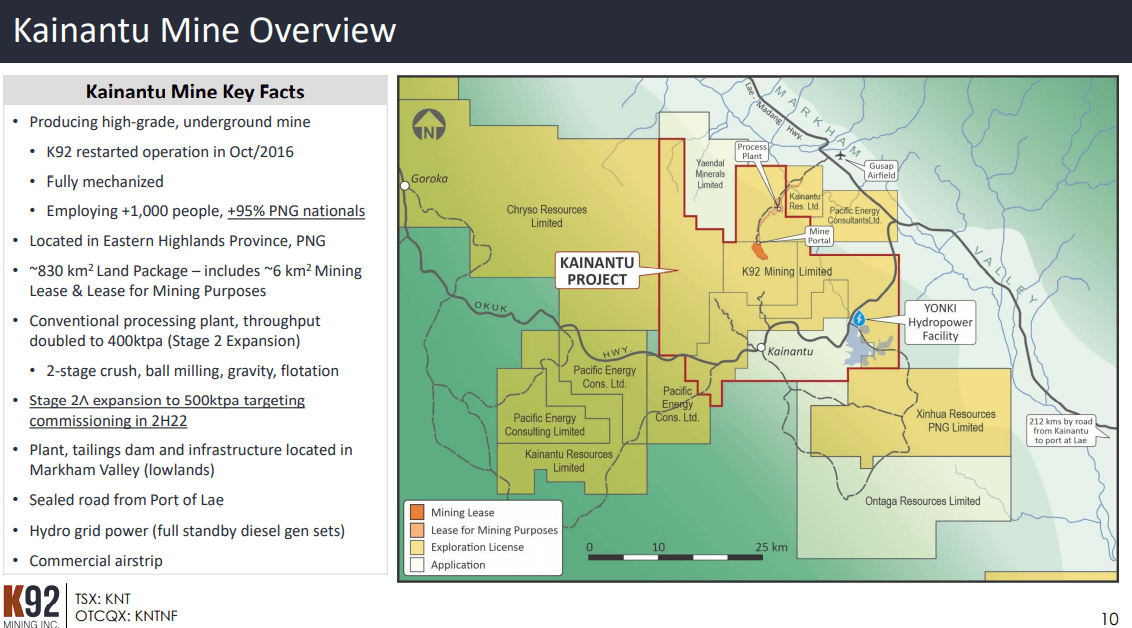

K92 Mining Inc. is a mineral exploration and development company that owns and operates the Kainantu Gold Mine located in the Eastern Highlands province of Papua, New Guinea. The Kainantu Gold Mine is a high-grade, low-cost underground mine within an 860 square kilometre land package in a region known for Tier 1 deposits.

Matt Gordon caught up with John Lewins, CEO and Director, K92 Mining. Mr. Lewins is a mineral engineer with over 35 years of experience in the mining industry. He has previously worked in Africa, Australia, Asia, North America, and the former Soviet Union. He previously served as the Chief Operating Officer for K92 mining from May 2016 to August 2017. Mr. Lewins has successfully managed the development of a number of open pits and underground gold, precious, and base metal mines from Feasibility Study through to profitable operations.

He has operated extensively at the corporate level in various roles from Executive General Manager to Director and CEO with a number of other mining companies including MIM Holdings, First Dynasty Mines, Platinum Australia, and African Thunder Platinum. He received his National Diploma for Technicians (Extractive Metallurgy) from Technikon Witwatersrand, South Africa, a Bachelor of Science degree (Honors) in Mineral Engineering from the University of Leeds, England, and a Graduate Diploma in Management from the University of Queensland.

Company Overview

K92 Mining is a mineral exploration and development company. It was founded in 2010 and is headquartered in Vancouver, British Columbia. The company is listed on the Toronto Stock Exchange (TSX: KNT) and the OTC Markets (OTCQX: KNTNF). K92 mining was recognized among the best 50 companies on the OTCQX in 2021. Its flagship asset is the Kainantu Gold Mine, located in the Eastern Highlands province of Papua, New Guinea, which was acquired in 2014 from Barrick Gold.

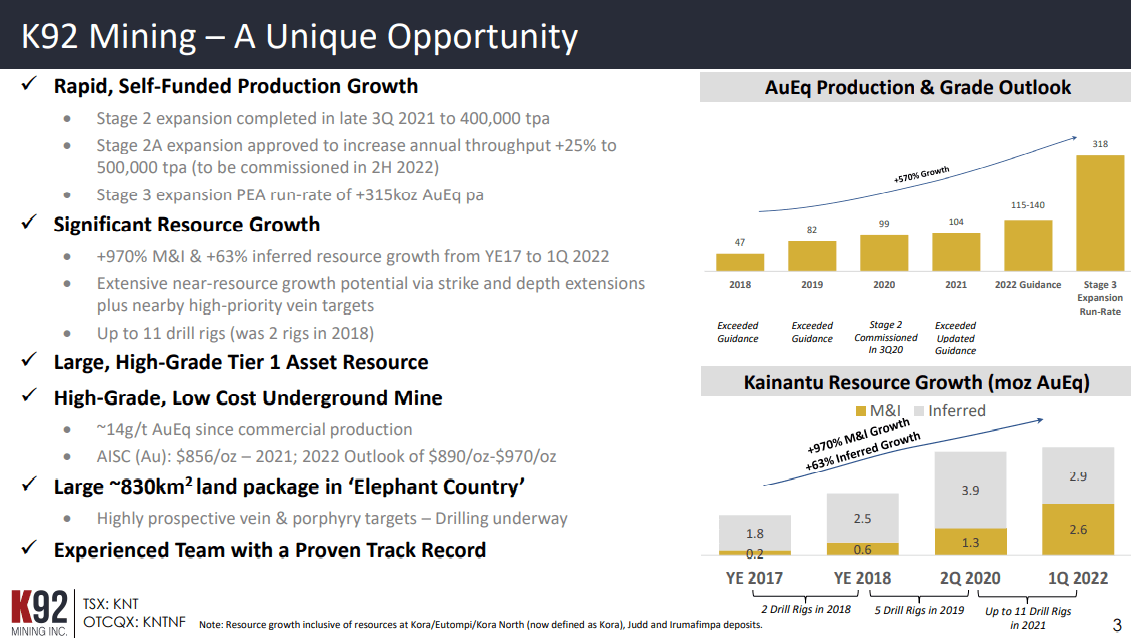

K92 Mining operates the high-grade K92 mine in Papua, New Guinea. This is one of the highest-grade mines in the world. The company recently had a record year in terms of production numbers. It has plans to expand the current yearly production from 100,000oz to 350,000oz by the year 2025.

Q4 Results

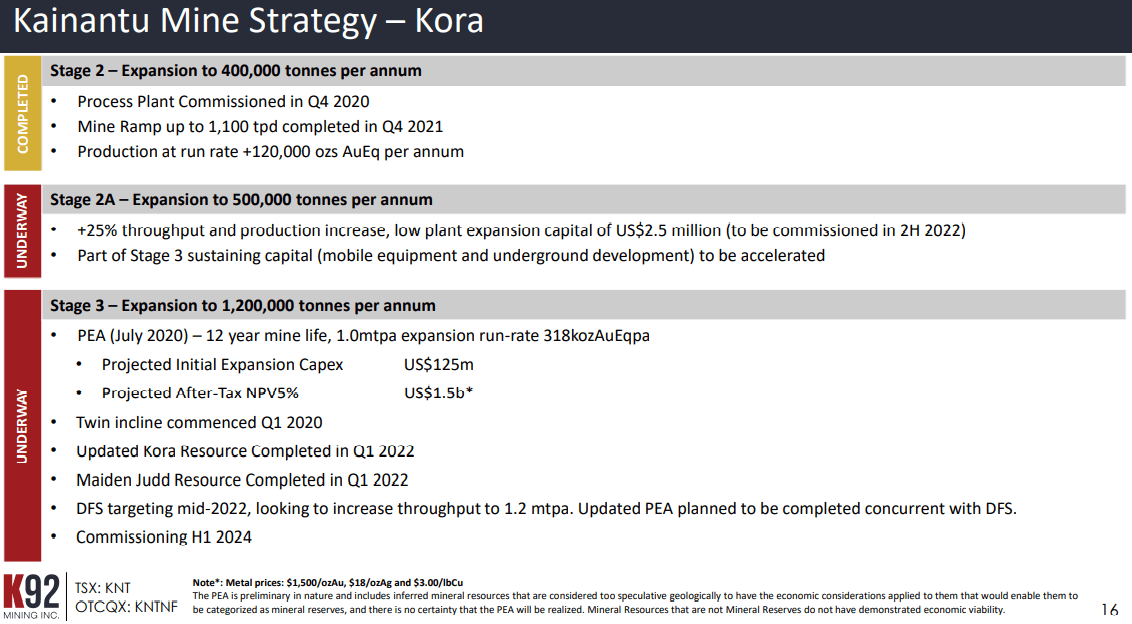

Last year, K92 Mining commissioned Stage 2 expansion for its mine, doubling its yearly throughput from 200,000oz to 400,000oz per annum. By Q4 2021, the company was able to expand the throughput to 99,713t. This expansion resulted in the company achieving a record gold production of 36,000oz gold equivalent. Notably, these are the production numbers in the company’s history.

For the fourth quarter, the company had $456/oz gold in cash costs along with $672/oz in AISC (All-in Sustaining Costs). During this time, the company also brought out its first stop material from the new Judd Vein. Additionally, the company commissioned a new gravity circuit. The company ended the year with a record annual tonnage of over 336,000t, a 46% increase from the previous year. The company achieved a record annual production of 104,000oz gold equivalent, with $614 in cash costs along with an AISC of $856.

K92 Mining was able to beat its data guidance which was $670-$720 cash costs and $920-$970 gold. It is important to note that the company has achieved these numbers while simultaneously working on expansion plans.

Guidance Metrics

For 2022, K92 Mining has set guidance metrics between 115,000oz-140,000oz. The relatively wide guidance has taken the potential impact of covid into account. Notably, the company lost about 20,000oz in production due to the pandemic and also had to expend direct costs to deal with covid. The direct costs included expanded rosters, quarantining, and testing, bringing the company’s production costs to about $60 an ounce.

Ongoing Operations

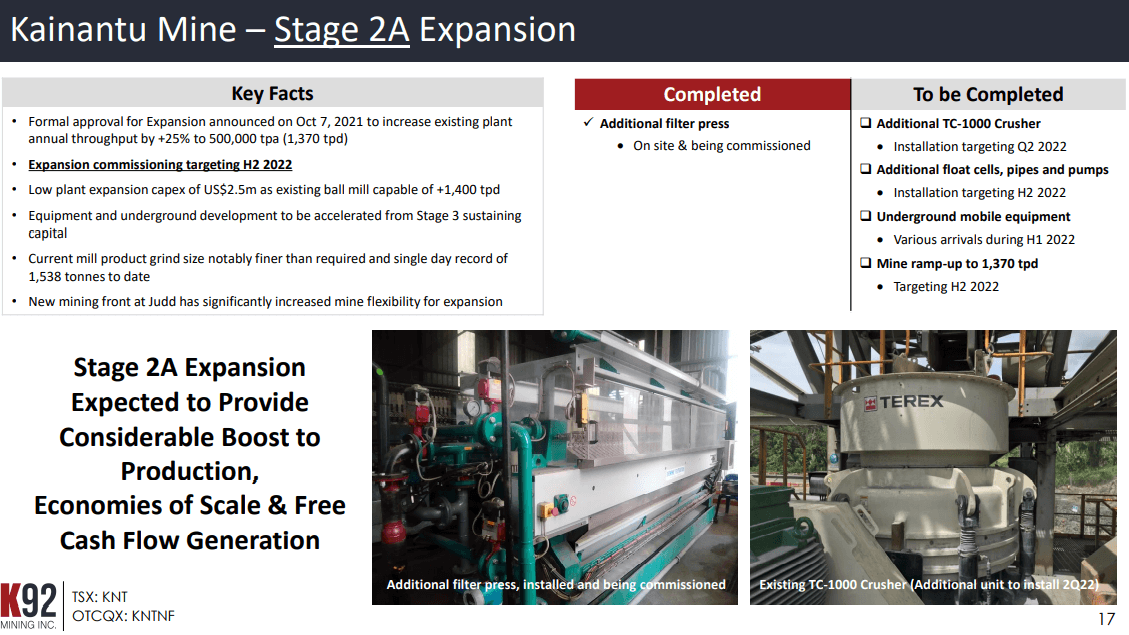

K92 Mining is working on a DFS (Definitive Feasibility Study) and a PEA (Preliminary Economic Assessment), which are a part of the Stage 3 expansion, that will bring the company’s annual production to 1.2Mt. This year, the company is focused on Stage 2A expansion that would expand the throughput and production by 25%, increasing the production from 400,000t per annum to 500,000t per annum. Stage 2A is set to be commissioned by Q4 2022.

The company is currently working on a twin incline that is more than a kilometre in length. It is involved in multiple areas of camp expansion that comprise a brand new workshop. In addition, it has a 700m raised board going into the vent shaft that is 5m in diameter. The increase in throughput would enable the company to reach between 300,000oz to 350,000oz in annual production. An increase in production will drive the company’s cash costs and AISCs down. The company’s original PEA had a 1Mt/annum production with a $1.5Bn NPV (Net Present Value) at $1,500/oz gold and $3/lb copper.

K92 Mining recently announced a resource update for the Kora asset and a maiden resource for the high-grade Judd vein system. The company is looking to increase its M&I (Measured and Indicated) resource to feed into the DFS. It was able to increase the resource to 2.3Moz in the M&I category along with 2.6Moz in the Inferred category. In essence, the company was able to increase the number of ounces while still producing 200,000oz.

The company has a major focus on underground drilling, with 6 rigs deployed for resource expansion. The Judd bit is over 300,000oz in gold equivalent ounces and offers significant expansion potential. It is important to note that the company has only drilled 20% of the area within its mining lease which is covered by Kora and a system that runs parallel to Kora.

Drill Operations

Outside the mining lease, K92 Mining recently completed its first-ever drill at Kora Judd South. The veins are going southwards of the existing mining lease. The modelling estimates that the Kora vein system extends 1km to the south. The company anticipates that the Judd system must also extend 1km to the south. This effectively doubles the strike length as the company already has a 1km strike length within its mining lease.

The company has reported on 2 drill holes so far, that were drilled 75m and 150m to the south. It is currently working on a series of fence lines that are going southwards. Both these holes offered results that were better than expected. The first hole was drilled 75m along the strike length, intercepting 2 Judd veins with higher-than-average grades of 1.3m over 16g and 0.9m over 15g.

At Kora, the company went through the K1 vein with grades of 0.9m at 36g/t, while the K2 vein returned grades of 6.2m at 17g/t. These grades were higher than average. At K3, the company found grades of 5m at 8g/t. The company found that the K2 and K3 were based in a dilatant zone where 36m at 6g/t gold equivalent grades were found.

Notably, 80% of the value comes from copper which has a rich presence here. The core of 2 of these veins feature 1m over 20% copper. The first hole was drilled 75m along strike length, while the second drill hole wasn’t successful in getting into the core. The grades for the Judd One vein averaged 2.9m at 9.5g/t. The second vein had grades of 15m at 16g/t, which are well above average for Judd.

The dilatant zone incorporates the two veins and features 66.5m at 5g/t with about 30% of the value coming from copper. 75m east of this hole, the company encountered a vein that carried grades of 3.5m over 10g/t gold equivalent. Notably, this plane had never been drilled before. The company anticipates that this is a whole new vein system that is potentially opening up. Both holes have shown to have an endowment of metal four times greater than the mining lease. There are several indications that this area features a huge endowment of metal.

K92 Mining expects to see higher copper presence as it moves south because the copper seems to be heading towards the porphyry which is believed to be the source of all the mineralization. The company currently has 2 drill rigs employed here, along with a planned third rig that would be deployed in the third quarter in order to expand production.

At the Karampe Vein system, K92 Mining has had one of the best drill results with 3.5m of 15g/t. This is the company’s secondary target after Kora South and Judd South. Interestingly, all the underground developmental work carried out by the company sits between Kora and Judd, which are located 150m apart. As a result, the area has an immediacy for development as the company extends both Judd and Kora to the south. Once the twin incline is in place, the company will extend Judd and Kora at depth as well.

Cash Position

K92 Mining has funded all its expansions internally. It plans to continue self-funding in the main part of the deposit, in order to avoid dilution. The current metal pricing has also instilled confidence as the company expects to see an increase in the project’s CapEx (Capital Expenditure). The industry as a whole has seen a significant escalation in prices. The company expects the same for the project as well as the DFS. Despite the increased expenditure, the company anticipates that it will have sufficient cash flow from the operation to build the project and fund exploration. In 2021, K92 Mining was the largest explorer in Papua, New Guinea. The company is looking to be the largest explorer in the country this year as well and has allocated about $15M on exploration.

Additionally, the company is looking to spend around $90M on CapEx along with sustaining CapEx that includes the twin incline, expansion capital, and more. Last year, the company was the second-highest taxpayer in the mining space in Papua, New Guinea. In Q1 2022, the Prime Minister’s office published a press release noting that K92 is a good corporate citizen and a significant taxpayer.

K92 Mining is covered by 14 analysts, the highest in the sector. This indicates the potential and interest in the company’s assets. The company is the recipient of the Thayer Lindsley Award for the best global discovery from PDAC (Prospectors & Developers Association of Canada). The quality of Kora and the work gone into finding the asset is well-recognized.

The company’s institutional shareholder base includes 1832 Asset Management, RBC (Royal Bank of Canada), Fidelity Institutional, Donald Smith & Co., Equinox Gold, and more. The company is highly north-American-centric. However, the company is looking to further expand its institutional shareholder base into Europe, Asia, and Australia.

On the retail side, the company’s shareholder base is dominated by North Americans, primarily Canadians, however, the company also has a substantial US retail shareholder base as well. As per the company, it has the right mix of both retail and institutional shareholder base. For the past 2 years, the company has majorly focused on expanding its M&I. However, this year, it is focused on a major resource expansion.

Expansion Plans

K92 Mining is looking to publish an updated Kora resource and Judd’s maiden resource by Q1 2023. Currently, it has 2 surface and 4 underground rigs working on resource expansion. The company is looking to increase the number of both surface and underground rigs, further accelerating the expansion process.

In December last year, the company flew the largest aerial geophysics program in Papua, New Guinea in the past 15 years. The company was able to generate a large number of new targets within an 800-square-kilometre area of mining and exploration leases. It is looking to balance the expenditure between exploration and expansion. This is because the company is mindful that exploring such a large number of targets would have significant cost considerations, despite the highly-favourable metal pricing.

K92 Mining was able to enter production early and achieved the target throughput at the Kora deposit within 4 months. It recognized the exceptional possibilities at Kora in terms of strike length, drilling, hit rate, and more. The company was looking to expand its existing plant where it had the opportunity to double the throughput. It spent a relatively low $15M and was able to double the output on the back of the PEA. Following this, the company continued to expand its resource and the plan for the next stage. The next stage in the process was to reach 1Mt in yearly production. At this point, the company had $1.5Bn NPV5 for an outlay of $125M. The company realised that it could internally fund the sustaining capital cost which was estimated between $115M to $240M.

The company took the project through a Feasibility Study while completing the expansion towards a 400,000t annual production. It started with a smaller capacity in order to avoid debt or the need to raise equity. It was able to fund operations through the existing cash flow. This would help bring the project to the next phase. For the next phase, the company is looking at a 1.2Mt annual production instead of 1Mt. It has recognized 2 km of potential strike length that is currently being drilled. The actual depth of the deposit is currently unknown, however, every hole drill at depth has hit mineralization with commercial grades and thickness.

The company is looking to deploy the twin incline early in the next phase. Committing to a 1.2Mt operation would require the twin incline to be a certain size. The twin incline would also enable the company to potentially work towards stages 3,4 and 5 of the operation. This could lead the company to a 5Mt operation with a conveyor system in place. K92 Mining is already carrying out preliminary work on the same.

The quality of the deposit is exceptional, in fact, it is the third highest grade in the world, and the company is working towards developing a 5Moz underground resource. It has worked hard to ensure that it can provide as much measurable information as possible so that the potential for the deposit would be recognized in the market.

M&A and Listing Considerations

Covid has given K92 Mining the opportunity to establish its position in terms of production and the completion of a DFS. Interestingly, all the concrete used in the project was produced by the company, while all the steel work done on the project was sourced locally. The company wanted to ensure that it can conduct as much in-house work as possible. It is open to a potential M&A (Merger and Acquisition) in the future. Papua, New Guinea has enabled K92 Mining, a junior company to effectively have a tier 1 asset in its portfolio. According to the company, the endowment in its leases is among the best in the region.

K92 Mining is currently happy with its TSX and OTC listings as it has access to both major North American markets. As per the company, TSX values companies operating in Papua, New Guinea higher than the ASX. As a result, the company isn’t looking to get listed on the Australian Stock Exchange in the near future.

To find out more, go to the K92 Mining website

Analyst's Notes

Subscribe to Our Channel

Stay Informed