Marimaca Copper (TSX-V: MARI) - Project Advancing on All Fronts

Interview with Hayden Locke, President & CEO of Marimaca Copper Corp. (TSX: MARI)

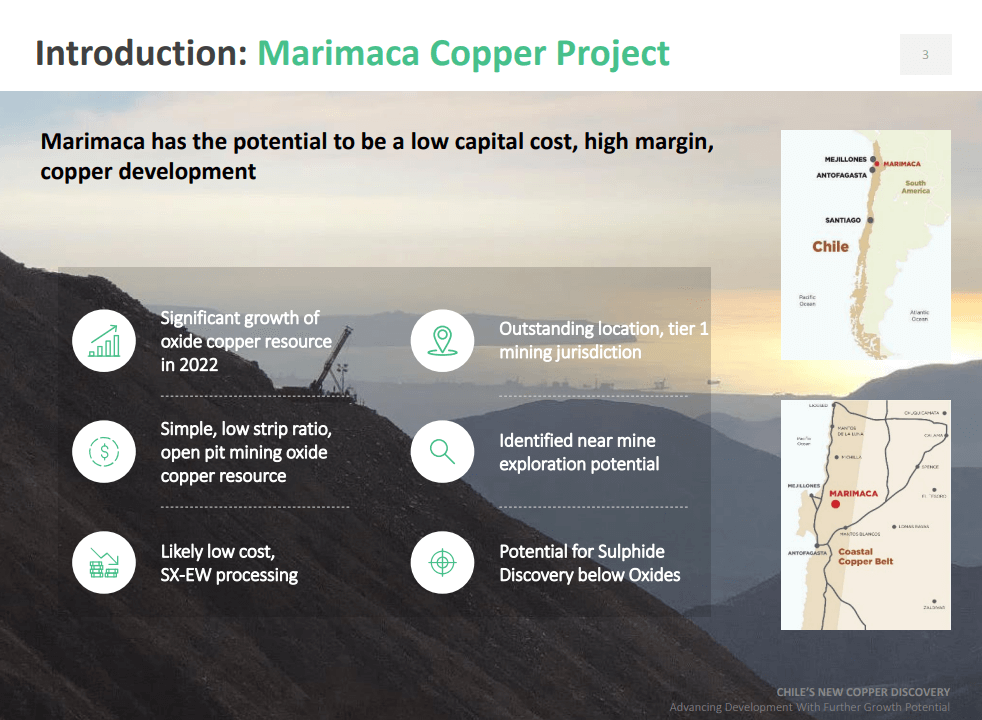

Marimaca Copper Corp. is a Canadian copper exploration company focused on exploring and developing new copper resources to supply an increasing global demand for this essential commodity. The company's flagship asset is the Marimaca Copper Project in Chile's Antofagasta region. It is the only copper discovery made globally within the last five years. It is a low-risk project that offers substantial exploration potential.

Merlin-Marr Johnson caught up with Hayden Locke, President, and CEO, Marimaca Copper. Hayden has extensive experience as a mining executive with a significant part of his career spent developing and leading successful LSE and ASX-listed mining companies. He has previously worked with J.P. Morgan and Barclays Natural Resource Investments. As of 2018, he has served as the CEO at Emmerson Plc, a Morocco-based potash development company where he currently holds the Director position.

Company Overview

Marimaca Copper (formerly known as Coro Mining Corp.) is a copper exploration and development company. It was founded in 2004 and is headquartered in Canada. The company is listed on the Toronto Stock Exchange (TSX-V: MARI) and the OTC Markets (OTCQX: MARIF). Compañía Minera Cielo Azul Ltda, Minera San Jorge S.A., Minera Coro Chile Limitada, Minera Rayrock Ltda., Machair Investment Ltd., Rising Star Copper Limited, and Sea To Sky Holdings Ltd. are the company's subsidiaries. The Marimaca Project has been one of the most important copper oxide discoveries in northern Chile for over a decade. The company believes that it has the potential to be one of the best open-pit copper oxide projects globally.

The Copper Market

In recent times, the copper market pricing has bounced back to $9,000/t. Copper companies were cognizant that due to a small surplus in supply, copper pricing would be under pressure in 2022 and 2023. There was a bit of pressure on the copper market last year, which was driven by a general fear of global recession, however, this seems to be abating. Based on the numbers coming out of the inflation, many believe that the peak levels have already been reached. As a result, a loosening of monetary policy is expected, which, in turn, could lead copper companies back into a growth phase, leading to a fair bit of excitement in the market.

There have also been other issues with copper-producing assets that aren’t producing at the expected levels. The problem is further magnified by the combination of restocking, demand, and relatively low inventory levels. According to the company, all the research indicates that 2023 is going to be a relatively strong year for copper. The company is highly-bullish on copper over a 10-year timeline.

In recent times, there has been an increased focus on electrification across the globe. Large development projects are in decline and are suffering from falling grades. Recently, Codelco’s CEO announced that it will be producing 1.7Mt copper per annum. However, if the company is unable to acquire funds to reinvest into the operations, the company could cut down production to 400,000t. The amount of money required simply to maintain a 1.5Mt-1.7Mt of yearly copper production is astronomical. According to Marimaca Copper, Codelco would need to invest around $40M over the next 20 years simply to maintain production. Financing becomes increasingly challenging in a rising interest rate environment. Increased pressure is expected on operations rather than the potential for expansion.

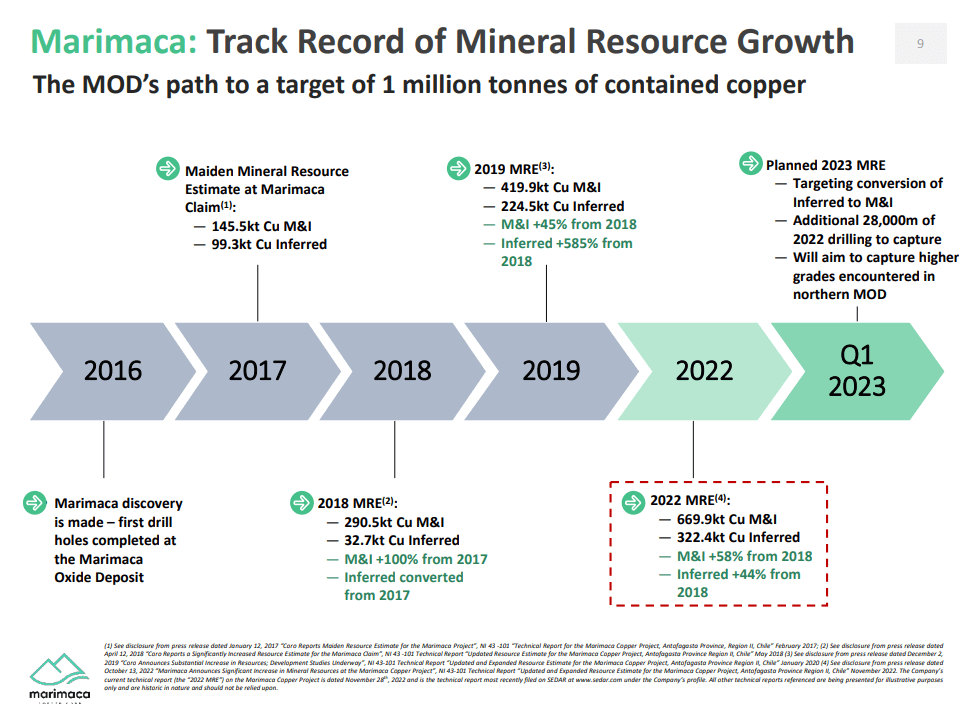

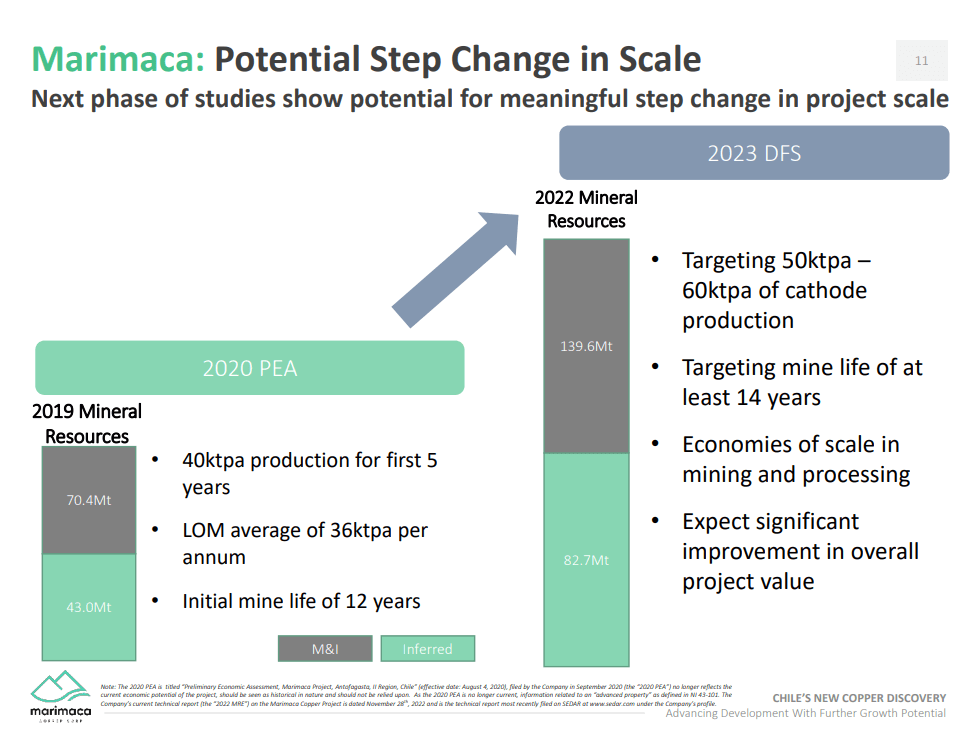

Marimaca Copper Project is one of the few projects that can be built in the short term or a 5-year development timeline. While this is great news for the company, it is concerning for the copper market and the people that need to source copper. The Marimaca Copper Project is an exceptional development-stage copper asset. Back in 2020-2021, the project lacked the scale that would make people take notice. In the copper industry, there’s an arbitrary threshold of a million tons of contained copper in a project. Over the past 2 years, the company has been focused on addressing this aspect by drilling the discovery at depth and trying to develop a resource.

Ongoing Operations

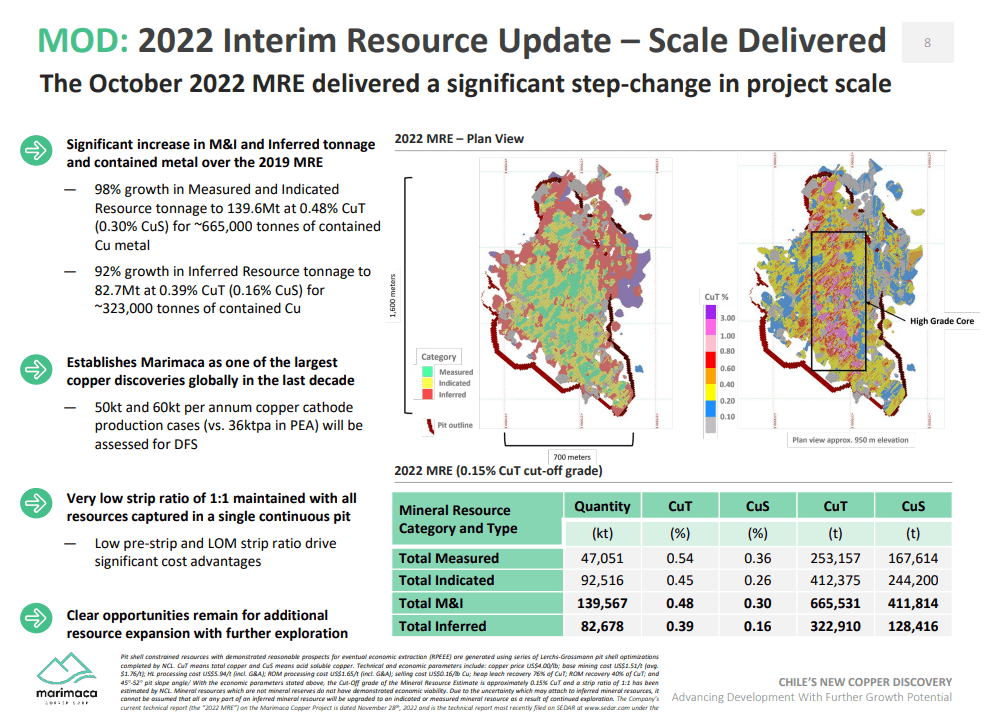

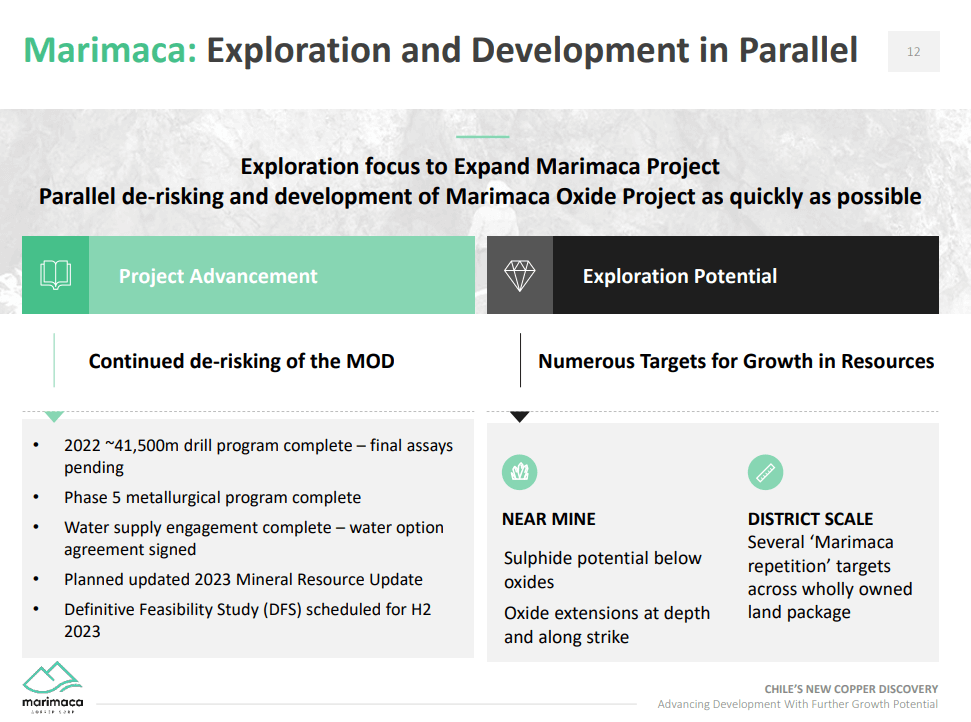

The company carried out a 40,000m drill program and delivered a resource upgrade in October 2022. The resource update led to exceptional results with a 100% increase in resource tons. This enabled the company to reach the million-ton contained copper threshold. This development has been transformational for the company as it went from a 40,000t a year production for a 12-year mine life to a potential 50,000t-60,000t production for a mine life between 12-15 years. This year has been exceptional for the company from a mineral endowment perspective. The company anticipates that this would also lead to a significant jump in the project’s value. The Marimaca asset continues to have a very low strip ratio, a great location, and low capital costs of production, all the fundamentals that made it a great project in the first place. From a value perspective, 2022 has been a transformative year for the company.

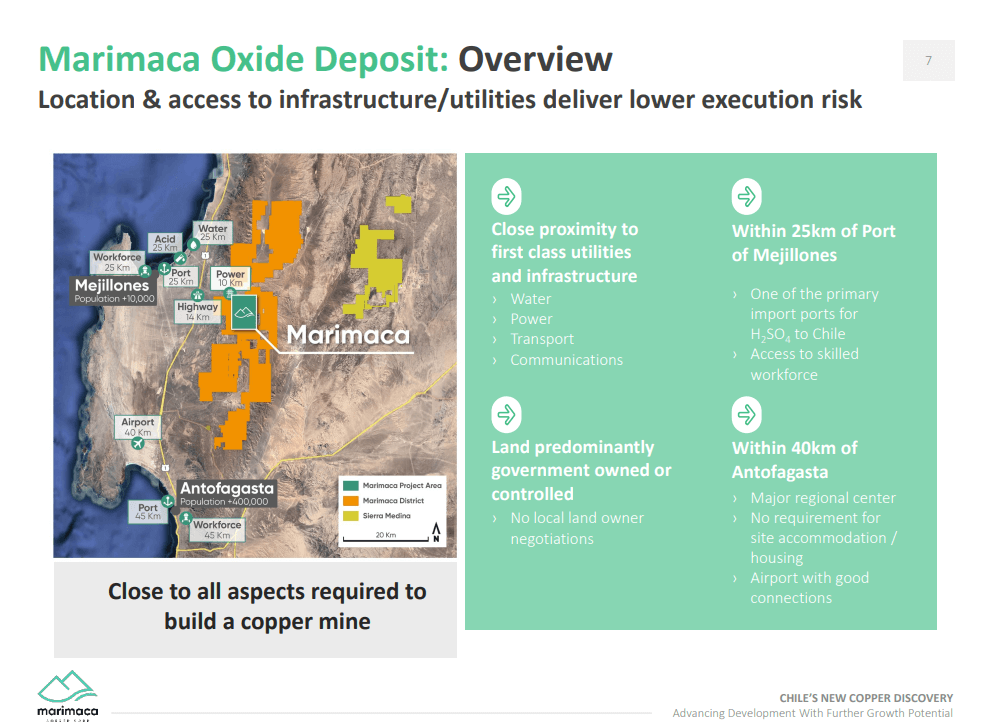

Preparing for the next phase of operations, the company is looking to go from concept to construction and then production. One of the biggest issues that every mining company faces is access to the water supply. The water supply issue is even bigger in Chile, specifically in the Antofagasta region. The company signed an option agreement that has helped it secure a water supply for a larger-scale project. This is a major de-risking milestone for the company.

The company has also completed all the preparation work required to obtain a mining permit in Chile. It found that there’s minimal impact on issues that could make it difficult to obtain a permit. This has been confirmed through the work done in 2022.

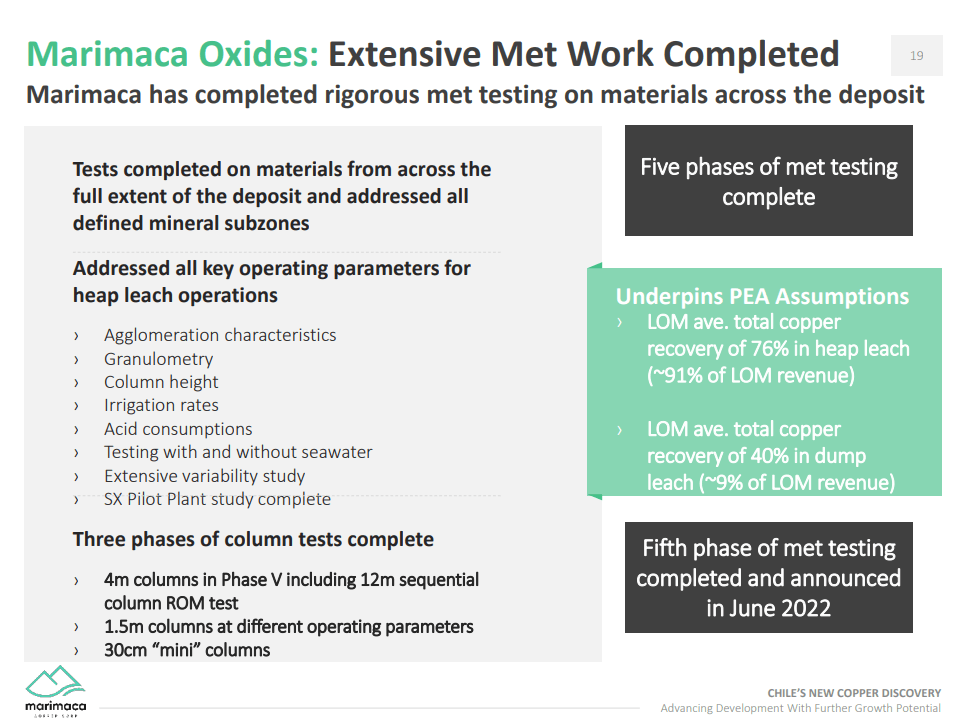

It is important to note that the company will be using seawater for mine operations. The option agreement was signed with one of the local power stations in Mejillones Bay that possesses water extraction rights. As per the deal, the company will build a pipeline to the project and the power station will provide the water supply. Based on the design work and metallurgical testing, the company assumes that untreated seawater will be used in the project. The company does not need to use freshwater, which would require massive aquifers and would cause a massive public backlash in Chile. The company does not need to install an expensive desalination plant as it can directly use untreated seawater.

Adding salt to the leaching solution helps improve the leaching kinetics. As a result, using seawater is actually beneficial to the processing. The company intends on adding salt to the agglomeration phase as it improves the overall recoveries and leach kinetics by a couple of percentage points. It hasn’t found any clear benefits from having chloride in the oxide zone, but there aren’t any negatives either. While the company would need to manage the salt before the solution goes into the SW-EW (Solvent Extraction and Electrowinning), using salt offers incredible benefits for the project.

In Chile, there has been a law proposal that could change the tax bracket for a company once it goes past 50,000t per annum production. Once the production goes beyond this point, there’s an incremental royalties scale. If a company mines 49,999t, the average royalty load is around 2%. However, if the production surpasses the 50,000t mark, the company is charged an additional 5% royalty.

According to Marimaca Copper, the law is currently under discussion and is yet to be formally enacted. The company will factor in the post-tax impacts of the new fiscal regime while considering the scale of the DFS (Definitive Feasibility Study). While it does make sense to produce 60,000t, at higher copper prices, the company is likely to take a 50,000t project into the DFS in case the law is enacted.

In the previous year, the company added tons to the existing resource by incorporating more lower-grade material. This led to a fall in average grades. As per the company, this is the function of the commodity price assumptions. In an ideal scenario, the company would prefer the grade to stay the same or go up as the size of the project is increased. While the grade is considered king, the assumption does not take into account other aspects of the project. It is important to analyze these aspects in order to determine whether a project is profitable or not.

One of the biggest positives for the Marimaca Oxide project is that it features an incredibly low strip ratio of 1:1. This means that for every ton of usable material moved, the amount of waste is significantly lower relative to the vast majority of other projects. Comparing other projects while accounting for the strip ratio leads to a 1% grade. Since the per-pound cost of mining is lower, it ends up being a significantly higher-grade project. At $4/lb, the economic cut-off grade for the Marimaca project is 0.15%. This means that the operations will be profitable if 0.15% material is processed through a heap leach operation. Based on this, the 0.45% or 0.5% cut-off is well above the economic grade, and the company expects to generate significant revenue.

In the first 5 years of the mine plan, the high-grade core of the project is the first part of the mining process. This means that all the capital costs that have been expended on the project are paid back very early, providing a better return on invested capital. Once the capital is paid back and the money is returned to the investors, the effective economic cut-off grade excluding the CapEx (Capital Expenditure) tends to be lower. Furthermore, the company has the ability to carry out dump leaching, which can lead to a lower grade. This is because the dump leaching process used significantly less acid and crushing. The company isn’t dissatisfied with the material grade. It is concerned with the period of the mine life, and the return on investment capital, which is expected to be exceptional.

Marimaca Copper is looking to publish the resource towards the end of Q1 or early Q2. The last drill results are coming in and the team is currently working on it. The company is looking forward to the next batch of drill results, which will be from the new high-grade center at the northern end of the pit. The results will be exciting for the company from a grade perspective in the northern end of the deposit. It might require a slight change in the mine plan because of the near-surface high-grade material in the northern end. As part of the 2023 strategy, the company intends on delivering the resource. The critical path for the project is to acquire permits and go from the current position to first copper production.

In the early part of 2023, the company will majorly focus on addressing the sulphide drill hole. At the same time, the company is carrying out the work needed to submit a permit and mine building application by Q3 or Q4 this year. This way, as the project goes through the system, the company will receive real-time feedback from the authorities on the environmental management perspective. It can then use this information and incorporate it directly into the planned DFS, saving a lot of time on the back end. In essence, permitting will be the main focus in the early part of 2023. The DFS is expected to have a relatively short timeline as all the other work required to complete the study has already been done.

The new resource will feed into the Feasibility Study, following which the company will focus on a DFS. The resource that was published in March-April is targeting 90%+ in the M&I (Measured and Indicated) category, enabling it to declare a decent size reserve once the DFS is delivered.

Marimaca Copper could potentially deliver the DFS in 2023, however, to achieve this, it would need to commence the study at the start of Q3. Additionally, the company would also need to manage the finances and resources in order to publish the DFS. Even though permitting would be the biggest value add-on for the project, the company would need to take some resources off the permitting process in order to focus on the DFS. From an engineering perspective, moving the project forward and shortening the timelines to reach construction would be the biggest value add-on.

Cash Position

Marimaca Copper has $15M in current cash flow. The capital is sufficient to carry out all the planned work in 2023. Around late 2023-2024, the company would need to look at financing options for the next stage. In fact, the company is starting to get close to a decision where it will look at bigger capital sources in order to take the project through to production. The Marimaca project is exceptional, and it is on the radar of several potential funding partners. As a result, the company isn’t worried about financing the next stage. Instead, it is focused on moving the project forward as quickly as possible and achieving the best possible deal for current shareholders.

Drill Operations

While working on a geological and geotechnical hole, the company hit sulphide mineralization that was trending towards the north side of the pit. Here, the company found a 240m hole featuring 1% copper with 92m at 2%. It also found 100m at 1.7% copper.

In 2020 and 2021, the company carried out a lot of work around targeting a potential depth extension for the project. Based on the feedback, the company anticipates the presence of the sulphide feeder zone at depth. It has been trying to determine the scale of the zone. Through drill operations, the company realized that there was a high degree of association between magnetic susceptibility and the presence of higher-grade primary mineralization. It used the data to try and target the zone through a drilling program. While looking for the sulphide extension, the company ended up making the Marimaca mixed oxide discovery. The company found that the oxides extended quite significantly at depth.

The company was targeting a large-scale magnetic anomaly at depth that was looking to the north along with an easterly dipping altitude to all of the structural controls in the Marimaca oxide project at the surface. The issue arises when trying to target deeper mineralization. The company would need to drill on the eastern periphery, and the drill depth required to test the targets is between 1,000m-1,500m. Drilling at this depth would be significantly more expensive than the company is looking to spend.

This drill hole is called MAD-22 which is drilled in the opposite orientation, making it a significantly shallower hole. The risk here was that the hole was drilled down the dip to the extent of the structures from the surface. The hole intersected 120m+ at nearly 1.7%, where the majority of the material was found within chalcopyrite. The true width of the zone is between 30m-50m. The company anticipated that something interesting could be found, and as a result, it revisited the drill hole to determine the reason for the mineralization’s existence. Here, the company once again saw a very strong association with the magnetic high. From a planning perspective, this is a magnetic inversion model and MAD-22 appears to be right in the middle.

The company is currently revisiting all the drill results from the project in order to try and identify the logical place to follow up. It is looking to test the theory that there is a sulphide body of significant scale below the Marimaca pit. The depth of the discovery in relation to the pit is an interesting aspect. The chalcopyrite mineralization is expected to be open-pitiable. At a 1.7% grade, if there is enough material to have scale, this could be an incredibly profitable ore body especially if it hangs together and has continuity at depth.

Marimaca Copper is currently looking at magnetic susceptibility and its correlation to the highest-grade mineralization. The company has found almost a perfect correlation between the spikes in grade and magnetic susceptibility. It is looking to follow up on the targets that have the magnetic high. From a logical perspective, the company is following up on either side of the MAD-22 prospect, stepping to the north and south as the drill hole is in the middle of the magnetic high. Further north, the company found some magnetic highs that are on the same structure that controls the Marimaca Oxide project along with Mercedes and Cindy further to the north.

As a result, the company took a step back and realized that maybe it wasn’t targeting well enough relative to the location of the magnetic anomalies. The company put out an announcement last year that provided a volumetric calculation of the magnetic anomaly, which was around 170-180 cubic meters. At this specific gravity, the company has a magnetic anomaly scale between 400Mt and 500Mt. The company intends on following up on these targets and include them in the next phase of drilling in order to have the best possible chance at success.

The company is approaching this with an expectation to carry the momentum towards production, which is fundamental to delivering the maximum value for shareholders. It will also address the finding as it could potentially be a game changer for the company. The company has assigned Sergio Rivera to this task. Sergio is a geologist that brings nearly 40 years of experience to the role. The company is focusing on a tightly gated process where 4-5 holes will be drilled at a cost of under half a million dollars before stopping the operations.

Once the financing for the next phase is complete, the company will determine whether it has sufficient information to follow up on the targets. While half a million dollars is a considerable spend, the company believes that the size of the price sitting below the deposit is well worth the expenditure.

According to the company, the project is still in the early stages of discovery. It is a true greenfield discovery made by Marimaca Copper’s team. The MAMIX zone is one such example where the company hadn’t expected the oxides to extend to such a depth, but it did. As drilling continues, the company is gaining a better understanding of the deposit. It is continually finding new areas of prospectivity and areas that suggest that the deposit will continue to grow. The company is balancing this with sufficient capital expenditure in order to keep the bits moving forward and adding value with the drill bit while keeping an eye on the main prize, which is production.

Over the last 6 months, there have been significant changes to the team. The CEO has gone from an explorer to a developer, which is a challenging transition as it requires a different approach and mentality. The decision-making is driven a lot more by the process and risk management as opposed to exploration. The latter offers more freewheeling and less focus on the process.

Last year, the company hired Leonardo Hermosilla, who previously served as the Vice President of Project Development, Capital Projects for Barrick Gold in South America. Leonardo has built several mines with Hatch as a principal and a consultant. He joined Marimaca Copper as Vice President of Projects to lead the next phase of development. This includes the permitting aspects of design and engineering, and tying up the loose ends before getting to the DFS. Once the DFS is delivered, the company will start the transition from being a developer to actually commencing construction. Leonardo is the first key hire and the company is looking to hire additional people to fill other key positions while upskilling the existing team members at the same time.

In its current position, the company isn’t looking to make drastic changes to its structure, as it would have a considerable impact on corporate overheads and costs. The company believes that it can run a very lean team until the end of the DFS. During the DFS process, the company intends to put some detail around the HR, organic ground, and the structure of management in order to determine the positions that need to be filled toward the end of the DFS phase.

Targets 2023 and Beyond

Marimaca Copper is looking forward to a 10,000m drilling program that will be entirely focused on the northern higher-grade zone. It anticipates that this drill program is going to be quite positive for the overarching resource. The resource update is expected by late March or early April this year. The update will incorporate all the drill results and deliver something that is close to the 90% M&I resource.

At the same time, the company is working aggressively towards moving the permits forward. It is looking to submit the permit application towards the latter part of the year. A major portion of the first quarter will be focused on the sulphide potential, a process that is currently under planning. The company will likely drill 5 holes in the first pass and release the results to the market. It is hoping to make a new discovery here. In the case of a new discovery, the company will focus on drilling it out further. By the end of the year, the company will kick off the DFS and it hopes to be in a position to deliver the study by either 2023-end or the first quarter of 2024.

Financing Considerations

During the previous financing, the copper price was under $3/lb and there wasn’t a lot of interest in the market for copper projects in general. This has completely changed in recent times. Based on the discussions and feedback from institutions and investors, there’s a substantial interest in the project. The company has been well-financed over the last 2.5 years, negating the need to raise additional capital. A lot of groups have shown interest in participating in the next round of financing discussions.

The company does not intend on raising capital at the current prices, because it’s materially undervalued at the moment and a capital raise would be detrimental to the current shareholders. The company does not see financing as a risk. The shareholders have been highly supportive and are cognizant of the benefits of having a bit more free float and potential liquidity. This will be a major consideration in the next round of financing.

The company was listed on the OTC Markets late last year. It is looking to organize a road show to meet investors. Large private retail investors aren’t keen on investing directly on the TSX. The OTC listing will enable these investors to invest in the company’s stock.

Marimaca Copper is looking to give more reasons to buy the company’s stock, which, when considering the new value of the project, is being traded at a significant discount. The change in value is hard to quantify at the moment as the company is yet to publish a study. Based on rough estimates, if the Marimaca asset was valued at half a billion dollars or $3.15/lb copper, it is now valued at $4.15/lb, a significant improvement on the PEA (Preliminary Economic Assessment) that was carried out on a smaller resource. Furthermore, the company achieved almost a 100% increase in resource tons. This leads to a significant change in the project’s value, going from $500M to somewhere between $700M-$1Bn.

To find out more, go to the Marimaca Copper website

Analyst's Notes

Subscribe to Our Channel

Stay Informed