Mexico & Peru Supply Constraints Reduce Silver Inventories to 136Moz as Margin Leverage Expands Across Silver Mining

Mexico and Peru supply constraints, falling ore grades, and rising AI demand are tightening silver inventories and expanding mining margins.

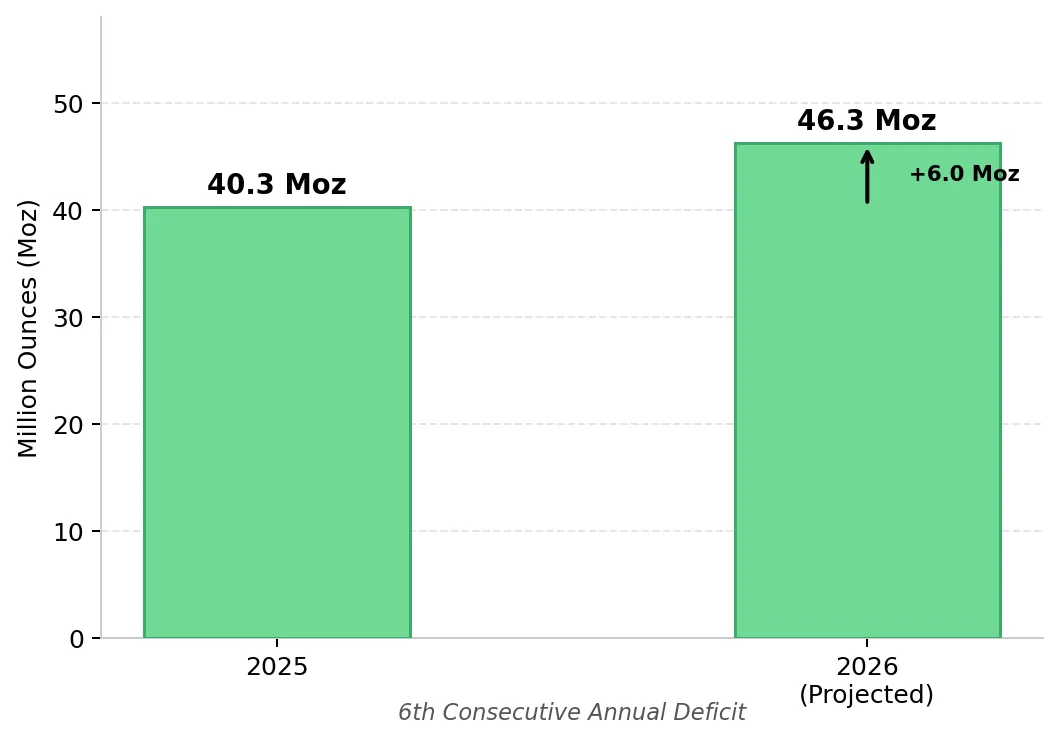

- The Silver Institute’s World Silver Survey 2026 projects a 46.3 million ounce silver supply deficit for 2026, the sixth consecutive annual shortfall and the largest on record. Global mined supply rose only 3% to 846.6 million ounces in 2025 even after silver reached a record $121.64 per ounce in January 2026, highlighting limited supply responsiveness at higher prices.

- Peru’s Emergency Decree No. 003-2026 to address a national energy crisis at state oil company Petroperú, increases operational risk for a country producing approximately 130 million ounces of silver annually and supplying roughly half of China’s silver-bearing concentrate imports.

- North America posted decade-low silver mine production in 2025 as ore grades declined in Mexico, the world’s largest silver-producing country. Higher silver prices have not offset the rising capital and operating costs required to access deeper, lower-grade ore.

- Silver’s inclusion on the USGS Critical Minerals List, combined with China’s one-year deferral of additional rare earth export controls under the November 2025 US-China trade framework and the ongoing Section 301 review, increases the likelihood of government and industrial stockpiling tied to supply chain security concerns.

- Production-stage silver companies are generating operating margin spreads of approximately $45 per ounce between all-in sustaining costs and realized prices. Development-stage projects are based on feasibility models using silver prices at roughly half of current spot levels, while exploration companies in Sinaloa, Mexico are advancing high-grade discoveries that could expand future supply.

Global Silver Supply Deficits Tighten Physical Inventories

The Silver Institute’s World Silver Survey 2026 projects a 46.3 million ounce silver supply deficit for 2026, widening from 40.3 million ounces in 2025 and marking the largest annual shortfall on record. Since 2021, cumulative market deficits have reduced above-ground silver inventories by approximately 762 million ounces. Rising LBMA silver lease rates and a decline in London silver free float to approximately 136 million ounces as of late 2025 indicate tightening physical availability.

Global mined silver supply rose only 3% in 2025 to 846.6 million ounces despite significantly higher silver prices. Approximately 70% of silver is produced as a by-product of lead, zinc, copper, and gold mining, limiting the industry’s ability to increase silver output in response to price gains alone. Primary silver producers, whose revenues depend more directly on silver prices, are becoming more valuable as market deficits reduce available physical inventories.

Mexico & Peru Supply Constraints Reduce Silver Market Flexibility

Mexico and Peru, the world’s two largest silver-producing countries, are both facing production constraints in 2026. Simultaneous supply risks in both countries are tightening a silver market where available LBMA inventories already remain historically low.

Peru Energy Disruptions Threaten Global Silver Concentrate Supply

Peru produced approximately 130 million ounces of silver in 2025. On May 11, 2026, the Peruvian Presidential Palace issued Emergency Decree No. 003-2026 authorizing emergency financial support for state-owned oil company Petroperú to address a nationwide energy shortage. Silver extraction, processing, and smelting are energy-intensive, and approximately 75% of Peru’s silver projects are operated by small and mid-sized mines with limited capacity to absorb sustained energy cost increases.

Peru supplies approximately half of China’s imported silver-bearing concentrates, meaning a prolonged decline in Peruvian output could constrain Chinese silver refining and fabrication capacity. Road blockades and social protests continue to disrupt concentrate shipments from mine sites to coastal ports, increasing supply risk in a market where LBMA silver inventories already remain limited.

Declining Ore Grades Reduce Mexico’s Silver Production Growth

Mexico drove North America’s decade-low silver production in 2025. As deposits mature, higher-grade near-surface ore is depleted, forcing miners to access deeper, lower-grade material at higher capital and operating costs per tonne. Production costs are rising faster than higher silver prices can offset, limiting the industry’s ability to increase output.

Sinaloa, Mexico’s largest historic silver-producing state, is central to Mexico’s declining mine supply. Falling output from mature mines is increasing the importance of earlier-stage projects in the same geological region as potential sources of future silver production.

US Critical Minerals Policy Increases Strategic Silver Demand

Silver’s inclusion on the USGS Critical Minerals List increases its importance within US supply chain and industrial policy. The designation raises the likelihood of future government and industrial stockpiling tied to energy, electronics, and defense supply security.

Under the November 2025 US-China trade framework, China deferred planned export controls on five additional rare earth elements for one year. China controls approximately 90% of global rare earth processing capacity, and the ongoing Section 301 tariff review could increase trade restrictions on industrial supply chains linked to silver demand. Further escalation could increase strategic stockpiling activity similar to the buying surge that supported silver prices in early 2026.

AI & Electronics Demand Offset Solar Silver Weakness

Photovoltaic silver demand is declining in absolute ounce terms, but demand from electronics, AI infrastructure, and automotive applications is increasing. The shift reduces the market’s dependence on solar demand alone and broadens silver’s industrial demand base.

Higher Solar Costs Reduce Silver Use per Panel

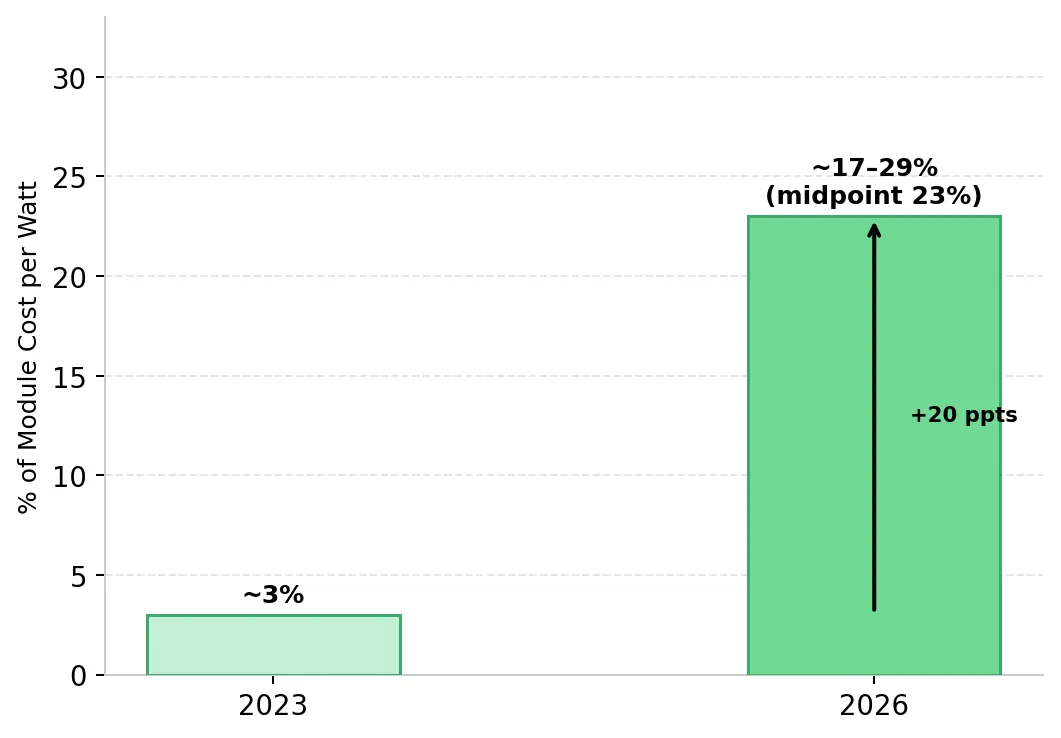

The Silver Institute projects photovoltaic silver demand will fall approximately 19% in 2026 to roughly 194 million ounces even as global solar installation capacity expands by approximately 15%. Solar manufacturers are reducing silver use per cell to offset higher input costs. Silver now accounts for an estimated 17% to 29% of photovoltaic module cost per watt, up from approximately 3% in 2023, making it one of the most expensive material inputs in solar manufacturing. The decline reflects cost reduction efforts rather than technological replacement, as no commercially scalable substitute for silver in photovoltaic cells currently exists.

AI Data Centers & Electronics Increase Industrial Silver Demand

Silver demand from AI data centers, high-speed transmission hardware, and automotive electronics is increasing as these technologies require highly conductive materials. Silver’s electrical conductivity makes it difficult to replace in precision electronic applications where heat management and signal performance are critical. Continued investment in AI infrastructure could support long-term silver demand at the same time global silver supply growth remains constrained.

Silver Supply Deficits Reshape Producer, Developer, & Explorer Valuations

Tightening silver supply, production risk in Mexico and Peru, critical mineral policy support, and rising demand from AI and electronics are creating different investment opportunities across silver producers, developers, and explorers.

Silver Producers Expand Margins as Spot Prices Outpace Costs

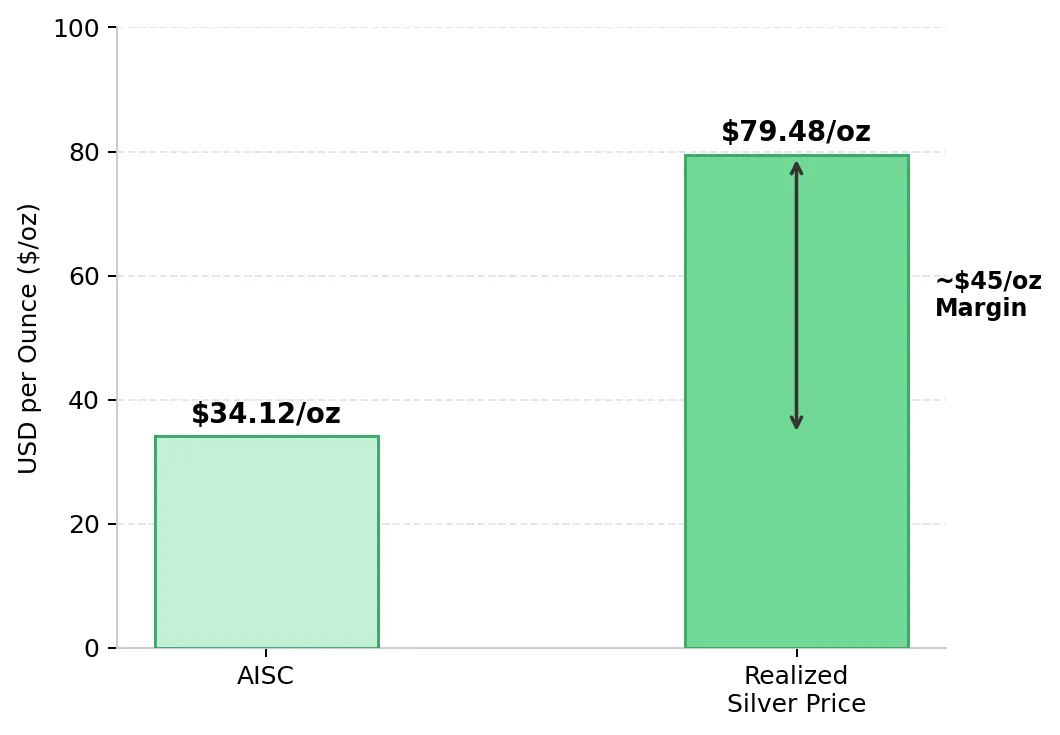

Americas Gold & Silver reported record consolidated silver production of approximately 787,000 ounces in Q1 2026, up 76% year-over-year, with all-in sustaining costs of $34.12 per ounce against an average realized silver price of $79.48 per ounce. The approximately $45 per ounce margin generated revenue of $67.8 million, up 187% year-over-year, and adjusted EBITDA of $33.6 million versus a loss in the prior-year period. Full-year 2026 guidance is 3.2 to 3.6 million ounces at AISC of $30 to $35 per ounce, with $122.4 million in cash as of March 31, 2026. The company’s February 2026 joint venture with US Antimony is also expanding domestic critical mineral processing capacity at the Galena Complex in Idaho.

Oliver Turner, Executive Vice President of Corporate Development at Americas Gold & Silver, explains why supply deficits are increasing the value of primary silver producers:

“We've had six years now of a deficit of about 150 to 200 million ounces a year. Demand is continuing to increase, but 70% of silver is a byproduct from other mines. You can't just turn on more silver supply when the world needs it. Primary silver producers are producing an increasingly critical and increasingly scarce metal required across all these applications.”

Higher Silver Prices Increase Upside for Feasibility-Stage Projects

Vizsla Silver completed a Feasibility Study for its 100%-owned Panuco silver-gold project in Sinaloa, Mexico in November 2025. The study outlined annual production of 17.4 million silver-equivalent ounces over an initial 9.4-year mine life, with an after-tax NPV5% of US$1.8 billion, an IRR of 111%, and a 7-month payback period based on silver prices of US$35.50 per ounce and gold prices of US$3,100 per ounce. Current silver prices of approximately $75 per ounce are more than double the study assumption, increasing potential project returns if pricing remains elevated. In May 2026, the company also secured approximately US$10 million unsecured working capital facility from Mexican government lender FIFOMI, supporting continued project advancement.

Jesus Velador, Vice President of Exploration at Vizsla Silver, explains how infill drilling at Copala is increasing resource confidence ahead of project development:

“We accomplished over 60,000 meters of infill drilling mostly on the central portion of Copala, and with that drilling we released an updated mineral resource with a substantial increase in the indicated and measured resources. For the first time, we put out a measured resource in the core of the high-grade central portion of Copala.”

High-Grade Silver Discoveries Expand Exploration Upside in Sinaloa

GR Silver Mining is advancing its 100%-owned Plomosas Project across 7,823 hectares in the Rosario Mining District of Sinaloa, Mexico. The company holds a 2023 Mineral Resource Estimate of 134 million silver-equivalent ounces and is conducting a 20,000-metre step-out drilling program with three active rigs at San Marcial. Recent drilling returned 45.1 meters grading 1,623 g/t silver, including 18.85 meters at 3,846 g/t and 8.25 meters at 8,579 g/t, supporting the potential for higher-grade resource expansion. An updated Mineral Resource Estimate and maiden Preliminary Economic Assessment are targeted for the second half of 2026. The company also reported C$28.5 million in cash with no debt.

Eric Zaunscherb, Interim President and Chief Executive Officer of GR Silver Mining, discusses the company’s resource growth potential in Sinaloa:

“We have 134 million ounces of silver equivalent and we feel that that has a significant chance to grow through our 20,000 meter drill program.”

The Investment Thesis for Silver

- Silver supply responds slowly to higher prices because approximately 70% of global output is produced as a by-product of other metals mining. That limits the industry’s ability to increase production quickly and supports the Silver Institute’s projected 46.3 million ounce market deficit for 2026.

- Supply risks in Mexico and Peru are occurring at the same time, tightening a silver market where LBMA free float inventories stood at approximately 136 million ounces as of late 2025. Declining ore grades in Mexico and Peru’s ongoing energy emergency are limiting production growth in the world’s two largest silver-producing countries.

- The USGS Critical Minerals designation increases the likelihood of future US government stockpiling and strategic procurement tied to supply chain security. That could add a new source of demand beyond traditional industrial and investment buying.

- Developers with feasibility studies based on silver prices of approximately $35 per ounce could generate stronger project economics in a market where spot prices exceed $75 per ounce, even without further price increases.

- Exploration companies in Sinaloa are expanding high-grade silver resources in a region where mature mines are producing less silver each year. New discoveries could become more valuable as declining output from existing mines increases the cost of replacing silver reserves.

- Producers generating margin spreads of approximately $45 per ounce between AISC and spot silver prices are delivering strong adjusted EBITDA growth as supply deficits support higher prices. These companies also provide investors with exposure to current silver market conditions without the financing and construction risks associated with development-stage projects.

The 2026 silver deficit is increasingly being driven by supply constraints in Mexico and Peru, the two countries most important to global silver mine output. Declining ore grades in Mexico and Peru’s energy and logistics challenges are limiting production growth despite higher silver prices. For investors, the key question is where to gain exposure across the silver mining value chain: producers generating approximately $45 per ounce margin spreads, developers with feasibility studies based on silver prices far below current spot levels, or explorers advancing high-grade discoveries in Sinaloa.

TL;DR

Silver markets are tightening as supply growth slows in Mexico and Peru, the world’s two largest silver-producing countries, while industrial demand from AI infrastructure, electronics, and strategic stockpiling continues to rise. The Silver Institute projects a record 46.3 million ounce supply deficit for 2026, with available LBMA inventories falling to approximately 136Moz. Producers are benefiting from expanding margins as silver prices outpace mining costs, while developers and explorers could see valuation upside as higher silver prices improve project economics and increase the value of new discoveries in Sinaloa, Mexico.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed