Millennial Potash Targets 2027 Construction Start for Massive Gabon Potash Project

Millennial Potash advances its Gabon potash project with US DFC backing, a 6Bt resource, and a dual funding/M&A strategy targeting 2027 construction.

- Millennial Potash has defined a resource of roughly 6 billion tonnes at its Banio Potash Project in Gabon yet covering only about 4% of its 1,500 square kilometer licence area, positioning it among the largest undeveloped potash deposits globally.

- The company has secured support from the US International Development Finance Corporation including a $3 million grant for feasibility work and a prospective pathway to construction debt financing alongside backing from the US State Department and Embassy in Gabon.

- Management is targeting completion of feasibility and environmental and social impact studies by early 2027, a finalised funding package and construction start by late 2027, using lower-capex solution mining methods.

- The company is pursuing parallel tracks of full project financing (targeting 60-65% debt with limited equity dilution) and potential M&A or strategic partnership opportunities, citing precedent from two prior potash projects sold to K+S and ICL.

- Planned infrastructure includes an existing transshipment port and a proposed deepwater port that could expand production capacity from an initial 800,000 tonnes per year toward 4-5 million tonnes per year over time.

Millennial Potash, chaired by Farhad Abasov, is advancing a potash project in Gabon that the company describes as one of the largest undeveloped potash resources in the world.

The Gabon project is now moving from an exploration phase into a development phase that includes feasibility and environmental and social impact assessments, alongside efforts to secure construction financing. For investors, the project sits at the intersection of global fertilizer supply security, geographic diversification away from concentrated producing nations, and the company's stated track record of advancing projects toward a transaction or production within a short multi-year window.

One of World's Largest Undeveloped Potash Resources

The Gabon project covers approximately 1,500 square kilometers, of which drilling to date has defined a resource of roughly 6 billion tonnes in the measured, indicated and inferred categories. Management notes this drilling has covered only about 4% of the total licence area, suggesting potential for further resource expansion as additional drill holes are completed. The company also completed a preliminary economic assessment earlier in the project's life, which management says indicated a cost structure among the lowest in the global potash sector.

The scale of the resource, combined with the project's geographic position relative to Brazilian and African demand centers, forms the foundation of the company's stated investment case. The project's classification as a solution-mining opportunity, discussed further below, also differentiates its capital intensity from larger underground operations being evaluated elsewhere in the region.

De-Risking the Project With US Government Backing

A central feature of the Gabon project is its relationship with the US International Development Finance Corporation (DFC), which began due diligence in early 2024 and signed a formal support agreement in June 2025. The arrangement has two components: a $3 million grant, released in matching tranches, earmarked specifically for feasibility study costs, of which the company has already received the first 10%; and a longer-term pathway toward DFC debt financing for construction, contingent on completion of feasibility and environmental and social impact studies and the receipt of mining permits. Abasov described the significance of this backing directly:

"We have [the] tremendous advantage of US DFC coming in and basically de-risking the project both politically and financially. We've seen tremendous support coming from the US not only directly from the US DFC but also from the State Department, from the US Ambassador and Embassy in Gabon."

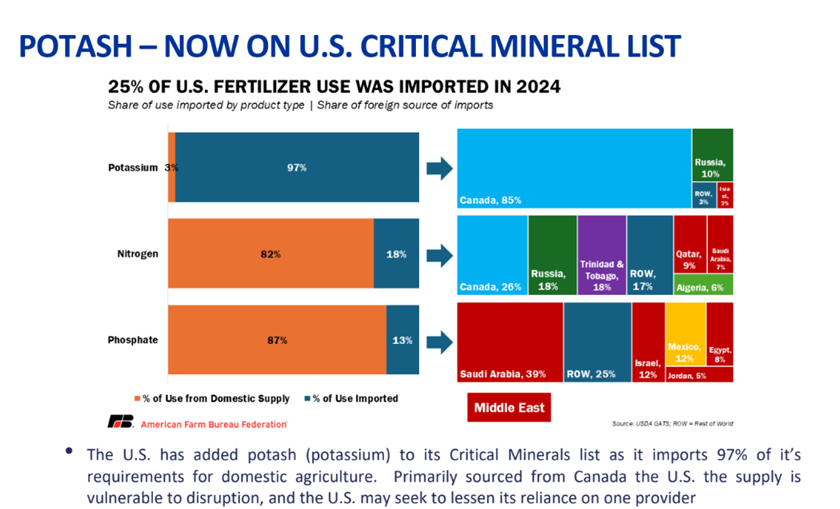

The company is also separately seeking support from the Canadian government. Management attributes US government interest in part to potash's recent addition to the US critical minerals list and continued US reliance on imported potash, including from Russia.

Inside a Tightly Held Pricing Structure

The global potash market is highly concentrated, with Russia, Belarus and Canada accounting for an estimated 70% of supply, rising to roughly 80% when Jordan and Israel are included. Management describes this concentration as a source of pricing discipline: low-cost producers such as Nutrien (Canada) and EuroChem (Russia) operate at an estimated all-in cost of around $120 per tonne FOB, against current prices in the range of $350 to $400 per tonne.

Regional pricing varies, with Brazil currently trading around $400-405 per tonne and African prices reported above $400 per tonne. Africa's total potash consumption is approximately 2 million tonnes annually, a small but underserved market compared with China's 17 million tonnes, of which 10 million tonnes is imported. Management positions the Gabon project to serve African agriculture as a primary market, supplemented by sales into Brazil, the US Atlantic coast, and growing interest from Asian buyers.

Interview with Farhad Abasov, Chairman, Millennial Potash

Turning Off-Takes Into Project Financing

The company's approach to off-take agreements differs from a conventional sales-only structure. Management indicated it is targeting commitments covering roughly 20-25% of future production, but only from counterparties willing to provide financial support to the project ahead of construction, whether through direct equity investment or prepayment arrangements, rather than simple purchase agreements. Off-take terms under discussion are typically structured for a three-to-five-year duration, after which output would be sold into the spot market.

On overall project funding, management is targeting a capital structure weighted toward debt, estimating 60-65% debt financing alongside royalty arrangements, with minimal equity dilution. Discussions for the equity component are currently focused primarily on US-based investors, in addition to DFC's grant and prospective debt commitments, with African conglomerates in the fertilizer sector also cited as potential partners.

A Fast-Tracked Path to Production

Management's stated schedule targets completion of the feasibility study by late 2026 or early 2027, a finalised funding package and a construction start by the end of 2027, with an 18-to-24-month build period to follow. The project will use solution mining, a method involving the injection of water underground to dissolve potash, followed by pumping the resulting brine to the surface for evaporation and separation.

Management describes this method as lower in capital intensity than underground mining and with a comparatively limited surface footprint. The same management team previously used solution mining at a Saskatchewan project later sold to Germany's K+S AG, which built it into a producer of more than 2 million tonnes annually, and at an Ethiopian project later acquired by Israel's ICL.

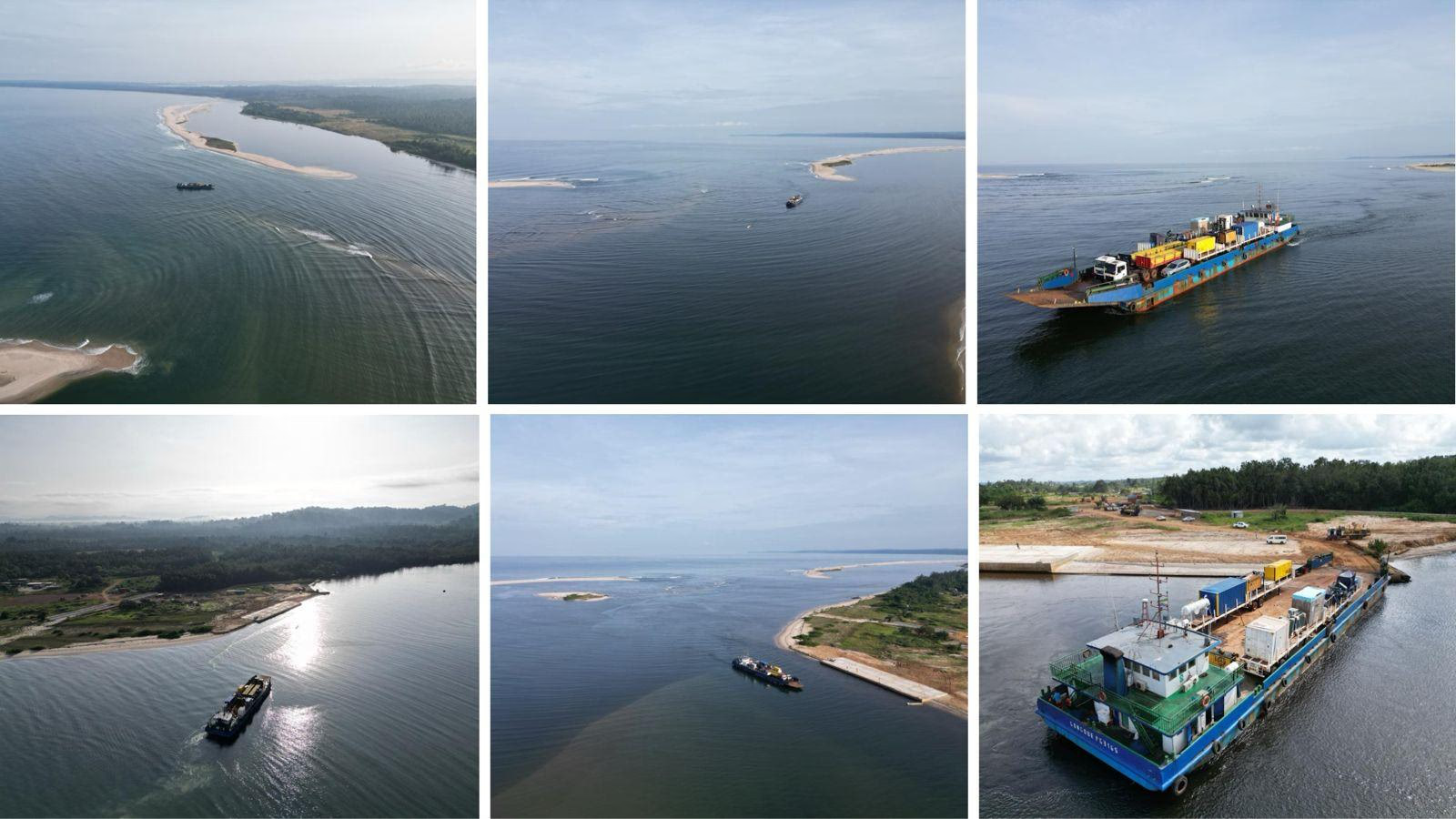

Supporting Infrastructure

Project economics are also tied to surrounding infrastructure. An existing transshipment port, developed by a private London-based group, is available to support initial production. Separately, the company is working with a partner group on a proposed deepwater port, which would be externally funded, built and operated in exchange for a handling fee.

Management indicates this could allow production capacity to expand from an initial level of approximately 800,000 tonnes per year toward 4-5 million tonnes annually over time. A natural gas pipeline has recently been extended to shore to support a power plant near the project area, which management expects to expand as part of feasibility planning.

Keeping Every Funding Path Open

Management is pursuing two parallel paths: full project financing through debt, grant and equity sources, and potential mergers, acquisitions, joint ventures or strategic partnerships. Citing precedent, Abasov noted that in a prior potash project sale to ICL, the acquirer was already a 17% shareholder but paid a 50% premium to acquire the remainder, a result management attributes partly to the credibility added by having the International Finance Corporation involved as a funding partner.

A Singapore-based family office, The Quaternary Group, with a mining and agricultural-sector background holds a significant minority stake in Millennial Potash and is described by management as engaged in the project on a similar dual-track basis. Management noted that a sale to a Chinese buyer would likely exclude continued DFC involvement, while a Western acquirer or partner would retain access to the existing DFC support package.

The Investment Thesis for Millennial Potash

- Large-scale, low-cost resource: An estimated 6 billion tonnes of measured, indicated and inferred potash resource from drilling that has covered only 4% of the licence area, with operating costs management positions toward the lower end of the global cost curve.

- US government de-risking: Formal support from the US DFC, including grant funding for feasibility work and a stated pathway to project debt, plus backing from the US State Department and Embassy in Gabon.

- Geographic supply advantage: Positioned as the nearest forthcoming potash supplier to Brazil and well placed to serve underserved African agricultural markets, where prices are reported above $400 per tonne.

- Disciplined capital structure: Target funding mix of 60-65% debt plus royalties, with off-take partners required to provide financial commitment ahead of construction, aimed at limiting equity dilution.

- Accelerated development timeline: Feasibility study targeted for completion by early 2027, funding package by mid-2027, and construction start by late 2027, against multi-decade timelines management cites for some peer projects.

- Lower-capex mining method: Use of solution mining, previously applied by the same management team on two prior potash projects, both of which were sold to established industry players (K+S and ICL).

- Infrastructure scalability: A proposed deepwater port could expand production capacity from an initial roughly 800,000 tonnes per year toward 4-5 million tonnes per year over time.

- Dual funding and exit optionality: Management is simultaneously pursuing full project financing and M&A or strategic partnership discussions, citing a prior 50% acquisition premium received on a comparable project.

Global Potash Market

Global potash supply remains highly concentrated, with Russia, Belarus and Canada controlling an estimated 70% of output, a dynamic that has historically supported stable, narrow-band pricing despite periods of global surplus capacity. Abasov framed this concentration directly:

"Remember potash is a very unique sector where basically three countries control almost 70% of supply [...] Now right now, the way we're positioning our projects that it's going to be primarily African potash for African agriculture and probably quite a bit of this material will also end up in Brazil."

Western governments have increasingly classified potash as a critical mineral given import dependence, including continued US purchases of Russian potash despite broader sanctions. This has driven policy interest in geographically diversified, Western-aligned supply sources. Africa's potash demand remains small in absolute terms but is structurally underserved relative to its agricultural needs, while Brazil's large import requirement adds a second underserved market for new low-cost entrants.

TL;DR

Millennial Potash is advancing a large-scale, low-cost potash project in Gabon backed by the US Development Finance Corporation, with feasibility studies targeted for completion in early 2027 and construction potentially starting by late 2027. The company holds an estimated 6 billion tonnes of resource across just 4% of its licence area and is targeting a capital structure weighted toward debt to limit equity dilution. Management is simultaneously pursuing full project financing and potential M&A or strategic partnership opportunities, drawing on its track record of selling two prior potash projects to established industry acquirers. Key catalysts ahead include completion of environmental and social impact studies, finalisation of off-take agreements, and progress on a proposed deepwater port to support future production scale-up.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.webp)

Stay Informed