Atlas Salt: A De-Risked Salt Developer Trading at a Fraction of Its Feasibility Study Value

Atlas Salt is advancing the Great Atlantic Salt Project in Newfoundland, Canada, while the market valuation lags the project economics.

- Atlas Salt trades at an enterprise value (EV) of $138.5 million, representing a material discount to the $920 million after-tax net present value at an 8% discount rate (NPV8%) outlined in the 2025 Updated Feasibility Study (UFS).

- North America imports 8 to 10 million tonnes of salt annually, a reliance that is further exacerbated by the closure of legacy salt mines in the United States.

- The Great Atlantic Salt Project models an average annual post-tax free cash flow (FCF) of $188 million over a 24.3-year mine life based on a base salt price of $81.67 per tonne.

- Management has identified project financing and construction execution as the primary remaining milestones, having reduced typical metallurgical, geological, and permitting risks from the risk profile.

- The company recently secured $1.25 million through a flow-through share offering and a provincial grant to drill the Black Bay nepheline property, unlocking potential non-core value while preserving capital for advancing the Great Atlantic Salt Project.

A Feasibility-Stage Asset Pricing a Material NAV Discount

Atlas Salt (TSXV:SALT) trades at an enterprise value (EV) of $138.5 million, which sits materially below the underlying economics of the Great Atlantic Salt Project. The 2025 Updated Feasibility Study (UFS) outlines an after-tax net present value of $920 million at an 8% discount rate (NPV8%). Based on an $ 81.67-per-tonne base salt price, the project models an average annual post-tax free cash flow (FCF) of $188 million and an average annual earnings before interest, taxes, depreciation, and amortisation (EBITDA) of $325 million over a 24.3-year mine life.

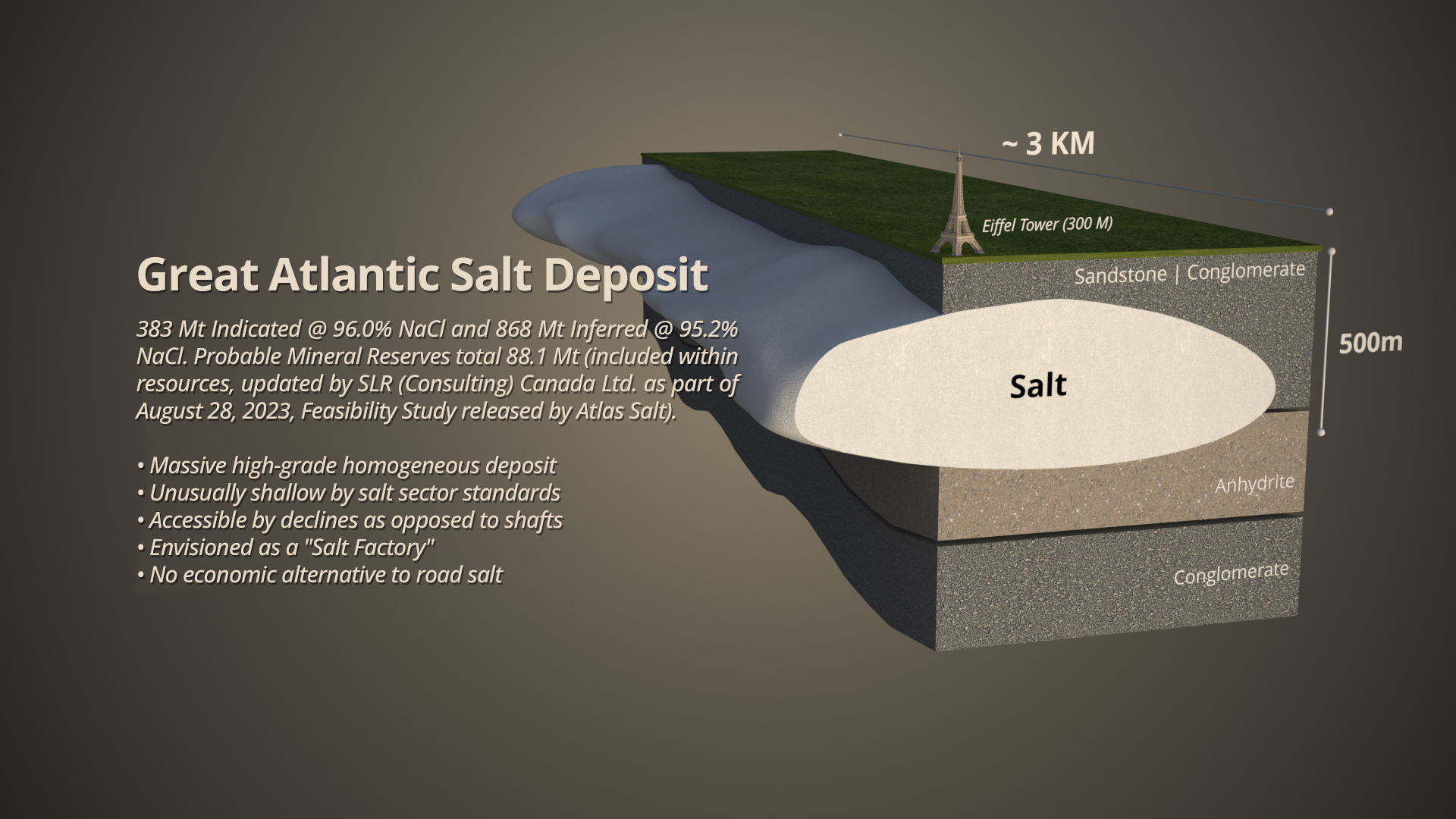

At current levels, the company trades at roughly 0.1x forward-looking Net Asset Value (NAV). Management argues the market is applying conventional mining risk frameworks to an asset with materially lower technical complexity. Salt deposits are highly homogeneous and easy to define, eliminating metallurgical risk. The block model grades 95.9% sodium chloride across 95 million tonnes of probable reserves, while the project was released from the provincial environmental assessment process in April 2024, leaving financing and construction execution as the primary remaining hurdles.

The valuation gap widens further against operating salt producers. Atlas Salt trades at an enterprise value of US$98.9 million, while Compass Minerals trades at 9.1x EV/EBITDA and recent private transactions for K+S Americas and US Salt cleared at 12.5x and 16.5x EV/EBITDA, respectively. While not direct comparables given that Atlas Salt remains pre-production, the transactions illustrate how mature salt assets are often valued on cash flow durability rather than conventional mining NAV frameworks.

Chief Executive Officer of Atlas Salt, Nolan Peterson, argued that conventional mining metrics fail to capture the asset's characteristics:

"If you're valuing Atlas Salt just based on its NPV like you would any other resource project, you are, in my view, undervaluing us and again, we're already at an undervalued even when you are comparing us or looking at us through that metric of a typical mining company, so from two levels you're undervalued"

Structural Supply Deficits in the North American Deicing Market

The economic fundamentals of the Great Atlantic Salt Project are underpinned by a structural supply deficit in the North American deicing market. North America currently imports 8 million to 10 million tonnes of salt annually to meet demand. A significant portion of these imports is shipped from overseas producers in Chile and Egypt, requiring more than 14 days of transit, compared to less than 3 days via the Great Atlantic Salt Project's deep-water port access in Newfoundland.

This reliance on imports has been exacerbated by the depletion of legacy domestic infrastructure. The last new salt mine in North America, American Rock Salt, opened in 2001. Since then, the market has faced structural reductions, including the closure of Cargill's Avery Island mine in Louisiana, which removed 2.5 million tonnes per year of domestic supply. Other legacy assets face challenging operating conditions and environmental constraints at depth, further threatening domestic capacity.

Atlas Salt's planned nameplate production capacity of 4 million tonnes per annum is positioned to be absorbed by this current market deficit. Because the primary end users are municipal and provincial governments, which are legally obligated to maintain winter road safety, the commodity avoids the volatile commodity pricing typical of conventional resource-sector companies.

Peterson highlighted how this dynamic reduces downside exposure:

“This is kind of the best customer anybody could ever ask for, right, that they're forced to buy your product. And if people knew that, and knew how much salt is purchased, how stable the salt market has been on the risk side, right, on the downside, the risk that you can't find a market there, they would become very, very comfortable with it."

Capital Structure & the Project Financing Pathway

Atlas Salt maintains a tightly held capital structure with 110.7 million basic shares outstanding and no warrant overhang. Insider ownership sits above 40%, aligning management with the long-term execution of the Great Atlantic Salt Project. The company reported $5.4 million in net cash, providing a near-term runway as it advances its financing initiatives.

The primary gating factor to production is the $589 million pre-production capital expenditure (capex) outlined in the feasibility study (FS). The company has engaged Endeavour Financial for project finance advisory. Management notes that the asset's predictable cash flow profile, projected at $188 million in average annual post-tax FCF, supports infrastructure-style debt capacity that is not typically available to conventional mining projects with volatile commodity exposure.

Once in production, the cash flow allocation model prioritises rapid deleveraging. The company targets applying 50% of FCF to debt repayment and 50% to shareholder returns in the first 8 years. In subsequent years, that ratio shifts to target more than 90% of FCF for shareholder returns and life-of-mine extension initiatives.

Financing & Execution Risk

The primary risk facing Atlas Salt is the successful arrangement of a project financing package sufficient to fund the $589 million pre-production capex. While Endeavour Financial's engagement signals active progress, the financing has not yet been secured, and until it is, the timeline for construction and first production remains subject to change. The company's current net cash position of $5.4 million underscores the importance of completing this milestone on time.

Construction execution risk, while manageable relative to the technical complexity of conventional mining projects, remains a factor given the scale of the build. The project's shallow deposit depth of approximately 180 metres, reduced processing requirements, and fully electric mine design limit the technical surface area of this risk, but do not eliminate it. No comparable salt mine has been built in North America in approximately 25 years, which management notes makes salt a niche commodity that the broader market is generally unfamiliar with compared to typical resource sector plays.

Unlocking Non-Core Optionality at Black Bay

While the Great Atlantic Salt Project remains the core focus, Atlas Salt recently secured funding to advance its Black Bay nepheline property in Southern Labrador. The company arranged a $1.25 million non-brokered private placement of flow-through shares. The proceeds, combined with funding from a provincial Junior Exploration Assistance (JEA) 2026 grant, provide a relatively low-cost opportunity to drill the asset while the company focuses on advancing the Great Atlantic Salt Project.

The supply is structurally concentrated, with only 1 producing mine in North America. Surface sampling conducted at Black Bay in 2017 recovered more than 3 tonnes of material, with subsequent analysis by SGS Lakefield indicating that the rock's mineral content is comparable to that of other commercial deposits and that initial beneficiation tests were positive toward meeting industrial standards.

The upcoming maiden drill program will test the deposit at depth to evaluate potential tonnage. By funding this exploration through flow-through shares, which qualify as "flow-through mining expenditures" under the Income Tax Act, Atlas Salt aims to uncover and subsequently potentially monetise a non-core asset while preserving capital for its flagship salt development.

Investment Thesis for Atlas Salt

- The company is advancing an environmentally approved salt development asset in a top-tier global mining jurisdiction.

- The North American deicing salt market is facing structural supply deficits and price increases due to recent mine closures.

- The project economics demonstrate a rapid payback period and significant long-term free cash flow generation.

- The current enterprise value presents a material discount to the net present value calculated in the feasibility study.

- The parallel exploration of an industrial mineral asset using flow-through financing provides a low-cost opportunity to uncover non-core value.

The resolution of remaining execution risks is the primary pathway for the market valuation to align with the feasibility study's underlying economics.

TL;DR

Atlas Salt is developing the Great Atlantic Salt Project in Newfoundland, targeting a structurally undersupplied North American market. The project has an after-tax NPV8% of $920 million relative to a current enterprise value of $138.5 million. With geological and environmental assessment risks removed, management is focused on securing project financing as the primary remaining milestone, while advancing a secondary industrial mineral asset through non-dilutive government grants and flow-through capital.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed