O3 Mining (TSX-V: OIII) - Buy it at Cash and Get an Option Worth $400M-$600M!

Interview with Jose Vizquerra, President & CEO of O3 Mining Inc. (TSX-V:OIII)

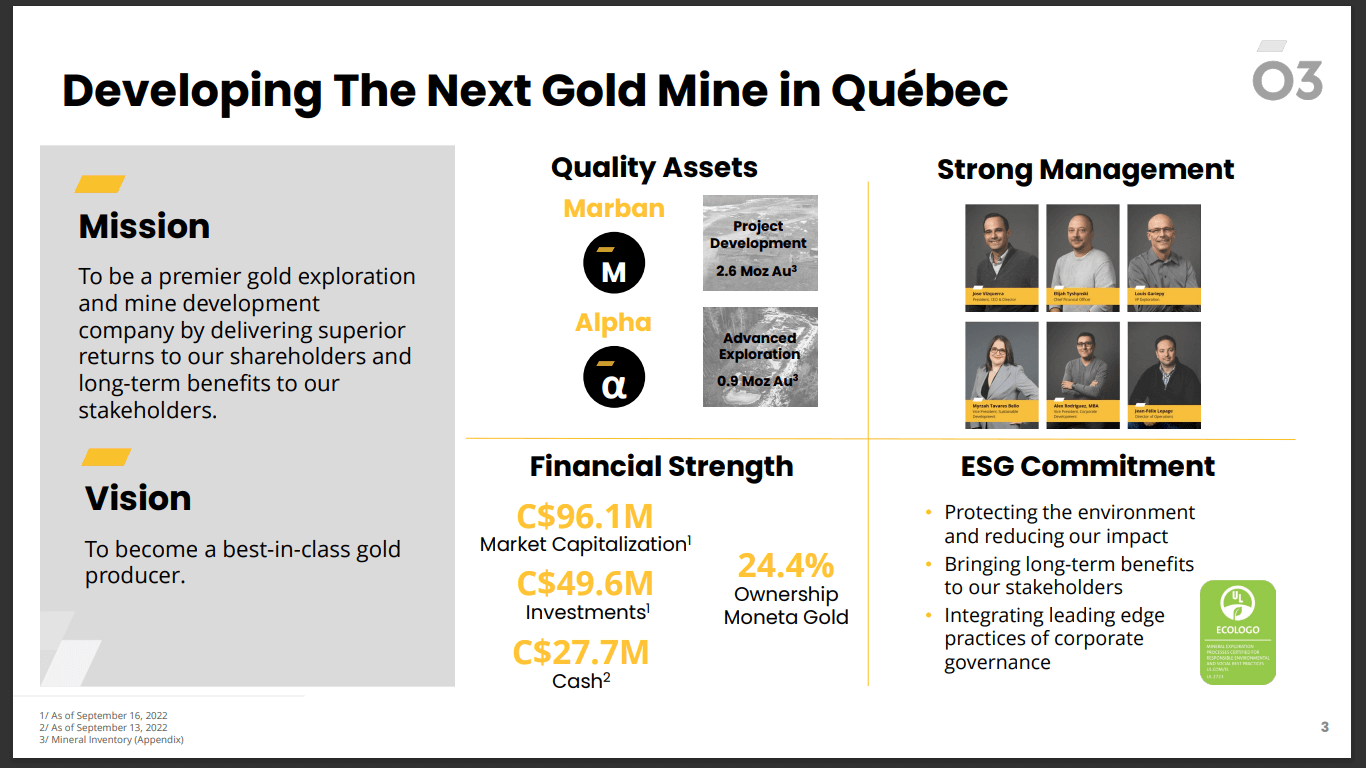

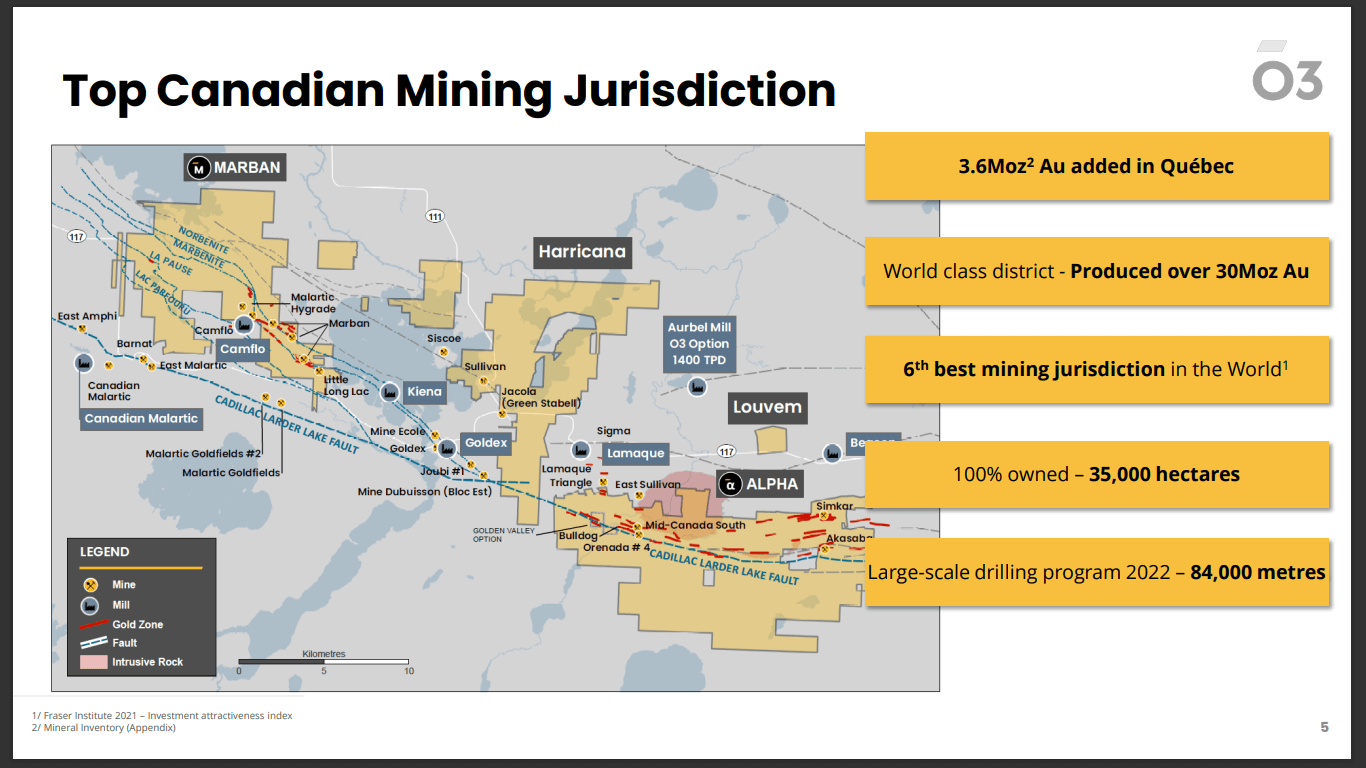

O3 Mining Inc (formerly Chantrell Ventures Corp.), an Osisko Group company is a gold explorer and mine developer. The company is well-capitalised and owns a 100% interest in all its properties (137,000 hectares) in Quebec. The company is focused on delivering superior returns to its shareholders and long-term benefits to its stakeholders.

Matt Gordon caught up with Jose Vizquerra, President, CEO, and Director, O3 Mining. Prior to his appointment with O3 Mining, Mr. Vizquerra was Executive Vice President of Strategic Development for Osisko Mining Inc. He joined the company from Oban Mining Corporation, where, as President and CEO, he played a leading role in the combination of Oban, Corona Gold Corp, Eagle Hill Exploration Corp, and Ryan Gold Corp. to form Osisko Mining. Through ambitious drilling and prudent capital raising, Osisko Mining has become the highly valued proponent of the world-class Windfall gold project. Before that, Mr. Vizquerra was Head of Business Development for Comañia de Minas Buenaventura. Previously, he was a production and exploration geologist at the Red Lake gold mine in Ontario. He currently serves as a Director of Osisko Mining, Sierra Metals Inc., and as an advisor to the Boards of Discovery Metals Corp, and Palamina Resources. The Young Mining Professionals recognized him as one of their Young Mining Professionals of the year with the 2019 Peter Munk Award. Mr. Vizquerra is an alumnus of the General Management Program at the Wharton School of Business. He holds an M.Sc. in Mineral Exploration from Queens University and a B.Sc. in Civil Engineering from UPC Universidad Peruana de Ciencias Aplicadas. He is a Qualified Person pursuant to National Instrument 43-101.

Company Overview

O3 Mining is a gold explorer and mine developer ready to produce from its highly prospective gold camps in Quebec. The company is listed on the Toronto Stock Exchange (TSX-V: OIII) and the OTC Markets (OTCQX: OIIIF). ORCan Oilfield Services Ltd. and Harricana River Mining Corporation Inc., O3 Markets Inc., and Niogold Mining Corp. are the company’s subsidiaries. It is headquartered in Toronto, Canada.

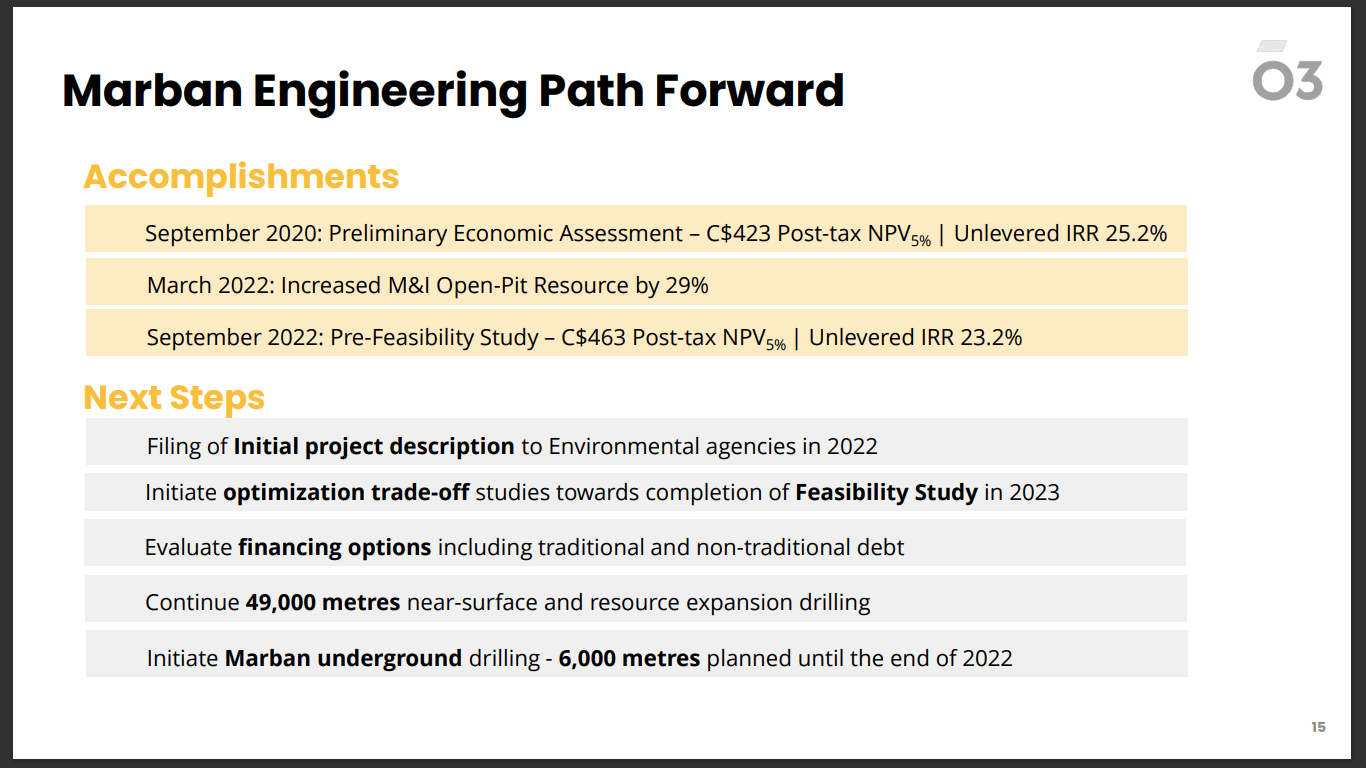

O3 Mining is a multi-million-ounce gold company with projects in development. The company’s representatives recently attended the Gold Summit at Beaver Creek, Colorado. At the Marban project, the company has a $463M NPV (Net Present Value) at a 5% discount rate with a 23% un-levered IRR (Internal Rate of Return). The levered IRR is very high at 40%. The project AISC (All-in Sustaining Costs) is under $900/oz gold. The Marban asset has a project CapEx (Capital Expenditure) of $435M.

Market Landscape

O3 Mining is looking to produce 160,000oz of gold on a yearly basis, placing it in the range of mid-tier producers. The market has been largely unchanged by the recent developments. According to the company, this is due to the sentiment on gold. When gold is in a positive run, there’s an increased interest from the market.

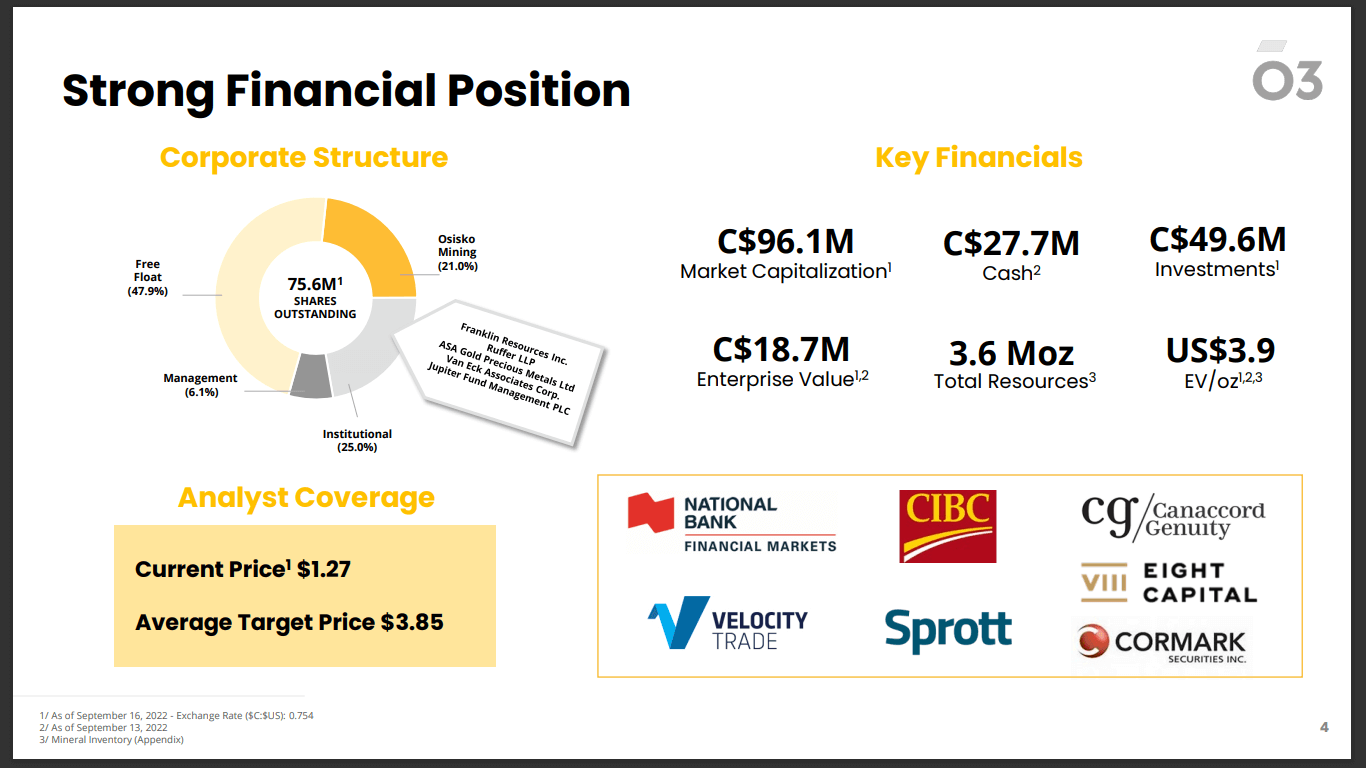

Notably, 4 weeks ago, when the market was trending positively, the company was trading at $1.60, however, things have come done due to a decreased interest in gold. Since the gold market is cyclical in nature, the company is looking to work the aspects of the operation that it can control to be in a better position when the market is once again in a favourable position. The company has a $100M current market cap.

Financing Considerations

O3 Mining has 3 financing alternatives. In a case where the company can collaborate with other producers in the area such as Canadian Malartic, it can potentially bring down the project CapEx from $435M to $200M. In order to raise funds, the company can raise $100M from debt financing and the remainder of $100M can be acquired through equity. The company currently has $80M in cash flow. It won’t need to carry out project financing if the equity goes up. Collaboration with other companies in the area will increase the IRR to over 60%.

If O3 Mining is successful in working with other producers, it can take the ore from one side to the other without having to build a tailings facility or additional infrastructure. This would reduce the project's CapEx while simultaneously maximising shareholder value. While this is the ideal case scenario, the company continues to look at different alternatives.

The company’s other projects are mostly financed. Four weeks ago, the company raised $18.7M in capital that was invested into the Feasibility Study. Currently, all the drilling is already embedded in the company. Essentially, investors are buying cash with the option to have a project that is valued between $400M and $600M.

In order to add immediate value, the company will focus on finding additional ounces close to the Marban project. These ounces will help extend the 10-year mine life to 12,14, or even 16 years. The company is currently focusing on 2-year increments. It is working on building additional resources around the project.

In 2023, the company plans to publish a new resource that will add more ounces to the project. Interestingly, for every 160,000oz added, the project NPV will increase by $50M. If the company is successful in uncovering an additional 1Moz, the project will essentially double in size. Since the project has an ongoing PFS (Preliminary Feasibility Study), everything is in the M&I (Measured and Indicated) category.

O3 Mining seeks to utilise the existing funds to move the project into a Feasibility Study. Following this, it will focus on obtaining the necessary permits. For the Feasibility Study, the company is looking to carry out a financing raise, which could come from debt and equity.

The worst-case scenario would be a $200 dilution in equity. In the best-case scenario, the company will use a facility from another company. The second-best scenario would be to team up with private equity. No matter the condition, the company is determined to build the project.

It is important to note that the company isn’t looking to sell the project to private equity, but intends to work together in order to build it. There is also a middle ground where the private equity may take 50% of the project, and the remainder will be financed. There is also a possibility that the market sentiment could experience a positive change, enabling the company to reach a $3 share price once again. In this case, the company will be in a position to finance the project with minimal dilution.

O3 Mining is urging its competitors to be proactive. Canadian Malartic has publicly said that it will run out of ore by 2027. The company has only one mill in operation. The energy required to process material will be the same regardless of the amount of feed. To save on costs, it would be a better strategy to process the ore elsewhere or to process ore from other companies.

O3 Mining is the only company that currently has a PFS in place. No other projects are expected to have a PFS or a Feasibility Study by 2023. Furthermore, no other project is expected to have permits by 2026. Franklin Templeton, Merck & Co., and Osisko Mining are responsible for making a decision to sell. However, at current prices, O3 Mining is not in favour of selling. The company is looking to make money for investors over the long term. Investing today can potentially lead to 50%-200% margins within 1-3 years.

Companies are valued at half their NPV or lesser in the current market environment. O3 Mining is currently valued at 25% of the NPV. O3 Mining is currently valued at 25% of the NPV. There is a fair amount of re-rating that needs to take place in the market. O3 Mining is the only company in the main Val-d’Or region, that is located 12km from 2 major mines, placing it in a strong position.

In recent times, the inflationary environment has gone up quite a bit. It is possible that inflation will increase further. In O3 Mining’s case, the inflation was largely mitigated by way of better recoveries. In case the inflation keeps going up, by Q1, 2023, the gold market will be in a highly-unfavourable position. There is a chance that this might happen.

Targets 2022 and Beyond

O3 Mining is currently focusing on completing the Feasibility Study, acquiring the necessary permits, and making a decision to build. The company intends to build the project with private equity, or in conjunction with another major company. It is in a good position with a rock-solid project in place. This is an excellent opportunity for investors to come in. The current market conditions make it a great time to buy.

To find out more, go to the O3 Mining website

Analyst's Notes

Subscribe to Our Channel

Stay Informed