Osisko Gold Royalties (OR) - Best Royalty Company in the World?

Osisko Gold Royalties (OR) - Best Royalty Company in the World?

Could this really be the best royalty company in the world as Roosen says? Well, its a different business model for sure with a portfolio of royalties "on track' to deliver the best growth profile within the royalty sector over the next 3-5 years"...

We like royalty companies; so do many high-profile investors. They offer invests exposure to the excitement and leveraged growth of mining, but with much less of the downside.

Osisko Gold Royalties is an 'intermediate' precious-metals-focussed royalty company. Having been founded in April 2014 and commencing activities in June 2014, Osisko Gold Royalties has been on a relentless pursuit for growth. The company now holds a North American focussed portfolio consisting of in excess of 135 royalties, streams and precious metal offtake agreements. Mightily impressive stuff, and secured in a stable jurisdiction.

Osisko’s portfolio is anchored by its 5% NSR royalty on the Canadian Malartic Mine (CMM), which is Canada’s largest operating open-pit gold mine. It is is owned equally by Agnico Eagle Mines and Yamana Gold and has been operating since 2011.

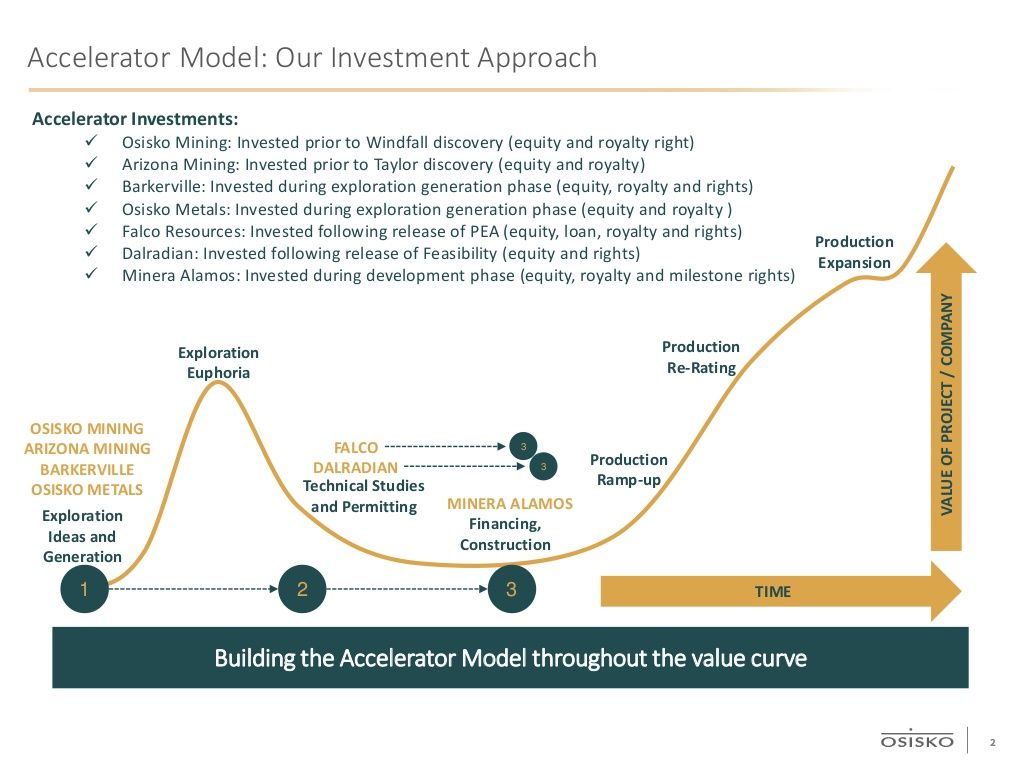

Away from its impressive royalty portfolio, Osisko also owns an additional portfolio of public resource companies, featuring interest in Osisko Mining, Falco Resources and Barkerville Gold Mines. This is an unconventional royalty investment package, and it is little surprising to see the company with a mammoth C$2.5Bn market cap. But the company has its detractors who bemoan the lack of return and distraction of the private equity component. Roosen disagrees as this is where he believes the most upside resides.

This journey of growth has been quite remarkable. When it first started operating, Osisko Gold Royalties owned 4 royalties. While these included its current flagship royalty, the others were in the form of a 2% NSR on Hammond Reef, Upper Beaver, Kirkland Lake and Pandora. Today, the management team has taken this US$15M portfolio of investment along with US$157M cash and turned Osisko into the 4th largest precious metals royalty company in the world. It is an extraordinary accomplishment, which has established the company as one of the most important in Québec’s mining sector.

Osisko is now the largest investors in exploration in the Québec’s region, trading on the TSX and NYSE, carrying out over US$2Bn in transactions and holding a credit facility of US$450M. With such a strong balance sheet and worthwhile partners, the company could well be primed to grow even more. Net zero balance as Roosen describes it.

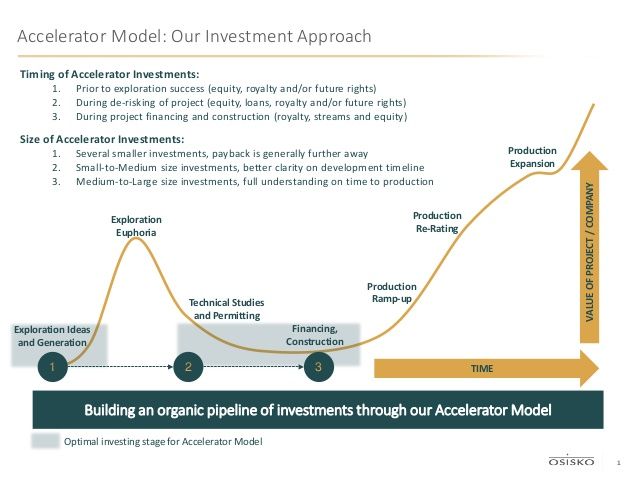

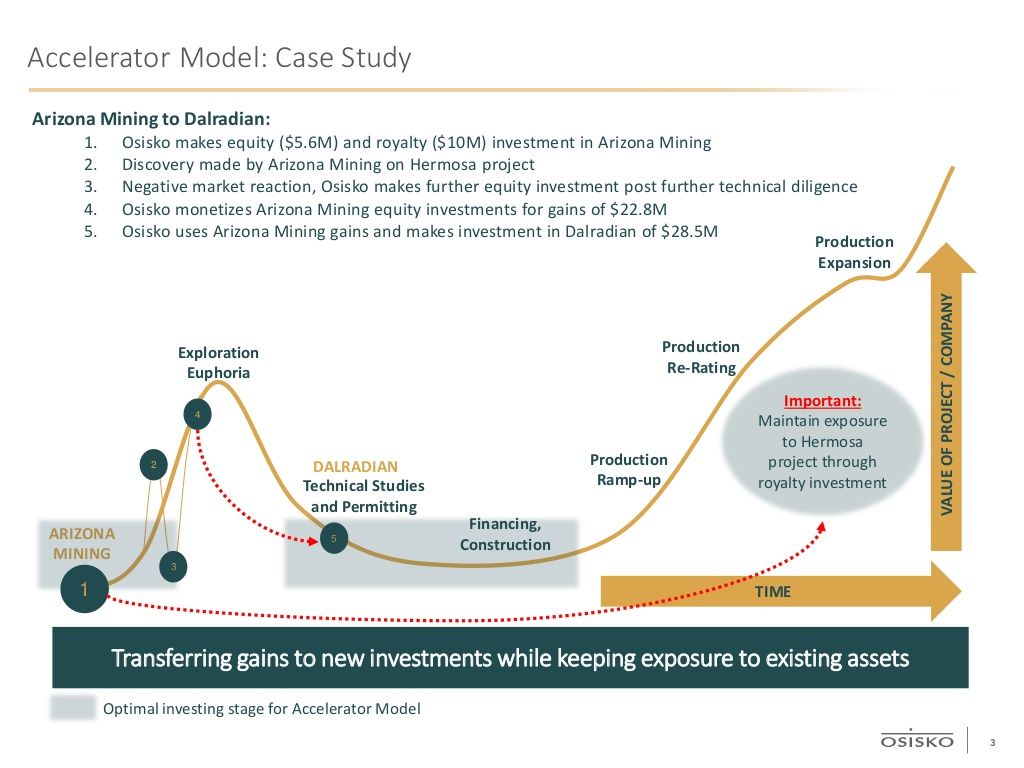

Osisko's hybrid business model is unique and accelerative.

This is an intricate methodology. It is good to see a coherent strategy on show for all to see. Whether you agree with it or not is up to you. But Roosen is a charismatic and larger than life character who has a track record of building big companies and the financial acumen to solve problem, eventually.

Investors can be incredibly impatient at times (nothing wrong with that as it keeps CEOs on their toes). However, Osisko Gold Royalties pays out a 1.5% dividend to shareholders, which is the best in the royalty sector, but investors will be hoping to see more value accretive decision making affecting the share price in what is the most positive gold environment in years. So what next? Roosen says he is "getting back to basics" and simplifying the message to the market. Wise words.

In terms of the share registry, this is a predominantly institutionally-held stock (c. 25%). The supportive Canadian government owns collectively 22% of the company. The stock is traded, and there is very little volatility. Just the what the doctor ordered. Companies that run a "pure royalty model" are more generally understood conventionally. Roosen feels that once the company's development-stage royalties turn into fully-fledged mines, this could be the inflection point for his company to experience dramatic share price growth. Even if the company wasn't to make another investment, its royalty portfolio would eventually double in size and primarily from "premium Canadian assets." The flow-through share programme and low-cost exploration offered by Canada ensures that Osisko Gold Royalties can enhance its revenue for years to come.

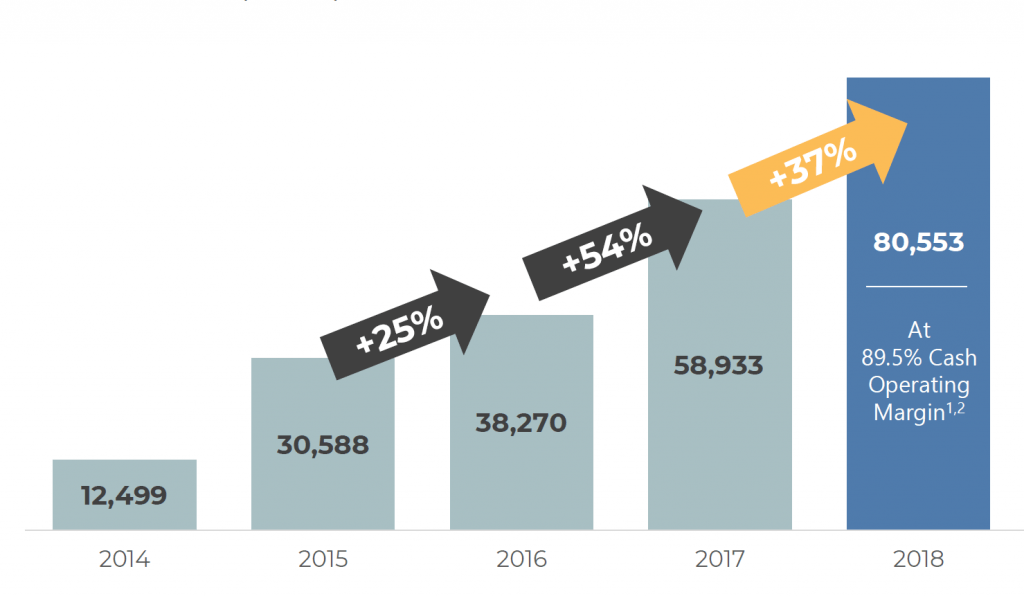

The company had US$423M in debt as of March 2020 and had drawn down US$92M of its credit facility. It has now drawn down a further US$50M in the wake of COVID-19 and raised US$85M in a private placement at a 10% premium. Impressively, the company has net income of over US$100M pa. It remains a strange reality that despite being well financed with such a clear plan, some royalty investors are still unsure.

The fundamentals of the company are great. In a downturn, it has the diversity and balance sheet to see out almost any storm. When things are on the up, it has enough capital available that it can accelerate projects. Osisko could well be a take-out target in the future; Roosen acknowledges that this company is the number 1 takeout target in the space, but he states that he will ensure investors get the payout they deserve no matter what.

The company's management changed last year, and some of the veterans from 2007 moved on. It was simply time for a refreshment, and Roosen feels the "eagerness and the hunger" has been revitalised in the new management team.

So, why invest in Osisko in the next 12-months? A big re-rating could be on the horizon with the underground development at the Malartic Mine. The company has managed to avoid a reduction in its royalty and will receive exposure to a really aggressive exploration programme. The evolution of Barkerville is also likely to be integral, and this should happen by the end of the year. With a few deals "in the hopper" and poised for completion, these catalyst moments are what Mr Roosen hopes will catch the markets attention again.

What did you make of Sean Roosen and Osisko Gold Royalties?

Analyst's Notes

Subscribe to Our Channel

Stay Informed