Revival Gold Announces Promising PEA for Mercur Gold Project

.webp)

Revival Gold's Mercur PEA shows strong economics: 95,600 oz/year for 10 years, 27-57% IRR, $208MM capex, trading at just 0.1x NAV and $8/oz, with recent gold deals setting precedent for significant re-rating potential.

- Revival Gold's Preliminary Economic Assessment (PEA) shows 95,000 to 105,000 ounces of annual gold production over a 10-year mine life, with a $294 million NAV and 27% IRR at $2,175 gold.

- At current gold prices ($3,000), the project's NAV increases to $752 million with an IRR of 57%, making it highly attractive for development.

- The Mercur project is on private patented claims, simplifying the permitting process to approximately 2 years through a state process rather than federal.

- The project benefits from its brownfield status, previous mining history, and proximity to Salt Lake City (1 hour away), reducing operational risks and capital requirements.

- Revival Gold plans to advance the project through metallurgical testing, drilling, and baseline environmental studies, with construction potentially beginning in 2-2.5 years.

Revival Gold recently announced promising results from their Preliminary Economic Assessment (PEA) for the Mercur gold project. The assessment highlights the project's economic potential, strategic advantages, and development timeline as the company positions itself as an emerging gold producer in the Western United States.

Economic Highlights and Project Fundamentals

The PEA demonstrates robust economics with projected annual gold production of 95,000 to 105,000 ounces over a 10-year mine life (averaging 95,600 ounces annually). At a gold price of $2,175 per ounce, the project shows a Net Asset Value (NAV) of $294 million and a 27% Internal Rate of Return (IRR) after tax. These numbers become even more impressive at current gold prices around $3,000 per ounce, where the NAV jumps to $752 million with an IRR of 57%.

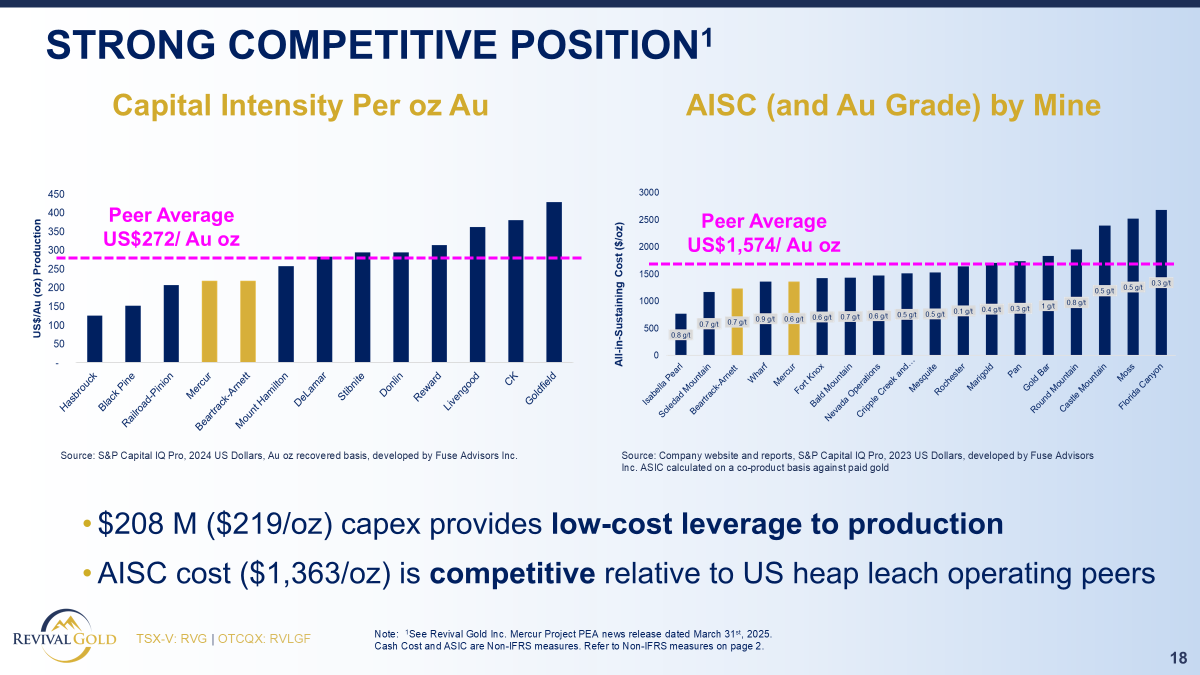

The project features modest upfront capital costs of $208 million, including working capital and all equipment lease costs. Operating costs are competitive with Cash Costs of $1,205 per ounce of gold and All-in Sustaining Costs (AISC) of $1,363 per ounce. Hugh Agro, President and CEO stated

"It's an outstanding result for Revival Gold. We are at 95 to 105,000 ounces of gold production typically from the project, PEA averaging 95,000 ounces a year over a 10-year mine life, a $294 million of NAV, more than doubling our underlying NAV in the company."

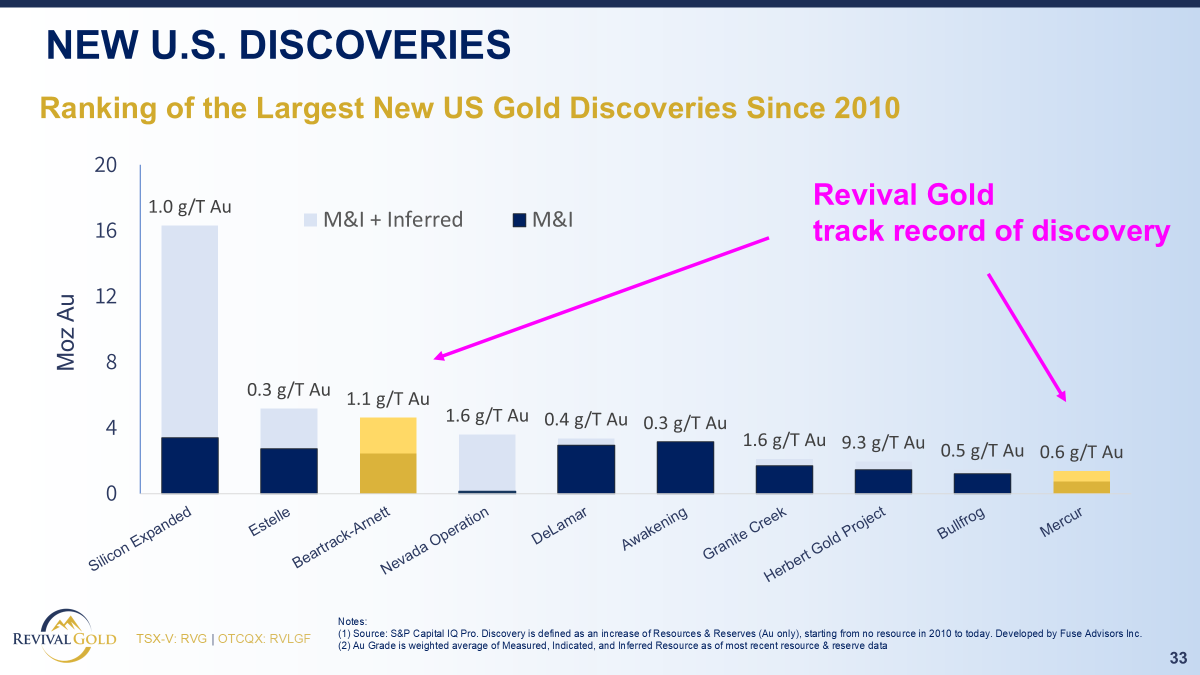

The resource base consists of approximately 1.4 million ounces of gold, with over 50% in the indicated category and the remainder in the inferred category. The average grade is 0.6 grams per ton, with metallurgical recovery rates averaging 75%. This level of resource confidence comes from extensive historical data and approximately 250 kilometers of drilling.

Project Location and Infrastructure Advantages

The Mercur project benefits significantly from its strategic location just an hour's drive from Salt Lake City, Utah, and approximately 30 minutes from a community of 40,000 people. This location provides ready access to equipment, services, skilled labor, and infrastructure without requiring a camp or remote-site logistics.

"Talking about a project that's located an hour's drive from Salt Lake City, where many of the dealers have offices based, for example, Caterpillar, we can get equipment and people very efficiently. Spares, no requirement for a camp, this is not a greenfield situation. It's a relatively low-risk, relatively attractive to staff kind of opportunity, and there aren't very many of those around."

This advantageous location translates to lower capital expenditure requirements and reduced operational risks compared to more remote projects, giving Revival Gold a competitive advantage in the development landscape.

Permitting and Development Timeline

A significant advantage of the Mercur project is its location on patented (private) claims, which allows Revival Gold to pursue permits through a state process rather than the typically more complex federal process. The company believes this will streamline the timeline, potentially allowing them to complete permitting within two years.

"Remember this project is located on patented claims, that is private claims, so we go through a state process, and we think we can get it all done within two years."

The company has outlined a two-phase development approach. The first phase involves approximately 20,000 meters of drilling to convert inferred resources to measured and indicated categories, along with collecting additional metallurgical samples. The second phase will focus on completing a Pre-Feasibility Study (PFS) and advancing the permitting process. The combined budget for these phases is approximately $8 million, relatively modest for a project of this scale.

"If all's going well, you know, we could be in a situation where we're turning a shovel, that is ready to start construction, you know, within the next two, two and a half years."

Technical Considerations and Risk Mitigation

The Mercur project carries lower technical risk than many comparable projects due to its brownfield status. The site has been previously mined using open-pit methods and processed through heap leaching, providing valuable historical data and operational insights.

John Meyer, VP of Engineering and Development, highlighted that their approach differs from previous mining at the site:

"The way the project was mined in the past, they were really looking for the high grade. We are mining largely lower grade, and we're mining more of the disseminated zones around those higher grades, so our task is easier from that perspective."

A key technical focus is on metallurgy, particularly managing carbonaceous material that could affect gold recovery. The team has modeled these zones in detail, which represent approximately 9% of the leachable gold. Their mining plan includes stockpiling this material for processing during the final two years of the mine life to reduce operational risk.

"We've gone to great lengths to model those carbonaceous zones... From the mining perspective, when we run across them during the first eight years of mining operation, we stockpile those materials and we don't begin to process any of those materials that have the potential for carbon materials until the last two years of mine life."

The project benefits from highly oxidized ore at depth, simplifying processing, and minimal environmental challenges with no perennial streams on site and very deep groundwater levels.

Environmental and Social Considerations

Environmental factors appear favorable for the Mercur project. The site contains no perennial streams, deep groundwater (below pit bottoms), and no threatened or endangered species identified from previous studies. The primary environmental baseline work will focus on cultural artifacts from historical mining and wildlife surveys. Meyer addressed environmental concerns directly:

"We don't have any threatened or endangered species that we're aware of on the site. That was the case for Barrick, so we expect it would certainly be the case for us. But those studies still have to happen, and we're fortunate because they can happen concurrent to our exploration activities."

The heap leach processing method eliminates the need for tailings facilities, reducing environmental footprint and associated risks. The company also notes that previous reclamation at the site has been successful without requiring synthetic liners, suggesting favorable environmental characteristics of the rock.

Corporate Portfolio and Market Valuation

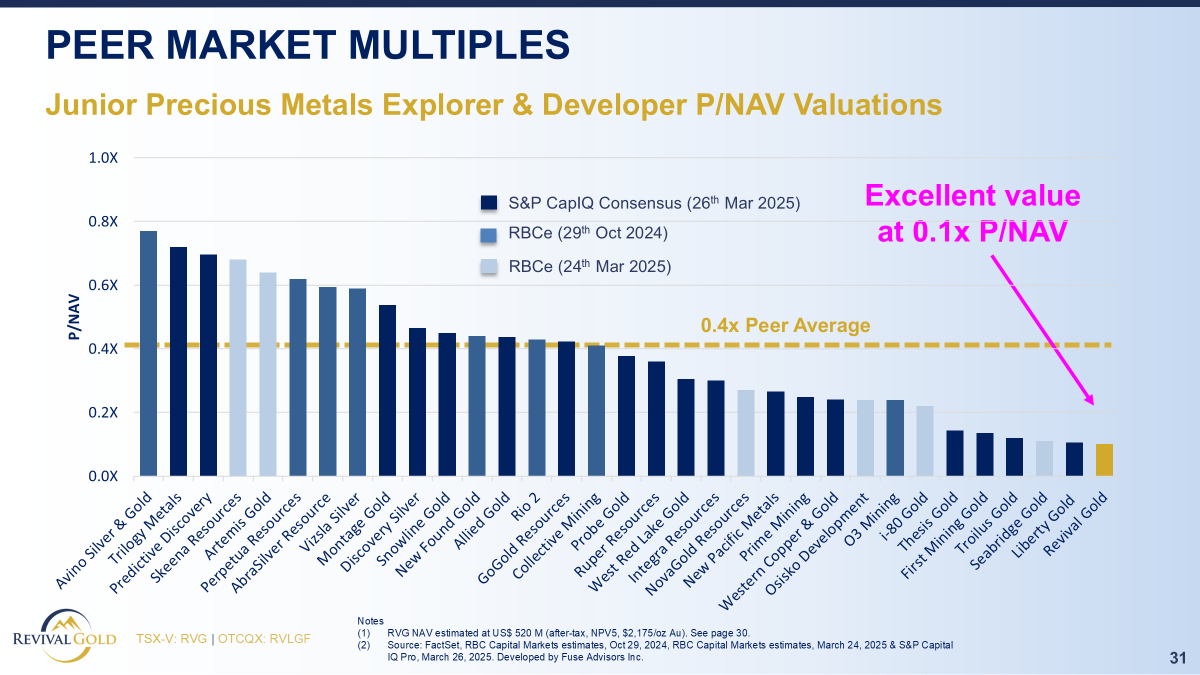

Revival Gold's overall portfolio now includes both the Mercur project and the Beartrack-Arnett project, representing a combined resource of approximately 6 million ounces of pure gold (not gold equivalent), with more than half in the Measured & Indicated category. The combined NAV at $2,175 gold is $520 million, increasing to $1.2 billion at $3,000 gold.

With a current market capitalization of approximately $50 million, the company is trading at just 0.1x NAV and $8 per ounce of gold resource, suggesting significant potential for value re-rating as the projects advance.

"The combined portfolio is half a billion dollars of underlying gold NAV, 160,000 ounces a year of production potential, and 6 million ounces of resource, all in the Western United States. I can tell you there is a lot of interest in the data and from corporates in what we're doing."

Financing Strategy and Market Context

Revival Gold is taking a measured approach to financing the project's development. Management and board members own approximately 15% of the company, aligning their interests with shareholders and creating sensitivity to dilution. Agro emphasized

"Dilution matters to this management team and to our owners, and so we'll be very careful about that.”

He noted that the company is exploring various funding options, including strategic partnerships, mergers and acquisitions, creative financing structures, and traditional equity.

Recent market transactions demonstrate strong appetite for North American gold projects. Notable examples include Musselwhite's sale to Orla for $850 million (approximately 1.1x NAV or $280/oz of resource), with Orla's stock more than doubling in the following 4.5 months. Similarly, CC&V sold to SSR for $275 million plus assumption of closure/environmental liabilities, representing approximately 1.9x NAV or $240/oz of resource, with SSR's stock up 50% in 3.5 months.

"The gold's not going anywhere. In the last five years, the value of that gold in the ground has gone up about $1.5 billion. It's not going anywhere, so the last thing we want to do is rush to get through the process of spending our shareholders' money and diluting our capital structure with the wrong money, the wrong path, and the wrong set of hands."

The Investment Thesis for Revival Gold

- Robust Project Economics: Mercur PEA demonstrates strong economics with 95,600 oz annual gold production over 10 years, modest $208MM initial capital, and competitive costs ($1,205/oz Cash Cost, $1,363/oz AISC).

- Significant Gold Price Leverage: At $2,175 gold, the project delivers $294MM NPV (5%) and 27% IRR; at $3,000 gold, these metrics increase to $752MM NPV and 57% IRR.

- Substantial Resource Base: Combined portfolio of 6 million ounces of pure gold resources (not gold equivalent) across two projects, with more than half in the M&I category.

- Compelling Valuation: Current $50MM market cap represents just 0.1x NAV and $8/oz of gold resource, suggesting significant potential for re-rating.

- Simplified Permitting Path: Located on patented (private) claims, allowing for state-level permitting expected to be completed within two years.

- Low-Risk Jurisdiction: Located in mining-friendly Utah, just one hour from Salt Lake City, with excellent infrastructure and access to skilled labor.

- Brownfield Advantage: Previous mining history reduces operational and technical risks while providing valuable data for development planning.

- Clear Development Timeline: Potential construction decision within 2-2.5 years, making this a near to mid-term production opportunity.

- Strong Market Comparables: Recent transactions for North American gold projects (Musselwhite, CC&V, Valentine Lake) demonstrate strong appetite and premium valuations for quality assets.

- Aligned Management Interests: Approximately 15% insider ownership creates strong alignment with shareholders and sensitivity to dilution.

Macro Thematic Analysis

The gold market has demonstrated remarkable strength in 2025, with prices exceeding $3,000 per ounce driven by central bank purchases, inflation concerns, and geopolitical tensions. This price environment transforms the economics of development-stage gold projects like Revival Gold's Mercur project, where NAV increases from $294 million to $752 million and IRR jumps from 27% to 57% when comparing $2,175 to $3,000 gold prices.

While capital markets remain challenging for junior mining companies, this extraordinary price environment is attracting new pools of capital seeking exposure to near-term production stories with manageable capital requirements. Recent transactions highlight this trend, with Musselwhite selling to Orla for $850 million (~1.1x NAV or $280/oz) and CC&V selling to SSR for $275 million plus liabilities (~1.9x NAV or $240/oz). Both acquirers saw significant share price appreciation following these deals, demonstrating the market's reward for companies securing quality gold assets.

Revival Gold's current trading multiple of 0.1x NAV ($8/oz resource) represents a stark discount to these transaction metrics, suggesting substantial upside potential as the company advances its projects toward production. With 6 million ounces of resources, a combined NAV of $520 million (at $2,175 gold) increasing to $1.2 billion (at $3,000 gold), and a clear development pathway, Revival Gold represents one of the few North American development opportunities with meaningful scale and a straightforward path to production. As CEO Hugh Agro notes:

"There is a lot of exploration potential... and importantly alongside of the PEA, we've been able to complete a schedule for permitting... This project is located on patented claims, that is private claims, so we go through a state process, and we think we can get it all done within two years. It's a great result to be announcing today."

Analyst's Notes

Subscribe to Our Channel

Stay Informed