Strait of Hormuz Disruption & Copper Supply Constraints Tighten the Financing Window for Near-Term Developers

Strait of Hormuz disruption and China's sulfuric acid export ban tighten copper supply, redirecting institutional capital to near-term developers.

- Iran's control of the Strait of Hormuz sustained crude risk premiums and accelerated renewable generation procurement in China and the Asia-Pacific region, where copper-intensive deployment had surged since the conflict began.

- LME copper traded at US$13,030 per tonne on May 5, 2026, holding above J.P. Morgan's medium-term support zone of US$11,100 to US$11,200 per tonne, because supply-side disruption rather than demand strength is setting the floor.

- China's sulfuric acid export ban effective May 1, 2026 placed approximately 200,000 tonnes of Chilean cathode production at risk per Goldman Sachs, raising the strategic premium attached to oxide developers with secured regional acid supply and existing solvent extraction-electrowinning access.

- Developers targeting final investment decisions in the second half of 2026 and through 2027 are capturing institutional capital ahead of greenfield peers because permitted status, defined feasibility economics, and oxide flowsheets reduce the cost of debt in a constrained equity market.

Strait of Hormuz Disruption Repriced Energy Security Risk Across Industrial Economies

The Strait of Hormuz typically carries roughly one-fifth of seaborne petroleum trade, and Iran's confirmed control of the corridor, reiterated by Islamic Revolutionary Guard Corps commander Yadollah Javani on May 4, 2026, sustained crude risk premiums through the Labor Day period and raised the implied cost of imported hydrocarbons for energy-deficient economies in Europe and Asia.

Higher imported energy costs improve the relative economics of domestic wind, solar, and nuclear additions because each megawatt of renewable capacity consumes materially more copper than the fossil fuel generation it displaces. Commonwealth Scientific and Industrial Research Organisation confirmed on May 8, 2026 that renewable energy systems can require up to five times more copper per unit of generation capacity than fossil fuel-based systems, with the differential concentrated in transmission and distribution rather than generation hardware.

Oil Supply Instability Accelerated Renewable Energy Procurement

Renewable energy demand had surged in China and the Asia-Pacific region following the outbreak of the conflict, with state-directed capacity additions concentrated in nuclear and grid-scale solar. China's expansion of high-voltage transmission and nuclear generation embeds copper consumption across both generation and distribution layers for asset lives of 25 to 60 years, anchoring demand growth in capital programmes that do not retract with industrial activity. The demand impulse runs against a mature global production base with declining head grades.

Merlin Marr-Johnson, President and Chief Executive Officer of Fitzroy Minerals, identifies the mismatch between accelerating electrification demand and the capacity of the industry to respond:

“There are many other houses and groups forecasting a copper crunch, which is going to come as demand from electrification, data centers, EVs, and all of that continues to drive demand.”

AI Infrastructure & Electrification Increased Copper Intensity Across Global Power Systems

Hyperscale data centre construction is adding baseload electricity demand at the same time grid operators are absorbing accelerated electric vehicle adoption and renewable interconnection backlogs. Each layer consumes copper across high-capacity cabling, substations, transformers, switchgear, and cooling systems, while mine supply faces declining discovery rates, multi-year permitting timelines, and the May 1, 2026 Chinese sulfuric acid export ban.

Data Centre Buildout Added Baseload Demand to a Constrained Grid Cycle

Copper futures climbed above US$6.20 per pound on expectations that artificial intelligence infrastructure, power grid modernisation, and clean energy investment would sustain long-term demand. Bloomberg stated that consensus mine supply forecasts for 2026 to 2027 continue to assume project ramp-up schedules that historical data do not support, and that copper must remain above US$10,000 per tonne to sustain incremental supply growth based on the current cost curve of operating mines.

Copper Prices Held Above Incentive Levels Because Supply Growth Lagged Infrastructure Demand

Goldman Sachs maintained its 2026 copper price forecast at US$12,650 per tonne on April 21, 2026, while flagging the May 1 Chinese sulfuric acid export ban as a binding downside risk to Chilean supply. J.P. Morgan identified US$11,100 to US$11,200 per tonne as the medium-term support zone, attributing sustained price strength to supply-side disruption rather than demand expansion. Copper assets capable of reaching commercial production before 2030 are commanding strategic valuation premiums because greenfield permitting, financing, and construction timelines typically exceed seven years from discovery.

Producer capital allocation reflects this view. Jonathon Deluce, President and Chief Executive Officer of Abitibi Metals, identifies the change in major-company behaviour relevant to institutional positioning:

“The majors are starting to bet that this is a sustained gold market and the early stage of a copper bull rally, where we see sustainable increases in the copper price.”

Sulfuric Acid Constraints Repriced Oxide Copper Projects with Secured Processing Access

Sulfuric acid feed has become a binding input constraint for solvent extraction-electrowinning, the dominant processing route for oxide copper in Chile. Goldman Sachs estimated that Chile sourced roughly one-third of its sulfuric acid imports from China in 2025, and that a year-long Chinese export ban would put approximately 200,000 tonnes of Chilean cathode production at risk, equivalent to 1% of global supply. J.P. Morgan specified that roughly 15% of global copper production is directly reliant on sulfuric acid availability.

Chinese Acid Export Ban Exposed Processing Vulnerability in Chile

The Chinese export ban running from May through at least December 2026 is targeted to remove approximately 3 million tonnes of sulfuric acid from the seaborne market, affecting Chile, Indonesia, and India as the largest importers. Chilean copper production declined approximately 6% in the first three months of 2026 versus the same period in 2025 even before the acid ban took effect, raising the financing premium attached to projects with secured regional acid supply, lower capital intensity, and shorter construction timelines.

Heap Leach & Solvent Extraction-Electrowinning Projects Gained Financing Relevance

Heap leach oxide operations carry materially lower upfront capital expenditure than sulphide concentrators because they avoid grinding circuits, flotation cells, and tailings storage facilities at scale, compressing payback periods and broadening the lender pool. Fitzroy Minerals signed a non-binding Letter of Intent with Sociedad Punta del Cobre on April 23, 2026 to process Buen Retiro material through Pucobre's Planta Biocobre electrowinning facility, which holds nameplate capacity of 9,600 tonnes of copper cathode annually and is currently significantly under-utilised. The arrangement is targeted to deliver approximately 10 million pounds of copper per annum, with commercial tolling terms targeted for negotiation within 90 days to support inclusion in the Pre-Feasibility Study economic model.

Marr-Johnson identifies the financing logic that distinguishes infrastructure-sharing structures from standalone development:

“We are working on terms with Pucobre to establish a heap leach joint venture. That operation gives us the potential for near-term, non-operated cash flow, which we think will distinguish us from many other explorers in the market. It would also provide non-operated cash flow with very low capital intensity.”

Developers Targeting Construction Decisions in 2026 to 2027 Are Capturing Institutional Capital

The pool of copper projects able to reach a final investment decision within the current price cycle is small, and equity capital is concentrated in names with permitted status, defined economics, and unencumbered balance sheets. Two categories are absorbing institutional flows: oxide developers with execution-ready feasibility studies, and polymetallic systems backed by equity from established mining counterparties.

Oxide Developers with Class 3 Engineering Are Re-Rating

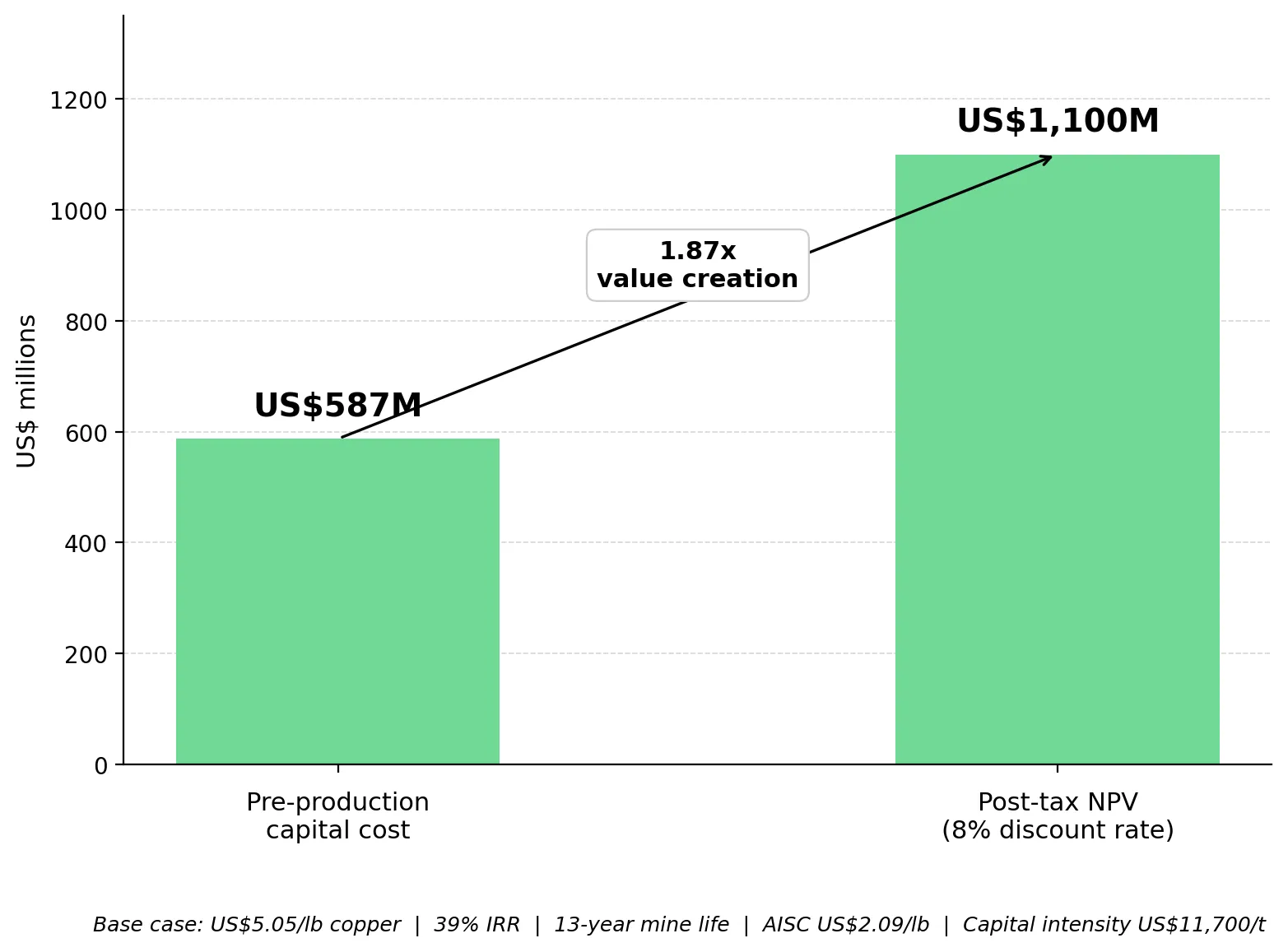

Marimaca Copper is targeting build-readiness for the Marimaca Oxide Deposit by the end of 2026. The 2025 Definitive Feasibility Study outlined a US$587 million upfront capital cost, a post-tax net present value (8% discount rate) of US$1.1 billion, and a 39% internal rate of return using a US$5.05/lb copper price assumption. The project carries all-in sustaining costs of US$2.09/lb over a 13-year mine life, placing it in the second quartile of global copper producers, with capital intensity of approximately US$11,700 per tonne of annual production capacity.

The study was completed to AACE Class 3 standards, with an estimated accuracy range of minus 20% to plus 25%. Environmental approval secured in November 2025 removed a major permitting risk ahead of construction, while budget quotations for roughly 80% of mechanical equipment reduced potential cost uncertainty ahead of a final investment decision targeted for the second half of 2026.

Capital discipline through detailed engineering is the recurring theme among developers entering construction in a high-capex inflation regime. Hayden Locke, President and Chief Executive Officer of Marimaca Copper, frames the trade-off that defines execution-phase decision-making:

“We do want to reduce capex, but every single design change that we make to reduce capex has to be considered within the broader impact on project risk. We’re going to take our time, and we’re going to increase the level of maturity of the project to make sure we minimize the level of variation that comes through as we move into the execution phase.”

Exploration Capital Concentrated on District-Scale Copper Systems & High-Grade Brownfield Restarts

Strategic value is migrating toward large, multi-decade copper deposits and brownfield restart assets because global supply growth beyond 2030 depends on a small number of greenfield discoveries and reactivations currently moving through resource definition. Investor capital is allocating to district-scale porphyry systems where geological scale supports a multi-decade production case, and to high-grade former operating mines where existing infrastructure compresses the development timeline to first production.

High-Grade Brownfield Restarts Compressed Development Timelines

Selkirk Copper closed an upsized C$35 million bought-deal private placement on April 30, 2026, capitalising restart evaluation of the Minto copper-gold-silver mine in Yukon. The Phase 1 drilling program completed 52,288 metres across 175 holes between August 2025 and March 2026, with hole 25SCM098 returning 6.60% copper, 5.18 grams per tonne gold, and 27.02 grams per tonne silver over 6.6 metres from 64 metres, ranking in the 98th percentile of more than 1,400 drill holes in the six-decade Minto database.

The Mineral Resource Estimate defined Indicated resources of 12.588 million tonnes at 1.203% copper, 0.461 grams per tonne gold, and 4.3 grams per tonne silver, supported by existing 4,100 tonne-per-day processing plant infrastructure, a 400-person camp, and connected powerline. The company is targeting a Preliminary Economic Assessment by mid-2026 and a restart decision in mid-2027.

The Investment Thesis for Copper

- Renewable generation, artificial intelligence infrastructure, and transportation electrification are embedded in national energy security policy in China, the European Union, India, and the US, anchoring copper demand in capital programs with 25-to-60-year operating lives rather than cyclical industrial activity.

- Goldman Sachs' estimate that the Chinese sulfuric acid export ban places approximately 200,000 tonnes of Chilean cathode production at risk has raised the strategic premium attached to copper supply originating outside concentrated geopolitical corridors, particularly Tier-1 jurisdictions in the Americas with established permitting frameworks.

- Developers with environmental approval, oxide flowsheets, secured regional infrastructure access, and AACE Class 3 engineering definition are capturing a lower cost of debt because shorter payback periods and bounded cost-variation envelopes expand the lender pool relative to greenfield sulfide alternatives.

- Producing assets reaching commercial output before 2028 are positioned for valuation expansion against incentive prices because BHP's August 2025 outlook forecasts zero Chilean production growth between 2031 and 2040, indicating that incremental supply must come from a small number of new builds and restarts.

- Explorers controlling district-scale porphyry systems in Chile with drill-confirmed hydrothermal architecture and demonstrable geological analogues to operating mines are positioned for strategic interest from producers replacing multi-decade reserves at the rate required to maintain output guidance.

The Strait of Hormuz disruption demonstrated that copper demand growth is now driven by energy security policy as much as by cyclical industrial activity. Renewable generation, artificial intelligence-related electricity demand, and transportation electrification have anchored copper consumption in capital programs whose operating lives exceed the typical permitting-to-production cycle for a new copper mine. China's sulfuric acid export ban, declining greenfield discovery rates, and Chile's August 2025 production outlook of zero growth from 2031 to 2040 continue to constrain the supply response. The gap between accelerating demand and constrained supply has concentrated institutional capital in oxide developers with permitted status and Class 3 engineering definition, polymetallic discovery-stage assets in Tier-1 Canadian jurisdictions, district-scale porphyry explorers in Chile, and high-grade brownfield restarts in stable jurisdictions.

TL;DR

LME copper closed at US$13,030 per tonne on May 5, 2026 as Iran's continued control of the Strait of Hormuz sustained crude risk premiums and China's sulfuric acid export ban placed approximately 200,000 tonnes of Chilean cathode production at risk per Goldman Sachs. Goldman maintained its 2026 copper forecast at US$12,650 per tonne while J.P. Morgan identified US$11,100 to US$11,200 per tonne as the medium-term floor, with both banks attributing price strength to supply-side disruption rather than demand expansion. BHP's August 2025 outlook of zero Chilean production growth between 2031 and 2040, combined with declining greenfield discovery rates and CSIRO's finding that renewable systems consume up to five times more copper than fossil fuel equivalents, has concentrated institutional capital in oxide developers with environmental approval and Class 3 engineering definition, district-scale porphyry explorers in Chile, and high-grade brownfield restart assets in Tier-1 jurisdictions positioned to deliver production into the 2027 to 2030 deficit window.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

.png)

Stay Informed