Structural Deficits & Macro Uncertainty Are Repricing Platinum Group Metal Assets

Platinum enters a supply-deficit era as macro demand rises, tightening inventories and boosting upside for PGM developers in stable jurisdictions.

- Platinum is entering a macro-driven demand regime where geopolitical risk and monetary uncertainty are directing investment flows beyond traditional industrial channels.

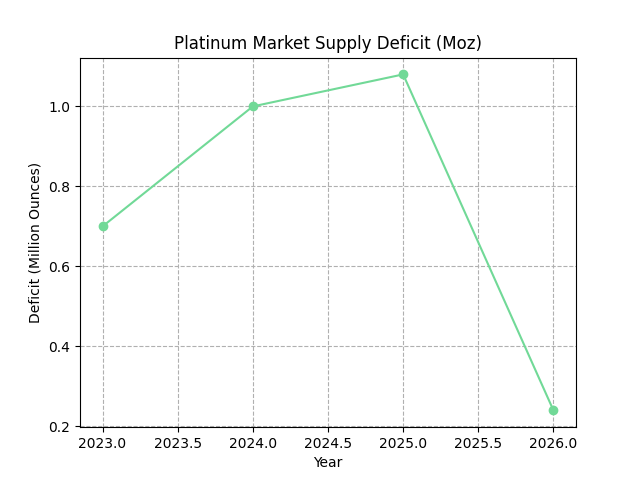

- Four consecutive supply deficits from 2023 through 2026 and above-ground inventories equivalent to roughly four months of global demand are tightening the market on a structural basis.

- Investment demand, particularly exchange-traded fund (ETF) holdings and bar and coin buying concentrated in China and the United States, is now the dominant marginal driver of price formation.

- Mine supply remains inelastic due to the deep, capital-intensive nature of underground platinum group metal (PGM) operations, with recycling the only near-term responsive source of incremental supply.

- Development-stage projects outside South Africa and Russia, such as ValOre Metals' Pedra Branca asset in Brazil, are attracting attention as the scarcity of jurisdictionally diversified PGM resources becomes a recognized valuation factor.

From Industrial Input to Macro-Sensitive Asset

Platinum has traditionally been priced as a cyclical industrial metal, driven by autocatalyst demand, jewellery consumption, and concentrated mine supply. That framework is now shifting.

In 2026, platinum is behaving more like a hybrid asset, still tied to industrial demand, but increasingly attracting investment flows typically reserved for gold and silver. The World Platinum Investment Council (WPIC) expects strong investment demand, supported by persistent supply deficits and macro-political uncertainty.

As a result, price formation is no longer dictated solely by automotive cycles or platinum-palladium substitution. Platinum is becoming more sensitive to macro factors such as geopolitics, trade tensions, and monetary policy. This raises a key question: if platinum is repricing as a macro asset, how should investors reassess exposure to PGM equities, especially developers and explorers.

A Structural Supply Deficit Meets Macro Demand

The platinum market is not operating near equilibrium. WPIC data indicates that the 2025 deficit reached approximately 1.08 million ounces (Moz), the deepest on record. The 2026 forecast projects a continued shortfall of roughly 240,000 ounces, marking the fourth consecutive annual deficit. Cumulatively, the market has absorbed a supply gap of approximately 3 Moz between 2023 and 2026.

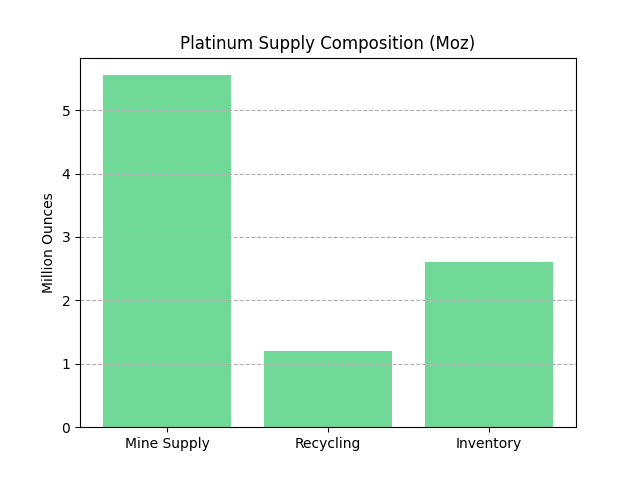

Above-ground inventories have declined to approximately 2.6 Moz, equivalent to just over four months of global demand. This figure is significant because inventories function as the primary shock absorber in commodity markets. When they fall below critical thresholds, price elasticity changes materially. Markets become more sensitive to incremental demand shifts, and the convex price response to supply disruptions becomes more pronounced.

Mine supply is forecast to remain essentially flat at approximately 5.55 Moz, constrained by the structural realities of deep-level underground mining concentrated in South Africa. Recycling supply, which is more price-elastic, is expected to increase by roughly 10 percent in response to elevated prices. On the demand side, automotive consumption remains supported by the continued growth of hybrid vehicles and a slower-than-anticipated transition to battery electric vehicles. Industrial demand is forecast to rebound by approximately 11 percent.

Investment Demand as the Marginal Price Setter

The key shift in 2026 isn’t just the supply deficit but who is driving demand. WPIC data shows sustained ETF holdings, bar and coin demand nearing a six-year high of about 725 koz, and strong buying from China with growing interest from India.

This reflects a broader macro rotation into hard assets amid geopolitical tensions, trade uncertainty including US Section 232 investigations, and persistent inflation, all of which are adding a risk premium to platinum.

Platinum’s appeal lies in its dual role. It trades at a discount to gold while retaining strong industrial demand from automotive, hydrogen, and chemical sectors. As a result, price formation is increasingly driven by financial flows and macro positioning, implying higher volatility and stronger sensitivity to interest rates, the US dollar, and geopolitics.

Supply Inelasticity & the Limits of Producer Response

One of the most consequential and frequently underestimated features of the platinum market is the rigidity of supply. Unlike copper or lithium, where new production capacity can be developed within a reasonably defined investment cycle, PGM supply is constrained by factors that operate on decade-length timescales.

South Africa accounts for approximately 70 to 80 percent of global platinum supply. Operations in that country are predominantly deep-level underground mines characterized by high capital intensity, rising all-in sustaining costs (AISC), complex labor relations, and increasing geological difficulty as ore bodies are accessed at greater depths. Development timelines from resource discovery to commercial production typically range from 10 to 15 years. These constraints mean that even sustained price elevation does not trigger a rapid supply response.

Reuters reporting has confirmed that producers operating at platinum prices in the range of approximately $2,300 to $2,900 per ounce are prioritizing shareholder returns over capacity expansion. AISC projections above $1,000 per ounce, combined with energy and labor inflation that shows limited signs of abating, mean that the economic case for greenfield development remains difficult to establish at current prices. For investors, this dynamic supports a view that supply-side constraints will persist, reinforcing the structural deficit and the price floor it implies

Jurisdictional Concentration & the Scarcity Premium

The geographic concentration of platinum supply introduces a layer of risk that has become more visible as geopolitical fragmentation accelerates. South Africa and Russia together account for approximately 80 to 90 percent of global platinum and palladium production. Both jurisdictions carry elevated country risk profiles. South Africa faces persistent operational challenges related to power availability, infrastructure reliability, and labor market complexity. Russia's position in global commodity markets has been fundamentally altered by sanctions regimes introduced following the 2022 invasion of Ukraine, with PGM supply chains among those affected.

In an environment where institutional capital is increasingly focused on supply chain security, the scarcity of development-stage PGM assets in politically stable, mining-friendly jurisdictions outside these two dominant regions is becoming a recognized valuation factor. Projects that offer exposure to meaningful resource scale in diversified geographies are attracting attention that would not have been warranted in a less geopolitically complex supply environment.

Strategic Optionality in Brazil

ValOre Metals' Pedra Branca project, located in northeast Brazil, represents one of the few advanced-stage PGM development assets positioned outside the traditional South Africa-Russia supply axis. The project hosts a National Instrument (NI) 43-101 compliant inferred resource of 2.2 Moz graded at approximately 1.08 grams per tonne (g/t) in combined platinum, palladium, and gold (2PGE+Au).

Near-surface mineralization extending to open-pittable depths offers a potential capital expenditure advantage relative to the deep underground operations that define the dominant supply base. Brazil's classification as a mid-tier mining jurisdiction with established regulatory frameworks and critical minerals policy support adds further strategic context.

Nick Smart, Chief Executive Officer of ValOre Metals, describes the infrastructure positioning directly:

"Brazil has a lot of what you're looking for in terms of infrastructure. We're about four hours from the state capital, with a paved highway that runs to the project site. There is good electrical infrastructure. Those would not be the sort of infrastructure benefits you’d have if you were developing a project in Africa."

Resource Progression & Development Catalysts

In junior mining, valuation is driven by milestone progression, with re-ratings tied to technical and economic derisking. For development-stage PGM companies, this includes upgrading resources, validating metallurgy, and advancing from PEA to feasibility. At Pedra Branca, test work supports flotation for fresh rock with recoveries in the high 70 percent range, while bioleaching is being evaluated for oxide material, offering potential reductions in capital intensity and operating costs.

Nick Smart contextualizes the significance of the metallurgical program and the anticipated PEA:

"The main ambition of the PEA is to show the economics of the project, proving the viability of what we've got on the ground. You have real potential to achieve high levels of extraction, high recoveries, and a very low-cost processing route."

ValOre targets a PEA by Q4 2026, which will define key metrics such as NPV, IRR, AISC, and mine life. This marks the transition from a geology-driven, EV/oz valuation to an economics-based EV/NPV framework. PEA releases often act as major re-rating catalysts, expanding institutional comparability and broadening the investor base.

Capital Structure, Financing Conditions & Development Outlook

Junior mining developers operate within a structurally capital-constrained ecosystem. Exploration and development activities are funded predominantly through equity issuance, making dilution risk an inherent feature of the asset class. Access to capital, and the cost at which it can be raised, is directly tied to macro sentiment toward the underlying commodity and the perceived quality of the specific asset.

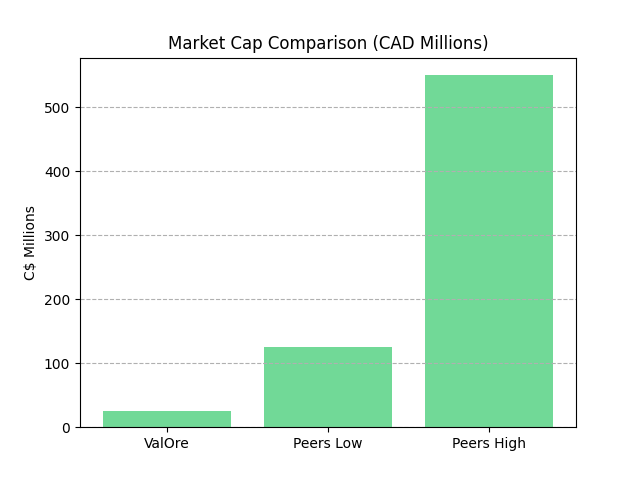

ValOre has a market cap of ~C$26 million, well below peers at C$126–550 million, and is backed by Discovery Group, which has raised over C$1 billion historically. About 55% insider and aligned ownership supports long-term alignment and reduces agency risk.

Pedra Branca’s current R&D budget is ~C$4 million, with additional capital needed for permitting and a demonstration plant to validate bioleaching at scale. Production is targeted to grow from 10,000-15,000 oz per year to 150,000–200,000 oz longer term, with strong platinum market conditions supporting future financing.

The Investment Thesis for Platinum

- Structural supply deficits in the range of 500,000 to over 1 million ounces annually provide a durable price floor that is not contingent on demand acceleration, but rather on supply remaining inelastic relative to a stable demand base.

- Investment demand has become the dominant marginal price driver in the platinum market, meaning price formation is now sensitive to macro capital flows, ETF activity, and portfolio allocation decisions in ways that add upside optionality beyond what industrial demand cycles alone would support.

- Mine supply is structurally constrained by the geology, capital intensity, and development timelines of deep-level South African operations, with no credible near-term expansion pipeline capable of resolving the multi-year cumulative deficit.

- Low above-ground inventories, currently at approximately four months of global demand cover, increase the convexity of price responses to incremental demand or supply shocks, benefiting investors with long exposure.

- Jurisdictional concentration in South Africa and Russia creates a scarcity premium for development-stage assets located in stable, mining-permissive jurisdictions outside those regions, a premium that is likely to expand as geopolitical fragmentation intensifies.

- Development-stage companies offer leveraged exposure to metal price appreciation combined with project-specific catalysts such as PEA publication, metallurgical validation, and resource expansion that can generate step-change re-ratings independent of commodity price movement.

- Capital structures with high insider alignment reduce agency risk and improve the probability that development capital is deployed in ways that preserve and build long-term asset value rather than funding management costs or short-cycle exploration programs.

- Development timelines for assets approaching PEA-stage, such as ValOre's Pedra Branca project, are aligned with a multi-year demand growth environment supported by hydrogen economy investment, hybrid vehicle production, and continued industrial sector demand recovery.

Platinum's role in investor portfolios is being redefined. The convergence of structural supply deficits, critically low above-ground inventories, and rising investment demand driven by macro-political uncertainty is changing how the market assigns value to both the metal and the equities of companies developing it.

The supply-side architecture of the platinum market, dominated by deep South African mines with multi-decade development lead times, ensures that the current deficit regime is not a condition that producers can resolve through conventional capital allocation cycles. The investment opportunity that follows is not limited to spot price exposure. It extends across the equity value chain, with particular relevance to development-stage assets in jurisdictions that offer both geological scale and political stability outside the traditional supply base.

The central question for institutional and sophisticated retail investors is not whether platinum prices will remain volatile.

The structural conditions are clear, and volatility is the expected outcome of low inventories meeting a financialized demand regime. The relevant question is whether investors have positioned themselves to capture the asymmetric upside created when durable physical scarcity intersects with macro capital seeking hard asset exposure.

TL;DR

Platinum is transitioning from a purely industrial metal into a macro-sensitive “hybrid asset,” driven by sustained structural supply deficits, critically low inventories, and rising investment demand (ETFs, bars, coins). With mine supply largely inelastic due to deep, capital-intensive operations concentrated in South Africa and Russia, the market cannot quickly respond to higher prices, creating a durable supply-demand imbalance. This shifts price formation toward macro factors like geopolitics, inflation, and monetary policy, increasing volatility but also upside convexity. As a result, development-stage PGM assets, especially those in stable jurisdictions like Brazil, are gaining a scarcity premium, offering leveraged exposure to both platinum prices and project-specific catalysts.

FAQs (AI generated)

Platinum is no longer priced solely on industrial demand (e.g., autocatalysts or jewelry); it is increasingly influenced by macroeconomic forces such as inflation, geopolitical risk, and capital flows into hard assets. Investment demand, particularly ETFs and physical buying, has become the marginal price setter, similar to gold and silver. This dual exposure means platinum now reacts both to economic cycles and financial market sentiment, making it more volatile but also more attractive as a portfolio diversifier.

The deficit is primarily a function of constrained mine supply and steady-to-growing demand. Most platinum comes from deep underground mines in South Africa, where high costs, technical complexity, and long development timelines (10-15 years) limit production growth. Producers are also prioritizing shareholder returns over expansion. Meanwhile, demand remains resilient due to hybrid vehicle production, industrial recovery, and increasing investment flows, resulting in multiple consecutive years of supply shortfalls.

Inventories act as a buffer in commodity markets. With platinum inventories now covering only about four months of global demand, the market has limited capacity to absorb shocks. This creates “convexity” in price behavior, small increases in demand or disruptions in supply can lead to disproportionately large price movements. For investors, this dynamic enhances upside potential but also increases short-term volatility.

Platinum supply is heavily concentrated in South Africa and Russia, both of which carry elevated geopolitical and operational risks (e.g., power instability, labor issues, sanctions). As global supply chains become more fragmented, investors are placing a premium on assets located in politically stable jurisdictions. This has elevated the strategic value of development-stage projects outside traditional supply regions, as they offer diversification and reduced geopolitical exposure.

These companies provide leveraged exposure to rising platinum prices while also offering independent catalysts such as resource upgrades, metallurgical validation, and economic studies (e.g., PEA). In a structurally undersupplied market, projects in stable jurisdictions with scalable resources, like Brazil, are increasingly scarce and valuable. As they advance toward production, their valuation can shift significantly from exploration-based metrics (EV/oz) to economics-driven metrics (EV/NPV), often resulting in step-change re-ratings.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

Stay Informed