Supply Constraints Define Copper’s Long-Term Investment Case as Near-Term Surplus Caps Price Discovery

Copper surplus through 2026 caps prices, but falling grades, rising capex, and policy-driven demand sustain a structural supply deficit supporting long-term upside.

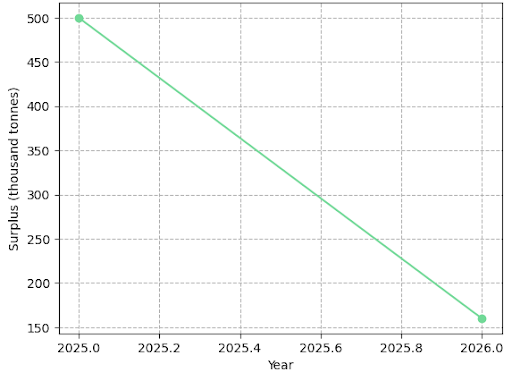

- Copper’s near-term price trajectory is constrained by an estimated 500,000-tonne surplus in 2025 and approximately 160,000 tonnes in 2026, according to Goldman Sachs forecasts, capping prices in the $10,000 to $11,000 per tonne range.

- Structural demand from grid electrification, electric vehicles, and artificial intelligence infrastructure is policy-driven and non-cyclical, maintaining long-term consumption regardless of short-term economic conditions.

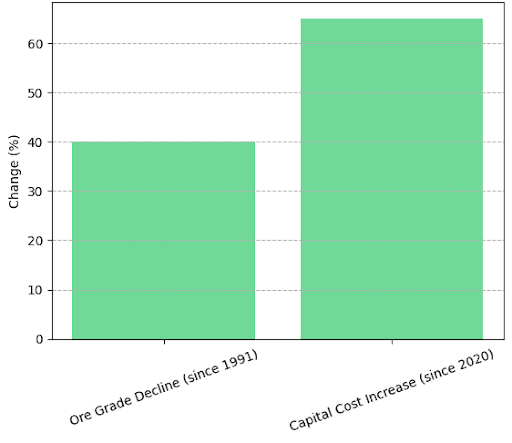

- Supply-side elasticity is materially limited by ore grade deterioration, which has declined approximately 40% since 1991, alongside permitting timelines that routinely exceed a decade and capital costs that have risen 65% since 2020.

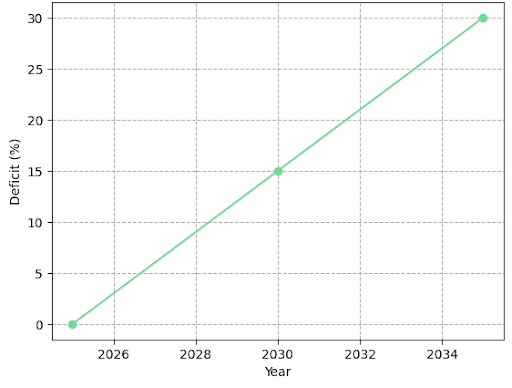

- The International Energy Agency (IEA) projects a potential 30% supply deficit by 2035, creating a structural pricing floor that near-term surplus conditions do not eliminate.

- The current environment rewards differentiated exposure across the development spectrum, with oxide-focused developers offering lower capital intensity and explorers in supply-constrained jurisdictions providing resource growth optionality.

Supply Surplus as a Transient Condition, Not a Structural Signal

Copper markets are operating under a near-term surplus that reflects post-stimulus demand normalization in China, elevated scrap supply at higher price levels, and inventory accumulation partially driven by tariff-related stockpiling. Goldman Sachs projects a surplus of approximately 500,000 tonnes in 2025 narrowing to 160,000 tonnes in 2026, with prices expected to remain range-bound between $10,000 and $11,000 per tonne. These conditions have reinforced a tactical ceiling on price discovery and contributed to multiple compression across copper equities.

Recent price strength is partly driven by speculative positioning rather than physical demand, with ~$30 billion in momentum inflows elevating prices above consumption signals and increasing the risk of unwind-driven corrections. The question is whether the current surplus, driven by demand normalization and scrap elasticity, reduces the structural supply deficit identified by institutional forecasts.

The surplus reflects timing effects, not a change in end-use demand, while sovereign-backed electrification and digital infrastructure investment continue to expand copper intensity and sustain deficit conditions. Copper therefore operates on two timelines, a near-term surplus that caps prices and adds volatility, and a long-term deficit that requires higher prices to incentivize new supply.

Electrification & AI Infrastructure as Durable Consumption Drivers

Copper demand is no longer fully explained by GDP-linked cycles, as incremental consumption is increasingly driven by capex-anchored segments, power grids, EV infrastructure, and AI data centers, linked to policy and utility investment rather than short-term economic activity. This reduces cyclical sensitivity and increases demand visibility, positioning projects deliverable within three to five years, especially those with lower capex, shorter timelines, and existing infrastructure, to capture a structural premium.

Marimaca Copper Corp. is advancing its Marimaca Oxide Deposit (MOD) toward a construction decision, with a completed Definitive Feasibility Study (DFS) confirming industry-leading capital and operating cost metrics.

The company’s Chief Executive Officer, Hayden Locke, summarizes the project’s development position:

“We delivered the DFS, effectively the final piece before transitioning into financing, detailed design, and engineering for the Marimaca Oxide deposit, which confirms what we already knew: industry-leading capital costs, highly competitive operating costs, and top-tier return on invested capital.”

The oxide deposit format is particularly relevant in this context. Oxide mineralization processed through heap leaching and solvent extraction-electrowinning typically requires lower upfront capital and shorter construction timelines than conventional sulphide operations. This positions Marimaca to deliver near-term copper supply into a market where structural demand is building and permitting constraints are limiting new project entry from conventional development pathways.

Grade Decline, Permitting & Capital Intensity

Copper’s long-term price outlook is anchored on supply constraints: ore grades have declined ~40% since 1991, increasing material throughput requirements, while capital intensity has risen ~65% since 2020 due to cost inflation and greater geological complexity. The IEA projects that without new project approvals and faster development, the market could face a ~30% supply deficit by 2035.

Permitting timelines are a primary constraint on supply elasticity, with development from discovery to production typically exceeding ten years due to environmental reviews, indigenous consultation, water management, and multi-agency approvals. ESG requirements add further cost and delay, embedding a structural lag between demand growth and supply response that price signals alone cannot resolve.

Infrastructure Access and Near-Term Cash Flow Define Explorer Differentiation

For explorers operating in this environment, the strategic value of new discoveries is not solely a function of grade or tonnage. Infrastructure proximity, jurisdictional stability, and the potential for low-cost early production can materially differentiate a project’s investment case.

Merlin Marr-Johnson, Chief Executive Officer of Fitzroy Minerals Inc., describes the positioning of the company’s Buen Retiro flagship asset in Chile:

“Buen Retiro is at low elevation, with superb surrounding infrastructure, making it an ideal project location. That operation gives us the potential for near-term, non-operated cash flow, which we believe will distinguish us from many other explorers in the market.”

Chile’s combination of established mining infrastructure, access to processing capacity, and regulatory frameworks that are familiar to institutional capital represents a meaningful advantage for early-stage projects seeking to reduce development risk. The ability to generate near-term cash flow from non-operated production, as Fitzroy is pursuing, provides a form of financial optionality that is uncommon at the exploration stage and reduces the equity dilution dependency that characterizes most exploration-stage companies.

Resource Scale & Economic Quality in a Capital-Constrained Funding Environment

Institutional capital allocation to copper equities is becoming more selective, with investors prioritizing assets that combine resource quality, development certainty, and balance sheet strength amid price volatility and rising capital costs. High-grade polymetallic systems attract disproportionate interest due to by-product credits that enhance NPV and IRR, while scalable resources with consistent grade support the production longevity required to justify large-scale capital investment.

Jonathon Deluce, Chief Executive Officer of Abitibi Metals Corp., describes the B26 project’s resource trajectory in Quebec, Canada:

"So since optioning the project, we’re up over 125% in terms of tonnage growth, looking at the 13 million tons indicated at 2.1% copper equivalent, 12.3 million tons inferred at 2.2%. I think we’ve grown it from our last update, 18.5 to 25.3, maintaining the grade."

A 124% increase in total resource to approximately 25.3 million tonnes, maintained at 2.1 to 2.2% copper equivalent (CuEq) grade, while securing 80% ownership of the project represents a combination of scale expansion and economic quality that is rare at the advanced exploration stage. The ability to maintain grade while growing tonnage is the critical validation point for what Deluce describes as a potential 30 to 50 million tonne system.

Capital Markets Dynamics & Liquidity as a Differentiating Factor

Mining equity capital markets are operating in a bifurcated mode. Macro-driven inflows into the base metals complex have increased aggregate sector visibility, but capital allocation within the sector is increasingly concentrated in assets with demonstrated project economics, lower execution risk, and institutional-grade disclosures. Exploration-stage companies remain dependent on equity issuance cycles and market sentiment, both of which can deteriorate rapidly under geopolitical or macroeconomic stress.

Marimaca Copper Corp.’s C$409 million capital raise reflects the degree to which institutional participation is available to copper developers when project economics, permitting status, and development readiness are clearly established. The company has received its environmental approval, a milestone that removes one of the primary sources of development-stage binary risk.

Liquidity differentiates outcomes not only in absolute terms but in the timing of project advancement. Companies that can sustain drilling programs, advance feasibility work, and maintain institutional engagement through volatile macro periods are structurally advantaged relative to peers that must pause activity during capital markets dislocations.

The Investment Thesis for Copper

- Near-term price volatility created by macro-driven sentiment shifts and positioning unwinds provides entry points that are structurally disconnected from long-horizon supply-demand fundamentals, offering risk-adjusted opportunities for investors with defined time horizons.

- Structural demand anchored in electrification policy and AI infrastructure capital expenditure creates a durable, non-cyclical consumption base that reduces the demand-side uncertainty that has historically complicated copper equity valuation.

- Supply inelasticity driven by declining ore grades, permitting timelines exceeding a decade, and capital costs that have risen 65% since 2020 establishes a ceiling on supply response that is not addressable through price incentives alone within relevant investment timeframes.

- Oxide deposit developers such as Marimaca Copper Corp. offer lower capital intensity exposure through heap leaching and SX-EW processing, with environmental approvals secured and a construction readiness timeline targeting 2026, positioning the asset within the near-term supply response window.

- Early-stage explorers with infrastructure-adjacent assets in established mining jurisdictions, as demonstrated by Fitzroy Minerals in Chile, provide discovery leverage with a potential path to near-term non-operated cash flow that differentiates the company’s risk profile from conventional exploration-stage peers.

- Advanced exploration assets with demonstrated resource growth at maintained grade, such as the B26 project advanced by Abitibi Metals Corp. in Quebec, offer scale optionality and high-grade polymetallic economics that support project-level NPV and IRR outcomes under a range of copper price assumptions.

- Jurisdiction selection, with Chile and Quebec providing regulatory transparency, infrastructure access, and institutional capital familiarity, reduces permitting and execution risk in a supply environment where project development delays are already structurally embedded.

The copper market’s near-term surplus and the structural supply constraints that define its long-horizon outlook are not contradictory conditions. They operate on different timescales and carry different implications for investor strategy. The surplus of 2025 and 2026 reflects demand timing and elevated scrap response at higher prices; it does not revise the IEA’s projection of a 30% supply deficit by 2035 or alter the permitting and grade realities that limit supply elasticity.

Copper remains one of the most significant industrial metals in the global energy transition. The investment case for selective copper equity exposure is grounded in supply physics, capital market realities, and the policy-anchored demand architecture that continues to take shape across electrification and digital infrastructure globally.

TL;DR

Copper is in a near-term surplus through 2026, with Goldman Sachs forecasting prices range-bound between $10,000 and $11,000 per tonne. This surplus is cyclical, not structural. Ore grades have declined 40% since 1991, permitting timelines exceeding a decade, capital costs have risen 65% since 2020, and the IEA projects a 30% supply deficit by 2035. Demand from grid electrification, electric vehicles, and AI infrastructure is policy-anchored and non-cyclical, meaning it does not pause with economic slowdowns. The current price environment creates entry points for investors who can distinguish short-term volatility from long-duration supply scarcity, with differentiated exposure available across oxide developers, high-grade resource growers, and infrastructure-adjacent explorers in established mining jurisdictions.

FAQs (AI generated)

This is consistently the most common point of confusion across Crux's copper coverage. Readers who encounter both the Goldman Sachs surplus figures and the IEA's 2035 deficit projection in the same article naturally ask how both can be true. The answer lies in the distinction between cyclical timing factors , demand normalization in China, elevated scrap response, inventory accumulation , and the structural supply-side realities of grade decline, permitting timelines, and capital cost inflation.

Multiple Crux articles reference development timelines as a core constraint, with figures ranging from 16 to 17 years on average today, compared to roughly seven years in the 1970s. Readers consistently want this quantified and explained, particularly in the context of why elevated prices cannot simply incentivize new supply quickly enough to close the projected deficit.

AI data centers appear across nearly every Crux copper article as a demand driver, and readers want a concrete number behind the claim. The IEA and related research cited across Crux's coverage estimate AI data centers alone could consume 250,000 to 550,000 tonnes annually by 2030, representing one to two percent of global demand , a figure that grounds the thesis beyond general references to electrification.

Chile and Quebec appear repeatedly across Crux's coverage as preferred destinations for institutional capital, and readers want to understand why one jurisdiction commands a valuation premium over another. The answer covers permitting predictability, infrastructure access, political stability, and the concentration risk that comes with China controlling approximately 45% of global copper refining capacity.

This is a technical distinction that Crux's coverage returns to repeatedly in the context of Marimaca Copper and heap leaching economics. Readers with limited mining backgrounds ask why oxide projects are described as lower risk and faster to develop, and what SX-EW processing means in practical investment terms , specifically, lower capital expenditure, shorter construction timelines, and faster payback relative to conventional sulphide concentrator-and-smelter routes.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed