The Commitment to Triple Nuclear Capacity by 2050

Uranium market faces supply deficit as 31 nations commit to triple nuclear capacity by 2050, creating opportunities for producers with advanced projects.

- The global uranium market faces a structural supply-demand imbalance with utilities needing to secure 2.1 billion pounds by 2040, while current production remains insufficient to meet growing demand.

- Nuclear power has gained significant policy support worldwide, with 31 countries now committed to tripling nuclear capacity by 2050, driving long-term demand growth for uranium.

- Uranium companies are advancing projects across various jurisdictions, with firms already restarting production while others at different development stages.

- Term contract prices have steadily increased to approximately $80/lb despite spot price volatility, creating favorable conditions for developers to secure offtake agreements and project financing.

- Queensland currently maintains a moratorium on uranium mining, but companies has strategically invested in the area's uranium project potential in anticipation of policy changes that would unlock its value.

The global uranium market is experiencing a fundamental structural shift characterized by growing demand and constrained supply. As nations worldwide pursue clean energy transitions and energy security, nuclear power has reemerged as a critical component of the global energy mix, creating what industry participants describe as an unprecedented opportunity for uranium investors.

"We have never been at a moment in time with this big of an uncovered requirements gap in front of us. Utilities today between now and 2040 have to buy 2.1 billion pounds of uranium in order to meet their run-rate requirements. This is just the requirements of the reactors being saved, the reactors being extended, and the new reactors that are being built." - Grant Isaac, CFO of Cameco (February 2025)[1,2]

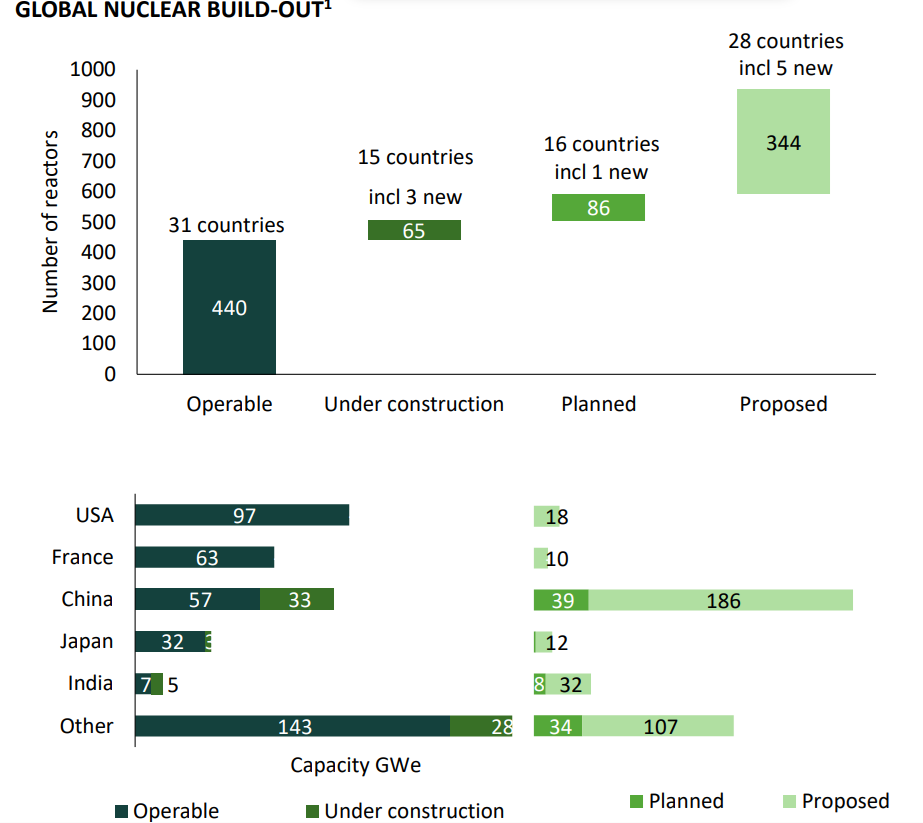

This renewed focus on nuclear energy is backed by significant policy commitments. At the UN's COP28 climate conference in December 2023, 22 countries signed a pledge to triple global nuclear energy capacity by 2050 to meet emissions targets. By COP29, this had grown to 31 countries making the same commitment to triple nuclear, demonstrating growing international acceptance of nuclear's role in decarbonization.

Uranium Market Fundamentals: Supply-Demand Imbalance

Growing Demand from Existing and New Nuclear Plants

Globally, there are approximately 440 operable nuclear reactors, with 65 under construction and an additional 430 planned or proposed. China is particularly aggressive in its nuclear expansion, with 33GWe under construction to complement its current 57GWe, and plans for an additional 200GWe. This resembles China's steel expansion in the early 2000s that drove the global iron ore demand boom.

The United States maintains the world's largest nuclear fleet with 97GWe of capacity and has announced plans to triple nuclear capacity by 2050, adding approximately 200GW with 35GW targeted by 2035. Additionally, many U.S. plants are receiving life extensions, while some decommissioned capacity is being recommissioned to supply clean baseload power for data centers.

Government Support and Regulatory Environment

Government policies increasingly favor nuclear energy development, with implications for uranium project permitting and development timelines.

- In the United States, federal mandates aim to streamline permitting processes for energy projects, including uranium mines. The U.S. Department of Energy has awarded research grants for projects like Laramide's Churchrock to advance groundwater restoration technology, recognizing the importance of domestic uranium production.

- Australia's regulatory landscape for uranium mining varies by state, with companies awaiting potential policy changes that could facilitate development of known resources. Boss Energy and Laramide is waiting for uranium policy clarification under the new LNP Government in Queensland for its Westmoreland project.

- In African nations like Malawi, specific mining agreements provide fiscal stability. Lotus Resources has secured a Mine Development Agreement (MDA) that guarantees 10 years of fiscal stability in Malawi providing investors with greater certainty regarding the tax and royalty regime.

Pricing Dynamics: Term Contracts and Spot Market

The uranium market operates with two distinct pricing mechanisms: spot prices (for immediate delivery) and term contract prices (for long-term supply arrangements). While spot prices receive more attention from equity investors and have been volatile, the term price has steadily increased to approximately $80/lb, providing a more stable indicator of market health.

Bannerman Energy acknowledges the disconnect between spot prices, term contract prices, and share price performance with spot prices declining from highs of $107 to the low $60s in early 2024. but remains focusedon patient execution of their strategy. Matt Horgan, VP Business Development& IR, emphasised their funding approach:

"Bannerman has had strong market support for its very disciplined approach to capital allocation, and one of the worst things we could do at the moment is pull the trigger preemptively on a highly dilutive equity raise."

Gavin Chamberlin, CEO, & Matt Horgan, VP Corporate Development for Bannerman Energy

This pricing environment has created favorable conditions for developers to secure offtake agreements with utilities. Several companies announced such arrangements, including Peninsula Energy with contracts covering about 40% of planned production over the next ten years, and Lotus Resources with multiple fixed-price agreements covering significant portions of future production.

Financing and Development Strategies

Various approaches to financing uranium project development, reflecting different stages and capital requirements.

Peninsula Energy has secured approximately US$132.8 million in funding through cash reserves, equipment facilities, and working capital arrangements. This funding covers both initial restart capital (US$50 million) and subsequent plant expansion costs.

Lotus Resources is advancing the Kayelekera project with a fully funded strategy that includes capital for offtake and processing negotiations. The company has also secured multiple offtake agreements, including with major utilities.

Companies are pursuing staged development approaches to manage capital requirements. Laramide's Churchrock PEA outlines a staged production approach that reduces initial capital needs while maintaining flexibility to increase production rates later. Similarly, Peninsula Energy is implementing a two-phase expansion at Lance, with initial production using existing satellite facilities before expanding to full yellowcake production capabilities.

Key Uranium Development Projects and Companies

United States: Focus on ISR and Conventional Assets

The U.S. uranium sector is experiencing renewed interest driven by energy security concerns and supportive federal policies. In February 2025, U.S. Energy Secretary Chris Wright issued a memorandum outlining plans for a "Golden Era of American Energy Dominance," specifically calling for unleashing commercial nuclear power.

Peninsula Energy

Peninsula Energy is positioned as North America's newest uranium producer with its Lance Projects in Wyoming. The company successfully restarted uranium production in December 2024 using low-pH in-situ recovery (ISR) methods. With a total resource of 58 million pounds and expansion potential, Peninsula targets production capacity of 2 million pounds annually after completing its Phase II plant expansion in early 2025.

Laramide Resources

Laramide Resources holds multiple U.S. assets including the Churchrock-Crownpoint project in New Mexico's Grants Mineral Belt, with 50.8 million pounds of inferred resources amenable to ISR mining. A January 2024 Preliminary Economic Assessment demonstrated potential for a long-life operation producing 31.2 million pounds over 31 years, with low initial capital costs of $47.5 million and unit operating costs of $26.70/lb.

The company is working with the Department of Energy and Los Alamos National Laboratory on groundwater restoration technology to support final permitting, highlighting the U.S. government's recognition of the significance of this project to advance domestic ISR uranium production.

Australia Positioning for Policy Changes

Australia holds approximately 28% of the world's identified uranium resources but has historically maintained restrictive mining policies in some states. Companies with Australian assets are positioning themselves for potential policy shifts.

Boss Energy (with Laramide Resources)

Boss Energy acquired Laramide Resources shares for the Westmoreland project in Queensland holding 48.1 million pounds of indicated and 17.7 million pounds of inferred resources. The company recently updated its mineral resource estimate, increasing indicated resources by 34% and inferred resources by 11% compared to previous estimates.

Queensland maintains a moratorium on uranium mining, but Boss considers its investment in the Westmoreland project prudent given the asset's potential value should the ban eventually be overturned. Managing Director Duncan Craib stated in the March 13th announcement,

“This investment represents an attractive opportunity to secure exposure to the significant exploration and development upside at Westmoreland for a relatively small cost. While Queensland currently has a moratorium on uranium mining, we believe the state will enviably lift this. If the moratorium is overturned, Boss’ can apply its knowledge, experience and financial strength to the Westmoreland project."

While waiting for uranium policy clarification under Queensland's government, Laramide is advancing a Mineral Development License application. A 2016 Preliminary Economic Assessment for Westmoreland demonstrated potential for a conventional open-pit operation with operating costs of US$23.26 per pound and a post-tax IRR of 35.8% at a uranium price of $65/lb. The company believes the project has significant exploration upside and expansion potential.

Africa and Central Asia: Established Production Regions

Africa and Central Asia represent established uranium producing regions with significant development potential.

Bannerman Energy

Bannerman Energy is advancing its large-scale Etango project in Namibia. Despite the current market challenges, CEO Gavin Chamberlain remains confident in the long-term uranium demand outlook. The company has made significant progress on its Etango project over the past year, completing critical infrastructure components including the access road and water facilities. Bannerman's patient approach, strong balance sheet, and strategic partnerships position the company to ride out near-term volatility while advancing a world-class asset in astable jurisdiction.

Global Atomic

Global Atomic's Dasa Uranium Project in Niger, the highest-grade uranium deposit in Africa and the only permitted greenfield uranium project currently under development globally. The high-grade Dasa deposit is on track for first production in 2026, with the mine now accessed via a completed ramp and plant construction well underway. Global Atomic has signed uranium off-take agreements with major utilities and is pursuing project financing.

Global Atomic also highlighted the significant economic benefits Dasa will provide to the local community through employment, training, and support of regional initiatives. The company's zinc recycling joint venture in Turkey is also expected to return to profitability starting Q4 2024.

Lotus Resources

Lotus Resources is advancing the Kayelekera project in Malawi, a past-producing mine that operated from 2009-2014 and produced approximately 11 million pounds of uranium. The company has completed detailed engineering and secured funding for a restart, targeting first production in Q3 2025. With average annual production of 2.4 million pounds and a mine life of 10 years, Kayelekera represents one of the more advanced restart projects globally.

Several companies have established positions in Kazakhstan, the world's largest uranium producer accounting for approximately 40% of global supply. Laramide Resources has secured prospective claims in the Chu-Sarysu basin, which hosts 60% of Kazakhstan's uranium production. The company has acquired historical exploration data that has identified numerous uranium roll-front targets amenable to ISR mining, with plans for drilling in the latter half of 2025.

The Investment Thesis for Uranium

- Supply-Demand Imbalance: Current global uranium production (~140Mlbs annually) is insufficient to meet expected demand growth from 31 countries committed to tripling nuclear capacity by 2050, creating a structural supply deficit that could persist for years.

- Limited New Production: Few new uranium mines have reached final investment decisions in the past decade, while development timelines typically span 5-10+ years, limiting how quickly supply can respond to higher prices.

- Production Cost Support: Industry cost curves suggest prices above $60-65/lb are required to incentivize sufficient new production, providing a potential floor for medium-term uranium prices.

- Utility Contracting Cycle: Utilities are entering a major recontracting cycle with ~2.1 billion pounds of uncovered requirements through 2040, supporting term contract prices and providing revenue visibility for producers.

- Asset Selectivity: Focus on companies with assets in stable jurisdictions, low technical risk profiles, clear paths to production, and management teams with proven operational experience.

- Diversification Strategies: Consider exposure across the spectrum from near-term producers to development-stage companies to balance immediate production exposure with longer-term growth potential.

- Financing Progress: Monitor project financing milestones and offtake agreements as key de-risking events that typically trigger revaluations of development companies.

- Processing Constraints: Beyond mining, limited uranium conversion and enrichment capacity creates additional supply chain bottlenecks that may support higher prices throughout the fuel cycle.

- Government Support: Increasing policy support for nuclear energy in major economies (US, China, France, UK) creates a more favorable environment for project approvals and potential subsidies.

- ESG Considerations: Nuclear power's low carbon footprint has improved its environmental perception, while uranium companies increasingly emphasize responsible mining practices and stakeholder engagement.

The uranium market presents a compelling opportunity driven by a convergence of factors: growing nuclear power development, persistent supply constraints, and improving sentiment toward nuclear energy as a clean energy solution. The fundamental supply-demand imbalance appears set to continue for years, as new mine development simply cannot keep pace with projected demand growth.

Investors have multiple avenues to participate in this sector, from near-term producers to companies with development-stage assets. Each presents different risk-reward profiles based on jurisdiction, development stage, and mining method. The sector's improved fundamentals are reflected in steadily rising term contract prices and increasing offtake activity, providing tangible validation of the market's strength.

References:

- Cameco’s CFO Tells U.S. Mining Conference The Uranium Industry’s Future is Bright (Discover Estevan's Keira Miller, Saskatoon Media Group, March 2025).

- Laramide Resources' March 2025 Corporate Presentation

- Lotus Resources' March 2025 Company Presentation

Analyst's Notes

Subscribe to Our Channel

Stay Informed