Troilus Targets 2027 Construction as $1.2B Financing and Offtake Deals Advance Toward Close

.jpg)

TLG: $1.2B debt mandate upsized; gold $4,585 vs $1,975/oz FS base. West Rim high-grade adds resource upside. Construction decision H2 2026.

- Troilus increased its project debt facility by 20% to US$1.2 billion, led by Societe Generale, KfW IPEX-Bank, and EDC, with ECA approval targeted mid-2026 and financial close in Q4 2026 - covering an estimated 55–65% of initial capital requirements.

- May 2026 gold at ~$4,585/oz (+132%), copper at ~$6.20/lb (+53%), and silver at ~$78/oz (+240%) versus the May 2024 Feasibility Study assumptions of $1,975/oz, $4.05/lb, and $23/oz - implying substantial upside to the published after-tax NPV5% of US$885M and 14% IRR.

- West Rim Zone Phase 1 drilling returned 6.93 g/t AuEq over 18.5m - including 53.90 g/t AuEq over 2m starting at 11.5m depth - within 200m of the FS reserve pit boundary, supporting an emerging near-mine resource addition.

- Connector Zone confirms inferred-to-indicated conversion potential: Completed program returned intercepts up to 1.15 g/t AuEq over 37m and 0.78 g/t AuEq over 54m within the current mine plan; converting inferred material within pit boundaries to indicated status could reduce early-year strip ratios and improve mill feed.

- Hydro-Québec has allocated 70 MW of hydroelectric power; the Environmental and Social Impact Assessment was filed with federal and provincial authorities in June 2025; indicative offtake agreements are in place with Aurubis (Germany) and Boliden (Sweden); construction start targeted 2027, first production 2029/2030.

The global mining industry is entering a period of structural supply tightness in both gold and copper. Gold has benefited from elevated sovereign demand, dollar-hedging dynamics, and geopolitical uncertainty, with spot prices approximately at $4,100 per ounce in June 2026. Copper, underpinned by energy transition demand and constrained greenfield development pipelines, has similarly re-rated to approximately $6.20 per pound. Within this context, large-scale, near-permitted copper-gold development assets in stable jurisdictions have attracted disproportionate capital market attention from majors and sovereign wealth-backed entities alike. Troilus Mining Corp.'s namesake project in north-central Québec sits directly at this intersection.

Asset overview: scale, jurisdiction, and brownfield advantage

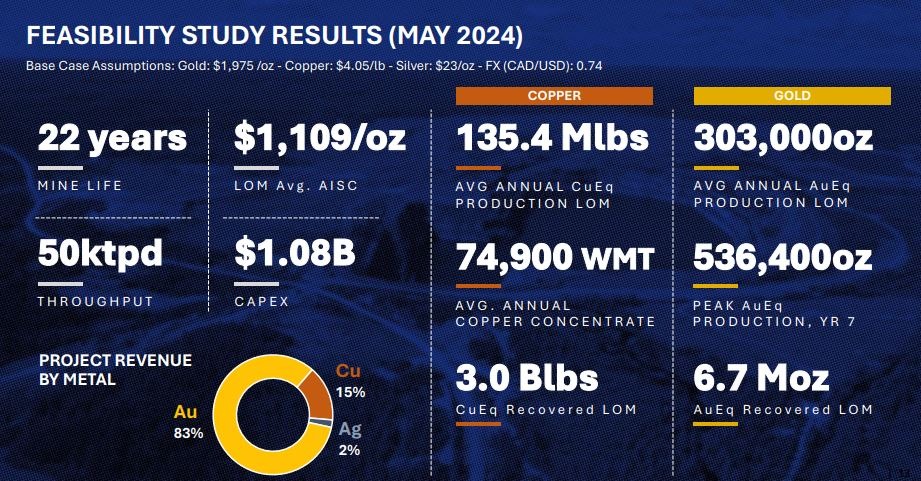

The Troilus Project encompasses a 435 km² land position in the Frôtet-Evans Greenstone Belt, approximately 170 kilometers north of Chibougamau, Québec. The property hosts an Indicated Mineral Resource of 11.21 million ounces AuEq across 508.3 million tonnes (0.69 g/t AuEq), with an additional Inferred Resource of 1.80 million ounces AuEq. Probable Mineral Reserves stand at 7.26 million ounces AuEq across 380 million tonnes at 0.59 g/t AuEq, underpinning a 22-year mine life at 50,000 tonnes per day.

A critical differentiator from greenfield peers is the project's brownfield status. The site operated as an open-pit mine from 1996 to 2010 under Inmet Mining Corp., producing over two million ounces of gold and approximately 70,000 tonnes of copper. Legacy infrastructure - including a 50 MW substation, water treatment facilities, a permitted tailings facility, over 100 kilometers of powerline, truck-ready roads, and a starter construction camp - carries an estimated replacement value exceeding US$500 million and materially reduces both capital requirements and permitting complexity.

Feasibility study economics and commodity price leverage

The May 2024 Feasibility Study established base case economics at gold of US$1,975/oz, copper of US$4.05/lb, and silver of US$23/oz. Under these assumptions, the project delivered an after-tax NPV5% of US$885 million and a 14% IRR, with a payback period of 5.7 years and initial capital expenditure of approximately US$1.074 billion. On a capital intensity basis, the project's all-in CAPEX per AuEq ounce of approximately US$216 compares favorably to a peer average of approximately US$310 per ounce among comparable Canadian development-stage assets, as compiled by Desjardins Securities.

Prevailing May 2026 spot prices are substantially above the FS base case across all three payable metals. Gold at approximately $4,585/oz (+132%), copper at approximately $6.20/lb (+53%), and silver at approximately $78/oz (+240%) mean the published project economics represent a material floor rather than a current estimate. While the company has not published a revised sensitivity analysis at spot prices, the magnitude of the commodity price deviation implies significant potential expansion of NPV and project cash flow, particularly given the project's 22-year, high-operating-leverage production profile.

Financing architecture: US$1.2B mandate and path to financial close

The most consequential recent development is the May 2026 upsize of the project debt mandate from US$1.0 billion to US$1.2 billion. The financing syndicate - led by Societe Generale, KfW IPEX-Bank, and Export Development Canada - is supported by export credit agencies including EIFO (Denmark), Euler Hermes (Germany), Finnvera (Finland), and EKN (Sweden). ECA participation provides structurally lower borrowing costs compared to purely commercial project finance and reflects the geographic distribution of Troilus's equipment supply chain and offtake relationships.

The target capital structure allocates 55–65% to senior debt, 25–35% to subordinated debt or royalty/streaming instruments, and approximately 10% to equity. With initial CAPEX of approximately US$1.074 billion and a US$1.2 billion senior debt mandate, the structure implies meaningful coverage of construction costs, subject to final credit approvals and definitive documentation expected in Q4 2026. The company held approximately C$153 million in cash and marketable securities as of the quarter ending January 2026, with an additional US$35 million loan facility through Auramet International, providing pre-construction liquidity.

Engineering, permitting, and construction timeline

Basic engineering was completed in 2025, narrowing the capital cost estimate accuracy from +/−35% (at Feasibility Study) to +/−10%. Detailed engineering is underway, led by BBA (engineering and procurement) alongside EBC (construction management). Troilus filed its Environmental and Social Impact Assessment with both the federal Impact Assessment Agency of Canada (IAAC) and the provincial MELCCFP in June 2025; provincial and federal permitting decisions are anticipated in late 2026 to early 2027.

The project carries a relatively low environmental risk profile. The processing design is cyanide-free, acid rock drainage has been confirmed as not material through extensive post-closure monitoring data, and the brownfield status reduces environmental uncertainty relative to greenfield peers. Construction is targeted to commence in 2027, with commissioning and first production expected in 2029/2030.

2026 exploration: West Rim and Connector Zone

Two active 2026 drill programs are generating incremental resource optionality outside the current mine plan. At the West Rim Zone - a discovery made in 2024 immediately west of the North Reserve Pit - Phase 1 drilling has returned some of the strongest near-surface intercepts encountered at Troilus. Hole WR-26-013 returned 6.93 g/t AuEq over 18.5 metres, including 53.90 g/t AuEq over 2 metres at just 11.5 metres depth; hole WR-26-016 (May 2026) returned 2.92 g/t AuEq over 19 metres. The zone lies entirely outside the current mineral resource estimate, within approximately 200 metres of the FS reserve pit boundary, and remains open along strike and at depth across an interpreted 5-kilometre prospective trend. A Phase 2 program is being planned.

In the Connector Zone - positioned between the formerly mined Z87 and J open pits - the completed 2026 program returned consistent mineralization with intercepts including 1.15 g/t AuEq over 37 metres and 0.78 g/t AuEq over 54 metres. The program targeted inferred material within the existing reserve pit boundary. Because only measured and indicated resources qualify for reserve conversion under NI 43-101, inferred material within the pit design is presently treated as waste. Successful conversion of this material to indicated could reduce the effective early-year strip ratio and improve mill feed grades - with positive implications for early-life cash flow generation.

Offtake, power, and strategic alignment

Troilus has established indicative offtake arrangements with Aurubis (Germany's largest copper producer, MoA signed August 2025) and Boliden (Sweden, MoU signed March 2026) for the long-term sale of copper-gold concentrate. Negotiations with a domestic Canadian refiner are underway. Critically, 70 MW of hydroelectric power has been allocated by Hydro-Québec - sufficient for both project development and full operations - enabling a low-cost, low-carbon emissions profile that aligns with provincial and federal critical minerals policy. The company has been included in Canadian government-led critical minerals missions to Germany, Japan, and Korea (August 2025), indicating a level of strategic endorsement from senior government at the federal level.

Conclusion

Troilus Mining enters H2 2026 with a structurally de-risked project relative to twelve months prior. Engineering risk has declined materially with basic engineering complete and capital estimates tightened to +/−10%. Power is secured. Offtake with two major European smelters is in place. The US$1.2 billion debt mandate is in active due diligence with completion expected by year-end. The remaining gating items - ECA approval, financial close, and a final construction decision - are targeted for the second half of 2026, with construction in 2027 and first production in 2029/2030. Against a commodity price backdrop that substantially exceeds the FS base case, and with near-pit exploration beginning to define potential resource additions at West Rim, the project's long-term value proposition for institutionally-oriented shareholders is being incrementally strengthened at each milestone. The primary risk remains the execution of a complex, multi-party project financing structure in a capital market environment that can shift materially on short notice.

Executive Summary (TL;DR)

Troilus Mining Corp. is advancing a 22-year, 50,000 tonne-per-day open-pit copper-gold project in Québec toward a construction decision in H2 2026, supported by a US$1.2 billion debt mandate anchored by Societe Generale, KfW IPEX-Bank, and Export Development Canada, alongside indicative offtake arrangements with Aurubis and Boliden and secured low-cost hydroelectric power. The project's May 2024 Feasibility Study established an after-tax NPV5% of US$885 million and a 14% IRR at gold of $1,975/oz and copper of $4.05/lb; prevailing May 2026 spot prices of approximately $4,585/oz gold and $6.20/lb copper represent substantial implied uplift to those published economics. Concurrent 2026 exploration is delivering high-grade intercepts at the West Rim Zone - a discovery entirely outside the current resource estimate - and supporting potential inferred-to-indicated conversion in the Connector Zone, providing additive optionality beyond the base mine plan. The primary near-term catalyst is completion of the comprehensive project financing package, with ECA approval expected mid-2026 and financial close targeted Q4 2026.

FAQs (AI Generated)

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

Stay Informed