Undervalued? Fully Permitted, Feasibility-Backed, and Potentially Mispriced: The Case for U.S. Gold Corp's CK Gold Project

Fully permitted Wyoming gold-copper project, feasibility-backed NPV of $630M, tight 16.5M share count — investors eye a valuation disconnect.

- U.S. Gold Corp's CK Gold Project in Wyoming is fully permitted and feasibility study-backed, making it one of the few genuinely construction-ready gold-copper assets among North American junior developers.

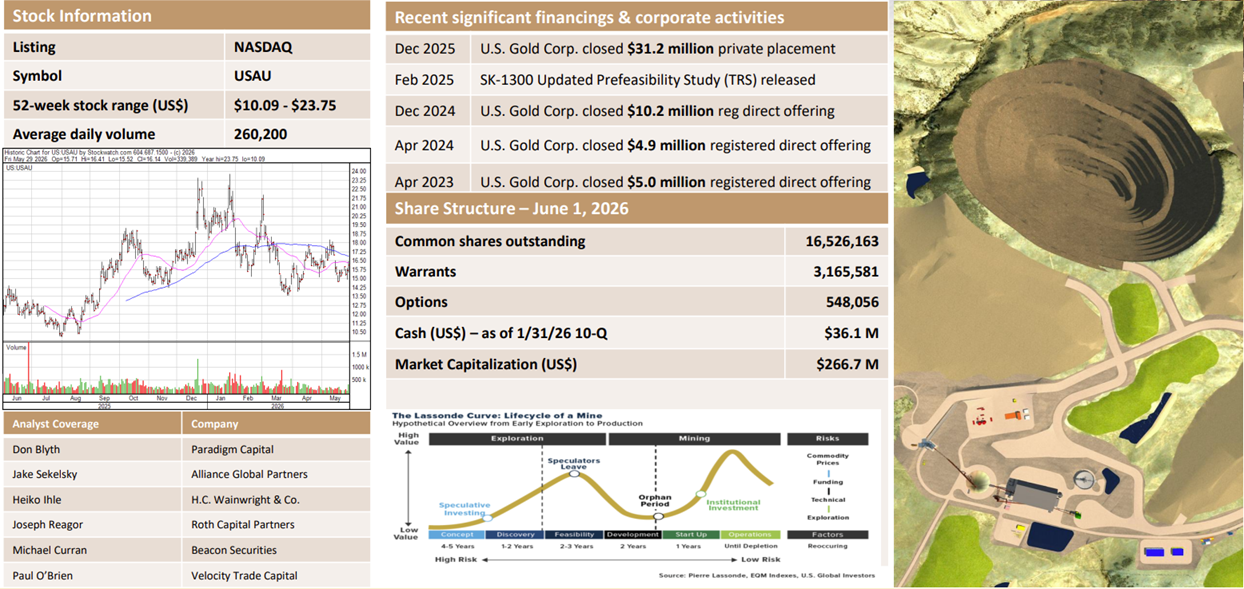

- The company's share count of approximately 16.5 million is unusually low for a junior developer, and Executive Chairman Luke Norman argues this has left the roughly $260 million market capitalisation disconnected from the project's calculated value.

- The definitive feasibility study uses a conservative base-case gold price of $3,250 per ounce, below prevailing consensus estimates near $3,800 and still delivers an after-tax NPV of approximately $630 million with an IRR near 30%.

- Additional value not yet reflected in the feasibility study includes mineralisation beyond the current reserve boundary, unrecovered gold in tailings, and commercially saleable waste rock.

- Project financing is expected to be resolved within a few months with management favouring debt over equity to protect the company's tight share structure from further dilution.

U.S. Gold Corp (NASDAQ:USAU) has positioned itself as an outlier among North American junior developers by advancing a fully permitted, construction-ready gold-copper project at a time when few comparable assets exist in the pipeline. In a discussion with Luke Norman, Executive Chairman and co-founder of the company, the case for the CK Gold Project outside Cheyenne, Wyoming, was laid out across permitting status, project economics, infrastructure, and financing strategy providing investors with a clearer picture of how the company's current valuation compares with the underlying asset.

A Permitted, Infrastructure-Rich Location

The CK Gold Project sits roughly 20 miles from Cheyenne, Wyoming, close to the Colorado border, and benefits from established road, rail and power infrastructure. Norman described the site as one of very few hard-rock mining developments to be fully permitted in Wyoming in close to a century, with the project's proximity to the i-80 corridor connecting it to established mining service hubs including Reno, Elko and Salt Lake City. This infrastructure positioning is presented as a meaningful cost and timeline advantage relative to more remote developments.

Norman also highlighted the state-level permitting structure in Wyoming as a distinguishing factor. Once state permits are issued, the formal objection period has passed, reducing the risk of the project being challenged mid-construction which is a risk he contrasted with permitting processes on federal ground or in Canada, where objections can arise later in the development timeline.

Capital Structure and Valuation

A central theme of the discussion was the company's share structure. With approximately 16.5 million shares outstanding, a notably low count for a junior developer, Norman argued that the company's roughly $23 per share 52-week high and current trading levels translate to a market capitalisation of around $260 million, which he contends undervalues the project relative to its feasibility study outputs. He attributed part of this disconnect to the company's Nasdaq listing, suggesting a pricing gap exists relative to how similar projects might be valued on Canadian exchanges.

Why the Market May Be Mispricing U.S. Gold Corp

The potential gap between U.S. Gold Corp's current market valuation and the value is implied by its own feasibility study. The most straightforward is share price perception: at a trading price in the mid-teens to low-$20s per share, retail investors accustomed to junior mining stocks trading at cents or low dollars may assume the company is fully priced, without accounting for the unusually small share count behind that price. Norman's argument is that the resulting market capitalisation of roughly $260 million looks materially low set against a feasibility study NPV of approximately $630 million even before accounting for upside not yet captured in that study.

That upside includes mineralisation identified in drilling beyond the current reserve boundary, unrecovered gold sitting in tailings material, and waste rock with a commercial resale value comparable to material sold by a neighbouring quarry operator, none of which is currently reflected in the project's economics. Commodity price assumptions add a further layer: the feasibility study's gold base case sits below consensus estimate and noted that copper, which makes up around 30% of the project's economics, was modelled using a copper price that has since been exceeded by the market:

"We ran $3,250/oz is our base case which is significantly below consensus. I think right now consensus is pushing up around $3,800 an ounce. At $3,250 you see an after-tax NPV of $630 million just under 30% IRR. Well, we start pushing up towards spot price in gold and you can see tremendous shift."

Listing venue is another factor Norman pointed to directly, suggesting that Nasdaq-listed mining developers may be priced differently by the market than comparable projects on Canadian exchanges such as the TSXV, where specialist mining investors are more concentrated. Finally, the company's stated preference for debt-heavy project financing is presented as a structural distinction from many junior developers, whose valuations are often discounted by investors pricing in anticipated dilution. Taken together, these are the specific mechanisms management cites for the disconnect between share price and underlying project value, though each depends on execution of successful financing, continued permitting stability, and commodity prices holding near or above current levels rather than being guaranteed outcomes.

Management Track Record

Norman pointed to the operational experience of the leadership team as a factor supporting execution confidence. CEO George Bee previously worked at Barrick Gold, including on the Goldstrike/Betze-Post project, while lead independent director Joanna Fipke brings securities law experience within the Canadian mining sector. Norman characterised the team as experienced in building and operating mines for public companies.

Interview with Luke Norman, Executive Chairman of US Gold Corp.

Engineering and Additional Upside

The feasibility study was developed by two engineering firms, Ausenco and Allied, with subsequent third-party review supporting the capital cost estimates. Norman identified the incorporation of Jameson Cell Flotation technology as a key engineering optimisation. Beyond the current reserve, Norman noted that approximately 80% of drill holes extending past the reserve boundary showed continued mineralisation, and pointed to additional potential in gold currently locked within tailings material, as well as commercial value in the waste rock comparable in grade to material sold by neighbouring quarry operator that has not been incorporated into current project economics.

The Investment Thesis for U.S. Gold Corp

- Scarcity value: CK Gold is one of a limited number of fully permitted, feasibility-backed gold-copper development projects available to investors in North America, reducing permitting-related timeline and regulatory risk relative to peers still navigating federal or provincial approval processes.

- Tight share structure: With approximately 16.5 million shares outstanding, the company has materially less dilution risk than many junior developers, though investors should monitor how financing decisions affect this structure going forward.

- Feasibility study economics: A base-case after-tax NPV of approximately $630 million and an IRR near 30%, calculated using a gold price below current consensus, suggests potential upside if commodity prices remain elevated though these are project-level estimates, not guarantees of realised value.

- Infrastructure advantage: Proximity to power, rail, road and skilled labour reduces anticipated capital and operating costs relative to remote-jurisdiction developments.

- Exploration upside: Mineralisation extending beyond the current reserve, alongside unrecovered gold in tailings and saleable waste rock, represents optionality not yet reflected in the feasibility study.

- Financing catalyst: Resolution of project financing which is expected within a few months represents a near-term catalyst that could materially affect share price and de-risk the development pathway.

- Considerations for investors: As with any development-stage mining company, actual construction costs, financing terms, commodity price movements and permitting outcomes may differ from current projections. Investors should review the company's public filings and feasibility study documentation directly before making investment decisions.

TL;DR

U.S. Gold Corp's CK Gold Project in Wyoming is fully permitted and backed by a definitive feasibility study showing an after-tax NPV of approximately $630 million and an IRR near 30%, calculated using a gold price below current consensus. With only around 16.5 million shares outstanding, the company's roughly $260 million market capitalisation looks low relative to those study economics, according to Executive Chairman Luke Norman. Additional upsides including mineralisation beyond the current reserve, tailings gold, and saleable waste rock aren't yet reflected in the numbers. Project financing, expected within a few months, is the key near-term catalyst, with management favouring debt over equity to limit dilution.

Macro Thematic Analysis

The case for U.S. Gold Corp's CK Gold Project sits within a broader macro backdrop favouring North American, permitted gold-copper development assets. Gold has maintained a sustained bull run in recent years, with prices moving well above the $3,250/oz base case used in the company's feasibility study, while copper has strengthened materially as global demand driven in part by electrification and grid infrastructure build-out and continues to outpace new supply. For a project where copper contributes roughly 30% of overall economics, this dual-commodity exposure provides a natural hedge against volatility in either metal individually.

Jurisdictional risk has become an increasingly prominent consideration for mining investors, particularly as permitting delays and legal challenges have stalled several high-profile North American projects situated on federal land or in more contested regulatory environments. Wyoming's state-level permitting framework, and its comparatively defined objection window, positions CK Gold as a lower-risk alternative within this landscape, a distinction that Norman suggested is not yet fully appreciated by the broader investment community.

As Norman summarised the opportunity:

"We've got a heck of a lot of runway between $260 million and where I could see ourselves being valued in the next 18 months and a lot of news to come to get us to that point."

The scarcity of fully permitted, feasibility-stage gold-copper assets also intersects with a wider capital discipline trend among junior developers, many of which have historically relied on heavy equity issuance to fund construction, diluting shareholders in the process. A company entering project financing discussions with a comparatively small share count and a stated preference for debt financing represents a structurally different risk profile than typical juniors at this stage.

Frequently Asked Questions (FAQs) AI-Generated

Analyst's Notes

Subscribe to Our Channel

%20(1).png)

.jpg)

Stay Informed