US-China Trade Stabilization & 6.15% Silver Surge Signal Industrial Demand Repricing

Silver surged 6.15% on May 11 as the US-China summit reprices industrial demand ahead of the November 10, 2026 trade truce expiry.

- Silver gained 6.15% to $85.36/oz on May 11, 2026, while gold gained 0.39% to $4,734/oz, with silver outperforming gold by 16:1, signalling industrial demand repricing rather than safe-haven buying.

- Approximately 60% of global silver demand comes from industrial sectors including solar PV, EVs, semiconductors, and AI data centers, linking silver demand directly to US-China manufacturing and trade flows, per the Silver Institute’s World Silver Survey 2026.

- China’s rare earth and critical mineral export controls raised supply-chain risk for EV, semiconductor, and industrial manufacturers that also consume silver, making any summit rollback supportive for silver demand.

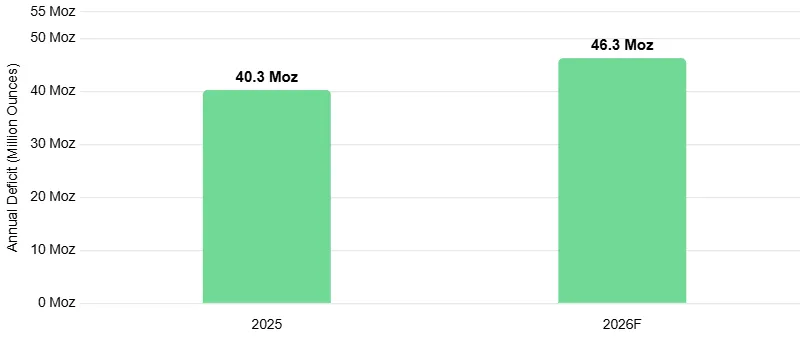

- The US-China truce expires November 10, 2026; an extension would restore six to twelve months of planning certainty for manufacturers that use silver in solar, semiconductor, and EV supply chains, releasing deferred procurement into a market already facing a sixth consecutive annual deficit of 46.3 million ounces.

- Silver producers, developers, and explorers with primary silver assets in established mining jurisdictions gain direct leverage to higher silver prices as trade normalization restores industrial demand.

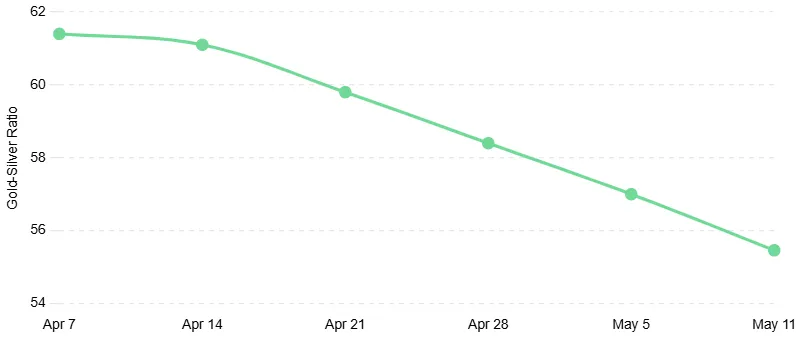

Silver closed at $85.36/oz on May 11, 2026, up 6.15% in a single session, while gold rose 0.39% to $4,734/oz. The gold-silver ratio compressed from above 61 in mid-April to 55.46, a 5.5-point move in under four weeks. That divergence signals industrial demand, not safe-haven buying, as the primary driver of silver prices.

When safe-haven demand drives precious metals, gold typically outperforms silver. Central bank buying, ETF inflows, and investor demand for safe-haven assets during geopolitical uncertainty drive gold demand first. When industrial demand leads, silver outperforms gold as manufacturers increase procurement expectations. Semiconductor, solar, EV, and AI data center supply chains all depend on silver and US-China trade flows. Stable trade conditions support procurement and capacity investment, while deteriorating trade conditions delay forward silver orders.

The Trump-Xi Beijing summit on May 14-15, 2026 is the first US presidential state visit to China since 2017 and will determine whether the November 2025 trade truce remains in place. An extension would restore procurement visibility for industrial silver buyers, while a breakdown in talks could reverse recent demand-driven gains in silver prices.

Gold-Silver Ratio Compression & Margin Expansion for High-Grade Silver Producers

Approximately 95% of gold demand is monetary, driven by central bank buying, sovereign wealth fund allocations, and investor demand for safe-haven assets during geopolitical uncertainty. Around 60% of silver demand comes from solar PV, EVs, semiconductors, AI data centers, and 5G equipment. The recent compression in the gold-silver ratio indicates industrial demand expectations are rising faster than monetary demand for gold

At current prices, each one-point decline in the gold-silver ratio adds approximately $0.80 to $1.50/oz to silver prices through stronger industrial demand expectations. The move from 61 to 55.46 added approximately $4.50/oz to silver prices, excluding any additional support from safe-haven buying. If the Beijing summit extends the trade truce and eases critical mineral restrictions, the ratio could compress toward 50:1, consistent with industrial demand recoveries in 2009 and 2016. A failed summit outcome could push the ratio back toward 60-61 and trigger a $5 to $7/oz correction in silver prices.

Silver producers increasing throughput into rising silver prices can expand operating margins as industrial demand strengthens. Oliver Turner, Executive Vice President of Corporate Development at Americas Gold & Silver, outlines the resource scale supporting future production growth:

“At Galena, we have 190 million ounces in measured, indicated, and inferred resources. This mine has more than a 100-year history of converting those ounces into reserves and production. The resource grade averages 500 grams per tonne silver.”

Industrial Supply Constraints & Vizsla Silver’s Resource Expansion

Any summit agreement that eases rare earth and critical mineral export controls would reduce supply-chain risk for industrial metals manufacturers. Semiconductor, EV, and industrial manufacturers that depend on critical minerals are also major silver consumers, so easing supply restrictions would support future silver demand. Vizsla Silver’s November 2025 Feasibility Study for its fully owned Panuco silver-gold project in Sinaloa, Mexico outlined an after-tax NPV5% of US$1.8 billion, a 111% IRR, and a seven-month payback period using a US$35.50/oz silver price assumption. Jesus Beldor, Vice President of Exploration at Vizsla Silver, outlines the resource growth and exploration efforts supporting future silver supply at the Panuco Project:

“Compared with the previous resource estimate, measured and indicated resources increased 43%. Within the Panuco district we have identified over 140 different vein prospects, of which we have drilled only approximately 30 so far, and for this year we plan to drill over 20,000 meters with the objective of making a new discovery.”

A breakdown in Taiwan-related talks could disrupt semiconductor production, reducing activity in one of the world’s largest industrial silver-consuming sectors. A Beijing-backed Iran ceasefire could reduce safe-haven buying in silver while lowering energy costs for industrial manufacturers.

US-China Trade Stabilization & Resource Growth Across Silver Supply Chains

Silver demand is concentrated in solar, EV, semiconductor, and AI infrastructure supply chains linked to US-China trade, which is why the Trump-Xi summit helped drive a 6% single-session move in silver prices. Any extension of the trade truce would restore procurement visibility for manufacturers that rely on silver across those sectors.

Solar PV, EVs, Semiconductors, & AI Drive Industrial Silver Demand

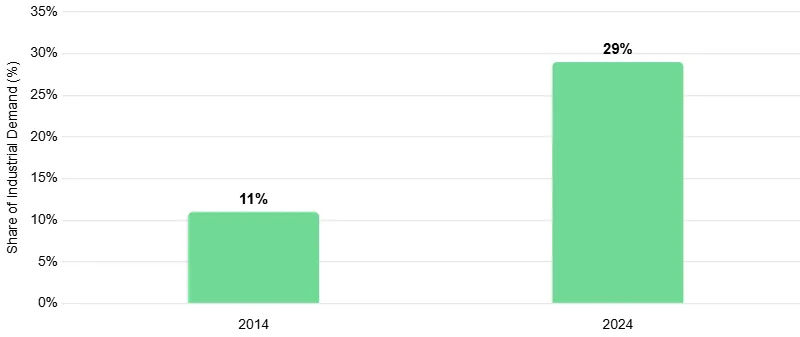

The Silver Institute’s World Silver Survey 2026 identifies solar PV, EVs, semiconductors, and AI data centers as the main industrial growth drivers for silver demand through 2030. Solar PV accounted for 29% of total silver industrial demand in 2024, up from 11% in 2014. EV manufacturers use silver in battery management systems, charging infrastructure, and motor controls. Semiconductor manufacturers use silver bonding wire and coated contacts because few scalable substitutes currently exist. AI data centers also use silver in thermal materials and high-reliability connectors, with limited commercial substitutes available. Silver's cost share in PV manufacturing has risen sharply as a result.

When US-China trade relations deteriorate through tariffs, technology restrictions, or critical mineral controls, manufacturers across these sectors delay capital spending and production expansion. Lower production activity reduces silver procurement against a mine supply base projected to grow only 1% in 2026 to 820 million ounces. Improving trade conditions would increase silver purchasing into a market with limited new supply growth.

Solar PV silver demand is forecast to decline 19% in 2026 to approximately 194 million ounces as manufacturers adopt lower-silver-content cell technologies after silver increased from 3% to 17%-29% of PV module costs per watt since 2023. Chinese solar manufacturers still imported 173% more silver than the 10-year seasonal average in March 2026, increasing purchases ahead of anticipated supply constraints despite lower silver intensity per panel. If sustained through 2026, China’s March silver import pace alone would absorb more than half of the Silver Institute’s projected annual supply deficit of 46.3 million ounces.

China’s Critical Mineral Controls & Supply-Chain Risk for Industrial Silver

China controls approximately 85% of global rare earth processing and more than 90% of permanent magnet production. In April and October 2025, Beijing imposed rare earth and magnet export restrictions that pressured the US to soften planned trade escalation measures. Silver demand remains exposed to rare earth policy because semiconductor and EV manufacturers use both silver and rare earth materials in motors, sensors, and electronic systems.

When critical mineral controls tighten, semiconductor and EV manufacturers face both silver supply risk and rare earth shortages. Easing critical mineral restrictions would reduce supply-chain uncertainty and support renewed silver purchasing by industrial manufacturers. Eric Zaunscherb, Executive Chair and Interim Chief Executive Officer of GR Silver Mining, outlines the company’s resource growth targets:

"We have 134 million ounces of silver equivalent, with significant growth potential through our 20,000-meter drill program. The San Marcial resource averages 22 meters in thickness, allowing us to build ounces quickly, efficiently, and cost effectively."

Trade Truce Negotiations & Renewed Silver Procurement

The Beijing summit will shape silver demand through the trade truce, critical mineral controls, Taiwan, and the Iran war. Taiwan and Iran matter indirectly because semiconductor and industrial supply chains that consume silver remain exposed to geopolitical disruption. The summit’s main economic objective is extending or replacing the truce, potentially alongside broader trade commitments. An extension would restore six to twelve months of planning certainty for solar, EV, and semiconductor manufacturers. That visibility supports new capital spending, with silver procurement typically increasing within 60 to 90 days of production expansion decisions.

Silver’s move above $85/oz on May 11 suggests markets are pricing a 40%-50% probability that the summit extends the US-China truce. A formal truce extension could add $5 to $10/oz to silver prices by restoring industrial purchasing confidence. A breakdown in talks could reverse the industrial buying that drove silver’s May 11 rally.

JPMorgan’s $81/oz silver price forecast already assumed partial US-China trade stabilization, making current spot prices above $85/oz more bullish than the bank’s base case. With silver trading above $85/oz, further upside likely requires a formal trade agreement with clear implementation timelines rather than broad diplomatic commitments.

The Investment Thesis for Silver

- Trade normalization would increase silver demand from solar, EV, semiconductor, and AI data center manufacturers that delayed expansion plans during trade uncertainty, tightening a market already facing a sixth consecutive annual supply deficit of 46.3 million ounces.

- Silver prices remain supported even without a summit agreement because global mine supply is forecast to grow only 1% in 2026 to 820 million ounces, limiting the market’s ability to meet stronger industrial demand without reducing existing inventories.

- Silver producers increasing production while lowering all-in sustaining costs can expand operating margins as silver prices rise. Brownfield discoveries near existing mines also reduce development costs and permitting risk.

- Development-stage silver projects with feasibility studies based on silver prices below current spot levels could become significantly more valuable at today’s prices, particularly where published IRRs already exceed 100%. Future construction decisions could also drive equity revaluations that have not yet been priced into the market.

- Exploration-stage silver companies with debt-free balance sheets, high-grade resources, and active drill programs could benefit from resource growth and lower financing risk, particularly if updated mineral resource estimates are released in the second half of 2026.

The Trump-Xi Beijing summit could drive major short-term moves in silver prices, but the broader supply-demand outlook does not depend on a single diplomatic outcome. Silver’s 6.15% gain on May 11, 2026 signalled that industrial demand, rather than safe-haven buying, was driving the rally. The gold-silver ratio at 55.46 supports that industrial-demand signal. An extension of the trade truce alongside stable critical mineral flows could push silver toward $90 to $95/oz as industrial purchasing recovers. A failed summit outcome could reverse roughly half of this week’s gains and push silver back toward $78 to $80/oz, although the Silver Institute still projects a sixth consecutive annual supply deficit of 46.3 million ounces.

For investors positioned across the silver development spectrum, from brownfield production operations in Tier-1 US jurisdictions to feasibility-stage projects in Mexico's proven silver districts to exploration programs targeting resource updates in the second half of 2026, the case for primary silver exposure rests on the same two foundations.

TL;DR

Silver’s 6.15% gain on May 11, 2026, while gold rose 0.39%, reflected rising industrial demand expectations ahead of the Trump-Xi Beijing summit rather than safe-haven buying. The gold-silver ratio fell from 61 to 55.46 in under four weeks, signalling stronger industrial demand for silver. Approximately 60% of silver demand is industrial, concentrated in US-China supply chains across solar PV, EVs, semiconductors, and AI infrastructure. The US-China trade truce expires November 10, 2026, and any formal extension would increase industrial silver purchasing in a market already facing a sixth consecutive annual supply deficit of 46.3 million ounces. A successful summit outcome could push silver toward $90 to $95/oz. A failed summit outcome could push silver back toward the $78 to $80/oz range, supported by continued global supply deficits.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed