US Dollar Weakness & Geopolitical De-escalation Drive Rotation in Precious Metals: Why Platinum's Supply Deficit Matters Now

Platinum's supply deficit deepens as dollar weakness drives precious metals rotation. Discover why development-stage PGE assets offer asymmetric upside now.

- US dollar weakness following the US-Iran ceasefire is reinforcing a broad commodity bid, with precious metals capturing a disproportionate share of capital rotation as real yields fall and investor demand for non-yielding assets rises.

- Platinum is structurally undersupplied, with the World Platinum Investment Council (WPIC) projecting a 2025 deficit of approximately 1.08 million ounces and continued imbalances through the decade, driven by inelastic mine supply and multi-sector demand growth.

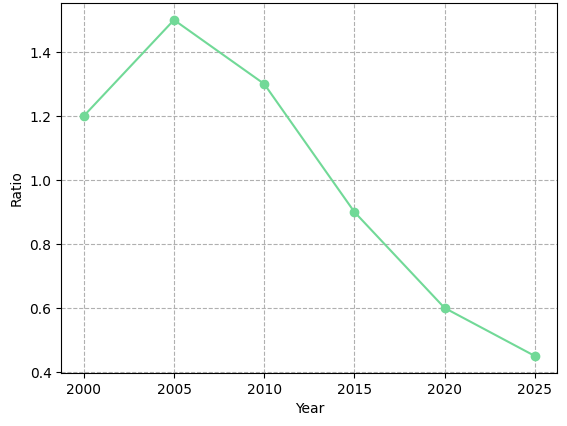

- The platinum-to-gold price ratio remains near 0.40 to 0.45, a historically wide discount given platinum's tighter supply-demand fundamentals, positioning it as a relative value catch-up trade if macro tailwinds persist.

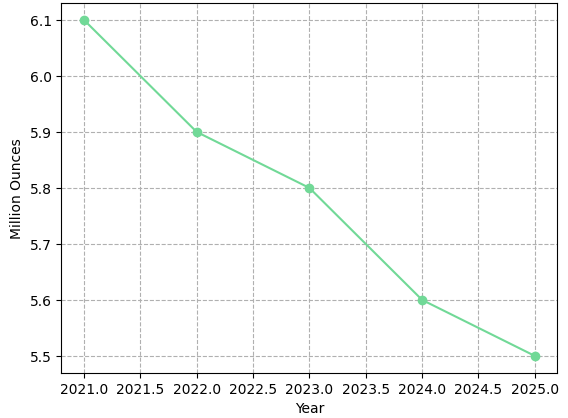

- Primary mine output has contracted from a 2021 peak of approximately 6.1 million ounces to a 2025 forecast of roughly 5.5 million ounces, a structural decline that has occurred against a backdrop of sharply rising metal prices, confirming supply inelasticity.

- Development-stage producers outside traditional supply regions are gaining strategic relevance as jurisdictional diversification becomes a material investment consideration for buyers of platinum group elements (PGEs).

Macro Repricing in Precious Metals

The US-Iran ceasefire that took effect in early 2025 triggered a rapid repricing of risk across commodity markets. Reduced geopolitical pressure contributed to softer oil prices, lower near-term inflation expectations, and meaningful depreciation of the US dollar against major trading currencies. For precious metals, the transmission mechanism was direct: a weaker dollar lowers the effective cost of commodities priced in US dollars globally, expanding the buyer pool and improving the economics of holding non-yielding assets relative to US Treasuries.

Gold responded immediately, extending a rally that has carried it to record highs. Platinum has lagged, a divergence that reflects the market's tendency to price macro liquidity flows before structural fundamentals. The current setup is one where platinum's supply-demand balance is materially tighter than gold's, yet the price ratio between the two metals remains compressed near historic lows. The thesis here is that macro tailwinds now provide the entry conditions for capital to rotate into a metal with stronger underlying fundamentals, and that repricing will be most visible in the equities of developers whose net present values are highly sensitive to the platinum price.

Dollar Weakness & Liquidity Repricing

US dollar depreciation works through two reinforcing channels for precious metals. The first is mechanical: a weaker dollar reduces the local-currency cost of dollar-denominated commodities, stimulating incremental demand from industrial buyers in Europe, Japan, and China. The second is financial: dollar weakness tends to accompany falling real yields, reducing the opportunity cost of holding non-yielding assets. Both channels are currently active.

Real yields on 10-year US Treasury Inflation-Protected Securities have declined from their 2023 peak, and institutional allocators have responded by increasing exposure to precious metals. ETF inflows into gold-backed products are rising, with early evidence of rotation into lagging metals including platinum and silver, where valuations relative to gold remain compressed. The pattern is consistent with prior cycles: gold leads, then relative-value buyers move into underpriced correlates.

Platinum is less sensitive than gold to pure monetary flows because its demand base is heavily industrial. This is precisely why it has lagged the gold rally in the near term, and also why, when the macro tailwind arrives on top of a structural supply deficit, it creates an asymmetric return profile that gold alone does not offer.

Supply Inelasticity in Platinum Markets

The platinum market's supply side is characterized by a degree of inelasticity that is unusual even by the standards of hard-rock mining. WPIC data shows a 2025 deficit of approximately 1.08 million ounces, with a 2026 forecast deficit of approximately 240,000 ounces. Above-ground stocks are declining toward critically low levels, and the council's multi-year outlook does not show a return to balance within the current decade.

Approximately 80-90% of global PGE supply originates from South Africa, Russia, and Zimbabwe. South African production faces persistent power constraints from Eskom, labor instability, and deep-level mining costs that rise with energy inflation. Russian supply faces geopolitical friction and Western sanctions. Primary mine output has contracted at roughly 4 to 5 percent annually over the past several years, a decline that has occurred while platinum prices roughly doubled.

Nick Smart, Chief Executive Officer of ValOre Metals, frames the structural challenge precisely:

"The primary mine production of platinum has been in decline over the last five years. In 2021, it peaked at just over six million ounces. The forecast for this year is around 5.5 million ounces, and that's in the context of a metal price that has doubled over the last year. That tells you something about the inelasticity of supply and the difficulty of bringing new metal into the market."

Beyond Automotive Cyclicality

Platinum demand has historically been dominated by automotive catalytic converters, which currently account for approximately 40 to 50 percent of total consumption. Near-term headwinds from electric vehicle adoption and a roughly 3 percent contraction in auto-sector demand are real. However, the demand mix is diversifying in ways that more than offset the automotive headwind over the medium term.

Platinum is a critical catalyst in proton exchange membrane (PEM) electrolyzers used for green hydrogen production and in hydrogen fuel cells for heavy transport and power generation. Industrial applications in glass manufacturing, petroleum refining, and chemical production provide a stable demand floor. Hybrid vehicles, which carry higher PGM loadings than conventional combustion engines, are partially offsetting pure-EV substitution at the margin.

Investment demand has accelerated markedly, with recent data showing a year-over-year increase of about 65 percent. The elevated gold price is reinforcing a substitution effect, as retail investors and jewelry consumers seeking exposure to precious metals at more accessible price points increasingly redirect capital toward platinum. While recycling activity has expanded by about 10 percent year-over-year, a trend that warrants continued monitoring, its capacity to meaningfully close the production gap remains constrained by the age distribution of the existing vehicle parc, which inherently limits how quickly secondary supply can scale.

Relative Value: Platinum vs Gold

For most of the twentieth century, platinum traded at a premium to gold, reflecting its greater industrial utility and lower annual production volume. The structural break occurred after 2008, compressing the platinum-to-gold ratio well below parity. The current ratio, approximately 0.40 to 0.45, compares with a historical range of 1.0 to 1.5.

The case for mean reversion rests on the observation that platinum's supply constraints are materially tighter than gold's, its demand mix is diversifying toward higher-growth end markets, and investment demand is recovering from cyclically depressed levels. A ratio normalization toward even 0.60, a conservative target by historical standards, implies substantial upside for platinum from current levels.

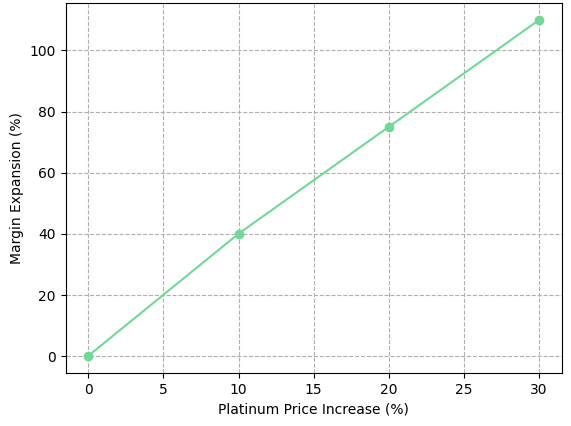

A 20% increase in the platinum price at current all-in sustaining cost (AISC) levels can translate into a 50 to 100 percent expansion in operating margin, depending on the asset's cost structure. NPV sensitivity for development-stage projects is even more pronounced, with valuations typically showing 2 to 3 times price leverage.

Supply Pipeline Reality & Development-Stage Positioning

The development pipeline for new PGE supply is thin relative to the magnitude of the deficit. Capital discipline following the 2015 to 2019 commodity downturn, combined with the complexity of PGE metallurgy, has left the global project inventory with very few assets at an advanced stage. This scarcity creates a dynamic in which new projects, particularly those offering low capital intensity, favorable jurisdiction, and differentiated metallurgical pathways, carry a scarcity premium that the current market has not yet priced.

ValOre Metals is advancing its Pedra Branca PGE project in Ceará, Brazil, an asset with an inferred resource of approximately 2.2 million ounces at 1.08 grams per tonne. The project is geographically strategic: Brazil sits outside the Southern Africa and Russia supply corridor, a consideration gaining weight among institutional buyers of critical metals. The asset benefits from existing paved road access to a deep-water port, grid electricity near the site, and strong community support, factors that materially reduce development capital intensity relative to a greenfield build in a remote jurisdiction.

Metallurgical Innovation & the Path to Economic Validation

The metallurgical path at Pedra Branca is a key differentiator. PGE processing is technically complex, and conventional sulfide routes entail high capital costs. ValOre's test work, which combines bioleaching with a hot caustic pre-treatment of chromitite-associated mineralization, has achieved palladium and platinum extraction rates of 73 to 74 percent via a lower-cost processing route. Smart explains the operational advantage unlocked by chromitite mineralization:

ValOre is targeting publication of a Preliminary Economic Assessment (PEA) in the fourth quarter of 2026. The PEA will establish the NPV, IRR, and capital requirement for the project, the data points institutional investors require before committing capital to a development-stage asset, while simultaneously initiating the formal licensing process in Brazil.

The Investment Thesis for Platinum

- Structural supply deficits in platinum are multi-year in duration and do not resolve through the current decade based on WPIC projections, providing a durable price floor that supports investment in production assets at current valuations.

- The macro environment, characterized by US dollar weakness, declining real yields, and post-ceasefire capital deployment, creates the liquidity conditions for a sustained rotation into commodity assets, with precious metals among the primary beneficiaries.

- Platinum's relative valuation discount to gold, reflected in a current ratio near 0.40 to 0.45 versus a historical range of 1.0 to 1.5, represents a quantifiable mispricing for investors positioned ahead of a fundamental repricing.

- Jurisdictional diversification outside Southern Africa and Russia is increasingly valued by institutional buyers as geopolitical risk in the traditional supply corridor remains elevated, creating strategic optionality for projects in stable jurisdictions such as Brazil.

- Development-stage assets with low capital intensity, near-surface open-pit potential, and commercially viable recovery rates offer asymmetric exposure to platinum price appreciation, with NPV sensitivity that typically runs two to three times the metal price leverage available from producing-company equities.

- The PEA milestone for projects in the current pipeline functions as a dual catalyst: a valuation inflection as NPV and IRR are formally established, and a regulatory trigger that initiates the licensing process required for construction.

The current moment in platinum markets reflects a convergence that does not occur frequently: a favorable macro entry point driven by dollar weakness and capital rotation, coinciding with a structural supply deficit that has no near-term resolution, in a market where development-stage assets remain deeply discounted relative to fundamental value.

Gold may lead the precious metals cycle in absolute price terms. But platinum offers greater convexity to the tightening of physical market balances, and that tightening is structural, not cyclical. It reflects a decade of under-investment in new mine development, supply concentration in geopolitically exposed jurisdictions, and the emergence of hydrogen-economy demand that the market has not yet priced into forward supply planning. For investors positioned ahead of that recognition, the combination of macro tailwinds and fundamental scarcity creates a risk-adjusted return profile that is difficult to replicate elsewhere in the commodity complex.

TL;DR

Platinum is structurally undersupplied, with a projected 2025 deficit of approximately 1.08 million ounces and no return to balance forecast within the decade. A weakening US dollar, declining real yields, and post-ceasefire capital rotation are creating favorable macro entry conditions precisely as platinum trades at a historically wide discount to gold, near 0.40 to 0.45 versus a historical range of 1.0 to 1.5. Against this backdrop, development-stage assets outside the traditional Southern Africa and Russia supply corridor, particularly those with low capital intensity and commercially viable metallurgical pathways, offer asymmetric exposure to a repricing that the market has not yet fully recognized.

FAQs (AI-Generated)

Primary mine production of platinum has declined from a 2021 peak of approximately 6.1 million ounces to a 2025 forecast of roughly 5.5 million ounces, a contraction that has occurred even as metal prices roughly doubled, confirming the inelasticity of supply. Between 80 and 90 percent of global PGE output is concentrated in South Africa, Russia, and Zimbabwe, jurisdictions facing persistent operational, political, and sanctions-related headwinds. The World Platinum Investment Council projects a 2025 deficit of approximately 1.08 million ounces, with continued imbalances through the end of the decade. Capital discipline following the 2015 to 2019 commodity downturn has left the global development pipeline thin, meaning new supply cannot be brought to market quickly enough to close the gap in any near-term scenario.

The US-Iran ceasefire in early 2025 triggered a broad repricing of risk assets, contributing to a meaningful depreciation of the US dollar and softer near-term inflation expectations. For precious metals, dollar weakness operates through two reinforcing channels: it mechanically reduces the local-currency cost of dollar-denominated commodities for buyers in Europe, Asia, and beyond, and it tends to accompany falling real yields, which lower the opportunity cost of holding non-yielding assets such as platinum. Institutional allocators have responded by increasing precious metals exposure, with gold leading the rotation and early evidence of capital moving into undervalued correlates including platinum, where the valuation discount relative to gold remains near historic extremes.

For most of the twentieth century, platinum traded at a premium to gold, with a price ratio typically ranging between 1.0 and 1.5, reflecting platinum's tighter annual production and greater industrial utility. That relationship broke down after 2008, and the current ratio of approximately 0.40 to 0.45 represents one of the widest discounts on record. The case for normalization rests on platinum's tighter supply-demand fundamentals relative to gold, a diversifying demand mix that includes hydrogen economy applications, and investment demand recovering from cyclically depressed levels. A conservative rerating toward a ratio of 0.60 would imply substantial upside from current levels, with the leverage effect amplified significantly for development-stage projects whose NPVs typically show two to three times metal price sensitivity.

Near-term headwinds from EV adoption are real, with auto-sector demand contracting by approximately 3 percent, and warrant acknowledgment. However, the demand picture beyond the automotive sector is diversifying in ways that more than offset this pressure over the medium term. Platinum is a critical catalyst in proton exchange membrane electrolyzers used for green hydrogen production, as well as in hydrogen fuel cells for heavy transport and stationary power generation, applications representing some of the fastest-growing demand vectors in the energy transition. Additionally, hybrid vehicles carry higher PGM loadings than conventional combustion engines, partially offsetting pure-EV substitution at the margin. Investment demand has also accelerated sharply, rising approximately 65 percent year-over-year, as the elevated gold price drives retail and institutional buyers toward platinum as a more accessible precious metals alternative.

Pedra Branca stands out within the global PGE development pipeline for several compounding reasons. The project is located in Ceará state, Brazil, outside the geopolitically exposed Southern Africa and Russia supply corridor, at a time when jurisdictional diversification is becoming a material consideration for institutional buyers of critical metals. Its existing infrastructure, including paved road access to a deep-water port and grid electricity near the site, materially reduces development capital intensity relative to a comparable greenfield project in a remote jurisdiction. Critically, ValOre's metallurgical test work has demonstrated a lower-cost processing pathway combining bioleaching with hot caustic pre-treatment, achieving palladium and platinum extraction rates of 73 to 74 percent, a commercially meaningful result given the technical complexity and capital intensity of conventional PGE processing routes. The publication of a Preliminary Economic Assessment in Q4 2026 is expected to serve as a dual catalyst, formally establishing the project's NPV and IRR while initiating the licensing process required for construction.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed