Russian Palladium Tariffs & Platinum Deficits Re-rate Low-Risk PGM Projects as 90% of Supply Remains Concentrated

Russian palladium tariffs and platinum deficits tighten PGM supply, lifting valuations for lower-risk projects outside Russia and South Africa.

- The US imposed combined countervailing and anti-dumping duties above 240% on Russian palladium, increasing supply costs across a market where Russia controls roughly 40% of global output.

- The World Platinum Investment Council forecasts a fourth consecutive platinum deficit in 2026, with above-ground inventories falling to roughly four months of global demand cover.

- South Africa, Russia, and Zimbabwe collectively supply about 90% of primary platinum group metals (PGMs), increasing valuation premiums for projects in lower-risk jurisdictions such as Brazil.

- China VII emissions standards and accelerating hydrogen infrastructure growth are sustaining platinum demand despite rising electric vehicle adoption, with global electrolyser capacity expanding nine-fold between 2021 and 2025.

- Exploration-stage PGM projects outside concentrated supply regions continue trading at lower EV/oz multiples than comparable peers, despite improving macro conditions and rising jurisdiction-risk premiums.

Russian Palladium Tariffs & Platinum Deficits Raise PGM Supply-Risk Premiums

Two announcements within a four-day window in late May 2026 increased PGM price and supply-risk premiums. The first was a US trade action that raised the delivered cost of Russian palladium for Western refiners. The second was the World Platinum Investment Council’s confirmation that the platinum market is entering a fourth consecutive annual deficit with inventories covering roughly four months of demand.

US Palladium Tariffs Raise Western Supply Costs for Russian Metal

On May 22, 2026, the US Department of Commerce published a final 109.1% countervailing duty on Russian unwrought palladium. The ruling adds to the 132.83% anti-dumping duty finalized in April 2026, lifting the combined tariff above 240% ahead of the US International Trade Commission injury determination.

Norilsk Nickel, which supplies roughly 40% of global palladium output, guided 2026 production to 2.415-2.465 million ounces, its lowest level in two decades. US imports of Russian palladium rose to 27.6 tons in 2024 from 23.8 tons in 2023, increasing procurement pressure on Western buyers to source from Sibanye-Stillwater and South African producers.

WPIC Confirms Fourth Consecutive Platinum Deficit as Inventories Tighten

The World Platinum Investment Council’s Q1 2026 Platinum Quarterly, published May 19, raised the 2026 platinum deficit forecast to 297,000 ounces from 240,000 ounces. The market is now tracking a fourth consecutive annual deficit, with the 2025 shortfall of 1.082 million ounces the largest in WPIC data since 2014. Cumulative above-ground stock drawdowns since 2023 now equate to roughly 42% of beginning inventory, leaving cover at approximately four months of global demand. Together, the tariffs on roughly 40% of palladium supply and the four-year platinum deficit reduced the market’s ability to absorb additional supply shocks.

90% PGM Supply Concentration Raises Valuations for Lower-Risk Jurisdictions

PGM supply is more geographically concentrated than any other major mined commodity. South Africa, Russia, and Zimbabwe account for roughly 90% of primary PGM supply. For most of the past decade, investors assigned limited valuation discounts to that concentration. The May 2026 tariffs and deficit data increased the valuation premium for projects outside concentrated supply jurisdictions.

South Africa, Russia & Zimbabwe Face Rising PGM Supply and Cost Pressures

South Africa, Russia, and Zimbabwe supply roughly 90% of primary PGMs. Each jurisdiction now faces active production, trade, or sovereign-risk pressures. In South Africa, 2025 flood disruptions continue to limit production recovery, while higher oil prices are increasing diesel and smelting costs. In Russia, the combined 109.1% countervailing and 132.83% anti-dumping duties sharply increase the delivered cost of palladium from the world’s largest producer. In Zimbabwe, Zimplats reported lower Q1 2026 production amid ongoing currency and sovereign-risk pressures.

Higher energy prices are increasing operating costs for PGM producers. The World Bank’s April 2026 Commodity Markets Outlook projects energy prices rising 24% in 2026 to their highest level since 2022, while the broader commodity index rises 16%. The International Energy Agency said the Strait of Hormuz disruption is the largest oil-supply shock on record, increasing fuel and transport costs for energy-intensive mining operations.

Nick Smart, Chief Executive Officer of ValOre Metals, describes how rising energy costs and Strait of Hormuz exposure are increasing operating risks for South African PGM producers:

"Electricity costs have increased by about 60% over that 5-year period from 2021 to 2026. About 60% of South Africa's diesel is coming through the Strait of Hormuz."

Jurisdiction Risk Now Carries Greater Weight in PGM Valuations

For most of the past decade, PGM equities were valued primarily on grade, contained ounces, and the ratio of measured-and-indicated to inferred resources. The 2026 tariffs and supply deficits increased the valuation premium for projects in lower-risk jurisdictions.

Enterprise value per resource ounce (EV/oz) no longer captures jurisdictional supply risk consistently across PGM projects. Projects outside South Africa, Russia, and Zimbabwe now warrant higher EV/oz multiples than projects within concentrated supply jurisdictions. The Shanghai-London platinum price spread widened after China removed its 13% platinum import VAT exemption in November 2025 and delivery stress increased at the Guangzhou Futures Exchange, showing that regional supply shortages now affect pricing directly.

Auto-Catalyst & Hydrogen Demand Continue Supporting Platinum Consumption

The main bearish case for PGMs has been that electric vehicle adoption will reduce auto-catalyst demand. WPIC’s 2026 forecasts show auto-catalyst demand declining more slowly than expected despite rising electric vehicle adoption. Stricter emissions standards are increasing platinum loadings per vehicle, while hydrogen infrastructure growth is adding a second source of long-term demand.

China VII Emissions Rules Increase Platinum Auto-Catalyst Demand

China VII vehicle emission standards take effect in 2026 and are expected to increase PGM loadings per vehicle through stricter cold-start and on-road emissions testing. China’s Stage 4 fuel consumption standards for light commercial vehicles also take effect in 2026 and support continued catalyst demand from hybrid and internal-combustion vehicles. WPIC’s Q1 2026 Platinum Quarterly forecasts automotive platinum demand declining only 2% in 2026 despite higher electric vehicle penetration.

Hydrogen Infrastructure Growth Expands Long-Term Platinum Demand

Hydrogen infrastructure is becoming a larger source of platinum demand. WPIC data shows green hydrogen production increased six-fold between 2021 and 2025, from 50 to 300 kilotonnes annually, while global electrolyser capacity expanded from 0.6 GW to 4.9 GW. By end-2025, China operated the world’s largest hydrogen vehicle network, with 40,000 fuel cell vehicles and 574 hydrogen refuelling stations.

Hydrogen technologies use significantly more platinum per unit than traditional auto-catalyst systems. Proton-exchange-membrane (PEM) electrolysers require platinum at the cathode to produce hydrogen. A fuel cell vehicle contains 30-60 grams of platinum versus roughly 5 grams in a conventional catalytic converter. WPIC also forecasts bar and coin investment demand rising 35% in 2026 to 725,000 ounces, driven partly by stronger retail demand in India.

Supply-Risk Repricing Changes Exploration-Stage PGE Valuations

Tariffs, supply deficits, and jurisdiction risks now affect how investors value PGM equities. Exploration and development-stage PGM companies are still largely valued on EV/oz metrics that underweight jurisdictional supply risk. That gap leaves lower-risk projects trading at EV/oz multiples below comparable assets in concentrated supply jurisdictions.

Exploration-Stage PGE Companies Trade at Wide EV/oz Valuation Discounts

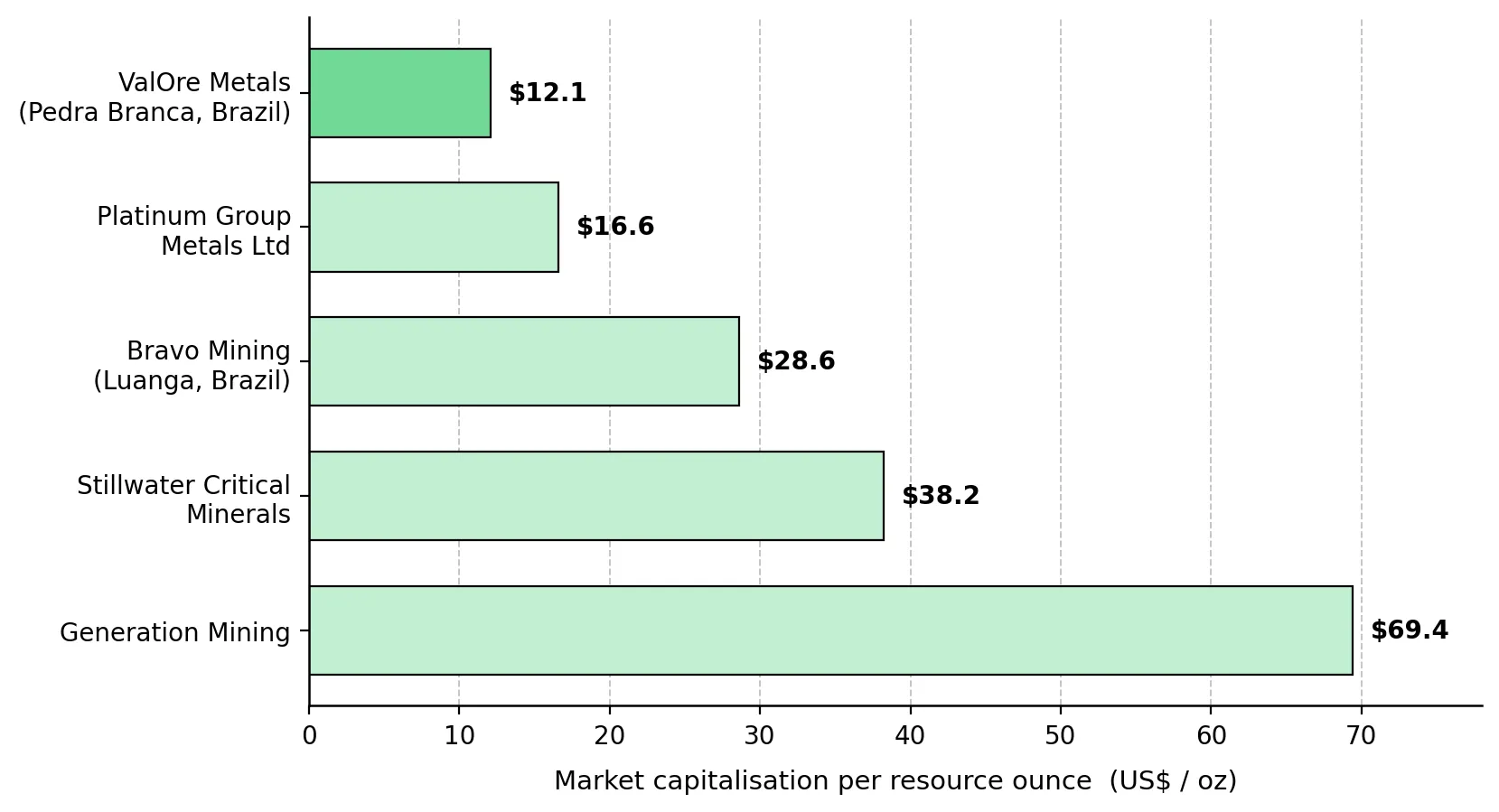

Few development-stage PGE companies trade in public markets. Stillwater Critical Minerals trades at roughly US$126 million against a Stillwater West resource containing 2.0 million ounces of palladium and 1.3 million ounces of platinum. Generation Mining trades at roughly US$236 million against the Marathon project resource of 2.6 million ounces of palladium and 0.8 million ounces of platinum. Platinum Group Metals Ltd trades at roughly US$389 million against the 23.4-million-ounce Waterberg resource. Bravo Mining trades at roughly US$440 million for its Brazilian Luanga project, which hosts 10.4 million measured-and-indicated and 5.0 million Inferred palladium-equivalent ounces.

ValOre Metals trades at roughly US$26-27 million despite Pedra Branca hosting a 2022 NI 43-101 Inferred Resource of 2.198 million ounces 2PGE+Au across 63.6 million tonnes at 1.08 g/t in northeast Brazil. Pedra Branca’s resource size is comparable to smaller peer projects, yet ValOre trades at a lower implied EV/oz despite its Brazilian jurisdiction.

Brazil’s Infrastructure & Permitting Advantages Support Higher PGM Valuations

Brazil offers geographic diversification, lower-cost grid power, and an established mining permitting system. Pedra Branca is located roughly four hours by paved highway from a deep-water port, has nearby grid power access, and has no disclosed community or permitting issues according to management. Brazil also graduates more mining engineers annually than the United States and Canada combined, supporting long-term mine staffing and technical capacity. Bravo Mining’s roughly US$440 million valuation at Luanga suggests Brazilian PGM projects already trade at higher developer-stage valuations.

Heap-Leach Metallurgy Supports Pedra Branca’s Q4 2026 PEA Target

A Preliminary Economic Assessment (PEA) is the first study to estimate project economics such as NPV, IRR, capex, and AISC for a defined mineral resource. Pedra Branca is targeting a Q4 2026 PEA supported by three programs: heap-leach metallurgical testing with the University of Cape Town that produced bench-scale recoveries of roughly 73% platinum and 74% palladium; geological relogging across the Curiu, Esbarro, and Cedro deposits; and a Q1 2026 resource update incorporating 2023 drilling, including the Salvador Target discovery. The heap-leach process is important because oxidised near-surface material does not respond efficiently to conventional flotation methods used in most PGE processing.

Downside Risks & Catalysts That Could Weaken the PGM Investment Thesis

The investment thesis depends on specific macro and project catalysts. Macro risks to the thesis include a negative ITC injury ruling that removes the Russian palladium tariffs and triggers an estimated 8-12% palladium price decline as inventories liquidate; a Strait of Hormuz de-escalation that lowers energy prices; commercial adoption of a non-platinum PEM fuel-cell catalyst; or a Federal Reserve policy shift that pushes real yields above 2.5% and reduces precious metals valuations.

Project-level risks include a delayed or cancelled maiden PEA, uneconomic PEA results at prevailing PGM prices, heap-leach recoveries below bench-scale test results, a lower resource estimate, or failure to complete announced asset sales and financings on schedule.

Exploration-stage PGM equities carry liquidity, dilution, and resource-conversion risks, with warrants and convertible debentures commonly used for financing. Under Canadian Institute of Mining standards, inferred resources have not demonstrated economic viability and may change due to environmental, permitting, legal, and market conditions.

The Investment Thesis for Platinum Group Metals

- The combined 109.1% countervailing and 132.83% anti-dumping duties increased the delivered cost of roughly 40% of global palladium supply, benefiting producers and developers in Western and allied jurisdictions.

- The platinum market is in its fourth consecutive annual deficit, with above-ground inventories covering roughly four months of demand, reducing the market’s ability to absorb supply disruptions.

- Because South Africa, Russia, and Zimbabwe supply roughly 90% of PGMs, Western automakers and refiners are placing higher value on projects in lower-risk jurisdictions.

- China VII emissions standards are increasing platinum loadings in auto catalysts, while green-hydrogen production increased six-fold and electrolyser capacity expanded nine-fold between 2021 and 2025, adding a second source of long-term demand.

- Exploration-stage PGM projects outside concentrated supply jurisdictions still trade at lower EV/oz multiples than comparable peers despite lower geopolitical and supply-risk exposure.

- The investment thesis depends on measurable catalysts, including the US International Trade Commission injury ruling, upcoming resource updates, and maiden PEA results that could confirm or weaken the valuation case for PGM equities.

The May 2026 Russian palladium tariffs and WPIC deficit confirmation increased the valuation impact of geographic supply concentration in PGMs. Investors are now valuing projects on both resource size and jurisdictional risk. Over the next 90 days, investors will receive the US International Trade Commission ruling on Russian palladium tariffs and maiden PEA results from several PGM projects outside concentrated supply jurisdictions. Both catalysts will show whether investors assign higher valuations to projects in lower-risk jurisdictions.

TL;DR

US tariffs on Russian palladium and a fourth consecutive platinum market deficit are reshaping how investors value PGM assets. Russia supplies roughly 40% of global palladium output, while South Africa, Russia, and Zimbabwe control about 90% of primary PGM supply, increasing supply-security concerns for Western buyers. At the same time, platinum inventories have fallen to roughly four months of global demand, reducing the market’s ability to absorb additional supply shocks. Stronger hydrogen demand, tighter emissions standards, and higher platinum loadings in auto catalysts are supporting long-term consumption despite electric vehicle adoption. The result is a valuation shift toward PGM projects in lower-risk jurisdictions such as Brazil, where exploration-stage companies still trade at lower EV/oz multiples than comparable peers.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed