Higher Interest Rates Raise Financing Costs as Critical Minerals Supply Tightens; 2026 Rate-Cut Odds Fall Below 3%

Higher interest rates and tighter critical minerals supply are shifting investor focus from resource size to financing capacity, balance sheets, and funding access.

- A leadership change at the United States Federal Reserve and an inflation shock have pushed market-implied odds of a 2026 rate cut below 3 percent, raising discount rates and borrowing costs that determine mining-project valuations.

- Battery and critical metals investors face a widening gap between supply fundamentals and funding conditions. Producer-nation supply discipline across cobalt, nickel and rare earths is reducing projected surpluses, while higher interest rates have raised the cost of funding new mines.

- Balance-sheet strength and funding access, rather than grade or tonnage alone, now determine which mining projects reach construction.

- Government support through offtake floors, development-finance loans, flow-through tax incentives and strategic reserves is helping Western critical minerals projects secure funding despite higher private-capital costs.

Higher Interest Rates Raise Mining Financing Costs as 2026 Rate-Cut Odds Fall Below 3%

For battery metals investors in 2026, capital costs now matter more than spot metal prices. Kevin Warsh was sworn in as Chair of the United States Federal Reserve on May 15, 2026, and Federal Open Market Committee minutes released on May 20 indicated that an Iran-driven inflation shock could require further rate increases. Market-implied probability of a 2026 rate cut has fallen below 3 percent. For long-duration assets such as mines, higher discount rates reduce project valuations.

Higher discount rates reduce the net present value (NPV) of projects whose production is years away. Tighter credit conditions and a stronger United States dollar raise the return threshold required for lenders to fund new project debt. Risk-off sentiment raises the cost of equity for pre-revenue developers, forcing them to issue more shares to raise the same capital.

Investors must weigh tightening supply against rising funding costs. Producer-nation supply discipline is tightening metal balances, while higher interest rates are raising project funding costs. Investors should focus on funding structure as well as resource quality, because higher capital costs increasingly determine which projects reach construction.

Higher Interest Rates Hit Mining Valuations Harder Due to Long-Dated Cash Flows

Mining projects generate much of their cash flow years into the future, making valuations highly sensitive to discount rates. A project valued at an 8 percent discount rate (NPV8) can lose significant net present value when re-rated at 10 percent (NPV10), because higher discount rates reduce the present value of future cash flows. Higher capital costs raise the internal rate of return (IRR) required to exceed a project's weighted average cost of capital (WACC) and support a final investment decision (FID).

Producers with current revenue are less exposed to higher rates because operating cash flow reduces reliance on external financing. Pre-revenue developers and explorers remain dependent on external financing. When equity is the only available funding source, lower share prices force companies to issue more shares to raise the same capital, increasing dilution. Dilution is the primary risk for early-stage developers, because repeated equity raises can reduce per-share value and increase the risk of permanent capital loss.

Higher Capital Costs Pressure Development-Stage Project Valuations

Sovereign Metals shows how higher capital costs affect development-stage project valuations. The April 2026 definitive feasibility study reported a pre-tax NPV8 of US$2.2 billion. That valuation depends on an 8 percent discount rate and declines as capital costs rise. Lower capital intensity reduces funding requirements and limits valuation pressure from higher capital costs. Sovereign Metals has identified monazite as a potential heavy rare-earth by-product recoverable from the existing processing flowsheet at near-zero incremental cost. The monazite credit is not included in the April 2026 definitive feasibility study and requires further metallurgical work before it can be assigned value.

Supply Constraints & Higher Capital Costs Separate Funded Projects from Unfunded Developers

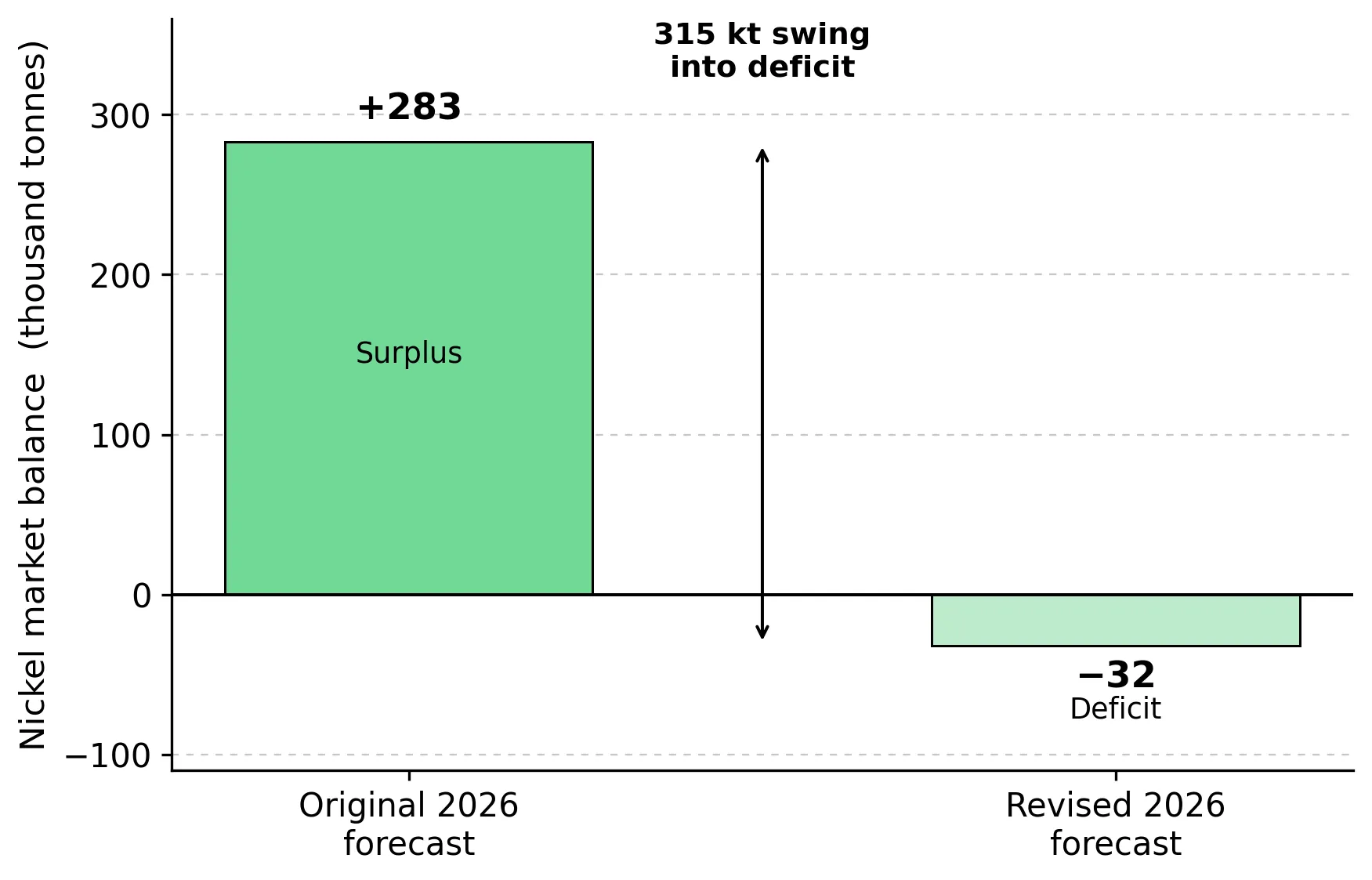

Producer-nation supply restrictions are reducing projected cobalt and nickel supply growth. The Democratic Republic of Congo set cobalt export quotas of 96,600 tonnes for 2026 and 2027, roughly half of 2024 levels, and Fastmarkets forecasts a 10,700-tonne cobalt deficit in 2026. Indonesia cut its 2026 nickel mining quota to between 260 and 270 million wet metric tonnes, down from 379 million approved for 2025, prompting the International Nickel Study Group to revise its 2026 balance from a 283,000-tonne surplus to a 32,000-tonne deficit. China continues to tighten rare-earth export controls, increasing supply-security concerns for Western buyers.

These measures support prices, but higher prices alone do not fund new projects. Higher prices improve project IRRs and increase debt capacity, but only projects with access to capital can capture that benefit. Funded or near-cash-flow companies can advance projects into construction, while capital-dependent developers and explorers remain constrained by financing access as much as geology.

Nickel Supply Constraints Increase the Value of Funded Sulfide Projects

Western nickel developers are focused on sulphide deposits, which are generally less processing-intensive than the laterite ores that dominate Indonesian supply. Sulfide concentrates are generally cheaper to process and produce more traceable units, improving financing and offtake prospects. Canada Nickel and Lifezone Metals both require substantial project funding in a higher-cost capital market.

Mark Selby, Chief Executive Officer of Canada Nickel, describes how few nickel projects have advanced far enough to benefit from tightening supply and improving project economics:

"There's 200 gold stories, there's 150 silver stories, there's 100 copper stories, but there really are only a half a dozen nickel stories that have had meaningful advancement."

Scarce advanced nickel projects can command higher valuations, but only funded projects convert tighter supply into shareholder value.

China's Rare-Earth Dominance Increases Demand for Ex-China Supply

China controls roughly 95 percent of global heavy rare-earth output, including dysprosium and terbium used in permanent magnets for defence systems and electric vehicles. China's market share increases the strategic value of ex-China rare-earth supply, improving financing and offtake opportunities for companies such as Sovereign Metals and Energy Fuels. Supply-security demand can support financing and offtake even when project economics alone are insufficient to attract capital.

Ben Stoikovich, Chairman of Sovereign Metals, explains why Rio Tinto's strategic investment reflects the importance of large-scale ex-China supply:

"Rio Tinto became a strategic investor in Sovereign in mid-2023. Today Rio has invested US$60 million and is a 19.9% shareholder."

Higher Capital Costs Increase the Importance of Balance-Sheet Strength

Higher capital costs produce different outcomes depending on a company's funding position. In a higher-cost capital market, balance-sheet strength matters as much as resource quality. The key question is which company can fund construction without significant shareholder dilution when capital is expensive.

Cash-Generating Producers Can Fund Growth Without Dilution

Energy Fuels is less exposed to higher capital costs because it generates operating cash flow. For the quarter ended March 31, 2026, Energy Fuels reported US$956.6 million of working capital and US$8.3 million of operating cash flow, while uranium sold for an average US$70.04 per pound versus a Pinyon Plain production cost of US$23-30 per pound. Those margins support a US$410 million Phase 2 rare-earth expansion with an NPV8 of US$1.9 billion and a 33 percent IRR without requiring near-term equity issuance.

Mark Chalmers, former Chief Executive Officer of Energy Fuels, explains how uranium cash flow lays the financial foundation for the company's rare-earth expansion:

"Uranium is now. We'll give guidance up to 2.5 million pounds and that's greater than anybody else in the United States. Really good cost structures and prices are firming. So that is the revenue story right now."

High-Grade Nickel Projects Still Depend on Project Financing

Lifezone Metals has an advanced project that remains dependent on project financing. The Kabanga nickel project carries a grade of approximately 1.92 percent nickel, equivalent to 4.1 percent copper-equivalent, supporting an after-tax IRR of 23.3 percent and an AISC of US$3.36 per pound net of by-product credits. High grade increases debt capacity, but the project still requires a framework agreement, renegotiation, power agreements and lender approvals before construction can proceed. Lifezone held US$15.3 million of cash at March 31, 2026, while its share price fell from US$4.27 to US$3.36 during the quarter.

Ingo Hofmaier, Chief Financial Officer of Lifezone Metals, explains how grade translates into financeability:

"Because of the high grade and therefore the high profitability, the debt capacity of the project is quite high, and we expect, after several rounds of discussions with lenders, that it will be around 60/40."

Capital Efficiency and Strategic Funding Reduce Dilution Risk

Companies with limited funding access rely on capital efficiency and strategic investors to reduce dilution. Rio Tinto owns 18.5 percent of Sovereign Metals, reducing reliance on equity financing, while a near-zero-incremental-cost by-product pathway helps preserve project value as discount rates rise. Canada Nickel is funding exploration through a C$4.97 million non-brokered flow-through placement priced at C$2.07 per share. Flow-through shares allow investors to deduct exploration spending against income, reducing funding costs for explorers. The placement is small and dilutive, highlighting the limited funding options available to micro-cap developers while Canada Nickel targets a Crawford permitting decision by early summer 2026.

Government Support Reduces Financing Risk for Western Critical Minerals Projects

Higher private-capital costs and Western supply-chain policies are increasing government involvement in critical minerals project financing. Energy Fuels' inclusion on the United States Critical Minerals List and accelerated permitting at Roca Honda and Bullfrog could shorten development timelines and improve access to government support. Lifezone Metals has completed United States Development Finance Corporation due diligence and submitted a combined US$41.5 million Department of Energy funding request for its platinum-group-metals recycling work. Canada Nickel is using flow-through tax incentives while pursuing government funding, and Sovereign Metals is pursuing government support and offtake agreements for its heavy rare-earth project.

Government backing can reduce financing risk and offset higher private-capital costs, shortening the path from permitting to a final investment decision. Government support also introduces policy and jurisdictional risk, because delayed approvals or funding decisions can postpone construction regardless of project quality.

The Investment Thesis for Battery & Critical Metals

- Producers with current cash flow have an advantage in a higher-for-longer rate environment because internally funded growth avoids dilutive equity when the odds of a 2026 rate cut are below 3 percent.

- Supply discipline across cobalt, nickel and rare earths improves project economics, but only developers that can secure financing above a rising cost of capital can advance projects.

- Capital efficiency matters more than scale when discount rates rise, because low-cost by-product pathways and strategic investors help preserve project value.

- Government capital can offset higher private-financing costs, as development-finance loans, offtake floors, flow-through incentives and strategic reserves reduce funding risk for Western developers and explorers.

- Supply-chain decoupling and jurisdictional preferences are increasing demand for ex-China heavy rare-earth and Western nickel-sulphide projects, although policy changes and trade retaliation remain key risks.

- Investors should size positions carefully because dilution, unresolved final-investment-decision requirements, permitting outcomes and pre-revenue cash burn can result in permanent capital loss.

Producer-nation supply restrictions have tightened cobalt and nickel balances that were in surplus a year ago. With the odds of a 2026 rate cut below 3 percent, project financing now matters more than resource size. Producers and fully funded developers can convert tighter supply into shareholder value, while undercapitalized companies remain exposed to dilution and funding risk regardless of grade or tonnage. Investors should assess balance sheets, funding structures, government backing and final-investment-decision timelines as closely as resource quality. In this cycle, access to capital increasingly determines which projects reach production.

TL;DR

Battery and critical metals markets are tightening as producer nations restrict cobalt, nickel and rare-earth supply, but higher interest rates are raising financing costs and reducing mining-project valuations. In this environment, balance-sheet strength, cash flow, government support and access to capital matter more than resource size alone. Companies that can self-fund growth or secure financing are better positioned to benefit from improving commodity fundamentals, while capital-constrained developers face dilution risk and delayed project timelines.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

%20(1).jpg)

.jpg)

Stay Informed