West Red Lake Gold: High-Grade Play in $4K Gold Era

West Red Lake Gold targets 100K oz/yr by 2029. Madsen ramping, Rowan PEA shows 42% IRR. C$41M financing secured. High-grade Red Lake camp benefits from gold rally.

- Gold futures surpassed $4,000 per ounce on October 7, 2025, driven by U.S. government shutdown concerns, tariff uncertainties, and safe-haven demand, creating a favorable pricing environment for high-grade producers.

- West Red Lake Gold closed a C$41 million bought-deal financing in September 2025, strengthening its balance sheet to support the Madsen Mine ramp-up and advance the Rowan Project toward a pre-feasibility study.

- The company produced 9,550 ounces from January to July 2025, with mill throughput averaging 650 tonnes per day and achieving 95% recovery rates, demonstrating operational momentum toward commercial production.

- The August 2025 preliminary economic assessment for Rowan outlined a $125 million net present value (post-tax, 5% discount) and 42% internal rate of return based on toll-milling 35,200 ounces annually over five years.

- Management targets greater than 100,000 ounces per year by 2029 through integration of Madsen, Rowan, and exploration assets including Fork and Upper 8 deposits in Ontario's proven Red Lake mining camp.

Gold's breach of the $4,000 per ounce threshold in early October 2025 marks a watershed moment for precious metals investors and junior producers alike. The Comex futures rally up 0.79% on October 7 to close above the psychological barrier reflects intensifying demand for safe-haven assets amid U.S. fiscal gridlock and monetary policy uncertainty. For companies operating high-grade gold assets in stable jurisdictions, the price environment presents a rare alignment of operational leverage and market timing.

West Red Lake Gold Mines Ltd., a Canadian junior that restarted production at its flagship Madsen Mine in Ontario earlier this year, exemplifies this opportunity. With a freshly capitalized balance sheet, expanding resource base, and clear pathway to mid-tier production levels, the company offers exposure to one of Canada's most prolific gold districts at a critical inflection point. This article examines why the convergence of macro tailwinds, project fundamentals, and corporate execution warrants investor attention.

The thesis rests on three pillars: operational de-risking at Madsen, near-term development optionality at Rowan, and exploration leverage across a consolidated land package in the Red Lake camp. Each component contributes to a sum-of-parts valuation that appears disconnected from current market pricing, particularly as gold's rally validates higher-margin operating scenarios.

Company Overview

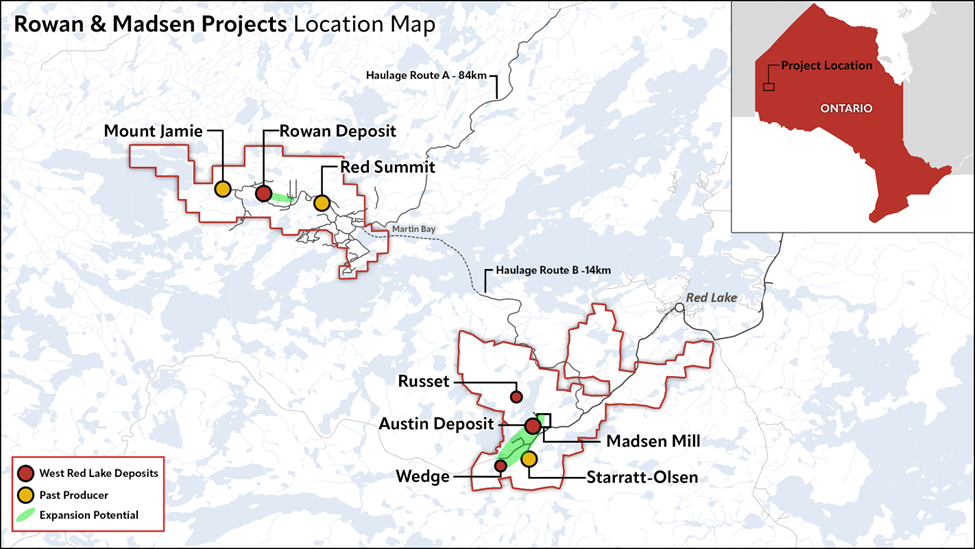

West Red Lake Gold acquired the Madsen Mine in 2023 as a distressed asset, inheriting infrastructure that included an 800-tonne-per-day mill, shaft access, and underground development in a district renowned for high-grade mineralization. The Red Lake greenstone belt has historically produced over 30 million ounces, with neighbor Evolution Mining's Red Lake operations and past-producing mines like Campbell and Dickenson establishing the region's credentials. West Red Lake's strategy centered on reversing operational missteps by prior owners through focused geology work, engineering upgrades, and workforce reconstitution.

The company's capital structure as of March 31, 2025 showed approximately 343 million shares outstanding and 517 million fully diluted, with cash of C$18 million prior to the September financing. Institutional ownership comprises roughly 30% of the shareholder base, with gold-focused funds and approximately 10% held by insiders and advisors, providing alignment between management and external capital. The September 2025 bought-deal offering was upsized to C$41 million, indicating strong institutional demand and providing runway through key operational milestones.

Management's stated goal involves a phased approach: achieve commercial production stability at Madsen by 2026, integrate the Rowan deposit through toll-milling arrangements, and pursue acquisition or development of an additional producing asset to accelerate the path to 100,000-plus ounces annually. This blueprint mirrors successful mid-tier builders in Canada's junior space, where consolidation of proximate high-grade assets within established infrastructure corridors generates operating leverage and capital efficiency.

Key Development: Madsen Ramp-Up & Rowan Economics

The Madsen Mine restart represents the company's primary near-term catalyst. Production from January through July 2025 totaled 9,550 ounces, with the mill processing at an average rate of 650 tonnes per day while achieving 95% metallurgical recovery. Throughput trials reaching 800 tonnes per day validate the mill's nameplate capacity, and the company has installed carbon-in-residue recovery equipment to optimize extraction. A critical bulk sample delivered 2,664 ounces against a predicted 2,771 ounces, representing 96% reconciliation and confirming grade control protocols.

The January 2025 pre-feasibility study outlined economics based on a six-year mine life producing 67,600 ounces annually at an average grade of 8.2 grams per tonne. The study projected a net present value of C$496 million (post-tax, 5% discount rate) and all-in sustaining costs of $1,681 per ounce, with average annual free cash flow of approximately C$94 million. Importantly, these metrics assumed a gold price well below current spot levels, suggesting meaningful upside to project economics as realized prices trend above model assumptions. Ongoing definition drilling 150,000 meters completed to date aims to tighten drill spacing to seven meters, enhancing grade confidence and mine planning flexibility.

The Rowan Project, located on the same property complex, advanced to preliminary economic assessment stage in August 2025. The study contemplated toll-milling ore through third-party facilities, eliminating the need for capital-intensive mill construction. Indicated resources total 196,700 ounces at 12.8 grams per tonne, with an additional 118,200 ounces in the inferred category at 8.7 grams per tonne. The PEA outlined $70 million in initial capital, 35,200 ounces per year over five years, a 42% internal rate of return, and $125 million net present value on a post-tax basis. Management plans to complete a combined Madsen-Rowan pre-feasibility study in 2026, with potential production integration targeted for 2028-2029.

Strategic Significance: $4,000 Gold & High-Grade Leverage

For high-grade producers like West Red Lake Gold, the price environment creates asymmetric optionality. The Madsen pre-feasibility study assumed an all-in sustaining cost of $1,681 per ounce, implying operating margins exceeding $2,300 per ounce at current spot prices a 137% margin over cash costs. High-grade operations benefit disproportionately from price increases because fixed costs represent a smaller percentage of total expenses per ounce produced, amplifying free cash flow generation. Additionally, higher gold prices often permit mining of lower-grade zones or smaller stopes previously deemed uneconomic, effectively expanding reserve bases and extending mine lives.

The macro drivers underpinning gold's rally fiscal uncertainty, geopolitical risk, currency debasement concerns typically persist over multi-year cycles rather than reverting quickly. India's Multi-Commodity Exchange saw gold futures for December 2025 delivery rise 0.72% to ₹121,120 per 10 grams from ₹120,249, reflecting parallel safe-haven demand in one of the world's largest physical gold markets. For investors seeking exposure to this theme, producers with near-term production growth, jurisdictional stability, and high-grade ore bodies offer leveraged participation compared to holding physical bullion or large-cap miners with diversified asset portfolios.

Current Activities: Exploration & Resource Expansion

Beyond Madsen and Rowan, West Red Lake Gold maintains an active exploration pipeline targeting resource additions and satellite deposit development. The Fork deposit, situated 250 meters from existing infrastructure, hosts a high-grade core with an estimated 33,000 to 43,000 ounces at grades between 8 and 9 grams per tonne. Its proximity to underground access and surface facilities positions Fork as a potential early-stage production contributor requiring minimal incremental capital for development.

The Upper 8 discovery generated investor attention with 15 of 17 drill holes intersecting gold mineralization, including a standout intercept of 1.3 meters grading 44.17 grams per tonne. Geological interpretation suggests stacked lenses of mineralization, a structural characteristic common to high-grade vein systems in the Red Lake camp. Successful delineation of continuous mineralization across multiple levels could establish Upper 8 as a standalone mining horizon or amalgamated with nearby zones to optimize development sequencing and dilution management.

Recent drilling in the lower Austin Zone has reinforced management's confidence in resource expansion potential. Shane Williams, President and CEO of West Red Lake Gold, stated:

"We are already being rewarded with very high-grade, broad intercepts of gold mineralization. There is significant ounce and tonnage potential remaining at depth in the Madsen orebody."

Williams, who leads the company's strategy to transition Madsen from restart to commercial production, brings experience in developing distressed mining assets in the Red Lake district. The company's systematic approach to drilling including intercepts of 139.45 grams per tonne over 7.8 meters and 74.70 grams per tonne over 8.7 meters validates the exploration thesis and supports the goal of exceeding 100,000 ounces annual production by 2029.

Investor Takeaway: Positioning for Mid-Tier Transition

West Red Lake Gold occupies the inflection point between operational restart and scalable production growth, a phase characterized by elevated execution risk but also asymmetric return potential. The company's September 2025 financing addressed near-term capital needs, providing an estimated 18-24 month runway to achieve commercial production at Madsen while advancing Rowan permitting and pre-feasibility work. With gold prices establishing a new trading range above $4,000 per ounce, the pricing assumptions underpinning both the Madsen and Rowan economic studies appear conservative, suggesting meaningful upside to published net present values.

The Red Lake camp's endowment and infrastructure density differentiate it from greenfield projects requiring hundreds of millions in upfront capital for mills, tailings facilities, and power distribution. West Red Lake's acquisition strategy purchasing distressed assets with existing infrastructure mirrors successful value-creation models deployed by mid-tier producers like Alamos Gold and SSR Mining in their formative years. The company's stated ambition to acquire or develop an additional producing asset aligns with this blueprint, offering investors exposure to potential M&A upside as consolidation activity intensifies in response to higher gold prices.

Risk factors warrant consideration, including operational challenges inherent in underground mining, permitting timelines for Rowan development, and the company's reliance on external financing or debt facilities to fund capital programs beyond current cash reserves. The C$496 million Madsen NPV implies a valuation disconnect relative to the company's approximate C$300 million market capitalization prior to the September financing, though investors typically apply discounts to pre-production and ramp-phase assets pending demonstration of sustained cash generation. Monitoring quarterly production metrics, cost performance, and progress toward the 2026 Madsen-Rowan combined study will provide signals regarding execution risk and rerating catalysts.

The Investment Thesis for West Red Lake Gold

- High-grade producers with sub-$1,700 AISC capture 120%+ margins, supporting share price rerating as cash flow visibility improves.

- Operational stability de-risks the investment case and triggers institutional re-evaluation of reserve life and NPV assumptions.

- Companies bridging the gap from single-asset juniors to multi-mine platforms historically achieve valuation premiums as corporate risk declines.

- Combined studies quantifying synergies between Madsen and Rowan will clarify optimal development sequencing and financing requirements.

- Drill success expanding reserves beyond current PFS estimates reduces replacement costs and extends cash flow duration.

- Relative valuation gaps versus producers with similar grades and jurisdictional risk profiles may signal entry points or exit timing.

West Red Lake Gold's investment case rests on the convergence of favorable gold pricing, operational momentum at Madsen, and near-term development optionality at Rowan. The company produced 9,550 ounces in the first seven months of 2025, validating restart execution while establishing a baseline for production scaling. The Rowan PEA's 42% IRR and $125 million NPV offer visible growth beyond Madsen's current capacity, supporting management's target of exceeding 100,000 ounces annually by 2029. With gold futures establishing new highs above $4,000 per ounce driven by macroeconomic uncertainty and safe-haven demand, high-grade producers in tier-one jurisdictions benefit from operating leverage that amplifies free cash flow generation.

For investors seeking exposure to gold's rally through junior producers, West Red Lake Gold presents a leveraged play on both metal prices and operational execution. The company's C$41 million September financing provides adequate runway to de-risk the Madsen ramp-up and advance Rowan toward production, while exploration success at Fork, Upper 8, and the Austin Zone offers potential resource expansion beyond current studies. The valuation gap between published NPVs and market capitalization suggests upside potential contingent on achieving commercial production milestones and sustaining throughput above 650 tonnes per day. Investors should balance this opportunity against execution risks inherent in underground mining ramp-ups and the company's need for continued capital access to fund growth initiatives.

TL;DR

West Red Lake Gold restarted the Madsen Mine in 2025, producing 9,550 ounces through July while ramping toward 67,600 ounces annually. A C$41 million September financing funds operations through key milestones, including the 2026 Madsen-Rowan combined pre-feasibility study. The Rowan PEA shows $125 million NPV and 42% IRR based on toll-milling 35,200 ounces yearly. With gold above $4,000 per ounce and AISC projected at $1,681, margins exceed 130%, driving cash flow leverage. Management targets greater than 100,000 ounces per year by 2029 across multiple deposits. Exploration at Fork, Upper 8, and Austin Zone offers resource expansion potential in Canada's proven Red Lake camp.

FAQs (AI-Generated)

The company produced 9,550 ounces from January through July 2025, with mill throughput averaging 650 tonnes per day at 95% recovery.

Rowan's PEA contemplates toll-milling 35,200 ounces annually over five years with $70 million capex, avoiding mill construction costs and generating 42% IRR.

Higher gold prices amplify margins for high-grade producers, with West Red Lake's projected $1,681 AISC implying 130%+ margins at current spot levels.

Management targets exceeding 100,000 ounces per year by 2029 through integration of Madsen, Rowan, and potential additional producing assets.

Execution risks include ramp-up consistency at Madsen, permitting timelines for Rowan, ongoing capital requirements, and operational challenges inherent in underground mining.

Analyst's Notes

Subscribe to Our Channel

Stay Informed