What the Term Sheet Terms & M&A Signals Say About CK Gold's Market Value

US Gold Corp received indicative financing terms with equity at premiums to market, as strategic interest in the CK Gold Project begins to emerge.

- Indicative term sheets received over the prior 18 months include structures with up to 80% debt and 20% equity, with the equity priced at premiums to market, suggesting counterparties see value in the CK Gold Project that is not fully reflected in the current market price.

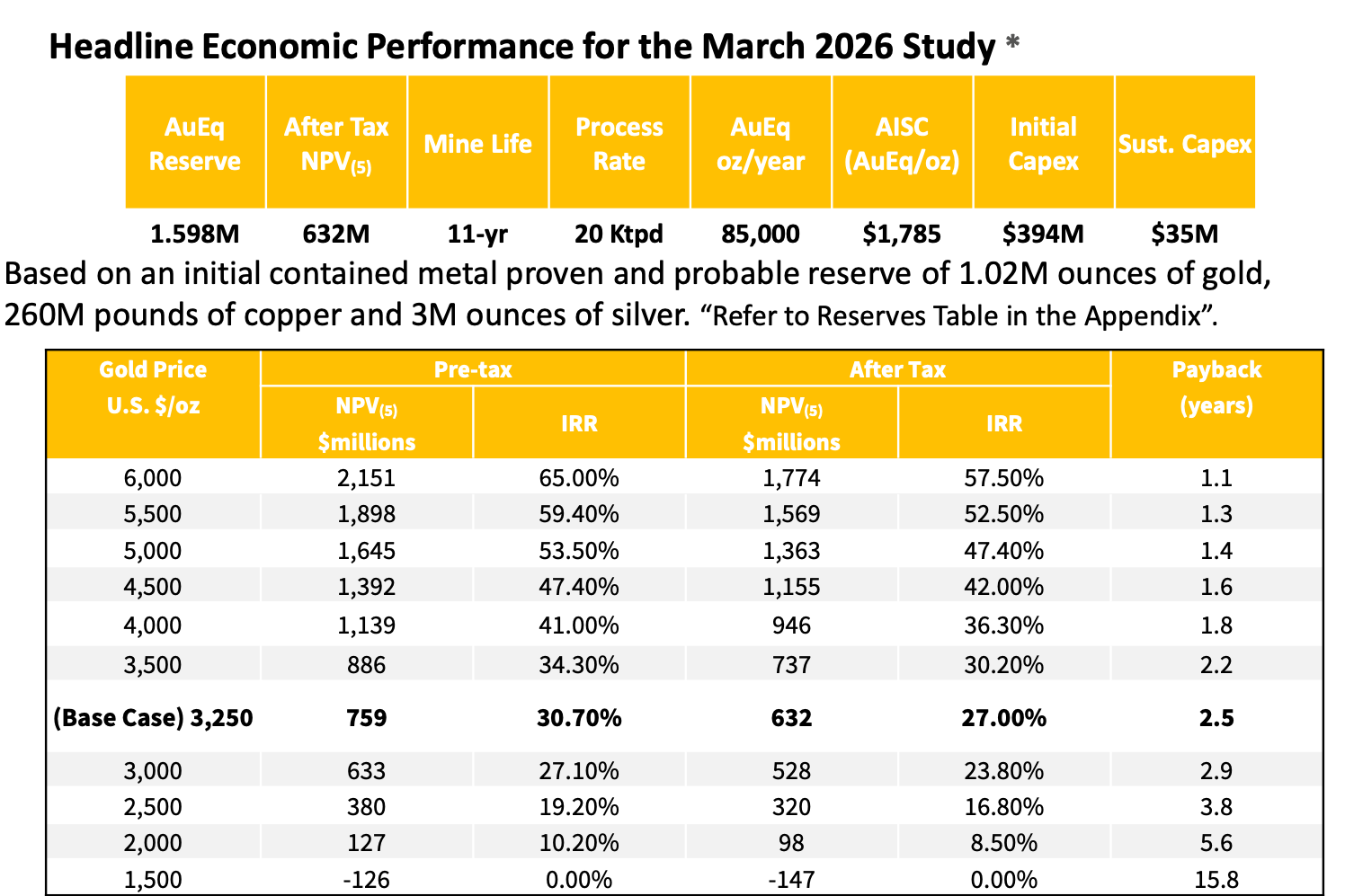

- The March 2026 Feasibility Study (FS) establishes a base case after-tax net present value (NPV) of $632 million at $3,250 per ounce gold, but management has identified approximately 900,000 gold equivalent ounces of resource outside the production schedule that an acquirer would price as a low-incremental-capital option within the existing $394 million infrastructure.

- CK Gold sits on Wyoming state land with no federal involvement, making its full permit suite irrevocable under Wyoming state law and materially reducing the post-award challenge risk that institutional capital explicitly prices as a discount in projects on federal land.

- The project produces a clean, high-quality gold-copper concentrate for which smelters are currently paying premiums, creating competitive tension among offtakers that management characterises as an additional commercial advantage not reflected in the base case economics.

- US Gold Corp. has confirmed that a positive FS at this project scale and the permitting status are attracting strategic interest, with potential acquirers beginning to evaluate the project following the FS release.

What Has Happened

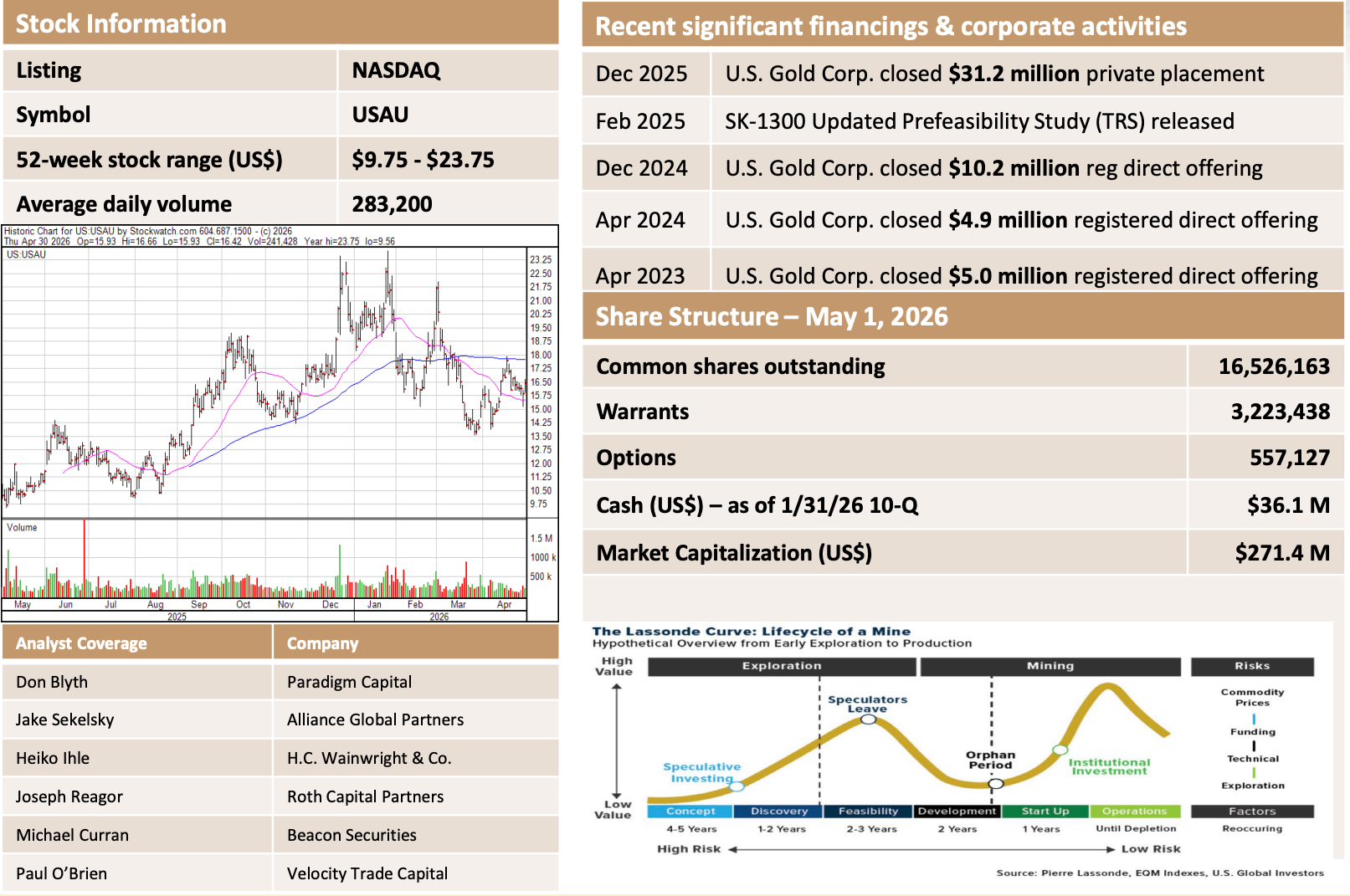

US Gold Corp (NASDAQ: USAU) released its Feasibility Study for the CK Gold Project on March 2026, establishing a base case after-tax net present value (NPV) of $632 million at $3,250 per ounce gold with an after-tax internal rate of return (IRR) of 27% and a 2.5-year payback period. US Gold Corp. simultaneously disclosed that indicative financing term sheets received over the prior 18 months include equity components priced at premiums to the company's market price - a structural signal that counterparties see value not fully reflected in the current share price. Chairman of US Gold Corp, Luke Norman, confirmed that the combination of a positive feasibility study (FS) and full permitting is attracting strategic interest, with potential acquirers described as beginning to evaluate the project. With term sheets pricing equity at a premium, the market focus shifts to how institutional capital and potential acquirers are currently valuing CK Gold's base case and expansion opportunities.

What the Equity Premium Signal Actually Means

Indicative term sheets are not binding commitments, but their structure is analytically useful. When counterparties propose equity components at premiums to market price, they are actively pricing the project above current market levels.

Norman described the financing environment:

"There's a lot of money out there right now chasing mining opportunities with. Not a lot of projects like ours that are shovel-ready, ready to go, so it's not a huge capex, that $400 million is a sweet spot."

The $394 million initial capital sits in a bracket that management explicitly contrasts with billion-dollar builds. This capital scale attracts a broad pool of project finance counterparties, which the company confirms includes offtakers, streaming companies, and equipment providers offering vendor financing. The competitive tension among those counterparties is what management describes as potentially driving more favourable pricing and timing on the project finance. The 80% debt structure cited by management reflects indicative terms received before the FS release. The FS removes a layer of technical uncertainty that typically constrains the appetite for project finance.

The Acquirer's Math: Buying Options That Are Not in the Base Case

From a strategic acquirer's perspective, the $632 million base case NPV is the floor, not the price. An acquirer evaluating CK Gold would be pricing three specific options that are excluded from the FS but quantifiable against the existing capital structure. The first is recovery improvement. The FS establishes a life-of-mine gold recovery of 71.5% through a flotation circuit, with approximately 300,000 ounces of gold reporting to fully lined tailings. Test work indicates that adding a CIL circuit or an alternative non-cyanide recovery method could increase recovery toward 95%, potentially adding approximately 250,000 ounces of payable gold from the current mine plan. Management noted they are actively exploring non-cyanide, reusable iodine alternatives as well as standard CIL, and deliberately kept these options out of the FS to avoid pricing in unoptimised technology at the feasibility stage. The second is resource conversion. Approximately 900,000 ounces of gold equivalent of measured and indicated resources are within the resource pit shell but outside the production schedule.

Norman described the capital logic directly:

“You double your NPV almost just with another million ounces in the reserve because your capex is already covered, the definitive feasibility doesn't change, you just have a larger reserve to go after."

The observation reflects the leverage that reserve expansion generates once major infrastructure capital is already committed, rather than a formal economic projection. The third is aggregate monetisation: approximately 40 million tons of granodiorite surface rock unvalued in the FS, with named offtake interest from a nearby railroad and an approach from Burlington Northern Santa Fe. An acquirer consolidating these options against the already-modelled $394 million initial capital sees a materially different risk-adjusted proposition than the base-case NPV, providing context for why recent indicative term sheets have priced equity at a premium to the current market.

The Permitting Premium in an M&A Context

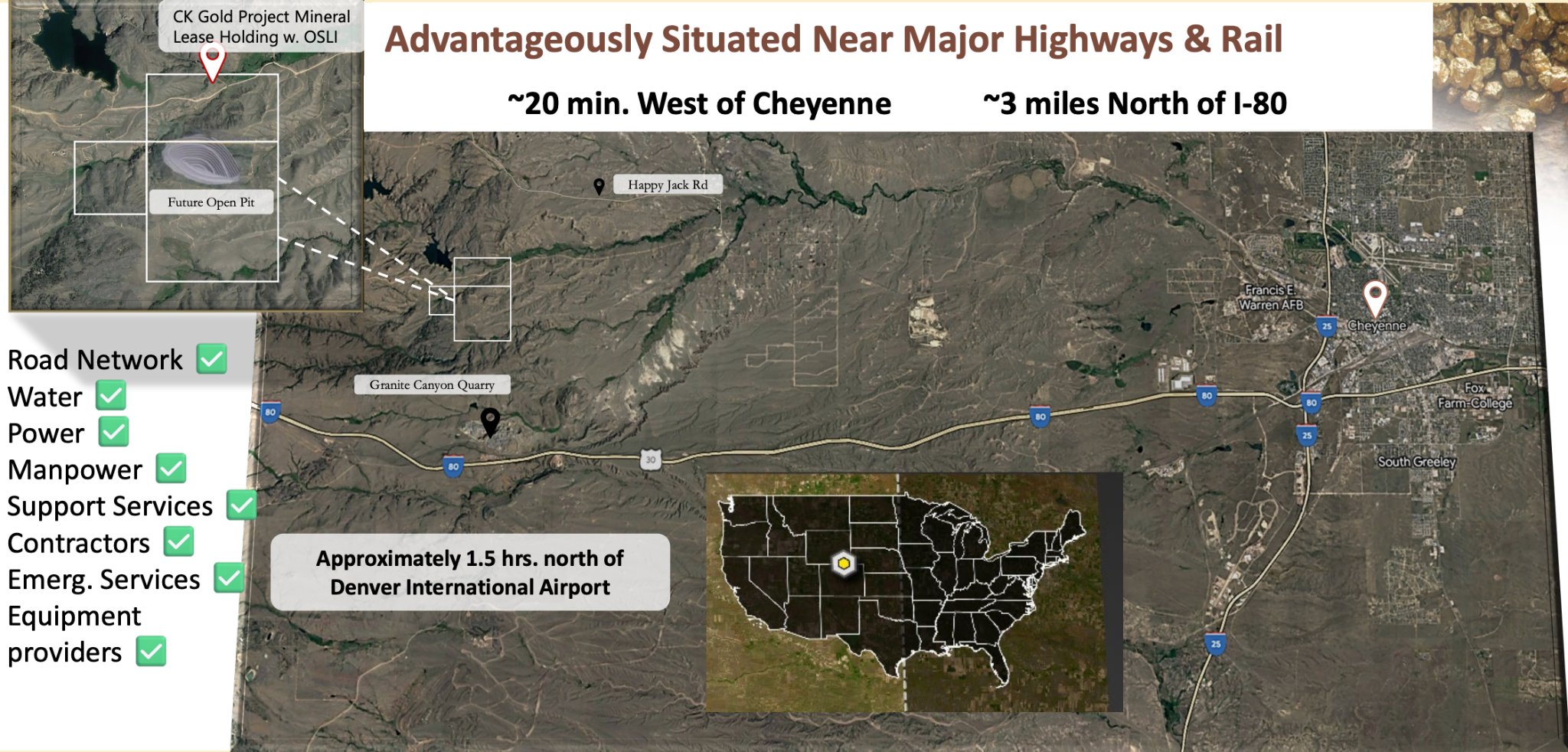

Institutional capital acutely prices the risk of federal permitting exposure, where late-stage challenges can stall projects and strand capital. Norman drew on direct banking experience to highlight this, noting he had seen projects held up for a year by sudden federal permit requirements, forcing money to be returned to investors. Because CK Gold is on Wyoming state land with no direct federal involvement, its permits are not reversible or revocable once awarded - a structural certainty that Norman noted decreases the cost of capital and makes it easier for financiers to avoid assigning large risk premiums to the project.

The construction of the mine access road, initiated in January 2026, further advances this de-risking. As Norman pointed out, starting the entry road officially triggered the company's permit-to-mine by proxy. For an acquirer, the project is not merely permitted on paper but is actively advancing under a mining permit right now.

Concentrate Quality & Offtake Competitive Tension

The CK Gold Project produces a clean, high-quality gold-copper concentrate with low sulfide content and minimal deleterious elements - and the market for that concentrate is already being priced before the mine is built. Offtake and streaming counterparties have been among those submitting indicative term sheets.

Norman noted that the company deliberately chose not to price the smelter premium for this material into the FS because the company did not want to factor that in or ever want to price in the fact that there's such competitive tension out there for these high-quality concentrates. This concentrated quality functions as a built-in commercial advantage. Because off-takers and streamers are already among the parties submitting term sheets, an acquirer entering the asset is inheriting active competitive pressure that management intentionally excluded from the base-case FS.

Broader Context

The M&A environment for permitted, construction-ready gold projects has tightened considerably as gold has traded well above the base case $3,250 per ounce. CK Gold sits in this exact window of scarcity with a specific structural advantage: its $394 million initial capital makes it a "sweet spot" that does not strictly require a major producer's balance sheet to finance, meaning the universe of potential acquirers and partners extends beyond the senior gold companies typically associated with large project transactions.

Norman acknowledged the M&A dynamic directly:

"Clearly, the hawks start circling, they're looking. There are companies interested in M&A activity or pure takeouts on the project."

The company's stated action plan is to finalise project financing and initiate development, but the acknowledgement that strategic interest is live is itself a signal worth tracking.

What to Watch Next

The financing decision expected in 2026 is the primary near-term signal. The structure of any announced financing - the debt-to-equity ratio, whether streaming or offtake arrangements are included, and whether those terms mirror the indicative structures already received - will reveal how institutional counterparties have ultimately priced the project. A financing structure echoing the indicative terms of up to 80% debt or equity priced at a premium to the market would confirm that the signals Norman described have translated into committed capital.

On the M&A front, no transactions have been announced, and the company's stated focus is on advancing development. The aggregate partnership process is a key indicator to watch: established aggregate companies are being sought to partner and monetise the waste rock, and whether that process attracts a party with broader strategic interest in the project is a concrete, disclosed milestone the market can monitor.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed