What You Need to Understand About the Nuclear Sector Before You Invest in Uranium Part - 4

Secondary uranium supply declines as geopolitical risks shift flexible sources to "unspecified" category, forcing utilities toward primary producers in stable jurisdictions.

- Global inventories, recycling, and re-enrichment once masked production deficits, but they are no longer reliable buffers of secondary supply.

- Underfeeding and tails re-enrichment, key flexible sources, have shifted into “unspecified” supply due to the Russia-Ukraine conflict, increasing geopolitical risk.

- Commercial inventories and re-enrichment programs show extreme correlation to uranium prices, creating volatility in marginal supply.

- Stable, jurisdictionally secure projects in Canada, the US, and Namibia are increasingly rewarded by investors for their predictability.

- Companies advancing Tier-1 projects with low All-In Sustaining Costs (AISC) and near-term catalysts, such as In-Situ Recovery (ISR) operators in the US, Athabasca explorers, and African developers, stand to capture premium valuations as predictable secondary supply shrinks.

From Invisible Buffer to Structural Liability

For decades, the uranium market operated with an invisible safety net. Cold War stockpiles, highly enriched uranium (HEU) downblending programs, and opportunistic inventory sales buffered shortfalls in primary mine production. These secondary sources allowed utilities to defer long-term contracts, confident that material would emerge when needed. That era has ended. What once functioned as a predictable surplus has become an unpredictable geopolitical lever, subject to price volatility, jurisdictional risk, and strategic hoarding.

The transition matters because it removes the cushion that masked structural deficits in primary supply. Utilities can no longer assume that secondary material will bridge gaps between reactor demand and mine output. Financial investors, recognizing this shift, have begun accumulating physical uranium as a strategic asset rather than a commodity buffer. The result is a market increasingly dependent on primary production from politically stable jurisdictions, a dynamic that rewards developers advancing projects in Canada, the United States, and Namibia while penalizing reliance on flexible but unpredictable secondary flows.

This structural change forces a fundamental recalibration of investment strategy. Companies with near-term production visibility, low-cost operations, and jurisdictional security are capturing premium valuations. Developers without these attributes face intensified scrutiny. The removal of secondary supply as a reliable backstop means that primary uranium mining has become the only predictable source of material through 2040.

Dissecting Secondary Supply: Specified vs. Unspecified

The distinction between specified and unspecified secondary supply has become central to understanding uranium market dynamics. Specified sources offer transparency and predictability but have declined to marginal contributions. Unspecified sources provide flexibility but have become increasingly contingent on geopolitical considerations that Western utilities cannot incorporate into long-term fuel planning. This bifurcation creates strategic advantages for primary producers in stable jurisdictions.

Specified Sources Losing Ground

Specified secondary supply encompasses predictable, government-declared sources: scheduled HEU downblending, disclosed excess inventories, and defined recycling flows. These contributions, while transparent, have diminished to marginal relevance. Under reference scenarios from the World Nuclear Association, specified sources contribute approximately 5% of global reactor demand through 2040. The United States Department of Energy (DOE) holds 3,194 tonnes uranium (tU) in excess inventory, but this material is tied to domestic defense priorities and strategic reserve considerations, limiting commercial availability.

Major incumbent producers continue to face operational challenges that exacerbate the supply deficit left by declining secondary sources. Denison Mines' Phoenix ISR project advancement occurs against a backdrop of persistent production shortfalls across the industry. President and Chief Executive Officer David Cates characterized the reliability issues affecting established producers:

"We've got Kazatomprom that's had multiple years now of struggles achieving production guidance, and Cameco recently announcing that they'll fall short this year as well."

The Unspecified Category & Market Volatility

Unspecified secondary supply includes underfeeding, tails re-enrichment, and opportunistic inventory sales, flexible sources that respond to price signals but lack contractual visibility. The Russia-Ukraine conflict fundamentally altered this category. Enrichment flows that once provided flexibility to Western utilities shifted into a category marked by uncertainty. Material from Russian sources, while technically available, faces jurisdictional and sanction risks that prevent utilities from relying on these supplies for long-term fuel planning.

This reclassification has forced utilities to reconsider contract strategies. When flexible supply becomes geopolitically contingent, predictability commands a premium. Projects in Saskatchewan's Athabasca Basin, Wyoming's Powder River Basin, and Namibia's Erongo Region have gained strategic value precisely because they offer stability that unspecified sources cannot guarantee. The fundamental uncertainty surrounding supply availability drives utilities toward earlier contracting and jurisdictional diversification. ATHA Energy's exploration program in the Anjikuni Basin represents the scale of discovery required to offset secondary supply decline. Chief Executive Officer Troy Boisjoli emphasized the supply-side risk that necessitates aggressive exploration:

"The vast majority of the risk is on the supply side and there's supply side uncertainty here."

Strategic Inventories & Investor Accumulation

The composition and mobility of global uranium inventories have undergone a fundamental transformation. While headline inventory figures appear substantial, the distinction between strategic holdings and commercially accessible material has become increasingly pronounced. This shift has created scarcity premiums for jurisdictionally secure projects and transformed how investors view physical uranium holdings.

Utility & Sovereign Inventories

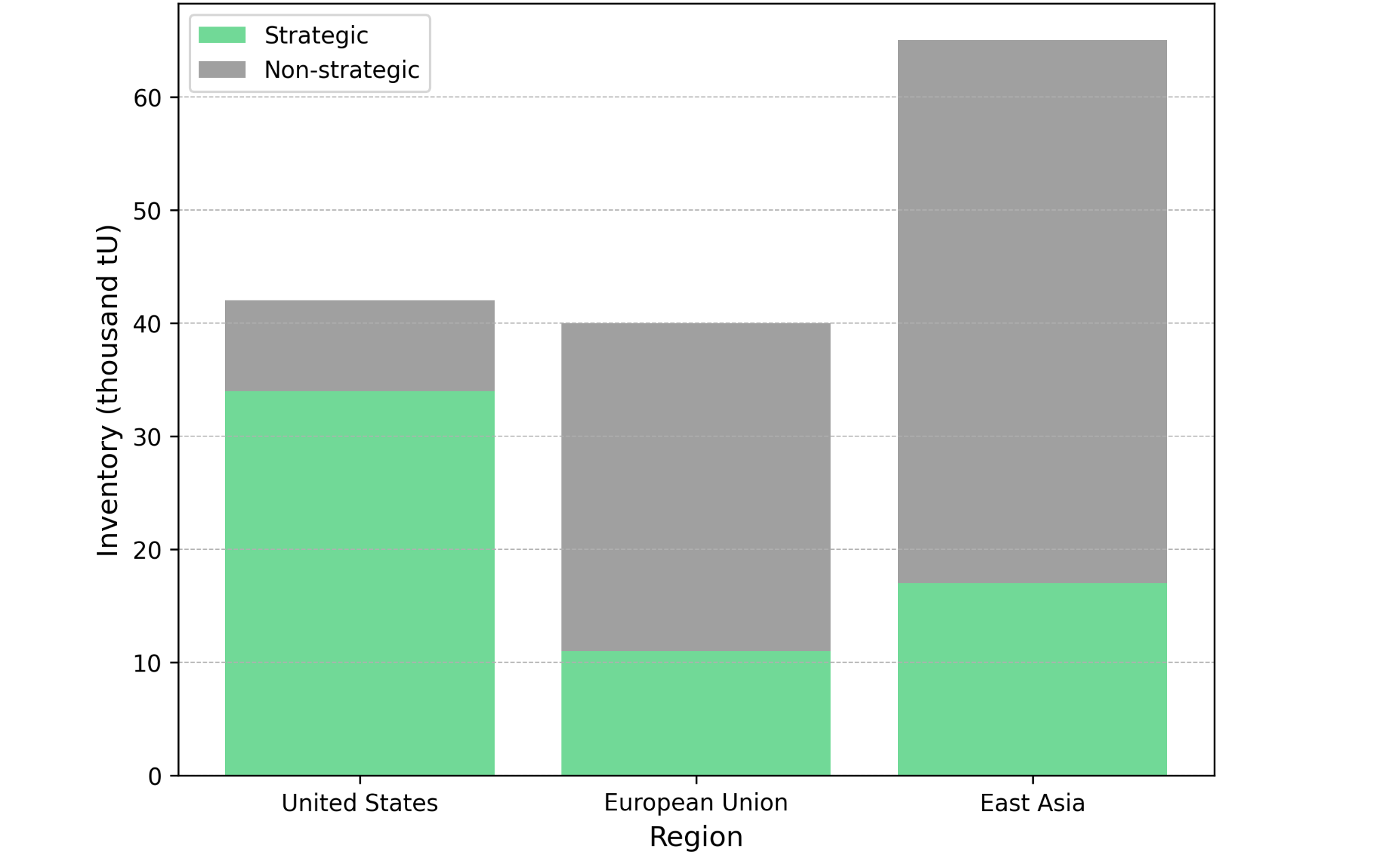

Global utility inventories stood at approximately 147,000 tU in 2024. This figure, while substantial, obscures a critical distinction: the majority of this material is strategically held and not market-mobile. China's estimated inventory of 139,000 tU serves strategic energy security objectives rather than commercial arbitrage. True mobile supply available to Western utilities represents a fraction of the headline number.

The composition of inventory varies significantly by jurisdiction, with the United States maintaining a higher proportion of strategic holdings that are largely immobile, while East Asia, primarily China, accounts for a dominant share of non-strategic material. The European Union exhibits a more balanced inventory structure but remains constrained by policy and infrastructure considerations.

This disparity between reported inventories and accessible material creates a scarcity premium for jurisdictionally secure supply. Large-scale projects in stable jurisdictions face less competition from locked strategic stockpiles, improving their positioning in utility procurement processes.

The United States faces a particularly acute uranium supply challenge that creates strategic vulnerabilities and investment opportunities. Domestic reactor demand far exceeds indigenous production capacity, forcing reliance on imports even as geopolitical tensions restrict traditional supply sources. Global Atomic's Dasa project in Niger, despite jurisdictional complexities, has secured substantial US utility offtake precisely because it addresses this supply imbalance. The project's scale positions it as a meaningful contributor to closing the domestic supply gap. President and Chief Executive Officer Stephen Roman quantified the strategic alignment with US utilities.

"We are primarily supplying US utilities and they're probably taking 90% of our offtake contracts at the moment. This is strategic. Our mine will produce as much as every uranium mine combined in the US."

Traders & Financial Investors

Financial players including Sprott Physical Uranium Trust and Yellow Cake plc have fundamentally altered inventory dynamics by shifting U3O8 into storage. US trader and financial inventories grew to approximately 13,000 tU by 2023, reflecting price-driven accumulation rather than commercial consumption hedging. This shift transforms inventories from countercyclical buffers into procyclical assets that behave like exchange-traded funds.

When inventories move with prices rather than against them, their stabilizing function disappears. Rising spot prices trigger holding behavior among financial participants, reducing liquidity precisely when utilities seek incremental supply. Conversely, price declines prompt financial selling, amplifying downward volatility. This procyclical behavior removes inventory from its traditional role as a market stabilizer and increases dependence on primary production to meet demand.

Recycling, Tails & the Limits of Flexibility

The theoretical capacity of recycling and tails re-enrichment to supplement primary supply faces economic, technical, and political constraints that limit scalability. While these pathways represent genuine sources of uranium equivalent, their mobilization depends on price thresholds, geopolitical access, and infrastructure availability that cannot be assumed in long-term planning. This gap between theoretical and practical supply reinforces the strategic value of conventional primary production.

Underfeeding & Tails Re-Enrichment

Global stockpiles of depleted uranium hexafluoride (DUF6) tails total approximately 2 million tonnes. Re-enrichment of these tails offers a theoretical supply source, but economic viability requires elevated spot prices. Russia holds approximately 913,000 tonnes, equivalent to roughly 41,000 tU, but geopolitical uncertainty restricts mobility of this material to Western markets.

The DOE-Global Laser Enrichment (GLE) project, involving 200,000 tonnes of DUF6, represents potential domestic re-enrichment capacity but remains uncommercial until after 2030. This timeline gap creates a strategic opening for ISR operators capable of delivering low-cost production before government-backed re-enrichment facilities come online. The cost structure of ISR production becomes critical when evaluating which sources can bridge the supply gap economically. Ur-Energy's Lost Creek operation demonstrates production economics that provide reliable baseline supply resistant to commodity price volatility. President Matthew Gili outlined the facility's competitive cost position.

"In the second quarter we produced uranium for $42 cash cost per pound at Lost Creek."

ISR operations benefit from operational flexibility that allows rapid scaling when market conditions warrant expansion. enCore Energy's acceleration of drilling activity illustrates how producers can respond to supply tightness through operational intensity rather than waiting for new projects to reach production. The company's drilling efficiency improvements demonstrate the operational leverage available to established ISR platforms. Executive Chairman William Sheriff quantified the productivity gains achieved through operational optimization:

"Our production rate on a daily basis has gone, depending on what time frame you're measuring it against, from up 200% to up 300%... We went from roughly a little over seven days average into just about 1.3 now."

Reprocessing (RepU, MOX)

Approximately 140,000 tonnes of reprocessed uranium (RepU) inventory exists globally. Mixed oxide (MOX) fuel provides another pathway, with one tonne of plutonium displacing approximately 75 tonnes of U3O8 equivalent. Global nameplate MOX capacity reaches approximately 2,000 tonnes per year, concentrated in France, Japan, and Russia. However, environmental, social, and governance (ESG) opposition and political constraints limit MOX expansion outside Asia and Europe.

Reprocessing faces technical, economic, and political limitations that prevent it from scaling as a primary supply alternative. Utilities in markets with strong environmental advocacy face community opposition to plutonium-based fuel cycles. Capital requirements for reprocessing facilities exceed those for conventional enrichment, and fuel fabrication costs for MOX remain elevated relative to fresh fuel. These constraints ensure that reprocessing serves as a supplementary source rather than a scalable replacement for primary supply.

The Market Consequence: Why Primary Supply Is the Only Predictable Source

The convergence of declining specified sources, geopolitically constrained flexible supply, and financialized inventory behavior creates a structural deficit that can only be addressed through primary mine production. Utilities have recognized this reality and adjusted contracting strategies accordingly. The market is repricing assets based on jurisdictional security, execution capability, and production timelines that align with near-term demand growth.

Secondary Deficit Through 2040

Specified secondary supply contributes approximately 5% of demand through 2040 under reference scenarios from the World Nuclear Association. Flexible sources exhibit high price sensitivity and geopolitical risk. The net effect is a structural deficit increasingly borne by primary supply. Utilities recognize this reality and have begun signing long-term contracts earlier in the development cycle, locking in Tier-1 developers before production begins.

The temporal dynamics of mine development create strategic value for projects that maintain optionality through extended market cycles. High-grade resources in proven geological environments can afford patient development timelines that align production with peak demand rather than forcing capital deployment during unfavorable market conditions. IsoEnergy's Hurricane deposit in Saskatchewan's Athabasca Basin represents the type of asset where geological quality provides strategic flexibility. Director and Chief Executive Officer Philip Williams articulated the advantage of holding Tier-1 assets through supply tightening cycles:

"Ultimately we have one of the marquee world class assets in our portfolio, the Hurricane deposit of Larocque East… The crunch in the basin is coming, and every day or month, mines are being depleted… We think it's more valuable the longer we hold on to it."

District-scale exploration success in established basins creates pipeline optionality that addresses long-term supply concerns beyond the current development queue. ATHA Energy's multiple discoveries within the Anjikuni Basin demonstrate the geological continuity required to support multi-decade supply commitments. Chief Executive Officer Troy Boisjoli described the strategic rationale for demonstrating district-scale potential.

"The reason was to be able to demonstrate what we saw in the data, which was the district scale or camp scale potential."

Investors Shift to Secure Jurisdictions

Premium pricing has emerged for projects in Saskatchewan, Wyoming, and Namibia compared to politically volatile jurisdictions or regions dependent on Russian enrichment capacity. Utilities are signing contracts earlier and locking in developers with jurisdictional advantages. This shift creates a bifurcated market where Tier-1 assets command valuations reflecting scarcity premiums while projects in uncertain jurisdictions face discounts regardless of resource quality.

US policy restrictions on Russian uranium imports have accelerated domestic consolidation as companies seek scale advantages in permitting, infrastructure access, and operational efficiency. Premier American Uranium's acquisition strategy focuses on building portfolios adjacent to existing production facilities, reducing infrastructure capital expenditures and permitting timelines. The consolidation imperative reflects industry recognition that fragmented junior developers cannot individually achieve the scale required to meaningfully offset secondary supply decline. The company's strategic focus emphasizes the structural inefficiencies that consolidation addresses.

Capital efficiency in greenfield development requires infrastructure advantages that reduce the proportion of capital allocated to non-productive assets. Bannerman Energy's Etango project benefits from existing regional infrastructure that lowers total development costs relative to comparable African projects. Chief Executive Officer Gavin Chamberlain quantified the capital advantage provided by infrastructure access.

"Our capital cost portion of infrastructure is less than 10%. An average project anywhere else in Africa is going to be between 40% and 50%, so the fact that we don't spend that extra 30% or 40% on the capital cost is a massive advantage to us."

High-grade deposits provide natural hedges against cost inflation that affects all primary production but particularly impacts marginal supply sources. Energy Fuels' Pinyon Plain mine in Arizona demonstrates how grade advantages translate into operational resilience during periods of input cost volatility. President and Chief Executive Officer Mark Chalmers emphasized grade as a strategic defense against inflationary pressures.

"The best ways to combat that was with higher grade, and that's what we're seeing at the Pinyon Plain."

The Investment Thesis for Uranium

The structural decline of secondary supply and the geopolitical reclassification of flexible sources create a multi-year investment opportunity in primary uranium producers. Companies advancing projects with jurisdictional security, low-cost structures, and near-term production visibility are positioned to capture scarcity premiums as utilities lock in long-term contracts.

- Operational producers capture disproportionate value during supply-constrained markets when spot prices rise faster than contract prices, rewarding companies with uncommitted production capacity positioned to sell into strengthening markets.

- ISR operators in Wyoming and Texas positioned in the bottom quartile of the global cost curve relative to volatile secondary supply mobilization costs, delivering production before DOE-GLE re-enrichment capacity becomes commercial.

- US policy restrictions on Russian imports drive strategic value for domestic producers with permitted capacity and operational momentum, creating a supply gap that cannot be filled by secondary sources and establishing jurisdictional premiums for domestic assets.

- High-grade Athabasca exploration projects with district-scale potential represent future cycle upside as secondary supply fades and utilities extend contracting horizons to secure fuel for reactors planned beyond 2030.

- Infrastructure advantages in established mining jurisdictions reduce capital intensity and execution risk for greenfield developments, enabling faster construction timelines and lower breakeven costs relative to projects requiring greenfield infrastructure investment.

A Market Repriced Around Primary Mining

The invisible buffer of secondary supply has become unreliable. Inventories have shifted from mobile commercial stock to strategic reserves. Re-enrichment capacity remains constrained by economics and geopolitics. Recycling faces technical and political limitations that prevent scalability. Investors must now view primary uranium miners as the central lever of supply stability through 2040.

The structural deficit guaranteed by these dynamics ensures a sustained rerating of Tier-1 assets and a scarcity premium across the cost curve. Companies with jurisdictional security, execution capability, and near-term production catalysts are positioned to capture valuations reflecting their role as the only predictable source of uranium supply in a market where secondary buffers have disappeared. The transition from invisible buffer to structural liability marks a fundamental shift in uranium market dynamics, one that rewards primary production and penalizes dependence on sources that can no longer be relied upon.

Click here for Part 3 - Nuclear Fuel Demand

TL;DR

Secondary uranium supply sources that historically buffered production deficits, Cold War stockpiles, HEU downblending, commercial inventories, and tails re-enrichment have become unreliable due to geopolitical reclassification, strategic hoarding, and price sensitivity. China holds 139,000 tU strategically, removing it from commercial markets. Russia-Ukraine conflict shifted flexible enrichment sources into uncertain "unspecified" categories. Specified secondary supply contributes only 5% of demand through 2040. Financial investors transformed inventories from countercyclical buffers into procyclical assets. DOE-GLE re-enrichment remains uncommercial until after 2030. This structural deficit forces utilities toward long-term contracts with primary producers in Saskatchewan, Wyoming, and Namibia, creating scarcity premiums for jurisdictionally secure, low-cost projects with near-term production timelines. Primary mining has become the only predictable uranium source through 2040.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed