Why Gold Is Protecting Investors from World Turmoil & Uncertainty

Gold companies adapt to severe supply constraints amid record prices, with development-ready assets commanding premium value in an accelerating M&A environment.

- Despite record gold prices, the industry faces a severe shortage of new projects entering the production pipeline, with few mines expected to come online before 2030.

- Truly development-ready gold assets are increasingly rare and valuable, creating potential for premium valuations for advanced projects.

- Traditional equity and debt financing has been largely replaced by innovative approaches including royalties, streaming, and phased, self-funded development strategies.

- Leading developers are prioritizing operational efficiency and high margins over scale, with a focus on "grade over tonnage" and simplified mining methods.

- Major producers facing reserve depletion are increasingly looking to acquisitions, positioning advanced developers as potential takeover targets.

- Companies with specialized knowledge in specific regions (Canada, West Africa, South America) are leveraging this expertise as a competitive advantage.

- A new generation of gold companies is redefining success through disciplined capital allocation, cash-flow-first approaches, and stakeholder engagement.

The gold market stands at a historic inflection point. With prices reaching all-time highs against a backdrop of severely constrained supply, investors face a rare opportunity in the gold equity space. The structural disconnect between robust demand and a barren project pipeline has created the perfect conditions for select gold companies to deliver exceptional shareholder returns.

This unprecedented supply-demand imbalance is reshaping the industry landscape. Major producers face depleting reserves with few new projects coming online before 2030, creating both pricing power for existing producers and premium valuations for development-ready assets. Companies with permitted, construction-ready projects represent increasingly valuable assets in a sector where "the cupboard is getting bare," positioning them as potential acquisition targets as M&A activity accelerates. As majors struggle to replace reserves, investors in these advanced developers may benefit from significant takeover premiums.

Simultaneously, a new generation of developers is demonstrating how focused, margin-driven operations can deliver exceptional returns—some exceeding 250% IRR—even at modest production scales. These companies are pioneering creative funding approaches that reduce dilution and accelerate pathways to production, allowing investors to participate in growth stories without the excessive share count inflation that plagued previous cycles. The most attractive opportunities lie with companies that combine development-ready assets, clear paths to production, and disciplined management teams focused on cash flow generation rather than ounce growth at any cost. These new industry leaders are poised not just to benefit from higher gold prices but to fundamentally reshape how gold mining creates and distributes value in a resource-constrained world.

For investors seeking inflation protection with growth potential, the gold sector's structural supply constraints make this a uniquely favorable moment to consider selective exposure to gold equities. With record prices and few new mines on the horizon, the companies addressing the supply gap today may deliver tomorrow's exceptional returns.

The Supply Squeeze: A Barren Project Pipeline

The gold industry is witnessing an unprecedented disconnect between price signals and supply response. While historical commodity cycles typically see production surge following price increases, the current gold bull market has revealed structural challenges that have fundamentally altered this relationship. After years of underinvestment in exploration and development, compounded by increasingly complex permitting processes and rising technical challenges at depth, the pipeline of new gold projects has contracted dramatically.

This supply crunch has created a scenario where even record gold prices—which would traditionally trigger a wave of new development—have failed to generate a meaningful supply response. Majors and mid-tiers alike find themselves competing for a shrinking pool of quality assets at the very moment when their existing operations face grade declines and reserve depletion. The timing couldn't be more critical: many of the industry's cornerstone operations are approaching the end of their productive lives, with few substantial replacements on the horizon.

Dan Wilton of First Mining Gold puts it bluntly:

"If you're not finishing up an environmental assessment in the next 12 months in Canada, you're probably not pouring gold before 2030."

This stark assessment highlights the severity of the supply constraints facing the industry.

The current situation is historically anomalous. Typically, rising commodity prices trigger a wave of new project developments. Yet today's gold market presents a different picture. As Justin Reid of Troilus Gold observes: "You look at all the mergers of equals—same ounces, different ownership."

The industry is reshuffling existing assets rather than bringing new supply online.

This supply conundrum is amplified by Shane Williams of West Red Lake Gold Mines, who notes that "there are very few projects moving into production in 2025—that's key with the gold price as it is today." The industry is witnessing a perfect storm: demand is robust, prices are strong, yet the project pipeline remains worryingly bare.

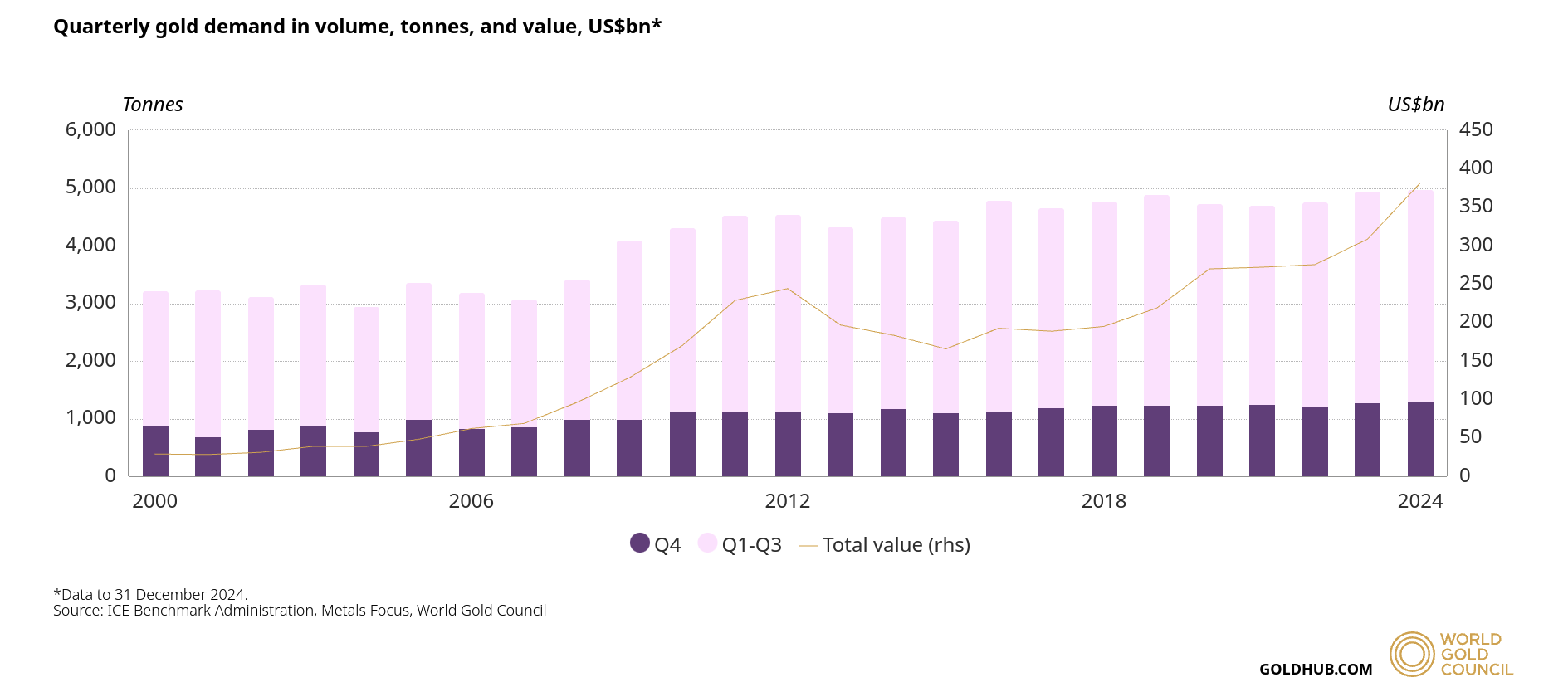

The above chart illustrates growing demand in both tonnage and value terms, especially a sharp increase in 2024. But what has caused this supply situation? A confluence of factors including:

- The prolonged bear market of the 2010s, which decimated exploration budgets

- Rising technical challenges as easily accessible deposits become scarce

- Increasingly complex permitting processes across major mining jurisdictions

- A shift in industry focus from growth to shareholder returns

Simon Marcotte of Northern Superior Resources highlights the scarcity of substantial undeveloped gold camps: "If you know of another camp of this size that is not currently either owned or controlled by one of the senior gold producers globally, let me know because I can't think of one." His statement underscores not just the lack of new discoveries but also how quickly major producers are moving to secure what little remains.

Scarcity Premium: The Value of Development-Ready Assets

As the reality of constrained supply takes hold, a new dynamic is emerging: development-ready gold projects are commanding increasing attention and, potentially, premium valuations. First Mining Gold's Wilton has observed this shift, noting that "the cupboard is getting bare" and that "scarcity value is starting to get recognized."

This scarcity premium is perhaps most evident in the disconnect between intrinsic value and market capitalization for many advanced-stage gold developers.

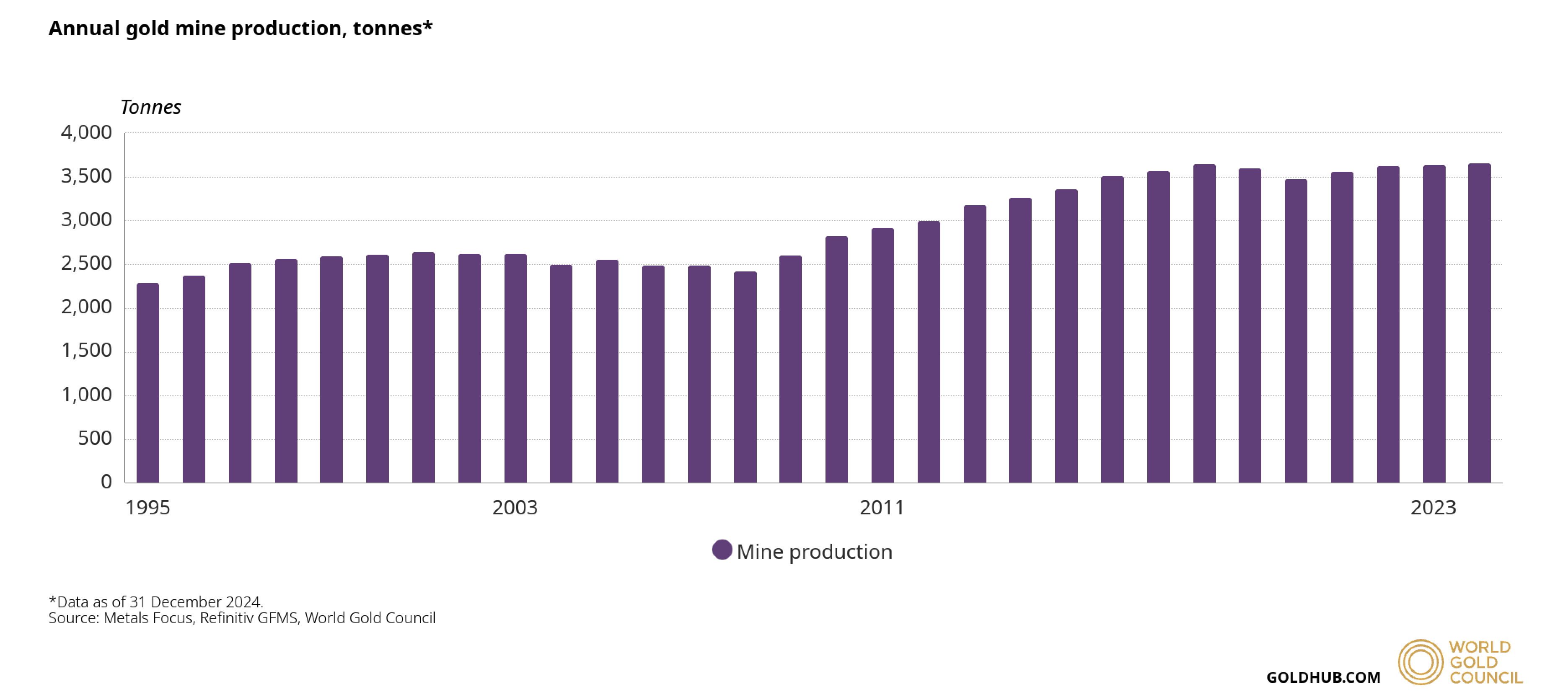

While mine production hit a record in 2024, the above chart shows a relatively modest growth rate compared to the demand chart, highlighting how rare development-ready assets have become. Even with record production, the pace of new project development is not enough to meet market needs.

Troilus Gold's Reid points out this valuation gap directly: "We're building a billion-dollar mine with a $160M market cap." Similarly, George Salamis of Integra Resources notes:

"We're trading at 0.25x P/NAV—our peers are twice that."

The situation has created a high-stakes environment where companies with viable, permitted projects are positioning themselves as takeover targets for major producers facing reserve depletion. "All the big projects have been bought—we're part of what's left," says Wilton, highlighting First Mining's position in a shrinking pool of available assets.

In Africa, Perseus Mining's Jeff Quartermaine exhibits similar confidence in the value of their development pipeline:

"We own two of the three best undeveloped assets in Africa."

This assertion reflects how gold producers are increasingly viewing high-quality, undeveloped projects as strategic assets that justify premium valuations.

The scarcity extends beyond simply the presence of gold ounces in the ground. Projects that have overcome regulatory hurdles hold particular value. As Wilton describes their permitting progress: "We're seven years into permitting. The only thing worse than that... is being anything less than seven years in." With permitting timelines extending into decades in some jurisdictions, assets that have navigated this process successfully represent a different category of value altogether.

Creative Capital: Reimagining Project Financing

The financial architecture that has underpinned gold project development for decades is experiencing a profound transformation. Traditional financing models—centered around large equity raises and project debt—have given way to more innovative, hybrid approaches as both market conditions and investor expectations evolve. This shift reflects broader changes in capital markets: institutional investors now demand stronger returns and clearer paths to profitability, while generalist capital has largely exited the mining sector in favor of technology and other growth industries.

Simultaneously, traditional mining banks have dramatically reduced their exposure to development-stage projects, creating a financing gap that has forced companies to reimagine how gold mines are funded. The days of raising hundreds of millions in equity and debt to build large-scale projects with long payback periods have largely disappeared. In their place, a new generation of developers is pioneering capital-efficient, staged approaches that prioritize early cash flow generation and financial self-sufficiency.

The result is a financing landscape transformed by necessity, where royalties, streams, offtake agreements, and phased development plans have become essential components of the modern mine builder's toolkit. Companies that can successfully navigate this new financial reality hold a significant competitive advantage in bringing new supply to a gold market desperately seeking production growth.

Jason Attew of Osisko Gold Royalties describes this new reality:

"Equity is expensive, and banks have largely exited project finance—royalties are now essential to funding."

This observation highlights how the financing ecosystem has evolved, with royalty and streaming companies becoming critical participants in the project development cycle.

The pressure to avoid shareholder dilution has led some companies to pioneer self-funding approaches. Alan Carter of Cabral Gold articulates this strategy:

"We're breaking away from the hamster wheel. This starter project is to fund exploration—not dilute shareholders."

This "walk before you run" approach prioritizes generating cash flow from modest initial operations to fund more ambitious growth plans.

Troilus Gold's Reid highlights another financing strategy—using by-products to make projects economically viable: "Copper funded this mine—if we were pure gold, we wouldn't have financed this project." This underscores how polymetallic deposits may hold advantages in securing project financing compared to pure gold plays.

These financing innovations reflect a broader shift in market expectations. Investors no longer reward companies merely for growing ounce counts—they demand disciplined capital allocation and clear paths to profitability. As Perseus's Quartermaine states, "Our job is not spending money. It's generating value."

Operational Efficiency: The Grade Game

The evolving financing landscape has driven another significant shift in the gold sector: a move away from large-scale, capital-intensive projects toward smaller, higher-margin operations focused on operational excellence. Shane Williams of West Red Lake Gold articulates this new paradigm: "This is not a tonnage game. It's a grade game."

This focus on quality over quantity is reshaping how developers approach project planning. Williams adds: "We've done 18 months of operational readiness. Most companies build and figure it out later—that's where they fail." This emphasis on thorough planning before production represents a departure from the boom-era mentality of building at any cost.

Cabral Gold's Carter exemplifies this lean approach: "We're not blasting or crushing—we're scooping mud and leaching it. Cheap and simple." By focusing on easily accessible, oxidized material, Cabral aims to achieve production without the massive capital expenditures traditionally associated with mine development.

Similarly, Integra Resources' Salamis describes their "fit-for-purpose production" philosophy:

"70-75K oz/year is enough to de-risk other assets without coming back to market."

This approach prioritizes achieving cash flow self-sufficiency over maximizing production volume.

Rio2's Alex Black perhaps summarizes this operational philosophy most succinctly: "This is simple—it's an earthmoving exercise. Mining gold and trucking water—we can do both. You don't want to make mining complex." This back-to-basics approach reflects an industry-wide recognition that operational discipline and margin focus are paramount in today's financing environment.

The impressive returns possible from these leaner operations upend conventional wisdom about the economics of smaller mines. West Red Lake Gold's Williams notes their project delivers a "255% IRR" by starting "small and profitable." These metrics demonstrate how high-grade, focused operations can generate compelling returns even at modest production scales.

Strategic Timing: The M&A Wave

With major gold producers facing reserve depletion and few new discoveries in the pipeline, industry observers widely anticipate an acceleration in merger and acquisition activity. This expectation has created a strategic inflection point for developers with advanced projects.

Troilus Gold's Reid positions his company as being on the cusp of a significant revaluation: "We were all the same market cap as Skeena and Artemis—they quadrupled after completing financing. We're next." This statement encapsulates the sentiment among many developers that successful project financing packages can trigger substantial market re-ratings.

The current market dynamics favor companies that have already completed the hard yards of permitting and project de-risking. As First Mining's Wilton notes:

"We've done the hard yards. The catalysts are close. The timeline for a producer to need us is lining up perfectly."

This sentiment reflects confidence that major producers will increasingly look to acquisitions to replenish their depleting reserves.

Osisko Gold Royalties' Attew highlights their strategic positioning within this M&A landscape: "We're 5% of the sector's market cap but captured 10% of total royalty deal flow—we're punching above our weight." This observation underscores how specialized financing vehicles are capturing an outsized portion of industry transactions.

For the majors, acquisitions have become a more efficient path to ounce growth than exploration or organic development. Northern Superior's Marcotte frames their project as "an amazing opportunity for anyone... any of those large gold producers to walk into the camp." This positioning acknowledges the strategic imperative for producers to secure quality assets in favorable jurisdictions.

Jurisdictional Edge: Where Location Matters

In the modern gold industry, a project's location carries implications far beyond geology. Regulatory frameworks, community relationships, and social license to operate have become critical determinants of project viability.

Perseus Mining's Quartermaine addresses the perceived risks of operating in Africa head-on:

"We've invested heavily in Africa—it's our competitive edge. Sure, there are risks. But you can run a company well or badly in any jurisdiction. It's about execution."

This perspective highlights how specialized regional expertise can transform jurisdictional challenges into competitive advantages.

In Canada, First Mining Gold emphasizes the community development aspect of their project: "This is a once-in-a-generation opportunity for Indigenous communities in Ontario—$4B in procurement alone." This approach recognizes that successful modern mining requires creating value for all stakeholders, not just shareholders.

Brazil-focused Cabral Gold leverages proximity to established operations as a de-risking factor: "We're right next door to Tocantinzinho—and Cuiu Cuiu had 10x the historic placer gold production." This contextual positioning helps investors understand the project's potential within a proven gold district.

The jurisdictional calculus extends beyond political risk to encompass regulatory efficiency. Projects in jurisdictions with streamlined permitting processes may hold advantages over those in regions with more complex regulatory requirements. As permitting timelines stretch into decades in some areas, this efficiency differential becomes increasingly significant.

The Gold Industry's New Gatekeepers

As the gold sector navigates this period of structural supply constraints, a new class of companies is emerging to bridge the gap between declining production from majors and robust market demand. These companies share several distinguishing characteristics:

- They prioritize operational efficiency over scale

- They employ creative financing strategies to minimize dilution

- They focus on generating cash flow before pursuing growth

- They leverage jurisdictional expertise as a competitive advantage

- They position their projects with an eye toward eventual M&A outcomes

This new generation of developers is redefining what constitutes a successful gold company. As Cabral's Carter describes it, they're "walking so we can run." This measured approach contrasts sharply with the growth-at-any-cost mentality that characterized previous cycles.

The emphasis on self-funding growth is perhaps the most significant departure from traditional models. Integra's Salamis describes their pathway: "We're heading toward 300,000 oz/year across three projects—and we're self-funding the growth." This approach requires patience and discipline but promises to create more sustainable business models.

For investors and industry participants, these shifts offer both challenges and opportunities. The scarcity of quality development assets suggests potential for premium valuations of advanced projects. Meanwhile, the focus on operational discipline and cash flow generation may improve the overall financial health of the sector.

Conclusion: A Golden Opportunity in Crisis

The gold industry faces a pivotal moment defined by conflicting forces: record-high prices signaling robust demand yet a concerning shortage of new projects entering the production pipeline. This supply crisis, however, has catalyzed a transformation within the sector—one that may ultimately strengthen its foundations and create sustainable value for those positioned to capitalize on it.

As the gold price continues its historic ascent, the companies that can successfully navigate these structural supply constraints—bringing new ounces to market efficiently and profitably—stand to emerge as the new leaders in a transformed gold industry. For an industry long characterized by boom-and-bust cycles, this evolution toward financial discipline and operational excellence may represent the most valuable development of all.

In the words of Perseus's Quartermaine, "We aim for fair and equitable returns for all stakeholders—but you can only cut the cake once." This statement perhaps best captures the new ethos of the gold sector: disciplined, focused on value creation, and mindful that sustainable success requires balancing the interests of all participants in the mining ecosystem.

The M&A wave now gathering momentum will likely accelerate as major producers face the reality of reserve depletion against limited exploration success. For the select few companies with permitted, development-ready assets in favorable jurisdictions, this represents a rare moment of advantage in negotiations with potential acquirers. As First Mining's Wilton notes, the timing for developers and producers "is lining up perfectly."

The gold industry stands at a crossroads. The path forward will be defined not by who can build the biggest mines or claim the most ounces, but by who can most efficiently transform geological potential into shareholder value while navigating the complex realities of modern mining. In this new landscape, the winners will likely be those who embrace operational discipline, financial creativity, and stakeholder engagement as their guiding principles.

For investors seeking exposure to gold's continued strength, the companies addressing the supply gap—particularly those with advanced, de-risked projects and the operational discipline to deliver on promises—may offer compelling opportunities. As the structural imbalance between gold demand and supply persists, these new gatekeepers of the gold industry are positioned not just to benefit from higher prices, but to fundamentally reshape how gold mining creates and distributes value in a resource-constrained world.

Company Profiles: Gold's New Vanguard

First Mining Gold

First Mining Gold has positioned itself as a development company with one of North America's largest undeveloped gold projects. The company's flagship Springpole Gold Project in northwestern Ontario hosts 4.6 million ounces in the indicated category and represents one of the few remaining large-scale gold projects not yet controlled by a major producer. Under CEO Dan Wilton's leadership, First Mining has navigated a complex seven-year permitting process that few others have successfully completed in recent years. "All the big projects have been bought—we're part of what's left," notes Wilton, highlighting the company's position in a market of increasingly scarce development assets. With permitting in its final stages—"241 days left on the federal clock"—the company is approaching a crucial regulatory milestone that could significantly redefine its value to potential acquirers.

Investor Insight: First Mining offers exposure to a significantly de-risked, large-scale gold project nearing the end of its permitting journey. This seven year regulatory progress positions the company at a strategic advantage when major producers face increasing pressure to replace reserves. Beyond the project economics, First Mining has emphasized community engagement, noting that their project represents "a once-in-a-generation opportunity for Indigenous communities in Ontario—$4B in procurement alone."

Troilus Gold

Troilus Gold is advancing the restart of the past-producing Troilus Mine in Quebec, transforming it into a 22-year operation producing 350,000 oz gold-equivalent annually. CEO Justin Reid has navigated the company through challenging market conditions by leveraging the project's polymetallic nature, particularly its copper component. The company stands at a pivotal moment in its development journey, having completed critical technical studies and advancing financing discussions. "We're rounding third," says Reid, indicating the company is approaching the final stages before production. A key differentiator for Troilus has been its copper credits, with Reid noting that "Copper funded this mine—if we were pure gold, we wouldn't have financed this project."

Investor Insight: Troilus represents a compelling valuation opportunity with a clear path to re-rating. "We're building a billion-dollar mine with a $160M market cap," Reid points out, highlighting the significant disconnect between the project's intrinsic value and its current market valuation. The company sees itself following the trajectory of its peers: "We were all the same market cap as Skeena and Artemis—they quadrupled after completing financing. We're next." This potential for substantial share price appreciation, coupled with a diversified metal exposure that includes copper, positions Troilus as an attractive option for investors seeking leverage to both precious and base metals in a tier-one jurisdiction.

West Red Lake Gold Mines

West Red Lake Gold is advancing high-grade gold assets in Ontario's prolific Red Lake district, one of Canada's most storied gold producing regions. Under the leadership of Shane Williams, the company has differentiated itself through meticulous operational planning and a focus on high-margin ounces rather than tonnage. This approach represents a departure from the industry's traditional emphasis on scale, with Williams emphasizing quality over quantity: "This is not a tonnage game. It's a grade game." The company has invested heavily in pre-production planning, completing "18 months of operational readiness" to minimize execution risk when production begins.

Investor Insight: West Red Lake offers investors exposure to one of the few near-term production stories in a high-grade Canadian gold district. Their disciplined approach reduces the operational risks that have plagued many junior miners transitioning to production. "Most companies build and figure it out later—that's where they fail," Williams notes. The economics of their staged development approach are compelling, with the company highlighting that they're "starting small and profitable—255% IRR." Perhaps most significantly, their timing aligns perfectly with the current gold price environment: "There are very few projects moving into production in 2025—that's key with the gold price as it is today." This positions West Red Lake to capture maximum value from the current strong market conditions.

Cabral Gold

Cabral Gold is developing multiple gold deposits within a 7km-long anomaly in Brazil's Tapajos region, near the Tocantinzinho project. Led by CEO Alan Carter, the company has adopted an innovative approach to development that prioritizes early cash flow generation over traditional equity financing. Their initial focus is on easily accessible, oxidized material that can be processed without complex crushing or grinding circuits. "This is mud—we don't blast or crush, just scoop and leach. It's very low cost," explains Carter. This pragmatic approach allows Cabral to generate cash flow quickly while continuing to expand their resource base across multiple targets.

Investor Insight: Cabral represents a self-funding growth story with near-term production potential and substantial exploration upside. Carter's innovative financing strategy breaks the cycle of dilutive equity raises that has plagued junior miners: "We're breaking away from the hamster wheel. This starter project is to fund exploration—not dilute shareholders." The valuation proposition is compelling, with Carter noting that "The current market cap is about the same as the profit we'll make in year one." Beyond the initial production plan, the exploration potential remains substantial: "We've got five deposits and 50 targets in a 7km-long anomaly—it's the most stunning project I've worked on." This combination of near-term cash flow with blue-sky exploration potential in a proven gold district makes Cabral an intriguing option for investors seeking both immediate returns and long-term growth.

Integra Resources

Integra Resources is advancing multiple gold-silver projects across the western United States, anchored by the DeLamar project in Idaho. Under the leadership of George Salamis, the company has adopted a staged development approach focused on achieving cash flow self-sufficiency before pursuing more ambitious growth. This "walk before you run" strategy centers on initial production of 70-75,000 ounces annually, which Salamis describes as "fit-for-purpose production" that is "enough to de-risk other assets without coming back to market." This disciplined approach demonstrates Integra's commitment to minimizing shareholder dilution while methodically building a multi-asset production base.

Investor Insight: Integra offers investors exposure to a company with a clear path to becoming a self-funded, multi-asset producer in tier-one jurisdictions. Salamis points to a significant valuation opportunity, noting that "We're trading at 0.25x P/NAV—our peers are twice that." This discount persists despite the company having "already done the hard work" necessary to advance their projects toward production. Looking forward, Integra has articulated an ambitious but disciplined growth trajectory: "We're heading toward 300,000 oz/year across three projects—and we're self-funding the growth." This focus on organic, internally-funded expansion represents a sustainable model that contrasts with the dilutive growth strategies that have challenged shareholder returns in the sector historically.

Northern Superior Resources

Northern Superior Resources controls district-scale gold exploration and development assets in the mining-friendly jurisdiction of Quebec. Under Simon Marcotte's leadership, the company has assembled a portfolio that stands out for both its scale and its status as one of the few remaining large gold camps not controlled by a major producer. The company has highlighted the strategic value of their land package in a market where quality exploration platforms have become increasingly scarce. "If you know of another camp of this size that is not currently either owned or controlled by one of the senior gold producers globally, let me know because I can't think of one," notes Marcotte, underscoring the unique position Northern Superior occupies.

Investor Insight: Northern Superior provides investors with exposure to district-scale exploration potential at a time when such opportunities are increasingly rare. As reserve replacement challenges intensify for major producers, assets with the scale to meaningfully impact their production profiles become more valuable. Marcotte positions their project as "an amazing opportunity for anyone... any of those large gold producers to walk into the camp," highlighting its potential as an M&A target. The company's focused exploration in Quebec also offers jurisdictional advantages, with Canada consistently ranking among the world's most mining-friendly regions. For investors seeking exploration upside with a clear path to eventual development or M&A, Northern Superior represents a compelling option in a market of diminishing quality exploration plays.

Perseus Mining

Perseus Mining has established itself as a successful multi-mine gold producer focused on West Africa, with operations across Ghana, Côte d'Ivoire, and Sudan. Under the leadership of Jeff Quartermaine, the company has built a reputation for operational excellence and disciplined capital allocation in a region often perceived as challenging by Western investors. Perseus has successfully navigated the complexities of operating in Africa through deep regional expertise, with Quartermaine noting that "We've invested heavily in Africa—it's our competitive edge." This specialized knowledge has allowed Perseus to identify and develop assets that others might overlook, building a sustainable production base with substantial growth potential.

Investor Insight: Perseus offers investors exposure to a proven operator with multiple producing assets and a clear growth pipeline in a region that often trades at a discount to comparable operations in other jurisdictions. Quartermaine's straightforward management philosophy—"Our job is not spending money. It's generating value"—has translated to consistent operational performance and shareholder returns. The company has positioned itself for continued growth, with Quartermaine asserting that "We own two of the three best undeveloped assets in Africa." For investors concerned about jurisdictional risk, Quartermaine offers a pragmatic perspective: "Sure, there are risks. But you can run a company well or badly in any jurisdiction. It's about execution." This focus on operational excellence over geography has allowed Perseus to generate substantial value in regions where others have struggled.

Osisko Gold Royalties

Osisko Gold Royalties has built a diversified portfolio of precious metals royalties and streams, with a primary focus on the Americas. Anchored by their cornerstone Canadian Malartic royalty, the company has established itself as a key player in mining finance at a time when traditional funding sources have become increasingly constrained. Under Jason Attew's leadership, Osisko has maintained a disciplined approach to capital allocation while expanding its influence in the sector. The company has strategically leveraged its technical expertise to identify and secure high-quality assets, resulting in outsized market impact relative to its size.

Investor Insight: Osisko offers investors lower-risk exposure to gold price upside through a diversified portfolio of royalties and streams. Attew highlights their strategic positioning: "We're 5% of the sector's market cap but captured 10% of total royalty deal flow—we're punching above our weight." This ability to secure attractive deals stems from their technical expertise and disciplined investment approach: "We focus on high-return deals. We're not going to do 1-2% IRR transactions just to say we're busy." As traditional project financing becomes increasingly scarce, royalty companies like Osisko have gained strategic importance, with Attew noting that "Equity is expensive, and banks have largely exited project finance—royalties are now essential to funding." This evolving financing landscape positions Osisko to secure attractive deals in a supply-constrained environment while providing investors with diversified exposure to the gold sector.

Rio2

Rio2 is advancing the Fenix Gold Project in Chile, one of the largest undeveloped gold oxide deposits in the Americas. Under the leadership of Alex Black, the company has focused on a straightforward development approach that minimizes technical complexity and capital intensity. The Fenix project stands out for its simple metallurgy and operational design, with heap leaching of run-of-mine material eliminating the need for crushing and grinding. This focus on operational simplicity reflects Black's development philosophy, centered on practical engineering solutions rather than complex processing flowsheets.

Investor Insight: Rio2 offers investors exposure to a large-scale development project with a clear path to production and an emphasis on operational simplicity. Black's pragmatic approach is evident in his statement: "This is simple—it's an earthmoving exercise. Mining gold and trucking water—we can do both. You don't want to make mining complex." This focus on straightforward operations reduces execution risk—a critical consideration for investors in development-stage companies. The project's location in Chile also provides jurisdictional advantages, with established mining regulations and infrastructure. As one of the few substantial oxide gold projects advancing toward production, Fenix represents a valuable asset in an environment of constrained supply growth, positioning Rio2 to potentially benefit from both the current strong gold price environment and increasing scarcity value for development-ready gold projects.

Analyst's Notes

Subscribe to Our Channel

Stay Informed