150% Upside in Royalty Stocks, 33% Returns as M&A Activities Accelerates

-min.jpeg)

Mining M&A analysis reveals 150% upside in royalty stocks, 33% fund returns, and consolidation opportunities despite transaction complexity.

The mining sector's consolidation narrative gained renewed momentum with Royal Gold's acquisition of Sandstorm Gold and Horizon Copper, a transaction highlighitng both the value creation potential and operational complexities inherent in mining mergers and acquisitions (M&A). Understanding the M&A dynamics provides crucial insights into identifying undervalued assets and recognizing catalysts that can drive substantial returns. The recent performance of specialized mining investment funds and the mathematical frameworks used to value royalty companies offer concrete examples of how sophisticated investors are capitalizing on sector consolidation.

Strong Performance on Mining Investment Strategy

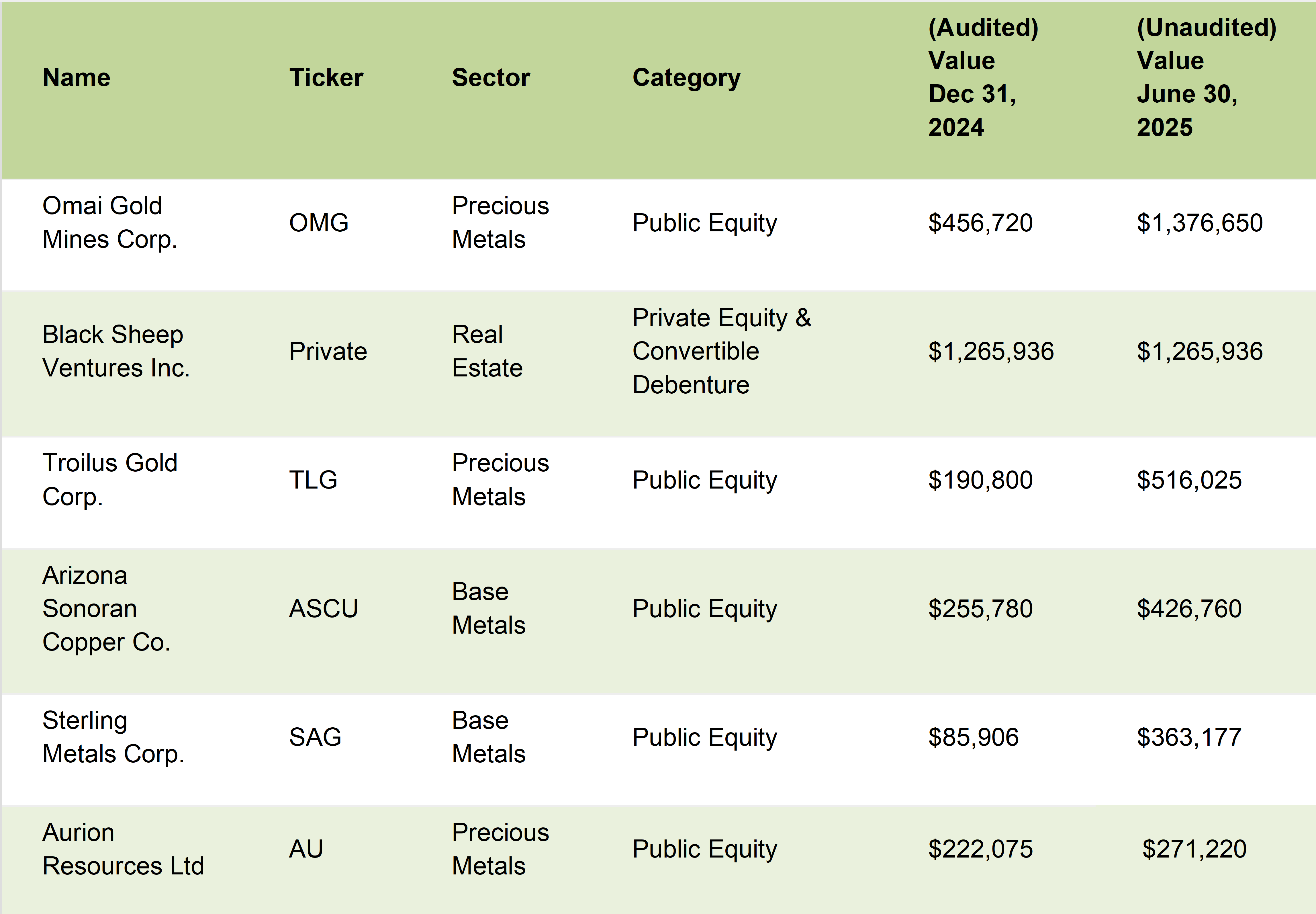

Olive Resource Capital's impressive 33% return in the first half of the year demonstrates the potential for focused mining investment strategies. The fund grew its assets under management from $6.4 million to $8.5 million after all expenses, with approximately 50-55% allocated to precious metals investments. This performance was driven by three key holdings: Omai Gold Mines, Troilus Gold, and Sailfish Royalties, each delivering over 100% returns for the fund.

The success of these investments illustrates the importance of selective positioning within the mining sector. Troilus Gold's appreciation from the $30-39 range to $60-70 represents the type of re-rating that can occur when mining companies execute on their development plans or benefit from improved market conditions. Similarly, the fund's convertible debenture investment in Sailfish Royalties, which has been converted to equity at substantial gains, demonstrates how structured investments can provide both downside protection and upside participation.

Source: Olive Resource Capital Provides Update on Investments for June 2025

Royalty Sector M&A Provides Valuation Framework

The Royal Gold acquisition of Sandstorm Gold (and Horizon Copper) offers investors a concrete framework for valuing royalty companies and identifying potential targets. According to the analysis presented, the transaction valued Sandstorm at approximately 88% of its attributable gold ounces at current spot prices, consistent with historical royalty M&A transactions that typically range from 60% to 100% of spot gold value.

This valuation methodology focuses on attributable ounces with reasonable certainty of delivery under current mine plans, providing a more reliable metric than net present value calculations that incorporate numerous variables. Historical precedent supports this approach: Triple Flag's acquisition of Fosterville and Young Davidson royalties from Santara was valued at approximately 93% of attributable ounces at $1,290 gold, while Royal Gold's acquisition of the Arrow royalty was valued at 78-79% of spot gold prices.

150% Upside Potential

Applying the 88% valuation metric to Sailfish Royalties reveals significant upside potential for investors. Based on estimated deliverable resources from the San Albino and Spring Valley projects, the company's fair value approaches $350 million. With the company currently trading at just under $150 million enterprise value, this suggests approximately 150% upside potential if Spring Valley develops as expected.

While Sandstorm was a diversified royalty company and Sailfish has one producing royalty plus a tier-one development asset, the presence of that development asset may actually command premium valuations. Royalty companies particularly value tier-one development assets on the path to production, as these represent the growth opportunities that justify higher multiples. The Spring Valley project's advancement toward production could serve as a catalyst for the re-rating implied by the valuation analysis.

Compass, Episode 22

The Complexity of Mining M&A

Understanding why more M&A doesn't occur in the mining sector reveals both challenges and opportunities for investors. The M&A process involves numerous complex steps, beginning with informal conversations between management teams and progressing through letters of intent, due diligence, definitive agreements, regulatory approvals, and shareholder votes. Each stage presents potential failure points where deals can collapse.

The process typically starts with CEOs discussing potential synergies, followed by negotiating a letter of intent that establishes exclusivity for due diligence. However, this initial agreement involves convincing not just two management teams but their respective boards, essentially requiring ten people to agree that further discussions make sense. The due diligence phase encompasses both technical evaluation of mining assets and extensive legal review to confirm property ownership, verify historical agreements, and identify potential liabilities.

Common Failure Points in Mining Deals

Three primary factors contribute to M&A failure in the mining sector: greed, structural complexity, and hidden liabilities.

- Greed manifests in two forms: unrealistic company valuations and excessive management compensation demands. Many management teams and shareholders maintain inflated views of their company's worth, particularly problematic given that the intrinsic value of most exploration companies approaches zero. Management change-of-control provisions can also derail otherwise sensible transactions. While these agreements are standard practice, unreasonable demands for cash payments rather than equity participation in the combined entity can kill deals that would benefit shareholders. This becomes particularly problematic when management seeks substantial cash payouts from mergers between junior exploration companies.

- Structural complexity represents another significant hurdle. The location of subsidiaries, shareholder composition, and regulatory jurisdiction can create insurmountable obstacles. Companies with majority US shareholders face additional SEC regulation, increasing costs and complexity. The prevalence of reverse takeover transactions in Canada means many public companies have existed for decades, creating potential corporate structure issues that surface during detailed due diligence.

- The due diligence process frequently uncovers previously unknown liabilities that can derail transactions. These may include improperly terminated employees, dormant subsidiaries with ongoing obligations, or historical agreements with continuing implications. The analysis revealed that many public mining companies are poorly managed from a corporate perspective, with outdated signing authorities and incomplete corporate records creating future complications.

These discoveries during due diligence can force deal renegotiation or termination, particularly when liabilities carry high probability of materialization. Even relatively small issues, such as a $300,000 employment liability from improper termination procedures, can significantly impact valuations for smaller mining companies and create deal uncertainty.

Recent Transaction Examples & Market Dynamics

The failed merger between ValOre and South Atlantic Gold illustrates how market conditions can undermine even logical consolidation plays. Despite both companies operating in Brazil with similar land packages in the same district, rising gold prices altered the relative attractiveness of the original merger ratio, leading to insufficient shareholder support. This demonstrates how external market factors can overwhelm fundamental deal logic.

Similarly, the ongoing situation between CANEX and Gold Basin represents the challenges in completing value-creating transactions even when synergies are clear. These adjacent projects could benefit from consolidation and operational synergies, yet the parties cannot reach agreement, highlighting how multiple stakeholder interests can prevent beneficial combinations.

Consolidation Imperative & Investment Implications

The mining sector's fragmentation creates both challenges and opportunities for investors. The analysis suggests the industry needs fewer, stronger companies rather than the current proliferation of small, poorly capitalized entities. This consolidation imperative creates opportunities for investors who can identify potential targets and acquirers before market recognition occurs.

Successful M&A requires significant management skill in navigating complex stakeholder dynamics and maintaining momentum through lengthy processes. Companies with experienced management teams capable of executing transactions may command premium valuations, while potential targets trading below fair value based on M&A comparables represent attractive opportunities.

The hostile takeover route remains prohibitively expensive in Canadian markets, requiring $200,000-300,000 minimum investment for small companies, plus ongoing management responsibilities. This cost structure favors negotiated transactions and creates protection for existing management teams, but also ensures that successful hostile bids must overcome significant economic hurdles.

The Investment Thesis for Precious Metals

- Target Royalty Companies Trading Below M&A Comparables: Focus on royalty companies with tier-one development assets trading significantly below 60-100% of attributable ounces at spot commodity prices

- Identify Management Teams with M&A Experience: Invest in companies led by executives with proven track records of completing successful transactions, as process complexity favors experienced operators

- Focus on Logical Consolidation Candidates: Prioritize adjacent projects or complementary assets where 1+1 truly equals more than 2, particularly in established mining districts

- Monitor Failed Transactions for Re-Entry Opportunities: Companies involved in failed M&A attempts often trade down despite unchanged fundamentals, creating attractive entry points

- Evaluate Corporate Structure Quality: Avoid companies with complex subsidiary structures, majority US shareholdings, or poor corporate governance that increase M&A complexity

- Position Before Catalysts: Development milestones, feasibility studies, and production decisions often trigger M&A interest; establish positions before these inflection points

- Diversify Across Potential Targets: Given high M&A failure rates, spread investments across multiple logical consolidation candidates rather than concentrating in single positions

- Understand Management Incentives: Evaluate change-of-control provisions and management equity ownership to assess alignment with shareholder interests in potential transactions

The mining sector's consolidation imperative, combined with the mathematical framework demonstrated by recent royalty M&A transactions, provides investors with concrete tools for identifying undervalued assets and understanding catalysts that drive substantial returns. While M&A complexity creates execution risk, it also protects against hostile actions and ensures that successful transactions often command significant premiums. Investors who understand these dynamics and position appropriately can benefit from the ongoing industry consolidation while avoiding the pitfalls that trap less sophisticated market participants.

Analyst's Notes

Subscribe to Our Channel

Stay Informed