Americas Gold & Silver, Vizsla Silver, Cerro de Pasco Resources & GR Silver Mining: The Silver Investment Thesis for 2025

Silver supply deficits and China export controls create opportunities in Americas Gold & Silver, Vizsla, Cerro de Pasco & GR Silver for leveraged returns.

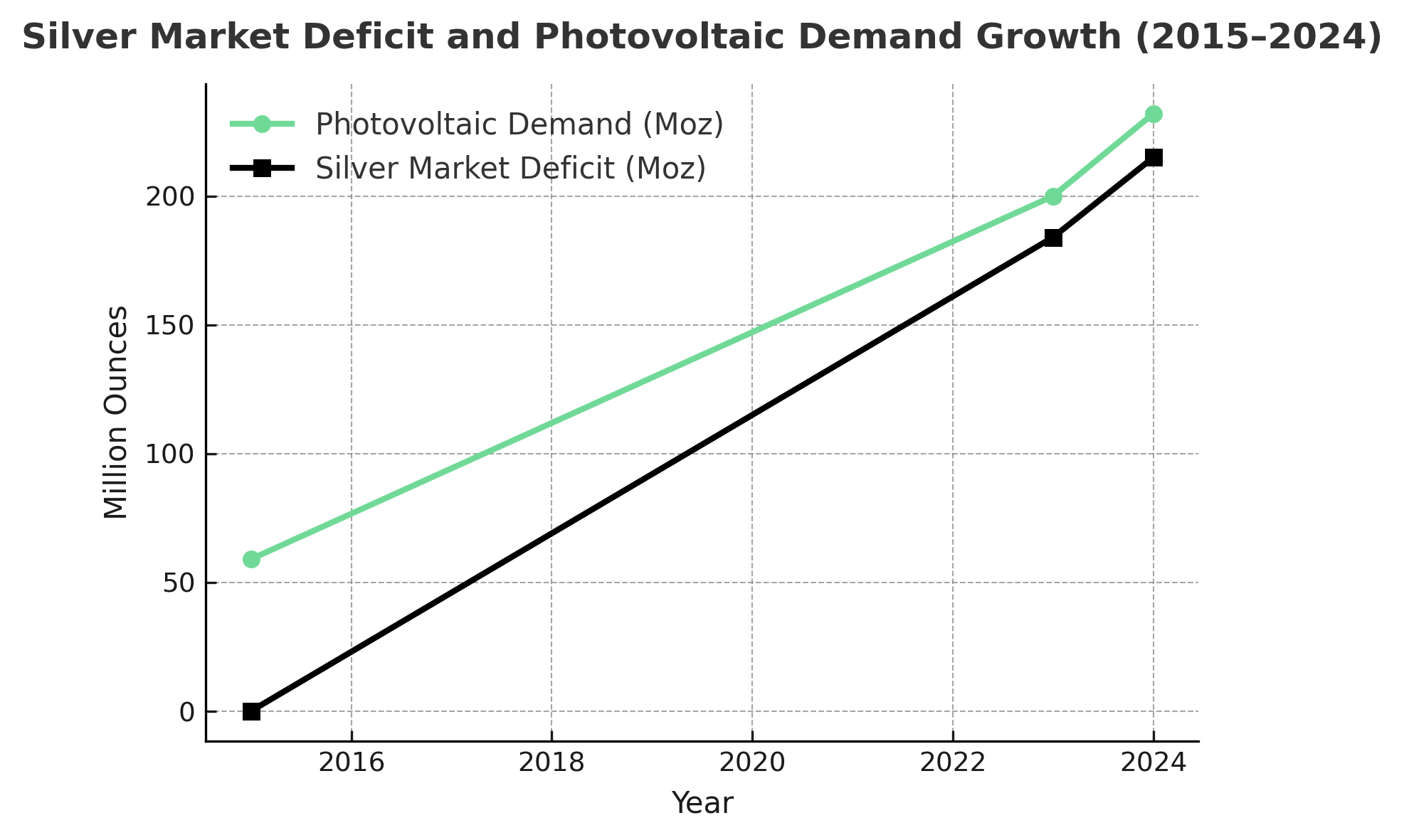

- The silver market deficit reached 184 million ounces in 2023 with expectations of a 17% expansion in 2024, driven by quadrupling photovoltaic demand (59 Moz to 232 Moz since 2015) while mine production stagnates, creating persistent supply-demand imbalances that favor producers with near-term production growth.

- China's November 1, 2025 addition of silver to controlled-export lists alongside existing dominance in critical by-products (98% of gallium production) accelerates "China Plus One" sourcing diversification, positioning North American and Latin American producers as strategic alternative suppliers.

- Silver's co-production with antimony (defense applications), gallium and indium (semiconductors), and copper (electrification) creates multiple revenue streams and strategic value beyond precious metals pricing, with U.S. policy prioritizing domestic critical minerals supply chains.

- Multiple high-grade silver projects advance toward production decisions in H2 2025-2027, offering investors exposure to construction-to-production valuation re-rating opportunities at discovery-stage valuations before cash flow visibility compresses risk premiums.

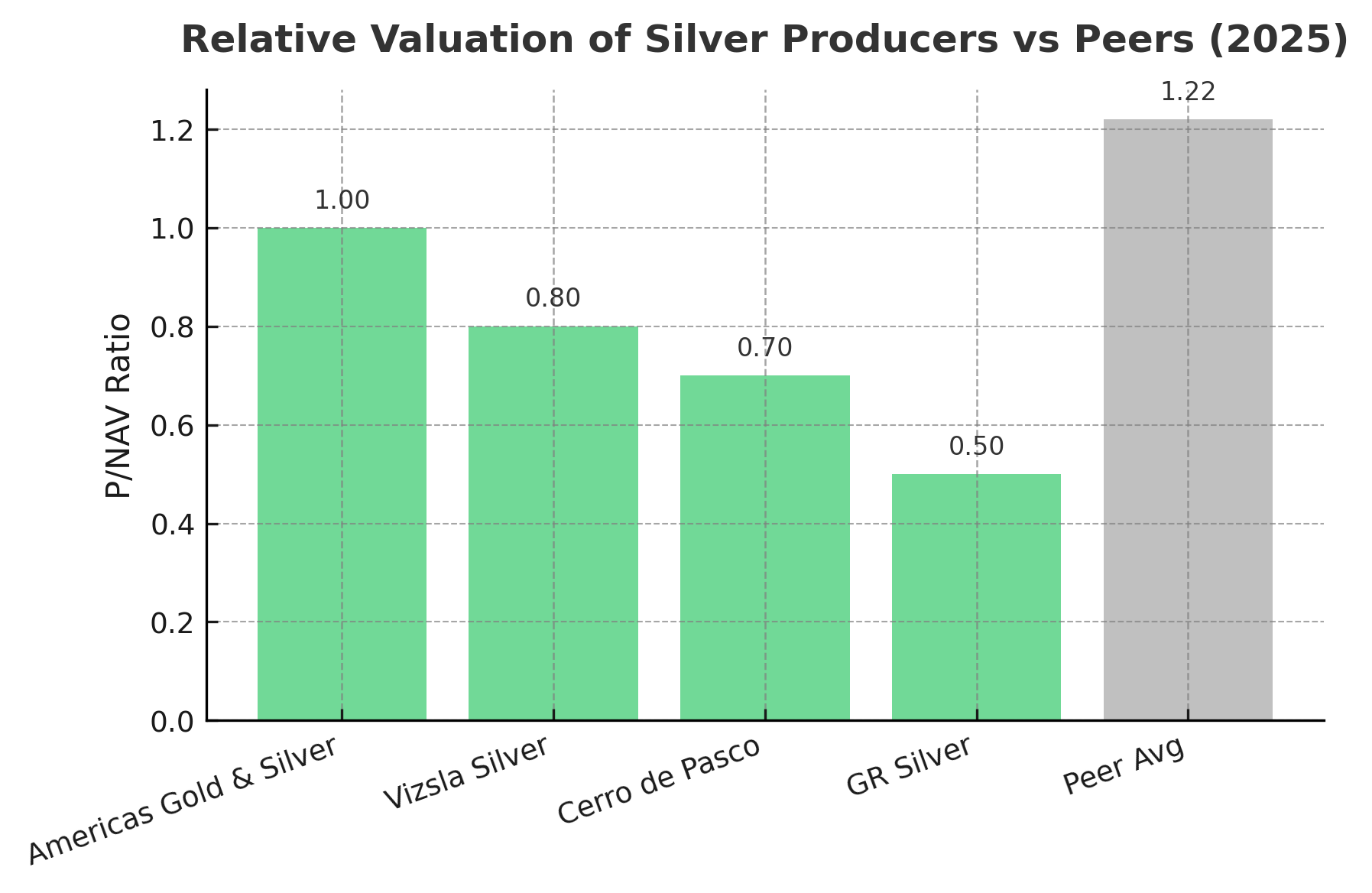

- Primary silver producers and near-producers trade at 30-50% discounts to diversified precious metals companies despite superior silver leverage (70-80% revenue exposure versus 20-30% for peers), with P/NAV ratios averaging 1.0x versus peer group 1.22x, presenting entry points before feasibility studies and financing milestones trigger institutional recognition.

The Silver Renaissance: Why North American and Mexican Producers Offer Compelling Risk-Adjusted Returns in 2025

The silver market enters 2025 fundamentally transformed from its 2020-2022 dynamics, with structural supply deficits, geopolitical supply chain reconfiguration, and accelerating industrial demand creating investment conditions not seen since the commodity supercycle of 2005-2011. Four companies (Americas Gold & Silver, Vizsla Silver, Cerro de Pasco Resources, and GR Silver Mining) represent distinct risk-reward profiles across the development spectrum, from operational turnarounds to district-scale exploration, each offering leveraged exposure to silver's ongoing supply squeeze while maintaining downside protection through industry-leading cost structures or resource scale.

The Macro Framework: Supply Deficits Meet Strategic Imperative

Silver's investment narrative rests on three converging forces that distinguish current market conditions from previous cycles. The photovoltaic industry alone consumed 232 million ounces in 2024, representing quadruple the 59-million-ounce demand from 2015, while electronics and 5G infrastructure deployment sustain robust industrial consumption. Mine production fails to keep pace, resulting in a 184-million-ounce deficit in 2023 that market participants expect to expand 17% in 2024, depleting above-ground inventories that historically buffered supply-demand imbalances.

China's November 1, 2025 policy shift adding silver to controlled-export lists alongside rare earth elements fundamentally alters global trade architecture. The immediate market reaction (a sharp Asian trading session decline followed by rapid recovery to $48.75 per ounce) signals investor recognition that restricted Chinese outbound flows will tighten global supply while potentially creating domestic oversupply within China. This policy framework mirrors China's 98% control of gallium production, a critical by-product of many silver operations, amplifying the strategic imperative for diversified supply chains outside Chinese jurisdiction.

The silver-to-gold ratio, historically averaging 60:1, traded above 80:1 for extended periods in 2020-2023 before compressing toward 70:1 in 2024-2025, suggesting silver remains undervalued relative to gold despite comparable safe-haven characteristics and superior industrial demand fundamentals. At current prices approaching $47 per ounce, silver has appreciated 134% from its 2016 low of $14.01, yet remains 40% below inflation-adjusted 1980 highs, providing runway for further price appreciation as supply deficits persist

Company Case Studies: Americas Gold & Silver: Operational Turnaround with Antimony Optionality

Americas Gold & Silver's transformation centers on the Galena Complex in Idaho's historic Coeur d'Alene Mining District, where management led by Chairman and CEO Paul Huet (architect of Klondex Mines' C$740 million sale to Hecla and Karora Resources' C$1.1 billion merger with Westgold) has orchestrated a comprehensive operational and financial restructuring. The October 2024 acquisition of the remaining 40% interest in Galena, increasing ownership to 100%, coincided with strategic investor Eric Sprott increasing his position to approximately 20% ownership, catalyzing institutional ownership expansion from 8% to 60%. The company's financial fortification proceeded in two phases: a C$50 million equity financing in October 2024 addressed immediate balance sheet needs, followed by a US$100 million debt facility plus US$15 million equity facility in June 2025, supported by offtake agreements with Teck Resources and Ocean Partners.

Galena's antimony production potential represents strategic optionality beyond silver revenue. As the only active U.S. mine producing antimony as a by-product, Galena has generated over 20 metric tons of antimony since 2001, with metallurgical testing demonstrating 99% recovery from concentrate grading approximately 19% antimony. Phase 2 testing completed in September 2025 confirmed commercial viability, positioning Galena to supply U.S. defense and flame-retardant markets currently dependent on Chinese and Russian sources representing 90% of global production. The company's approximately 80% silver revenue exposure for 2025 places it among the highest-leverage plays to silver prices within the peer group, yet valuation metrics show Americas Gold & Silver trading at approximately 1.0x price-to-net-asset-value versus the peer average of 1.22x.

Paul Andre Huet, Chairman and CEO, Americas Gold and Silver shared their operation:

"Our operation in Idaho is now starting to deliver results after spending significant effort underground at Galena conducting numerous time studies, engineering work, productivity-focused projects, implementing new equipment and adjusting the mining method. It is important to note that Galena achieved a quarter-over-quarter production improvement despite a 10-day shutdown conducted to complete Phase 1 of the upgrades to the No. 3 Shaft (a tremendous achievement). Additionally, last week's disclosure of year-to-date antimony and copper production further highlights the critical metal value of our tetrahedrite ore, as well as Galena's unique strategic position as the only current producer of antimony in the United States."

Vizsla Silver: Development Economics with Near-Term Production Visibility

Vizsla Silver's Panuco silver-gold district in Sinaloa, Mexico has evolved from exploration-stage asset to construction-ready project following a January 2025 Mineral Resource Estimate upgrade and continued advancement toward a feasibility study targeted for H2 2025. The company's 222.4 million ounces silver equivalent in Measured and Indicated resources grading 534 grams per tonne, plus 138.7 million ounces Inferred at 412 g/t, represents an 11% increase in global contained ounces versus the prior estimate, consolidating 40,000+ hectares with 86 kilometers of vein extent. The July 2024 Preliminary Economic Assessment outlined production of 15.2 million ounces silver equivalent annually over a 10.6-year mine life with all-in sustaining costs of US$9.40 per ounce, positioning Panuco in the lowest-cost quartile globally with after-tax NPV of US$1.1 billion, 86% IRR, and nine-month payback.

CEO Michael Konnert shared their vision:

"Vizsla's vision is to become the world's largest single-asset primary silver producer through exploration and development of the Panuco district in Mexico."

Vizsla's September 2025 execution of a Mandate Letter for US$220 million senior secured project financing led by Macquarie Bank, combined with US$200+ million cash position as of August 2025, establishes total financing capacity approaching US$450 million (exceeding estimated capital requirements for construction). This financing readiness, coupled with fully-permitted bulk sampling of 25,000 tonnes from the Copala and Napoleon deposits commencing Q4 2024, positions the company for a construction decision following feasibility study completion, targeting first silver production in H2 2027. The company's environmental, social, and governance framework has earned four consecutive years of ESR (Empresa Socialmente Responsable) distinction, with over US$600,000 invested in community initiatives since 2022, mitigating social license risk through signed agreements with all five local Ejidos and 70% local workforce participation.

The exploration upside narrative remains compelling despite the substantial resource base: only 30% of identified vein targets have been drill-tested across the 86-kilometer vein system, providing resource expansion potential beyond the current mine plan without additional capital requirements. With silver trading near $47 per ounce, Panuco's projected operating margins exceed $37 per ounce silver equivalent, providing substantial cushion against price volatility while offering leveraged upside to further silver price appreciation. The project's economic robustness extends to downside scenarios: even at $20 per ounce silver, AISC projections suggest Panuco remains cash-flow positive, addressing investor concerns about metal price sensitivity.

Cerro de Pasco Resources: Tailings Reprocessing at Industrial Scale

Cerro de Pasco Resources pursues a contrarian strategy focused on the world's largest above-ground silver-equivalent resource at the Quiulacocha tailings facility in Peru's Pasco Region. The historic estimate of 423 million ounces silver equivalent contained in sulphide tailings deposited from the 1900s through 1992 represents accumulated processing residues from different mining eras, with recent drilling results from 40 assayed holes demonstrating average grades of 1.66 ounces per ton silver (approximately 52 g/t), 1.47% zinc, and 0.89% lead, with composite silver-equivalent grades reaching 5.5 ounces per ton when including gallium (53 g/t) and indium (19.9 g/t) credits. These critical minerals by-products (essential for semiconductors, electric vehicles, solar panels, and LED applications) provide strategic optionality given China's 98% control of global gallium production.

The project's economic modeling presents compelling returns: the base case scenario processing 10,000 tonnes per day generates $39 per tonne profit with $2.9 billion life-of-mine value, while an upside case at 20,000 tpd production achieves $85 per tonne profit and $6.3 billion life-of-mine economics. These projections benefit from tailings reprocessing's inherent cost advantages (no drilling, blasting, or conventional mining infrastructure required) with submersible pumps mounted on barges moving slurry through floating pipelines for 24/7 operation. Environmental remediation represents a core value proposition beyond metal extraction economics, as legacy tailings contribute to acid water contamination affecting local water quality; reprocessing removes this environmental liability while generating economic returns.

Guy Goulet, Chief Executive Officer, Cerro de Pasco Resources stated their financial position:

"With the completion of this financing, Cerro de Pasco is in a stronger financial position to advance the Quiulacocha Project through the full feasibility stage and toward pre-construction readiness. Our immediate focus is on executing the technical, environmental, and engineering programs that will define the project's design and secure the highest standards of performance and sustainability. This additional capital reinforces our commitment to transforming the historic Cerro de Pasco district into a model of responsible resource development and long-term value creation."

GR Silver Mining: District-Scale Exploration with Near-Term Resource Expansion

GR Silver Mining occupies the highest-risk, highest-potential-return position within this peer group, pursuing district-scale exploration across 7,823 hectares at the Plomosas Project in Sinaloa while advancing bulk sampling and preliminary economic assessment work. The company's combined resource base of approximately 134 million ounces silver equivalent across the San Marcial Resource Area (68 Moz AgEq) and Plomosas Mine Area (66 Moz AgEq) provides scale comparable to established producers, yet current market capitalization near C$86 million (approximately US$63 million) implies discovery-stage valuation despite advanced technical work. September 2025 drilling results from the San Marcial Parallel Breccia Target intersected 9 meters grading 374 grams per tonne silver including 1 meter at 1,542 g/t silver with 1.4% copper and 0.62% tungsten, plus a separate 33-meter interval averaging 1.44 grams per tonne gold including 1.2 meters at 32.1 g/t gold.

Marcio Fonseca, President & CEO, GR Silver Mining stated the silver investment opportunities:

"We're encountering wide, high-grade silver intersections at San Marcial, 25 metres thick on average and we've only drilled 20 percent of the main geophysical anomaly. With two rigs on site and funding secured for the next 12 to 15 months, we're preparing a much larger program to expand the resource footprint, which we expect to be significantly larger in the next update."

The discovery confirms mineralization continuity approximately 500 meters south of the existing San Marcial Resource Area, validating geophysical targeting while 80% of the intrusive-related anomaly remains untested. Near-term catalysts through December 2025 include completion of Phase 1 step-out drilling (3,000 meters), advancement of the bulk sample program, and permit application for Phase 2 drilling (52 holes totaling 15,000 meters). The company's August 2025 C$13.8 million bought-deal financing ensures 12 months of drilling runway, while the integration potential between San Marcial's expanding resource and the Plomosas Mine's existing infrastructure creates optionality for a future hub-and-spoke operation that reduces capital intensity compared to greenfield development scenarios.

The Investment Thesis for Silver Development & Production Companies

- Vizsla Silver's US$450 million total financing capacity, fully-permitted bulk sampling, and H2 2025 feasibility study pathway exemplifies the risk-reward profile investors should target (construction-ready projects trading at discovery-stage valuations before cash flow visibility drives re-rating). Reduce reliance on established producers trading at premium valuations (1.2-1.5x P/NAV) by rotating into developers trading at 0.5-0.8x P/NAV, capturing the 30-50% valuation compression that typically occurs as production approaches.

- The 12-18 month period preceding construction decisions typically generates 40-60% returns as development risk diminishes and cash flow visibility increases, independent of commodity price movements. Vizsla's H2 2025 feasibility study and Americas Gold & Silver's Galena operational optimization completion represent near-term catalysts that could trigger project financing completion and construction timelines, reducing perceived risk and expanding the investor base to include funds restricted to producing assets.

- Americas Gold & Silver's 1.0x P/NAV versus the peer average of 1.22x, despite approximately 80% silver revenue exposure exceeding most peers' 20-30% silver leverage, illustrates market inefficiency driven by historical operational concerns rather than fundamental resource quality or economic potential. Similarly, GR Silver Mining's approximately US$0.47 per ounce silver equivalent enterprise valuation (US$63M market cap / 134 Moz AgEq resource) trades at steep discounts to peer group averages of $0.80-1.20 per ounce, offering re-rating potential as drilling expands resources and PEA work advances.

- Vizsla's 25,000-tonne bulk sample from Copala and Napoleon deposits, and GR Silver Mining's bulk sample test mining at Plomosas, will validate or challenge preliminary economic assessments' processing assumptions.

- Vizsla's 70% untested vein targets across 86 kilometers of structures, GR Silver Mining's 80% untested geophysical anomaly at San Marcial, and Cerro de Pasco's additional tailings areas beyond the initial Quiulacocha resource all offer resource expansion potential beyond current mine plans without additional capital requirements.

- Paul Huet's track record includes C$740 million Klondex sale and C$1.1 billion Karora merger, but operational delivery at Galena (particularly antimony production commercialization and achievement of 1,000 tpd processing targets) will validate or challenge investor confidence in the transformation thesis.

- A balanced silver portfolio might allocate 40% to near-producers with financing certainty (Vizsla), 30% to operational turnarounds with immediate cash flow (Americas Gold & Silver), 20% to innovative business models with proven resources (Cerro de Pasco), and 10% to aggressive exploration with district-scale potential (GR Silver Mining).

Conclusion: Positioning for Silver's Structural Supply Deficit

The convergence of persistent supply deficits (184 million ounces in 2023, expanding 17% in 2024), geopolitical supply chain fragmentation following China's November 2025 export controls, and accelerating industrial demand from photovoltaic and electronics applications creates conditions for sustained silver price strength independent of macroeconomic factors. At $47 per ounce, silver remains 40% below inflation-adjusted historical highs despite fundamentally tighter supply-demand dynamics than previous cycles, suggesting price appreciation potential even before considering safe-haven flows that typically accompany geopolitical uncertainty or monetary policy transitions.

Americas Gold & Silver, Vizsla Silver, Cerro de Pasco Resources, and GR Silver Mining represent distinct approaches to capturing this macro opportunity: operational turnarounds with critical minerals optionality, construction-ready development with industry-leading economics, tailings reprocessing at industrial scale, and district-scale exploration with near-term resource expansion. Collectively, these companies offer approximately 600 million ounces of silver-equivalent resources and production capacity, yet trade at aggregate enterprise value near $500 million (implying market valuations around $0.83 per ounce compared to peer group averages exceeding $1.20 per ounce for producing companies).

The 12-18 month catalyst pathway includes multiple inflection points: Vizsla's H2 2025 feasibility study and construction decision, Americas Gold & Silver's Galena production optimization and antimony commercialization, Cerro de Pasco's Phase 2 drilling and preliminary economic assessment, and GR Silver Mining's resource expansion drilling and PEA completion. These milestones represent opportunities for valuation re-rating as development risk diminishes and cash flow visibility increases, independent of silver price movements, while maintaining leveraged upside exposure to continued silver appreciation driven by structural supply deficits and industrial demand growth.

TL;DR

Silver's persistent 184-million-ounce deficit intensifies as China restricts exports while photovoltaic demand quadruples to 232 million ounces, creating structural supply tightness at $47 per ounce prices. Americas Gold & Silver transforms Idaho's Galena Complex into North America's antimony-producing silver operation with 80% revenue leverage. Vizsla Silver advances toward H2 2025 construction decision with US$450 million financing and $9.40/oz costs. Cerro de Pasco reprocesses 423 million ounces silver-equivalent tailings with gallium and indium credits. GR Silver Mining expands 134-million-ounce resources through district-scale exploration. These companies trade at $0.47-0.83 per ounce enterprise valuations versus $1.20 peer averages, offering 30-50% re-rating potential before production decisions compress risk premiums alongside silver's continued price appreciation driven by industrial demand and geopolitical supply fragmentation.

FAQs (AI-Generated)

Silver's supply deficit stems from accelerating industrial demand (particularly photovoltaic applications quadrupling to 232 million ounces annually) outpacing mine production constrained by declining ore grades, 7-10 year permitting timelines, and the fact that 70% of silver production occurs as a by-product of base metal mining, making supply partially inelastic to silver price movements.

China's export controls potentially restrict outbound shipments from the world's third-largest silver producer, tightening global supply while creating domestic Chinese oversupply, thereby accelerating "China Plus One" diversification that benefits North American and Latin American producers like Americas Gold & Silver, Vizsla Silver, and GR Silver Mining with minimal Chinese operational exposure.

Panuco combines exceptional grade (534 g/t silver equivalent), industry-leading low costs (US$9.40/oz AISC), robust economics (86% IRR with 9-month payback), operating margins exceeding $37/oz at current prices, US$450 million secured financing capacity, and four consecutive years of ESR social responsibility recognition, positioning it for H2 2025 construction decision and H2 2027 first production.

Tailings reprocessing eliminates 40% of conventional mining costs while accessing 423 million ounces silver equivalent of proven material with known metallurgy, generates $39/tonne profit in base case economics, provides critical minerals optionality (gallium and indium for semiconductors), and aligns commercial objectives with environmental remediation that creates social license advantages and ESG-driven valuation premiums.

A balanced allocation might dedicate 40% to near-producers with financing certainty (Vizsla), 30% to operational turnarounds with immediate cash flow (Americas Gold & Silver), 20% to innovative lower-capital-intensity models (Cerro de Pasco), and 10% to aggressive district-scale exploration (GR Silver Mining), capturing multiple inflection points across 12-36 month horizons while maintaining 70-80% revenue leverage to silver prices.

Analyst's Notes

Subscribe to Our Channel

Stay Informed