Atlas Salt: The Reported LOM Average EBITDA Makes This One of the Most Cash-Generative Industrial Minerals Operations in Canada

A North-American Displacement Play Against a Brittle Supply Chain

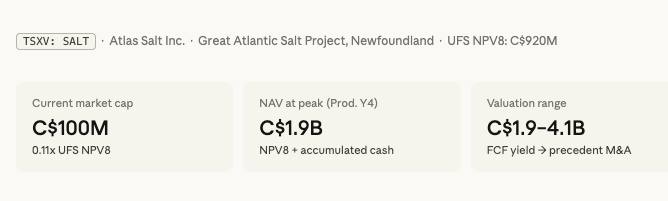

Atlas Salt's rolling NAV increases by roughly C$100M every year between now and first production. The stock is C$100M. That arithmetic deserves attention.

The Asset

Strip away the mining-sector framing and what Atlas Salt represents is a long-duration infrastructure asset with a captive municipal customer base, no metallurgical complexity, and a NAV that grows simply with the passage of time. That last characteristic is genuinely unusual in resource development and deserves to be the starting point for any serious analysis.

The company's updated feasibility study implies the project's NPV8 currently sits at C$920M, 9X the current market capitalisation, and that figure is not static. It potentially increases at roughly C$100M per year through the construction period, peaking at approximately C$1.9B in production year 4 once accumulated net cash is added to the residual NPV of future cash flows. By year 10, it reaches C$2.8B. By year 24 C$3.9B. This is what a long-life, infrastructure-style cash flow profile looks like in NAV terms: not an asset you consume, but one that compounds as capital is deployed and debt is retired.

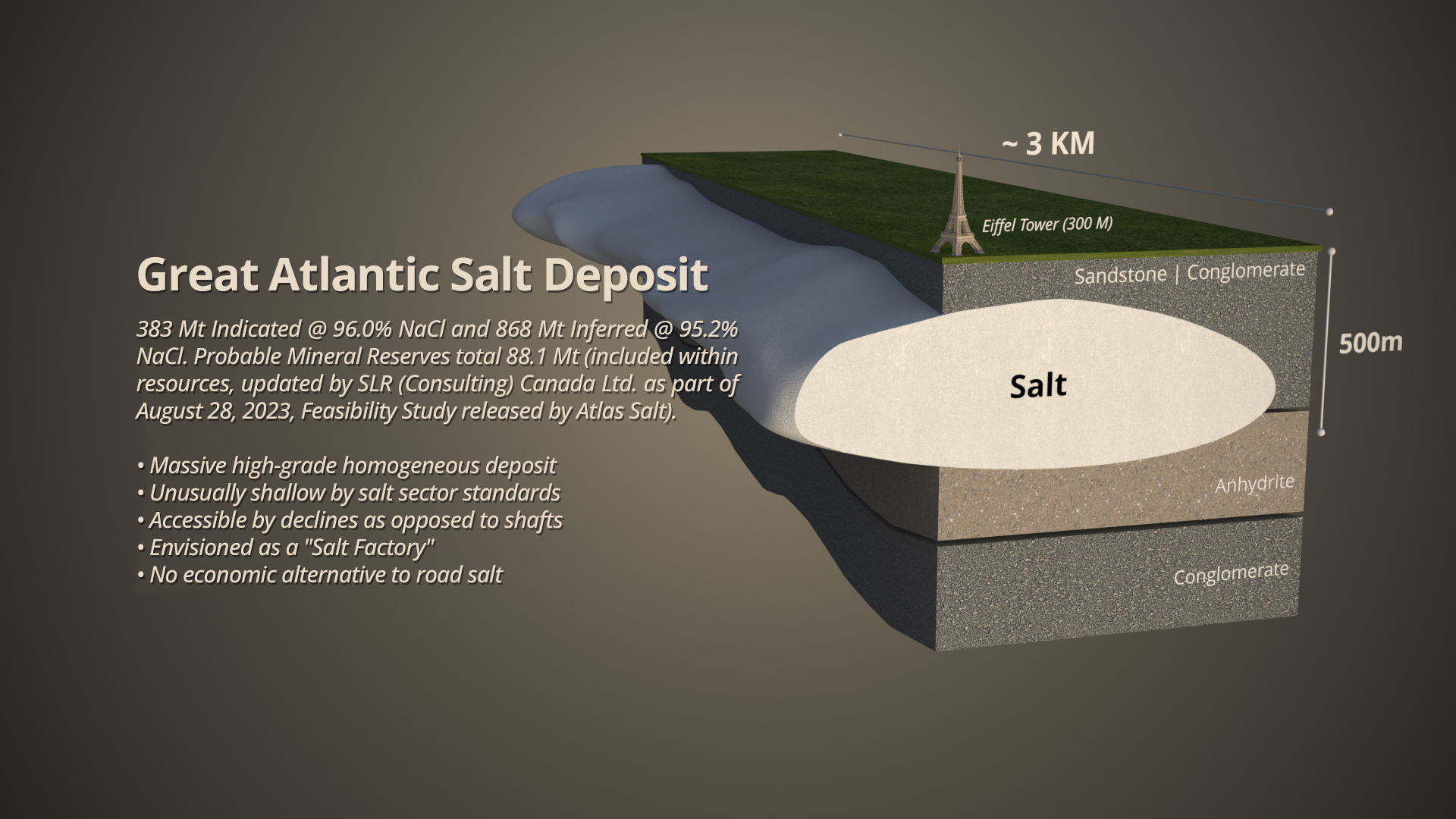

The Great Atlantic Salt Project is a proposed underground salt mine on the west coast of Newfoundland targeting de-icing road salt supply to northeastern North America, a market that is structurally import-dependent and exposed to supply disruption with every severe winter. The project holds an approved environmental assessment, probable reserves of 95 million tonnes at 95.9% NaCl, a total resource base of over 1.2 billion tonnes across three salt horizons, and no processing requirement. The ore is 96% pure at the face. There is no metallurgy. There is no recovery uncertainty. The two risks that remain are financing and construction execution, both real, but both generic to any large capital project, not unique to salt.

What Actually Matters

The first genuine value driver is the supply structure of the North American de-icing salt market. The continent's northeastern corridor, the highest-consumption zone, relies heavily on imported salt, primarily from Chile and the Caribbean. This creates a structural supply vulnerability that is exposed with each severe winter or vessel-chartering disruption. A domestically located, large-scale producer serving this corridor from Newfoundland is not merely a new entrant; it is a displacement play against a supply chain that is operationally brittle. The Great Atlantic project's location is not incidental - it is the asset.

The second driver is mine life and cash flow profile. A 25-year mine plan supported by 50 years of resource does something unusual: it decouples the standard relationship between production and value destruction. In a typical gold project, extracting the reserve is consuming the asset. In a salt deposit of this size and continuity, each year of production is better understood as collecting on a perpetuity with optionality. The reported life-of-mine average EBITDA would make this one of the most cash-generative industrial minerals operations in Canada on a per-dollar-of-capital-invested basis. That number requires scrutiny, but its order of magnitude is structurally credible given comparable operating salt mines globally.

The third driver, less obvious but equally important, is the potential financing structure. Management's argument that infrastructure-style lenders, not mining-sector project finance, may be the appropriate capital source deserves serious evaluation. If a lender concludes that the cash flow profile of a long-life, government-off-take-supported salt mine is sufficiently predictable to warrant infrastructure-rate debt rather than mining-rate mezzanine, the blended cost of capital improves materially. That outcome would itself be a significant re-rating signal. It hasn't happened yet. It may not. But the logic is coherent.

The forth value driver is the time-value arithmetic embedded in the rolling NAV. Most pre-production mining investments ask investors to discount a future cash flow stream at a rate that accounts for time and risk. Atlas Salt adds a dimension that most junior developers cannot offer: the NPV increases on its own as construction progresses and the first production year moves closer. An investor who buys at C$100M today and holds through a financing announcement, call it twelve to eighteen months, is not simply waiting for a re-rating. They are holding an asset whose intrinsic value is mechanically increasing. That is a fundamentally different risk-reward proposition than holding a junior gold developer through a development timeline where the NAV is static at best and eroding at worst as capital is consumed.

The fifth driver is the post-peak NAV decay rate. This is where the comparison with a conventional gold project is most instructive. The deck references New Found Gold's Queensway mine, where rolling NPV5 declines at roughly 30% per year after peaking in production year four because the mine is extracting its reserve and there is limited resource upside beyond the mine plan. Atlas Salt's rolling NPV8 declines at approximately 12% per year after its peak, because the discount rate unwinds more slowly over a 25-year mine life and accumulated net cash continues to grow. A shareholder in production year 10 owns C$2.8B of combined NAV. That is not a characteristic of a mining company. It is a characteristic of a long-dated infrastructure concession.

The final driver is valuation methodology. The feasibility study supports average life-of-mine EBITDA of C$325M and average FCF of C$188M. Applied to public comparable EV/EBITDA multiples, Compass Minerals trades at roughly 9x LTM EBITDA, that implies a steady-state valuation of approximately C$2.9B. A precedent transaction multiple of 12.5x, derived from the Stone Canyon/K+S Americas deal, implies C$4.1B. A 10% FCF yield implies C$1.9B. The range across all three methodologies is C$1.9B to C$4.1B. The current market cap is C$100M. That is not a small discount, it is a category error by the market, priced as though the project will never be built.

What Is Priced In

At C$100M and 0.11x UFS NPV8, the market is pricing Atlas Salt as though it carries the full risk profile of an early-stage junior miner with unresolved geology, contested permitting, and an uncertain commodity. None of those conditions apply. The environmental assessment is approved. The reserve grade is 95.9% NaCl with no processing. The customer base, municipal governments with legal procurement obligations, represents the closest thing to contracted off-take that exists outside a formal PPA. What the market is actually pricing, to the extent it has done the analysis at all, is financing risk and the unfamiliarity premium that comes with a niche commodity and a single public issuer in the space.

The Artemis Gold comparable in the deck are instructive precisely because they are grounded in actual market data rather than theoretical NAV frameworks. When Artemis began site construction in July 2022, it traded at 0.31x P/NAV, implying C$285M for Atlas on the same basis. When it secured project debt in March 2023, it re-rated to 0.45x, implying C$414M. At 59% construction completion it was at 0.55x, implying C$506M. At commercial production it reached 0.83x, implying C$764M. These are not aspirational figures. They are the documented re-rating path of a comparable development-stage miner. The starting point for Atlas on that same curve, at current pricing, implies the market assigns essentially zero probability to Atlas reaching the construction start milestone. That is an extreme position for a project with approved permits and a completed feasibility study.

The current valuation is not a fair reflection of risk-adjusted reality. It is a liquidity and awareness discount masquerading as a fundamental one. Ventum initiated coverage in March 2026. Before that, the stock had no institutional research support, no natural peer group for comparisons, and no sector rotation pulling generalist capital toward salt. Those conditions are beginning to change. The discount will not persist indefinitely once the financing process advances.

Where the Real Risk Sits

The key risk is not construction cost overruns, it is whether the financing can be structured at a cost of capital that preserves meaningful equity value. The feasibility study uses an 8% discount rate for the NPV8. If project lenders price this as a conventional mining credit, demanding 14–16% all-in cost of capital rather than the 8–10% that infrastructure-style financing would imply, the equity return compresses materially even if the project is built on time and on budget. The entire bull case for outsized equity returns rests on the assumption that lenders will look at the government-supported, zero-metallurgy, 25-year cash flow profile and categorise it differently from a gold mine. That categorisation test has not yet been passed. It is the single most consequential unknown in the investment case, and no amount of NAV arithmetic changes that.

Peer Comparison

There is no listed peer group that maps cleanly onto Atlas Salt at the pre-production stage, which is itself part of the problem. The integrated salt producers, Compass Minerals, K+S, trade on EBITDA multiples that reflect stable, utility-like cash generation. Junior gold and base metals developers trade at steep NAV discounts that reflect risks Atlas does not carry.

The honest positioning is that Atlas belongs in neither category. It is a development-stage asset whose cash flow profile, once operational, will look far more like Compass Minerals than like a junior gold mine, but it is currently priced as the latter. The gap between deserved categorisation and actual market placement is wide, and it closes only when either institutional capital begins to understand the distinction or a financing announcement forces the comparison to be made explicitly. The precedent transaction data, specifically the 12.5x Stone Canyon/K+S multiple, suggests that strategic acquirers already understand the categorisation correctly. Public market investors do not yet.

The "So What?"

The insight that the NAV grows by C$100M per year through the construction period is the most under-appreciated element of this investment case, and it changes the risk calculus in a specific way: time is not working against the equity holder here. In most junior mining investments, delay erodes value as capital is consumed and the project timeline extends. In this case, delay is broadly value-neutral or mildly value-positive because the NPV8 continues to accrete as the first production year approaches. That does not mean patience is free, dilutive equity financings are a real cost, and the opportunity cost of capital tied up in a pre-production stock is real, but it does mean the downside from waiting for the right financing terms is structurally lower than in comparable development plays.

The specific catalysts that would drive a re-rating, in descending order of impact: a project financing announcement (the primary trigger, with the lender category being the signal within it), the commencement of physical construction activity, and the continued build-out of institutional research coverage following Ventum's March 2026 initiation. Any one of these could move the stock meaningfully. All three arriving within an 18-month window would represent the conditions under which the Artemis Gold re-rating path becomes the base case rather than the bull case.

The conclusion is that this warrants serious attention, more so than the earlier analysis suggested, because the UFS NPV8 of C$920M is materially higher than the C$750M figure previously used, and the rolling NAV progression adds a dimension to the thesis that is genuinely differentiated. At C$100M with a C$920M NPV8, a C$1.9B peak total NAV, and a valuation range of C$1.9B to C$4.1B at steady state, the discount is not modest. It is structural, it is explicable, and it is the type that closes with milestones rather than narrative.

Five Key Takeaways

- The ability for the rolling NAV to grow approximately C$100M per year simply with the passage of time through construction, meaning the asset appreciates while the stock waits, a characteristic almost unique to long-life infrastructure-style projects.

- The FS NPV8 of C$920M means the stock trades at 0.11x its own feasibility-study value, a discount that would require metallurgical failure, permitting collapse, or commodity price destruction to be rational, none of which applies.

- Post-peak NAV declines at only 12% per year versus 30% for comparable gold mines, because 25-years of mine life combined with an NPV8 discount unwinds far more slowly than a front-loaded gold reserve.

- The three valuation methodologies, FCF yield, public comps EBITDA, and precedent transactions, produce a range of C$1.9B to C$4.1B at steady state; the current C$100M market cap sits below the floor of the lowest methodology by a factor of nineteen.

- Ventum's March 2026 initiation is the first institutional research coverage in the company's history; the absence of coverage was a structural cap on institutional awareness, and its removal is a necessary (though not sufficient) condition for re-rating.

The Investment Thesis for Atlas Salt

- Core opportunity: A long-duration infrastructure-quality asset trading at 0.11x its own feasibility-study NPV because it lacks a natural institutional audience, not because the project is impaired.

- Variant perception: The market treats this as a junior miner. The cash flow profile, C$325M avg LOM EBITDA, C$188M avg LOM FCF, 25-year mine life, government off-take, no commodity price volatility, is categorically closer to a utility concession.

- Time-value asymmetry: NAV could accrete ~C$100M/year through construction, meaning delay is far less value-destructive than in conventional development plays where capital burn erodes equity.

- Financing risk (primary): The thesis requires lenders to price this at infrastructure rates, not mining rates. This has not been demonstrated. It is the binary that determines the equity return range.

- Construction risk (secondary): Standard large-project execution risk, cost overruns, schedule delays, real but not unique to this asset.

- Key milestone 1: Project financing announcement, lender category (infrastructure vs mining) is the signal within the signal.

- Key milestone 2: Commencement of physical construction, which on Artemis Gold comps alone implies a re-rating to C$285M (0.31x NAV), a 2.85x from entry.

TL;DR

Atlas Salt trades at C$100M against a C$920M feasibility-study NPV8 and a peak total NAV of C$1.9B in production year four. The project has approved permits, 96% pure salt with no processing, and government municipal customers. The NAV grows ~C$100M per year simply with time. The stock is priced as though the project will not be built. The financing outcome, specifically whether lenders categorise this as infrastructure or mining, is the single event that determines whether the re-rating is 3x or 19x. It is worth a meeting, and the analytical work is straightforward: the only question that matters is the financing structure.

For the Low-Risk Investor - Conditions for Consideration

The entry point at 0.11x NPV8 is arithmetically compelling even for a conservative mandate, but the conditions for inclusion are narrow: a signed financing facility with a disclosed cost of capital below 11%, and ideally a lender profile (infrastructure fund, export credit agency, or investment-grade bank) that validates the infrastructure categorisation thesis. Until that document exists, the financing binary is too wide for a benchmark-sensitive portfolio, the downside scenario is not a loss of capital so much as an extended period of illiquidity in a stock with thin institutional sponsorship. The cost of waiting for confirmation is real: the Artemis Gold data suggests the re-rating at financing close is sharp and swift, and conservative allocators who wait for certainty will pay 0.45x NAV rather than 0.11x. Whether that cost is worth avoiding the binary is the decision. For a portfolio that can tolerate a small non-correlated position, a tracker allocation at current prices ahead of a financing announcement is defensible, the downside is bounded by a project with real assets and approved permits.

For the Higher-Risk Investor - Case for Moving Early

The framework for an early position requires three beliefs to hold simultaneously: that the C$920M NPV8 is a credible floor on intrinsic value (the feasibility study is NI 43-101 compliant and the deposit is straightforward); that at least one lender will reach the same infrastructure categorisation conclusion that the three valuation methodologies and the Stone Canyon precedent transaction already imply; and that the re-rating path from 0.11x to 0.31–0.45x NAV at financing close, potentially a 3–4x return, represents adequate compensation for the 12–18 month financing timeline and the binary outcome risk. The timing logic is specific: Ventum's initiation in March 2026 marks the beginning of institutional awareness, not the end of it. The widest information gap between public market pricing and fundamental value is likely now, before a second or third research house initiates, before the financing mandate is announced, and before a construction start forces the Artemis Gold comparison to be made in every junior mining newsletter in Canada. The signal that the thesis is wrong is not a delayed financing, it is a financing announcement at a double-digit cost of capital that implies lenders view the project as a conventional mining credit. That outcome would require a reassessment of the entire infrastructure framing. Everything short of that is noise.

Nolan Peterson, CEO of Atlas Salt

Analyst's Notes

Subscribe to Our Channel

Stay Informed