North American Salt: Structural Supply Deficits & Domestic Reindustrialization Are Reshaping an Industrial Market

North America’s salt deficit is driving demand for domestic supply, with logistics, policy support, and infrastructure-like demand reshaping the market.

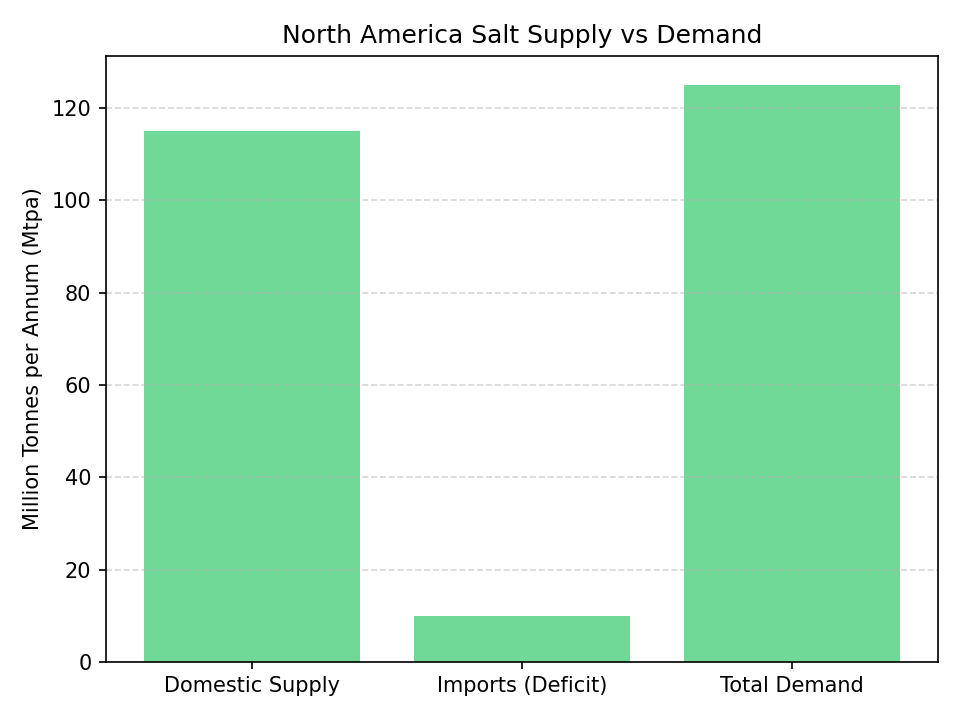

- North America carries a structural 8-10 million tonne per annum (Mtpa) salt supply deficit, creating measurable import dependency and logistical vulnerability across infrastructure and industrial systems.

- Domestic reindustrialization policy and "Buy North American" procurement directives are generating structural tailwinds for regionally positioned bulk commodity producers.

- Industrial salt demand is anchored in non-substitutable end markets, including the chlor-alkali chemical value chain and municipal water treatment, with the global market targeting approximately 5.8% compound annual growth rate (CAGR) through 2033.

- Delivered-cost competitiveness, not mine-gate economics alone, is determining pricing outcomes as logistics, weather volatility, and supply chain reliability command increasing premiums.

- Development-stage assets combining deep-water port access, sub-C$30 per tonne operating costs, and mine lives exceeding 50 years are attracting infrastructure-style capital on the basis of long-duration, stable cash flow profiles.

Constrained Supply and Inelastic Demand Support Sustained Salt Pricing

Salt receives limited analytical coverage despite serving as a non-substitutable input across multiple industrial processes, which results in persistent underpricing relative to its functional importance. North American supply has not added meaningful domestic production capacity for approximately 25 years, constraining supply elasticity and increasing reliance on imports during peak demand periods.

More than 50% of global salt demand feeds the chlor-alkali chain, producing chlorine, caustic soda, and soda ash, inputs required for water treatment, PVC production, pulp processing, and construction materials. Because these end uses are tied to population growth, industrial output, and regulatory standards for water quality, salt demand remains inelastic, limiting downside even in weaker economic cycles.

In North America, salt is also a critical input for road de-icing, where supply shortages translate directly into higher procurement costs and operational risk for municipalities. With domestic capacity stagnant, import dependence exposes supply to logistics disruptions and pricing volatility, particularly during severe winters. For investors, this combination of inelastic demand, constrained domestic supply, and policy support for local sourcing increases the probability of sustained pricing strength and margin expansion for domestic producers.

Regional Supply Security Over Global Cost Arbitrage

For two decades, commodity procurement in North America prioritized cost efficiency, with bulk materials like salt sourced from the lowest-cost global suppliers regardless of distance or delivery risk. That model is now being reconsidered.

Policy direction in both Canada and the United States is shifting toward domestic production, supply chain resilience, and infrastructure reliability. In salt markets, this is significant because logistics can outweigh production cost advantages, making nearby suppliers with port access and proximity to demand centers more competitive on a delivered-cost basis.

Salt markets are inherently regional, with limited ability to rebalance supply through global trade due to long shipping times. As a result, localized shortages can sustain price premiums. This is driving a valuation shift toward assets that offer regional supply security, faster delivery, and strategic positioning near end markets.

Understanding the Structural Supply Deficit in North America

North America imports 8-10 Mtpa of salt to meet de-icing demand in the northeastern United States and eastern Canada, reflecting a structural supply gap that has widened over ~25 years without significant new mine development.

This deficit is driven by aging domestic operations and limited project investment, as salt has historically been viewed as a low-growth, low-margin commodity. At the same time, demand has steadily increased due to municipal infrastructure spending, water treatment expansion, and chlor-alkali production growth.

Imported salt cannot fully replace domestic supply during peak demand due to long transit times and exposure to logistics and weather disruptions. In contrast, domestic producers near end markets offer faster, more reliable delivery, creating a durable opportunity to displace imports at competitive delivered costs.

Infrastructure-Like Characteristics of Salt Markets

Salt exhibits demand characteristics more commonly associated with regulated utilities than with cyclical commodities. Its two largest end markets, chlor-alkali chemical production and municipal water treatment, are structurally demand-inelastic. Chlor-alkali processes cannot substitute away from salt feedstock. Water treatment systems dependent on salt-based purification technologies have no operationally viable alternatives at scale.

Road de-icing demand is weather-sensitive but non-discretionary. Municipal procurement officers cannot defer purchase decisions when winter conditions require road treatment. This creates demand spikes that are non-negotiable from a timing standpoint, further reinforcing the premium placed on supply reliability over delivered-cost optimization alone. The global industrial salt market is projected to grow at approximately 5.8% CAGR through 2033, with North American demand supported by continued infrastructure investment and tightening environmental compliance requirements for water quality.

These demand characteristics support a framing more consistent with infrastructure than with resource extraction. Stable consumption patterns, non-substitutable end uses, and functionally required procurement create the conditions for predictable, long-duration revenue generation. This matters significantly for project finance structures, which depend on contracted or quasi-contracted offtake visibility.

Development-Stage Supply Response: Atlas Salt & the Great Atlantic Salt Project

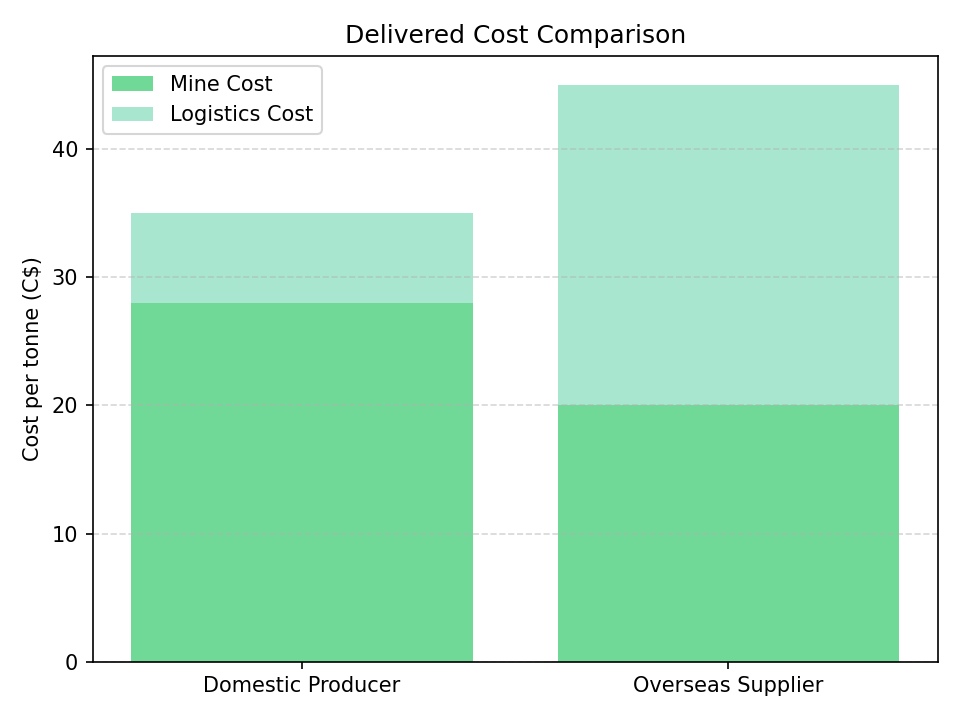

Atlas Salt is advancing the Great Atlantic Salt Project in Newfoundland, Canada, targeting North American import displacement with planned production of ~4 Mtpa,representing a meaningful portion of the structural supply gap. Its proximity (≈2 km) to a deep-water port enables delivery to the U.S. Northeast in ~3 days versus 14+ days for overseas supply, creating a clear advantage in reliability and delivered cost, particularly during peak demand periods.

The project’s feasibility study outlines strong economics, including a post-tax NPV (8%) of ~C$920 million and an IRR of ~21.3%, with operating costs around C$28/t FOB. The deposit grades ~95.9% NaCl, supports a ~24-year reserve life (with >50-year resource potential), and has already secured environmental approval while initiating early construction activities.

Nolan Peterson, Chief Executive Officer of Atlas Salt, highlights the project’s advanced stage and readiness:

"We have a feasibility study completed. We have an environmental assessment approved by the government. This is a project that's advanceable and it's ready."

Beyond the de-icing market, the project retains optionality toward higher-margin end markets including chlor-alkali chemical processing, agriculture, food-grade salt, and oil and gas applications. Peterson has identified the potential for incremental capital investment in processing infrastructure that would open access to these markets without requiring fundamental changes to the core mining operation. This optionality provides a secondary value pathway beyond the base case NPV.

Cost Curves, Logistics & the Emergence of Regional Pricing Power

Traditional mining analysis relies on global cost curves, but in salt markets this understates the advantage of regional producers. Because salt has a low value-to-weight ratio, logistics, freight, handling, and storage, form a significant portion of total delivered cost, not just mine-gate production.

A producer with ~C$28/t FOB costs and proximity to end markets can compete effectively against lower-cost international suppliers once freight and transit risks are factored in. This advantage strengthens during periods of high shipping costs or supply chain disruptions, while also enabling domestic producers to capture pricing premiums during short-notice demand spikes.

As a result, valuation frameworks should prioritize delivered-cost competitiveness rather than mine-site economics alone. The key metric is total cost to the customer, with assets that combine logistical efficiency and supply reliability holding durable, underappreciated advantages.

Structural Tailwinds for Domestic Supply

The policy environment in North America is increasingly supportive of domestic bulk commodity producers, with Canadian federal and provincial programs and U.S. procurement shifts favoring local supply over imports.

For Atlas Salt, this creates two key opportunities: access to government-backed financing through export credit agencies and development banks to reduce capital costs, and potential inclusion of salt in Canada’s critical minerals list, which would unlock additional policy support and funding access.

While these tailwinds do not change the underlying supply-demand dynamics, they improve financing conditions, lower investor risk, and enhance long-term offtake visibility, effectively strengthening project economics and risk-adjusted returns.

Conditions That Could Impair the Thesis

The North American salt thesis carries several key risks. Weather variability is the most immediate, as mild winters reduce de-icing demand and can materially impact short-term cash flows, though this is partly offset by exposure to industrial end markets with steadier demand.

On the execution side, permitting delays, construction cost inflation, and development risks can weaken project returns. Additionally, freight cost normalization could erode the delivered-cost advantage of domestic producers, while weaker industrial activity or policy shifts away from domestic sourcing could reduce demand and dampen long-term tailwinds.

The Investment Thesis for Salt

- North America's structural 8-10 Mtpa supply deficit provides long-term pricing support for domestic producers capable of displacing import volumes at competitive delivered costs.

- Demand is anchored in non-discretionary, non-substitutable end uses across the chlor-alkali value chain and municipal water treatment, supporting infrastructure-style revenue stability with low exposure to cyclical demand variability.

- Deep-water port-accessible assets targeting the northeastern United States market hold durable logistics advantages, including delivery timelines of approximately three days versus 14 or more days for overseas competitors, that compress delivered-cost differentials in favor of domestic producers.

- Reindustrialization policy and Buy North American procurement directives are generating incremental tailwinds for domestic bulk commodity supply chains, improving offtake visibility and the conditions for government-supported project financing.

- Development-stage assets with post-tax NPVs in the range of C$920 million, IRRs of approximately 21.3%, and mine lives exceeding 50 years are generating economics consistent with infrastructure-quality investments while trading at development-stage valuations.

- The optionality to access higher-margin chemical-grade and food-grade end markets through incremental processing capital provides a secondary value pathway beyond de-icing base case assumptions.

- Project de-risking milestones, including feasibility study completion, environmental assessment approval, and early works construction commencement, are systematically narrowing the discount applied by markets to development-stage net asset values.

Salt offers structural demand stability, non-substitutability in core industrial processes, and a supply-demand imbalance that has persisted without resolution for more than two decades.

Domestic reindustrialization policy, aging supply infrastructure, and rising logistical risk associated with import dependency are dictating how capital allocators assess regional bulk commodity producers. Assets positioned near end-market demand, with port-accessible logistics and long-life deposit profiles, are attracting institutional attention not as resource plays but as infrastructure-adjacent investments with predictable cash flow duration.

The North American salt market presents a defined and measurable opportunity. The supply deficit is structural, the demand base is non-discretionary, and the policy environment is moving in a direction that supports, rather than complicates, domestic project development.

TL;DR

North America faces a structural 8–10 Mtpa salt supply deficit driven by aging domestic capacity and rising demand from non-substitutable end uses like chlor-alkali and water treatment. This imbalance, combined with logistics constraints and policy support for domestic sourcing, is shifting market dynamics toward regional producers with strong delivered-cost advantages. Projects like Atlas Salt’s Great Atlantic Salt Project exemplify this trend, offering infrastructure-like economics, long-life assets, and the ability to displace imports while benefiting from improving financing conditions and policy tailwinds.

FAQs (AI generated)

The deficit stems from a lack of new mine development over the past ~25 years, combined with aging infrastructure at existing operations. While supply stagnated, demand continued to grow steadily due to infrastructure spending, water treatment expansion, and industrial chemical production. This imbalance has created a persistent reliance on imports that is structural rather than cyclical.

Imported salt faces logistical constraints, including long shipping times (often 10–14+ days), port congestion, freight cost volatility, and weather disruptions. These factors limit responsiveness during peak demand periods, especially for de-icing. As a result, domestic producers closer to end markets can deliver faster and more reliably, making them more competitive despite sometimes higher mine-gate costs.

Salt demand is anchored in non-discretionary and non-substitutable uses such as chlor-alkali chemicals and municipal water treatment. These applications are essential to public health, industrial production, and regulatory compliance, leading to stable, predictable consumption patterns. Even de-icing demand, while weather-sensitive, is operationally mandatory, reinforcing consistent long-term demand.

The key shift is from mine-gate cost competitiveness to delivered-cost competitiveness. Logistics now represent a significant portion of total cost, meaning proximity to end markets and port access can outweigh lower production costs overseas. Domestic producers also benefit from pricing power during demand spikes due to their ability to respond quickly to short-notice procurement needs.

Governments in North America are increasingly supporting domestic production through procurement preferences and financing mechanisms. Initiatives such as export credit financing and potential inclusion in critical minerals lists improve access to capital and reduce project risk. These policies enhance long-term offtake visibility and reinforce the structural shift toward regional supply security.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

%20(1).png)

Stay Informed