Battery Metals: Western Projects Attract Capital

Battery metals projects advance in Canada and Africa. Nickel, graphite, tin developers progress through permitting. Jurisdictional quality drives capital allocation.

- Congo's cobalt export restrictions removed 160,000-170,000 tonnes of intermediate material from global markets in 2025, driving cobalt hydroxide prices to parity with metal prices, a dramatic reversal from nine-year lows earlier this year and demonstrating how policy can create rapid price inflections in geographically concentrated commodities.

- Large-scale, low-risk nickel sulphide and graphite projects in established mining districts command strategic premiums as battery manufacturers seek supply diversification away from geopolitically sensitive jurisdictions, with infrastructure advantages and permitting certainty offsetting higher nominal operating costs.

- Multi-commodity projects with battery metals as by-products (graphite from rutile operations, PGMs from nickel sulphides) achieve first-quartile cost positions without capital-intensive downstream processing, providing resilience across commodity cycles while maintaining exposure to electrification demand.

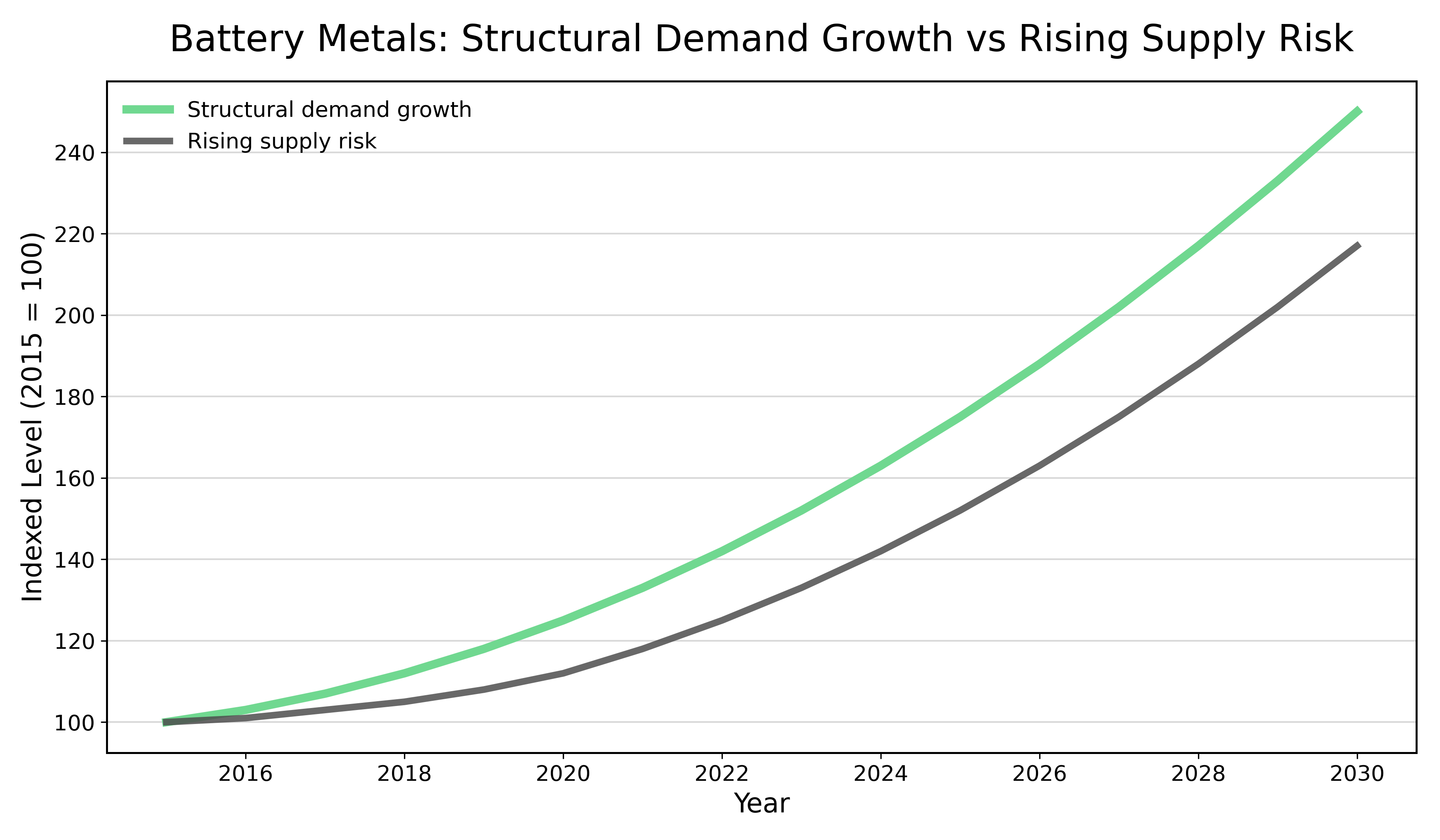

- EV penetration, grid-scale storage, and energy transition infrastructure drive multi-decade demand growth for nickel, cobalt, graphite, and copper, while supply increasingly concentrates in jurisdictions with rising royalties, export restrictions, and administrative complexity, creating sustained pricing support for new, large-scale developments.

- Challenging base metals capital markets favor projects advancing through permitting and engineering with clear pathways to construction financing, institutional support flowing to assets demonstrating technical de-risking, competitive economics, and embedded sustainability strategies aligned with decarbonization frameworks.

Battery Metals Supply Chain: How Policy Disruption & Structural Demand Are Reshaping Investment Opportunities

The global battery metals market entered a new phase in 2025, marked by supply disruptions, policy interventions, and renewed focus on Western-jurisdiction projects. Recent export restrictions in the Democratic Republic of Congo removed significant cobalt supplies from international markets, while large-scale nickel, graphite, and polymetallic projects advanced through permitting and financing milestones. These developments underscore a fundamental tension in battery supply chains: rapidly growing demand for electrification metals confronting geographically concentrated, politically sensitive supply sources.

For investors in the mining sector, this environment creates both risks and opportunities. Price volatility driven by policy uncertainty challenges short-term trading strategies, while structural demand growth supports long-term value creation for projects demonstrating technical validation, competitive cost positions, and jurisdictional stability. Understanding how these dynamics interact across different battery metals provides essential context for evaluating investment opportunities in a sector critical to the energy transition.

Company Case Studies: Battery Metals Developers Advancing Through Critical Milestones

The theoretical dynamics of battery metals markets become concrete when examining specific companies progressing through development stages. Four case studies illustrate distinct strategic approaches across the battery metals complex: Canada Nickel Company and Lifezones Metals advancing large-scale nickel sulphide development in established Canadian districts, Sovereign Metals pursuing graphite by-product strategy from primary rutile operations, and Rome Resources conducting polymetallic exploration targeting tin and copper systems. Each demonstrates different risk-return profiles, capital requirements, and pathways to value creation in an evolving battery materials landscape.

Canada Nickel: Carbon-Integrated Nickel Development

Canada Nickel Company represents one of the largest nickel sulphide developers globally, located in a well-established Canadian mining district with existing roads, rail, power, and skilled workforce. The company's flagship project demonstrates first-quartile net C1 cash costs and competitive all-in sustaining costs, with resilience across price cycles supported by scale and multi-commodity by-product credits including iron, chrome, and platinum group metals. Recent financing advancement provides capital for late-stage engineering, permitting, and financing negotiations ahead of a construction decision.

Mark Selby, CEO, Canada Nickel Company mentioned their next generation projects:

"Canada Nickel Company Inc. is advancing the next generation of nickel-sulphide projects to deliver nickel required to feed the high growth electric vehicle and stainless-steel markets."

The development strategy incorporates integrated carbon sequestration initiatives embedded in mine planning, with multiple pathways under evaluation to reduce or offset operational emissions, positioning the project for eligibility under government incentives and tax credits tied to clean technology and carbon capture frameworks. The long-term funding plan blends equity contributions, government incentives and refundable tax credits, export credit agency and institutional debt, and potential strategic and offtake-linked funding. The continued progress despite challenging nickel market conditions signals investor confidence in structural demand recovery driven by electric vehicle adoption and energy storage deployment, with sulphide projects offering longer mine lives, higher-grade resources, and lower carbon intensity that command strategic premiums as manufacturers seek secure, sustainable supply chains.

Lifezones Metals: Large-Scale Nickel District Development

Lifezones Metals closed a C$15.0 million bought-deal private placement in December 2025, with financing structured as equity units with attached long-dated warrants providing capital for advancement through late-stage engineering and permitting milestones. The project represents one of the largest nickel sulphide resources globally with long mine life supported by large reserves and resources, positioned in a well-established Canadian mining district with infrastructure advantages. The development incorporates multi-commodity by-product credits that materially enhance project economics, with bankable feasibility work demonstrating strong after-tax NPV and IRR.;

Ingo Hofmaier, Chief Financial Officer, Lifezone Metals shared their large-scale development:

"Following the successful completion of $75 million in capital raises in H2 2025, Lifezone has commenced execution readiness activities to advance and de-risk the project and prepare for full-scale execution."

The company maintains district-scale optionality through consolidation of a large nickel district with multiple ultramafic targets, with several resources already defined and additional estimates expected, supporting potential for district-scale growth beyond the flagship project and providing long-term upside beyond initial mine development. The integrated carbon sequestration initiatives and eligibility for government incentives tied to clean-technology frameworks enhance project competitiveness in a decarbonizing metals market, with the multi-source capital strategy reflecting modern mining project finance complexity where diverse financing structures enable large developments to advance, demonstrating continued institutional support in challenging base-metals capital markets.

Sovereign Metals: Graphite By-Product Economics

Sovereign Metals updated its corporate strategy in late 2025 to clarify its graphite by-product approach, with the project hosting world-class rutile mineralization where graphite is produced as a secondary product rather than the primary economic driver. This contrasts sharply with peers pursuing standalone graphite developments requiring significant capital for downstream anode processing facilities. The geological advantage stems from unique weathered, near-surface mineralization hosted in soft saprolite across a mineralised footprint exceeding 200 square kilometers, with simple processing producing higher purity graphite concentrate (96-98% carbon) while preserving medium, large, and jumbo flake sizes that command pricing premiums.

Frank Eagar, Managing Director & CEO, Sovereign Metals stated their graphite by-product approach:

“Sovereign intends to process the run-of-mine graphite in-country to produce a high-quality graphite product (96% C) suitable for major industry end markets including battery producers and refractory manufacturers.”

Critically, incremental graphite production costs sit materially below most global peers, approaching or undercutting weighted average Chinese production costs without exposure to opaque chemical processing markets or downstream execution risk. The strategy allows participation in battery materials upside through direct concentrate sales while maintaining flexibility to sell into higher-value traditional markets including refractories and foundries. This approach offers lower capital requirements compared to vertically integrated peers, enhanced resilience across commodity price cycles, and participation in battery materials growth without processing complexity.

The project's advancement toward definitive feasibility study completion, following successful pilot mining and processing programs, demonstrates technical de-risking with the strategy prioritizing capital discipline and risk control. The company completed an optimised pre-feasibility study with oversight from a technical committee, with demonstrated rehabilitation outcomes supporting environmental and permitting confidence, illustrating how by-product economics can achieve competitive cost positions while providing leverage to electrification demand.

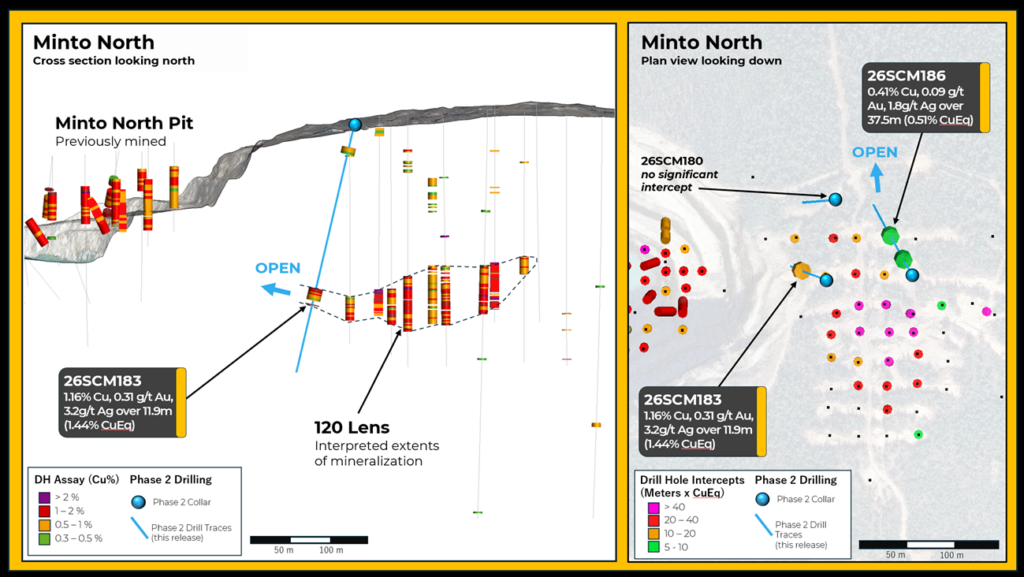

Rome Resources: Polymetallic Discovery Program

Rome Resources is advancing a polymetallic project in eastern Democratic Republic of Congo, identifying mineralized zones exceeding 200 metres in width across both polymetallic systems hosting tin, copper, zinc, and silver, and high-grade tin-dominant systems with structural similarities to nearby producing operations. The project sits in proximity to an established, world-class tin mining district, benefiting from demonstrated geological endowment and existing supply chain infrastructure including nearby airstrip access, heli-supported logistics, and permanent field camp.

Paul Barett, CEO, Rome Resources mentioned their discovery program:

"Drilled 26 core holes to date, a total of over 5,000m over 200m wide mineralization zone at Mont Agoma containing tin, copper, zinc and silver."

The company's strategic positioning emphasizes critical minerals exposure aligned with electrification and energy transition demand, with completion of a maiden mineral resource estimate targeted for 2025 representing transition from early-stage exploration toward resource definition. The company completed a reverse takeover and admission to public markets, raising capital across multiple financings to fund exploration and drilling while resolving historical licence and ownership issues, clearing the path for uninterrupted development. Metallurgical and beneficiation testing remains in progress, with bulk samples collected and shipped for analysis of recovery characteristics across tin, copper, and zinc, illustrating the polymetallic approach offering portfolio diversification across multiple commodity exposures within single operations, though jurisdictional considerations present execution risks that established mining activity nearby helps validate for technical and logistical feasibility.

Investment Implications: Supply Security & Capital Selectivity

The battery metals sector in late 2025 presents a complex investment landscape where policy-driven supply disruptions in cobalt markets created sharp price increases disconnected from underlying demand fundamentals, large-scale nickel and graphite projects advanced through permitting despite weak near-term pricing, and polymetallic discovery programs continued expanding resource footprints in strategic commodities. Several themes emerge for investors evaluating battery metals exposure: jurisdictional premiums are real and persistent as projects in established mining districts command valuation premiums; by-product economics matter more in capital-constrained markets as projects generating battery metals as secondary products achieve competitive cost positions; and sustainability credentials drive strategic value as embedded carbon intensity becomes a core competitive differentiator.

For investors considering battery metals exposure, these dynamics suggest favoring developers with large resources in established jurisdictions, advancing through systematic de-risking milestones, with clear pathways to construction financing. Scale and mine life attract institutional capital while technical de-risking through progression from exploration through resource definition, feasibility studies, and permitting creates systematic risk reduction that captures value even in weak commodity price environments. While exploration success creates optionality, conversion of resources to reserves and progression toward production decisions drive sustained value creation.

The battery metals supply chain faces fundamental tension between growing demand for electrification and geographically concentrated, politically sensitive supply, creating price volatility, policy risk, and supply uncertainty but also investment opportunities for projects positioned to deliver secure, sustainable supply. Understanding these dynamics, evaluating technical validation and jurisdictional positioning, and maintaining discipline on entry points will determine investment success as the electrification transition accelerates, with the structural demand case remaining compelling but requiring rigorous evaluation of jurisdiction, scale, cost position, and execution capability to convert demand into shareholder returns.

The Investment Thesis for Battery Metals

- Diversify across the battery metals complex rather than single-commodity concentration, as nickel, graphite, tin, and copper each face distinct supply-demand dynamics and policy risks that create portfolio resilience when exposure spans multiple battery inputs.

- Prioritize large-scale, long-life assets in established jurisdictions over high-grade, short-life deposits in frontier regions, where infrastructure advantages, permitting certainty, and access to skilled workforces justify valuation premiums despite potentially higher nominal operating costs.

- Favor developers advancing through systematic de-risking over early-stage explorers or pre-production stories without clear financing pathways, as projects demonstrating execution momentum through resource conversion, feasibility completion, and strategic funding capture value even in weak commodity price environments.

- Consider by-product exposure for cost-curve advantages and cycle resilience, where companies generating battery metals as secondary products from primary commodity operations achieve lower operating costs and maintain cash flow leverage to electrification upside while limiting downside risk.

- Evaluate sustainability credentials as strategic differentiators rather than peripheral ESG considerations, since embedded carbon intensity, renewable energy integration, and community engagement increasingly determine access to capital and offtake agreements with battery manufacturers facing supply chain scrutiny.

- Monitor policy developments in producing jurisdictions as leading indicators of supply disruption risk, because export restrictions, royalty increases, and administrative requirements can rapidly tighten markets and create price spikes that disproportionately benefit companies with diversified supply or domestic processing capabilities.

- Maintain discipline on entry points despite compelling structural demand narratives, as EV adoption and energy storage support multi-decade battery metals growth but near-term oversupply can persist for extended periods requiring patient capital allocation to technically validated assets rather than speculative positioning.

Battery metals supply chains entered a critical transition phase in 2025, marked by geographic concentration risks and renewed focus on Western-jurisdiction development projects. Large-scale nickel, graphite, and polymetallic projects advanced through permitting and financing milestones despite near-term price headwinds, demonstrating investor confidence in structural demand recovery. For investors, this environment rewards selectivity: favoring large, long-life resources in established jurisdictions; prioritizing developers demonstrating systematic technical de-risking; and recognizing that sustainability credentials and by-product economics increasingly differentiate winners from a crowded field of battery metals aspirants. The structural demand case for electrification metals remains compelling, but conversion of that demand into shareholder returns requires rigorous evaluation of jurisdiction, scale, cost position, and execution capability.

TL;DR

Battery metals markets in 2025 saw large-scale nickel sulphide projects from Canada Nickel Company and Lifezones Metals secure financing and advance through permitting in established Canadian districts, demonstrating investor confidence in structural demand recovery driven by electric vehicle adoption. Sovereign Metals emphasized graphite by-product economics over capital-intensive downstream processing, achieving competitive cost positions without processing risk exposure through unique geological advantages and simple processing flowsheets. Rome Resources expanded polymetallic resource footprints hosting tin, copper, and zinc through systematic drilling programs in strategic African locations. For investors, the environment favors selectivity: large resources in established jurisdictions, systematic technical de-risking, and embedded sustainability strategies differentiate winners. Projects incorporating carbon sequestration, renewable energy integration, and eligibility for government clean technology incentives command strategic premiums as battery manufacturers seek secure, sustainable supply chains with lower embedded carbon intensity.

FAQs (AI-Generated)

Large-scale nickel sulphide developers secure financing and progress through permitting because institutional investors differentiate between near-term Indonesian laterite oversupply and long-term structural EV demand, favoring projects with longer mine lives, higher-grade resources, lower carbon intensity, valuable by-product credits, and eligibility for government clean technology incentives.

Single-commodity developers provide pure price exposure advantageous for high-conviction positioning but create concentrated risk, while polymetallic projects offer diversification across multiple metals within single operations providing cycle resilience though introducing processing and marketing complexity that by-product economics can address through first-quartile cost positions without requiring strength across all commodities.

Jurisdiction fundamentally impacts project risk profiles through infrastructure advantages, permitting certainty, skilled workforces, and stable regulatory frameworks in established mining districts that justify valuation premiums over frontier regions despite higher nominal costs, with policy stability in Western jurisdictions providing predictable development timelines and better access to project financing.

Sustainability credentials evolved from peripheral ESG considerations to core competitive differentiators determining capital and offtake access, as battery manufacturers face supply chain carbon intensity scrutiny creating preferences for suppliers demonstrating emissions reductions through carbon sequestration, renewable energy integration, and robust community engagement that can materially improve project economics through government incentives and tax credits.

By-product strategies achieve lower operating costs by spreading fixed costs across multiple revenue streams, provide resilience during commodity price weakness through diversified cash flows, avoid capital-intensive downstream processing requirements, and maintain optionality to sell into traditional industrial markets while capturing battery materials upside without dependency on single commodity price performance.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed