China Export Controls & Western Industrial Policy Reprice Critical Minerals as Strategic Supply Chain Assets

China export controls and Western policy are reshaping critical minerals markets, driving premium valuations for secure non-Chinese supply chains.

- Bloomberg Intelligence projects neodymium-praseodymium and heavy rare earth pricing to remain fragmented between Chinese domestic markets and ex-China markets through 2030, with magnet feedstock shortages persisting for buyers restricted from Chinese supply under Section 30D Foreign Entity of Concern provisions.

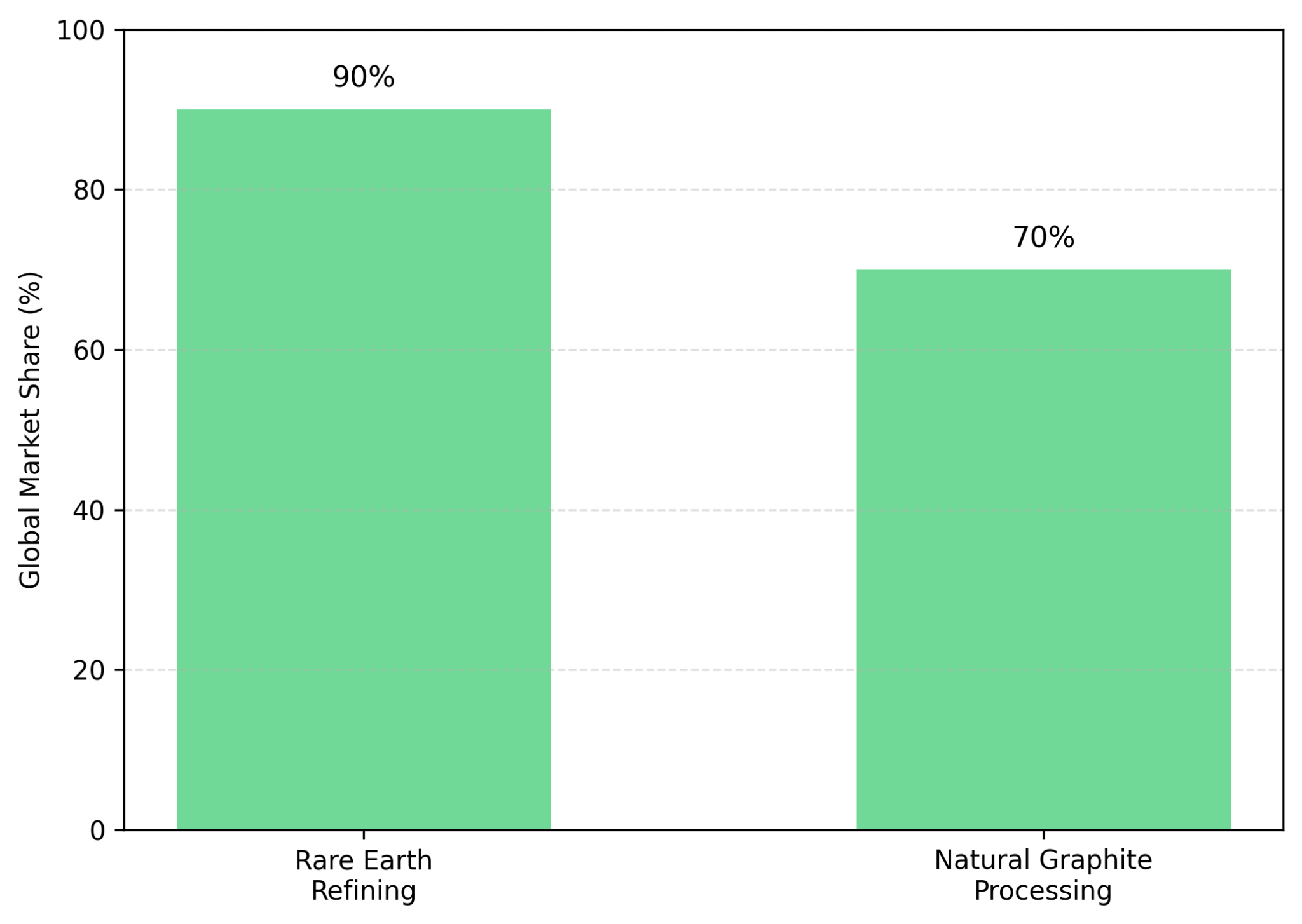

- China retains approximately 90% of global rare earth refining capacity and approximately 70% of natural graphite processing capacity per the International Energy Agency 2024 Critical Minerals Outlook, concentrating supply chain risk for Western original equipment manufacturers.

- The US-European Union 2025 critical minerals coordination plan and Chinese Ministry of Commerce export controls expanded between October 2023 and December 2024 are channelling sovereign-backed financing and offtake commitments to developers in OECD jurisdictions.

- Equity placements across 2024 and 2025 concentrated in developers with completed definitive feasibility studies, secured infrastructure access, and confirmed strategic partners, with junior explorers without these factors underperforming the VanEck Rare Earth and Strategic Metals ETF benchmark.

- Investors evaluating exposure should screen for definitive feasibility study economics with named source documents, permitting status within stated regulatory windows, and offtake routes qualifying under Section 30D Foreign Entity of Concern compliance.

Critical Minerals Are Becoming a Geopolitical Asset Class

Rare earths outlook in 2026 projects neodymium-praseodymium (NdPr), terbium, and dysprosium pricing to remain fragmented between Chinese domestic markets and ex-China markets through 2030. Magnet feedstock shortages will persist for buyers restricted from Chinese supply under United States Inflation Reduction Act Section 30D Foreign Entity of Concern provisions and European Critical Raw Materials Act sourcing requirements adopted in March 2024. The financial consequence is that equity valuations for developers operating outside Chinese-controlled refining now incorporate a price differential that spot-price models referencing Shanghai Metals Market or Asian Metal indices do not capture.

China retains approximately 90% of global rare earth refining capacity and approximately 70% of natural graphite processing capacity. Three policy mechanisms are redirecting capital flows: Chinese Ministry of Commerce export licensing on dysprosium, terbium, and graphite anode material introduced between October 2023 and December 2024; US Department of Defense direct purchase commitments for non-Chinese rare earth oxides under Defense Production Act Title III; and Inflation Reduction Act Section 45X advanced manufacturing production credits providing direct revenue support to qualifying battery components and critical minerals produced in the US.

Mark Chalmers, Chief Executive Officer of Energy Fuels, argues that fragmented supply chains cannot meet Western industrial policy objectives at commercial scale:

“The world wants to see fast and quick solutions, and you don't get there with a fragment.”

Western Industrial Policy Is Repricing Strategic Mineral Supply Chains

The framework parallels semiconductor reshoring under the 2022 CHIPS and Science Act, which committed approximately $52 billion in direct funding to US-based fabrication, and LNG energy security alignment following the 2022 European supply shock. The mechanism in critical minerals is functionally identical: targeted government intervention establishes preferential demand and financing channels for assets located within aligned jurisdictions, repricing those assets relative to lowest-cost global supply.

The US & European Union Alignment Changes Capital Flows

The US and European Union announced expanded coordination on critical minerals in 2025 under the Minerals Security Partnership framework, building on the 2023 European Critical Raw Materials Act and the 2022 United States Inflation Reduction Act. The action plan includes coordinated procurement under Defense Production Act Title III, aligned subsidy frameworks under Section 45X, and streamlined investment review for projects within OECD jurisdictions. Projects qualifying for Section 30D consumer credit eligibility, satisfying Critical Raw Materials Act sourcing thresholds, and operating within stable permitting regimes are eligible for sovereign-backed financing through Export Development Canada, the US Export-Import Bank, and the European Investment Bank.

Eligibility differentiation is observable in 2024 and 2025 equity placements, where developers with confirmed Section 30D-compatible offtake agreements priced placements at narrower discounts to spot than developers without such agreements. Strategic partner participation, including original equipment manufacturer prepayments and sovereign wealth fund cornerstone allocations, concentrated in this same tier of developers.

China's Export Controls Reinforce the Scarcity Narrative

Beijing has progressively expanded its export control regime since 2023. Restrictions now cover heavy rare earths including dysprosium and terbium, graphite anode material, lithium-ion battery production technologies, and neodymium-iron-boron magnet manufacturing equipment. Heavy rare earths matter to investors because dysprosium and terbium are required to maintain magnet coercivity above 150 degrees celsius operating temperatures in electric vehicle traction motors, aerospace actuators, and guided defense platforms

Energy Fuels' White Mesa Mill in Utah operates as the only commercial-scale separated rare earth oxide facility in the US, with pilot production of separated terbium and dysprosium oxides confirmed in 2024 company filings. The company is integrating uranium concentrate, separated rare earth oxides, and heavy mineral sands processing within a single critical minerals platform addressing midstream gaps in Western supply chains.

Nickel Markets Are Shifting From Oversupply to Strategic Security

Investor focus across 2024 and 2025 was dominated by Indonesian nickel oversupply and London Metal Exchange (LME) Class 1 nickel prices that traded below $16,000 per tonne for sustained periods, contributing to the suspension of higher-cost Western operations including BHP's Nickel West announced in 2024. A second pricing dynamic has now emerged for nickel sulphate qualifying under Inflation Reduction Act Section 30D Foreign Entity of Concern restrictions. US automakers seeking the $7,500 consumer tax credit cannot source from entities with 25% or greater Chinese ownership, creating a separate procurement pool with measurable price differentiation from unrestricted LME-grade supply.

Indonesia's Dominance Creates Structural Risk

Indonesia produced approximately 60% of global nickel mine supply in 2024 per the US Geological Survey 2025 Mineral Commodity Summaries published in January 2025, with current expansion targeting 75% to 80% of global supply by 2030. The Indonesian government implemented royalty restructuring under 2025 mining law amendments, tightened permitting for new smelter capacity, and introduced selective export licensing for nickel matte and mixed hydroxide precipitate.

Section 30D Foreign Entity of Concern restrictions disqualify Indonesian nickel processed under Chinese ownership thresholds from US consumer tax credit eligibility, creating a measurable price separation between unrestricted LME-grade nickel and Section 30D-compliant material delivered to North American battery manufacturers.

Why Sulphide Nickel Projects Are Regaining Strategic Importance

Sulphide nickel deposits offer lower carbon intensity processing, established hydrometallurgical and pyrometallurgical pathways to battery-grade nickel sulphate, and capital expenditure profiles distinct from laterite high-pressure acid leach (HPAL) projects that have experienced cost overruns at multiple Indonesian operations. Canada Nickel's Crawford project in the Timmins, Ontario mining district holds a measured and indicated resource base reported under National Instrument 43-101 standards in the company's 2023 Feasibility Study, with integrated mineral carbonation in tailings providing carbon sequestration. Lifezone Metals' Kabanga project in Tanzania holds higher-grade sulphide mineralisation than typical sulphide deposits, with the company targeting in-country hydrometallurgical refining to produce LME-grade nickel and cobalt rather than exporting concentrate.

Mark Selby, Chief Executive Officer of Canada Nickel, ties the Crawford development pathway to district-level production scaling:

“Over a 10- or 15-year period, you could potentially reach 250,000 to 300,000 tons of nickel coming out of this district.”

Ingo Hofmaier, Chief Financial Officer of Lifezone Metals, on the processing differentiation that European buyers will price under the Carbon Border Adjustment Mechanism:

“Hydromet would be cleaner, definitely far lower in terms of emissions, while also offering high recovery rates.”

Graphite & Titanium Are Emerging as Strategic Bottlenecks

Graphite accounts for approximately 95% of anode mass in lithium-ion batteries by composition. Announced North American battery cell capacity is targeting more than 1,000 GWh by 2030 per Benchmark Mineral Intelligence assessments, against a non-Chinese spherical purified graphite anode supply base producing under 5% of global volumes in 2024. The supply gap is being addressed through Section 45X production credits for qualifying graphite anode material produced in the US, Section 232 tariff investigations on Chinese anode imports initiated in 2024, and procurement preference under Defense Production Act allocations.

Western Governments Are Moving Beyond Lithium

The US Department of Energy designated graphite and titanium as critical minerals in the 2023 Critical Materials List, and the European Union included both in the 2023 Critical Raw Materials Act strategic raw materials list. The US imports approximately 100% of its titanium sponge requirements per the 2024 USGS Mineral Commodity Summaries. China controls approximately 65% of natural graphite mine supply and over 90% of spherical purified graphite anode processing globally per the International Energy Agency 2024 Critical Minerals Outlook.

Low-Cost Non-Chinese Supply May Command Strategic Premiums

Sovereign Metals' Kasiya project in Malawi reported a 2024 Pre-Feasibility Study post-tax net present value (NPV) of $1.6 billion at an 8% discount rate and a post-tax internal rate of return (IRR) of 28%, with project economics anchored by rutile, the titanium dioxide feedstock used in pigment and metal applications, as the primary revenue driver. Graphite is produced as a co-product at an incremental cash cost of $241 per tonne per the same study. Rio Tinto invested $60 million in 2023 for a 19.9% interest, and a joint Definitive Feasibility Study is currently advancing under the Joint Ore Reserves Committee (JORC) reporting standards.

Ben Stoikovich, Chairman of Sovereign Metals, identifies the cost-curve positioning that separates Kasiya from competing non-Chinese graphite projects:

“Many non-Chinese graphite projects are struggling. They’re simply too high on the real cost curve.”

Institutional Capital Is Becoming More Selective Across the Critical Minerals Space

Junior exploration equities with critical minerals exposure but without bankable feasibility studies, infrastructure access, or offtake visibility underperformed the VanEck Rare Earth and Strategic Metals ETF benchmark across 2025. Institutional placements concentrated in a narrower set of developers meeting defined screening criteria.

The screening criteria institutional allocators apply include completed definitive feasibility studies with disclosed sensitivity tables, permitting visibility within stated regulatory windows, infrastructure access including grid power, water rights, and transportation corridors, ESG compliance with International Finance Corporation Performance Standards, and downstream integration into refining or processing capacity. Lifezone Metals completed equity placements supported by institutional investors and government-backed development finance through 2024 and 2025, with proceeds directed to Kabanga feasibility advancement. Canada Nickel has secured both federal and provincial Canadian government endorsements for Crawford. Sovereign Metals' resource confidence has progressed through the joint Rio Tinto pilot program, with measured and indicated resources expanding through feasibility-stage drilling.

The Investment Thesis for Critical & Battery Metals

- Projects positioned outside Chinese-controlled refining ecosystems with offtake routes qualifying under Inflation Reduction Act Section 30D Foreign Entity of Concern restrictions and European Critical Raw Materials Act sourcing thresholds

- Developers with completed definitive feasibility studies, advanced permitting status within stated regulatory windows, secured infrastructure access, and confirmed offtake or strategic partner agreements supporting financing visibility

- Sulphide nickel projects with lower carbon intensity processing relative to Indonesian laterite high-pressure acid leach supply, positioned to qualify under European Carbon Border Adjustment Mechanism reporting requirements that began transitional implementation on 1 October 2023

- Rare earth and graphite projects aligned with Defense Production Act Title III procurement, Section 45X advanced manufacturing production credits, and Critical Raw Materials Act strategic project designation

- Producers and developers integrating downstream into refining, separation, hydrometallurgical processing, or recycling rather than exporting unprocessed concentrate to Chinese refiners

Pricing power and equity multiples now incorporate geopolitical alignment, downstream processing capability, and industrial policy support. Bloomberg Intelligence's projection of rare earth pricing fragmentation through 2030, combined with the US-European Union 2025 critical minerals coordination plan and the Chinese export-control expansion announced through December 2024, defines a market structure where Section 30D-compliant supply commands measurable price differentiation from unrestricted material.

TL;DR

Critical minerals have moved from cyclical commodity pricing to geopolitically differentiated pricing. Bloomberg Intelligence projects rare earth fragmentation through 2030. Chinese Ministry of Commerce export controls expanded between October 2023 and December 2024 to cover dysprosium, terbium, graphite anode material, and magnet manufacturing technologies. Indonesia produced approximately 60% of 2024 global nickel mine supply per the USGS 2025 Mineral Commodity Summaries, with concentration targeting 75% to 80% by 2030. Section 30D Foreign Entity of Concern restrictions create a separate procurement pool for Western buyers, repricing supply outside Chinese-controlled processing.

FAQs (AI-generated)

Critical minerals are no longer valued purely on commodity pricing cycles because governments now view them as strategic assets tied to energy security, defense, and industrial competitiveness. Chinese export controls, Western subsidy programs, and sourcing restrictions under the US Inflation Reduction Act and European Critical Raw Materials Act are reshaping capital flows and creating pricing premiums for supply chains outside China-controlled processing networks.

China controls most global rare earth refining and graphite processing capacity, giving it significant leverage over downstream supply chains. Export restrictions on materials such as dysprosium, terbium, graphite anode material, and magnet technologies have tightened supply availability for Western manufacturers, accelerating investment into alternative refining and mining projects in OECD-aligned jurisdictions.

Sulphide nickel projects are increasingly viewed as strategically valuable because they offer lower-emission processing routes and are better positioned to produce battery-grade nickel sulphate that complies with Section 30D Foreign Entity of Concern requirements. Investors are prioritizing projects with feasibility studies, infrastructure access, and downstream processing integration as Western automakers seek compliant supply chains for electric vehicle tax credit eligibility.

Western governments are actively supporting critical minerals projects through subsidies, export credit financing, procurement commitments, and industrial policy initiatives. Programs tied to the Defense Production Act, Section 45X manufacturing credits, and the Minerals Security Partnership are helping developers secure funding, strategic partnerships, and offtake agreements, particularly for projects located in politically aligned jurisdictions.

Institutional investors are focusing on developers with completed definitive feasibility studies, advanced permitting progress, secure infrastructure access, ESG compliance, and confirmed strategic partners or offtake agreements. Markets are rewarding projects capable of integrating into downstream refining or processing chains rather than companies solely exporting raw concentrate into China-dominated supply systems.

Analyst's Notes

Subscribe to Our Channel

Stay Informed