Copper Investment Opportunity: Why Smart Money is Betting on Red Metal Companies

Copper demand will double by 2050 from EVs/renewables while ore grades decline 40%. Quality developers in Canada/Chile offer 3-5x leverage to the red metal bull market.

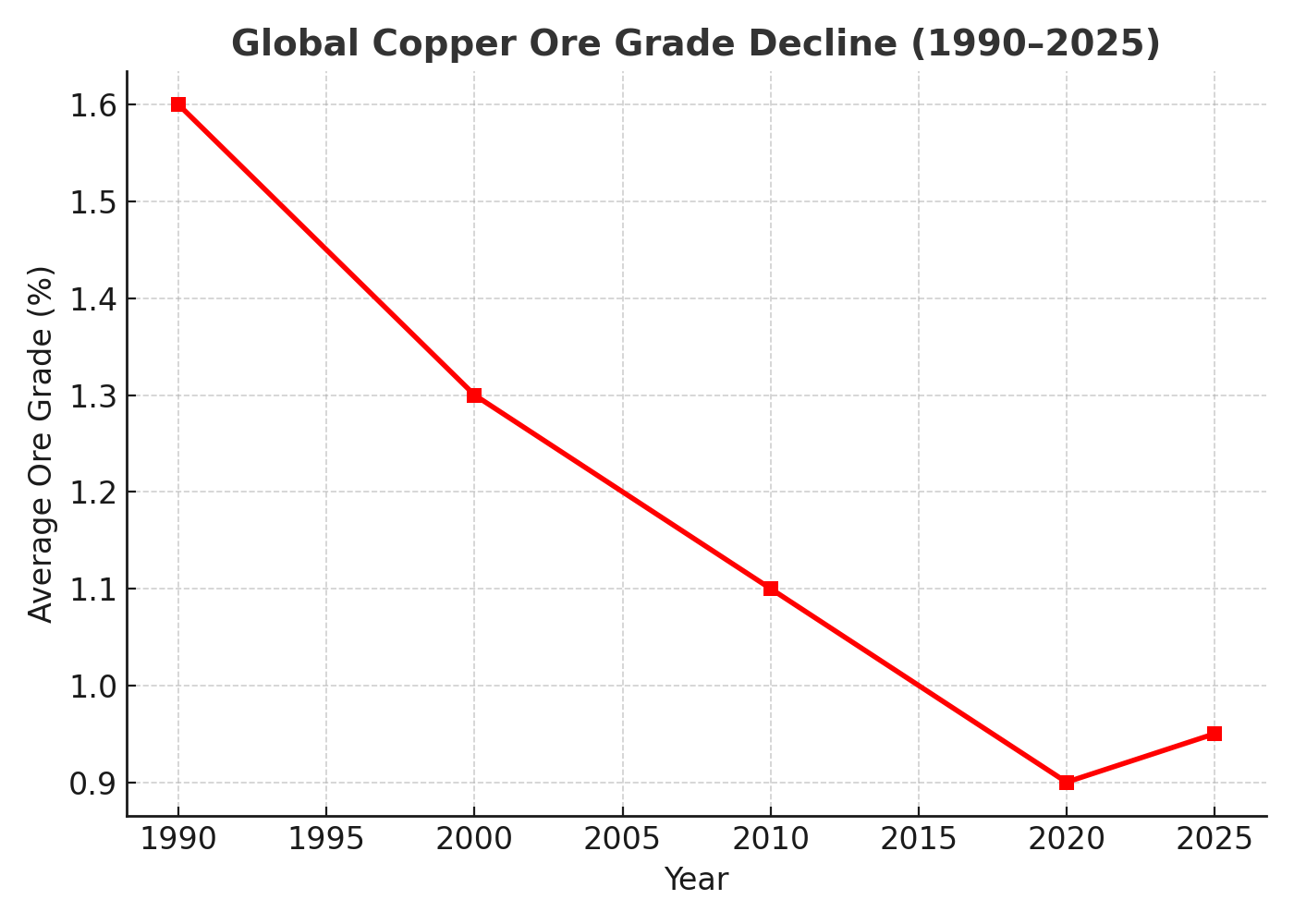

- Copper supply faces a structural crisis as ore grades have declined 40% since 1990 while exploration budgets dropped to just 28% of historical levels (previously 50-60%), creating severe supply deficits as development timelines have extended by 4+ years since 2005 due to regulatory and environmental complexities.

- Global copper demand is projected to double to 40 million tonnes per year by 2050, driven by electrification trends including electric vehicles that require 4x more copper than traditional cars, renewable energy infrastructure expansion, grid modernization requirements, and the massive power demands of AI and 5G data center development.

- Geographic risk concentration has become a critical factor as over 60% of global copper supply comes from politically unstable regions, creating significant premiums for projects in Tier-1 jurisdictions like Canada, Chile, and Australia where companies such as Gladiator, Marimaca, and Fitzroy operate with lower political and regulatory risks.

- Rising capital intensity and stringent ESG requirements now favor established operators with existing infrastructure access and strong community partnerships, as demonstrated by Marimaca's proximity to seawater and power infrastructure and Gladiator's established relationships with First Nations communities.

- Major mining companies including BHP, Rio Tinto, and Freeport are aggressively acquiring copper assets as organic growth options diminish, creating a highly competitive M&A environment that drives premium valuations for quality development-stage projects with defined resource bases and clear development pathways.

The global economy stands at a critical inflection point where copper—the "metal of electrification"—has emerged as perhaps the most compelling investment theme of the decade. As governments worldwide accelerate decarbonization efforts and artificial intelligence reshapes energy infrastructure, copper demand is poised for unprecedented growth while supply faces mounting structural challenges.

Recent corporate presentations from emerging copper companies reveal a market dynamic that should capture every serious investor's attention. From Canada's Yukon Territory to Chile's Atacama Desert, a new generation of copper developers is positioning to capitalize on what industry experts describe as a once-in-a-generation supply-demand imbalance.

The Electrification & Transportation Revolution Driving Massive Copper Demand

.png)

The automotive industry's electric transformation represents copper's most visible demand driver. Electric vehicles require approximately four times more copper than traditional internal combustion engines—typically 80-185 pounds per EV compared to 50 pounds for conventional vehicles. With global EV sales projected to reach 30 million units by 2030, this single sector will consume an additional 2.4 million tonnes of copper annually.

Tesla's success has catalyzed every major automaker to electrify their fleets. General Motors pledged $35 billion toward electric vehicles through 2025, while Ford committed $50 billion through 2026. This corporate commitment, backed by government mandates in California, Europe, and China, creates an inexorable demand trajectory that traditional copper supply cannot satisfy.

Grid Infrastructure & Renewable Energy Expansion

The electrical grid modernization required to support renewable energy and EV charging infrastructure represents an even larger copper consumption driver. Wind turbines require 4-15 tonnes of copper each, while solar installations consume significant copper for wiring and grounding systems. The International Energy Agency estimates that achieving net-zero emissions by 2050 will require global copper consumption to increase by 70%.

Smart grid technologies and battery storage systems add additional layers of copper demand. Tesla's Megapack battery installations, for example, require substantial copper infrastructure for power conditioning and grid integration. As utilities worldwide upgrade aging electrical systems to accommodate bidirectional power flows and distributed generation, copper consumption will accelerate beyond current projections.

Data Centers & AI Infrastructure

Artificial intelligence and cloud computing have created an unexpected copper demand surge. Advanced data centers require sophisticated cooling systems, backup power infrastructure, and high-capacity electrical distribution—all copper-intensive applications. NVIDIA's latest AI chips and training systems demand 10-20 times more power than traditional computing, translating directly into copper consumption for supporting infrastructure.

Critical Supply Challenges & Declining Ore Grades Threaten Market Balance

The copper mining industry faces a fundamental challenge: ore grades have declined 40% since 1990 as easily accessible, high-grade deposits become exhausted. Major producing mines like Chile's Escondida and Peru's Cerro Verde process increasingly lower-grade ores, requiring more energy and infrastructure investment to maintain output levels.

This grade decline particularly impacts operating costs and environmental footprints. Processing lower-grade ores requires more water, energy, and waste rock management, creating sustainability challenges that further complicate project development. Companies like Marimaca Copper Corp have gained competitive advantages by identifying higher-grade oxide deposits that can be processed through environmentally favorable heap leaching rather than energy-intensive flotation.

Extended Development Timelines Limit New Supply

Mining development timelines have extended by an average of four years since 2005, according to industry data. Environmental permitting, community consultation, and infrastructure development now require decade-long processes that delay supply responses to price signals. BHP's Resolution Copper project in Arizona exemplifies these challenges—despite containing enough copper to supply 25% of U.S. demand, legal and regulatory hurdles have delayed development for over a decade.

This timeline extension particularly impacts investor returns and project financing. Companies must now plan 15-20 year development horizons while managing political, environmental, and commodity price risks. Only the most robust projects with exceptional economics can attract the multi-billion dollar investments required for world-class copper mines.

Exploration Budget Constraints Limit Discovery Pipeline

Mining companies have reduced exploration spending to 28% of historical levels (previously 50-60% of budgets), constraining the discovery pipeline for future copper supply. This spending reduction reflects investor pressure for immediate returns over long-term resource development, creating a strategic shortage of development-ready projects.

The exploration deficit particularly impacts smaller, higher-risk jurisdictions where significant discoveries traditionally occurred. Companies like Gladiator Metals in Canada's Yukon Territory and Fitzroy Minerals in Chile represent the rare explorers still actively building copper resource inventories, potentially positioning them for premium valuations as major miners seek acquisition targets.

Best Copper Companies: Tier-1 Jurisdiction Premium and Operational Advantages

Political stability and regulatory predictability have become paramount investment criteria for copper projects. Chile, Canada, and Australia command significant valuation premiums over projects in riskier jurisdictions, even when geological characteristics are comparable.

Marimaca Copper Corp exemplifies this jurisdiction advantage, operating in Chile's established Antofagasta mining region with access to existing infrastructure, skilled labor, and proven regulatory frameworks. The company's proximity to existing seawater pipelines and renewable power sources reduces both development risk and long-term operating costs—critical factors as water scarcity and carbon pricing impact mining economics globally.

Similarly, Gladiator Metals' Whitehorse Copper Project benefits from Canada's mining-friendly regulatory environment, year-round road access, and proximity to hydroelectric power infrastructure. The project's location within an established copper belt with historical production provides geological confidence while reducing infrastructure development requirements.

Recent drilling results demonstrate the project's expansion potential beyond initial resource estimates. Jason Bontempo, CEO of Gladiator Metals explains:

"Gladiator's first drillhole targeting mineralisation below 200m at Cowley Park highlights the significant upside potential of the deposit which has still only been explored at relatively shallow levels. Significantly a new style of mineralisation was observed with disseminated bornite observed over more than 180m within the granodiorite, outside of the skarn. Further drilling is in progress to assess the full potential of this new zone of mineralisation."

Infrastructure Access Drives Project Economics

Successful copper projects increasingly depend on existing infrastructure access rather than greenfield development. Transportation costs, power availability, and water access can determine project viability in today's capital-constrained environment.

Fitzroy Minerals has strategically assembled copper projects near existing infrastructure in Chile's established mining regions. The company's Buen Retiro project sits 60 kilometers from Copiapó with direct access to coastal ports, existing power lines, and established mining service providers. This infrastructure proximity reduces capital intensity and accelerates development timelines—critical advantages in competitive acquisition markets.

"Drilling at Buen Retiro continues to demonstrate good copper grades and thicknesses below the gravels in the Southwest Area. The wide and shallow mineralization we are finding will increase the dimensions of any potential future pit.” - Merlin Marr-Johnson, CEO of Fitzroy Minerals

Technology & Processing Innovation

Advanced processing technologies increasingly differentiate successful copper companies from struggling producers. Heap leaching for oxide copper deposits offers 38% lower carbon intensity compared to traditional flotation processing, creating both environmental and cost advantages.

Companies implementing innovative extraction technologies can unlock previously uneconomic deposits while meeting increasingly stringent environmental standards. Marimaca's successful pilot plant work and geometallurgical modeling demonstrate how technical innovation can improve project economics and reduce development risk.

"SMRD‑16 is a further 300 m step out to the west of the previously announced SMRD‑12 and has intersected a similar broad zone of high‑grade copper mineralization, including 70 m at 1.0% and a number of discrete very high‑grade zones." - Sergio Rivera, Vice-President of Exploration Marimaca

Top Copper Stocks: Investment Strategies from Development-Stage Leverage to Market Conditions

Companies with advanced development projects provide maximum leverage to copper price appreciation while maintaining defined development pathways. Marimaca Copper Corp, with its definitive feasibility study nearing completion and secured water/power access, represents this category's risk-reward profile.

These companies typically offer 3-5x leverage to copper price movements while providing clear milestones for project advancement. Resource expansion drilling, permitting progress, and financing arrangements create regular catalyst events that can drive share price appreciation independent of commodity price movements.

Exploration Companies Provide Blue-Sky Discovery Potential

Early-stage exploration companies offer the highest potential returns through resource discovery, but require careful selection based on management track records, geological potential, and financial capacity. Gladiator Metals and Fitzroy Minerals represent quality exploration plays with experienced management teams and projects in established mining districts.

Successful copper explorers typically require $10-50 million in exploration spending to define economic resources, making financial capacity and access to capital critical selection criteria. Companies with strong shareholder bases and proven ability to raise development capital provide better risk-adjusted return potential.

Geographic Diversification Reduces Political Risk

Investors should consider geographic diversification across copper investments to reduce political and regulatory risks. The optimal portfolio might include Canadian projects (stable but higher costs), Chilean operations (established infrastructure but water constraints), and select opportunities in Australia or other Tier-1 jurisdictions.

Industry Consolidation & Major Miners' Quest for Quality Assets Creates Premium Valuations

Large mining companies increasingly compete for quality copper assets as organic growth options diminish. BHP, Rio Tinto, Freeport-McMoRan, and others have announced significant copper expansion commitments while facing limited internal project pipelines.

This acquisition competition creates substantial premiums for development-ready copper projects. Recent transactions suggest valuations of $3-5 billion per million tonnes of annual copper production capacity—multiples that justify significant share price premiums for companies with defined development pathways.

Strategic Partnerships Accelerate Development

Joint ventures and strategic partnerships have become common development strategies for copper projects requiring substantial capital investment. These arrangements provide technical expertise, financial capacity, and market access while allowing smaller companies to maintain significant ownership stakes.

Companies like Fitzroy Minerals, with Pucobre S.A.'s 30% clawback option on the Buen Retiro project, demonstrate how strategic partnerships can provide development optionality while preserving upside participation for original investors.

Investment Timing & Market Catalysts: Copper Price Momentum Supports Equity Performance

Copper prices have demonstrated resilience above $4.00/pound, supported by Chinese infrastructure spending, U.S. grid modernization, and global decarbonization efforts. Technical analysis suggests continued strength as inventory levels remain below long-term averages while demand growth accelerates.

Equity markets typically anticipate copper price movements by 6-12 months, creating opportunities for investors who can identify supply-demand imbalances before they impact spot prices. Current market conditions suggest continued strength through 2025-2026 as new supply remains limited while demand growth accelerates.

ESG Requirements Drive Premium Valuations

Environmental, social, and governance factors increasingly influence copper project valuations as institutional investors require sustainable operations. Companies demonstrating superior environmental practices, community engagement, and governance standards command significant valuation premiums.

Marimaca's focus on renewable energy, seawater utilization, and community partnerships exemplifies how ESG excellence can differentiate companies in competitive capital markets. Similarly, Gladiator's indigenous partnership agreements and environmental remediation efforts position the company for superior ESG ratings.

Risk Factors & Mitigation Strategies: Managing Commodity Price Volatility

Copper prices remain subject to economic cycles, Chinese demand patterns, and global trade dynamics. Investors should consider position sizing and diversification strategies to manage commodity price exposure while maintaining upside participation.

Dollar-cost averaging into copper equity positions can reduce timing risk while maintaining exposure to long-term demand trends. Companies with superior cost structures and established infrastructure access typically outperform during price downturns while capturing full upside during bull markets.

Development & Operational Risks

Mining projects face numerous execution risks including cost overruns, permitting delays, and operational challenges. Thorough due diligence on management track records, project economics, and development timelines remains essential for successful copper equity investments.

Companies with experienced technical teams, proven financing capabilities, and realistic development schedules provide better risk-adjusted returns than those with aggressive timelines or unproven management.

The copper investment landscape presents a compelling opportunity for investors who understand the structural supply-demand dynamics reshaping this critical commodity market. Companies positioned in Tier-1 jurisdictions with advanced projects and experienced management teams offer the most attractive risk-adjusted return potential as the world transitions toward electrification and sustainable energy systems.

The Investment Thesis for Copper

- Diversify into mid-cap developers when copper hits $4.50+ per pound as companies like Marimaca and Gladiator offer 3-5x price leverage with defined development timelines, providing optimal exposure for capturing price momentum while maintaining manageable risk profiles

- Target Tier-1 jurisdiction exposure for portfolio stability by prioritizing Canadian, Chilean, and Australian copper assets over higher-risk jurisdictions, as political stability premiums justify 20-30% valuation multiples versus comparable projects in unstable regions

- Weight exploration companies at 15-25% of copper allocation since Fitzroy-style early-stage plays provide blue-sky discovery potential, limiting exposure due to binary outcomes while maintaining meaningful positions for portfolio-changing returns

- Focus on infrastructure-advantaged projects for lower execution risk because companies with existing road, power, and water access require 40-60% less capital than greenfield developments, while proximity to ports and processing facilities reduces timeline and cost overruns

- Consider ESG leaders as institutional capital flows accelerate since environmental and community-focused operators command 20-40% valuation premiums, and sustainability credentials increasingly determine access to development capital from major investors

- Monitor M&A catalysts as majors seek quality assets because development-ready projects with over 1 million tonnes contained copper attract acquisition premiums of $200-400M+, and companies advancing toward feasibility studies often see 50-100% rerating ahead of strategic transactions

Analyst's Notes

Subscribe to Our Channel

Stay Informed