Elevated Rates Drive Gold’s 16% Pullback Despite Record Producer Margins

Iran energy shock pushes gold to $4,550/oz, but production-stage gold equities with AISC below $3,000/oz are generating their widest cash margins on record.

- Gold fell 3.8% in the week of May 12 to 19, 2026, to $4,550 per ounce after April CPI rose 3.8% year-over-year and core PPI increased 1.0% month-over-month, reinforcing expectations that the Fed will hold real rates elevated. CME Group FedWatch now assigns a 37% probability of a Fed rate hike before year-end 2026, increasing near-term pressure on non-yielding gold.

- Iran's Strait of Hormuz blockade has held WTI crude above $102 per barrel, feeding energy costs into consumer prices and delaying Fed rate cuts. COMEX gold open interest, ETF inflows, and Managed Money positioning have stalled near multi-quarter lows, signalling weak institutional paper demand despite historically high gold prices.

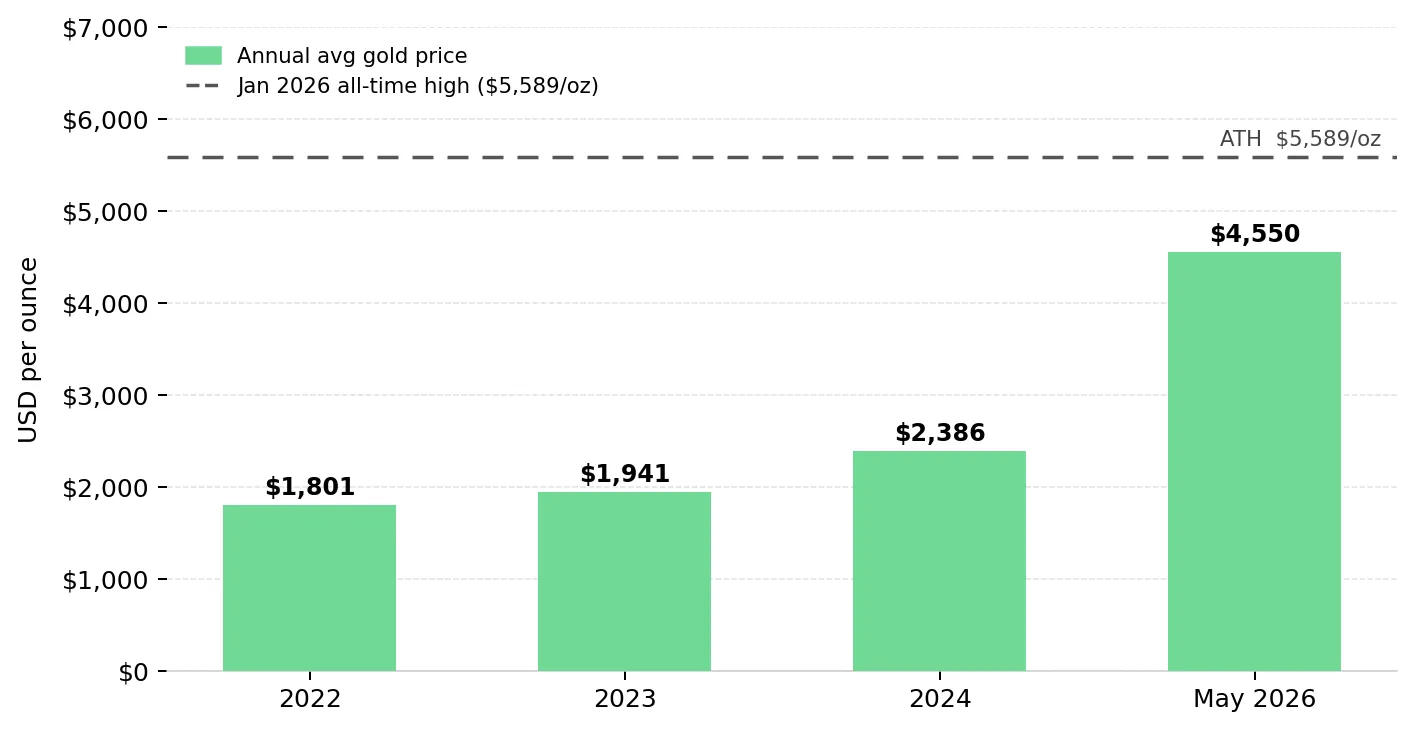

- Gold at $4,550 per ounce remains 41% above year-ago levels and more than double the 2022 annual average of approximately $1,801 per ounce, sustaining historically high producer margins. Producers with AISC below $3,000 per ounce generate $1,500 to $2,500 per ounce in gross margin at current spot prices.

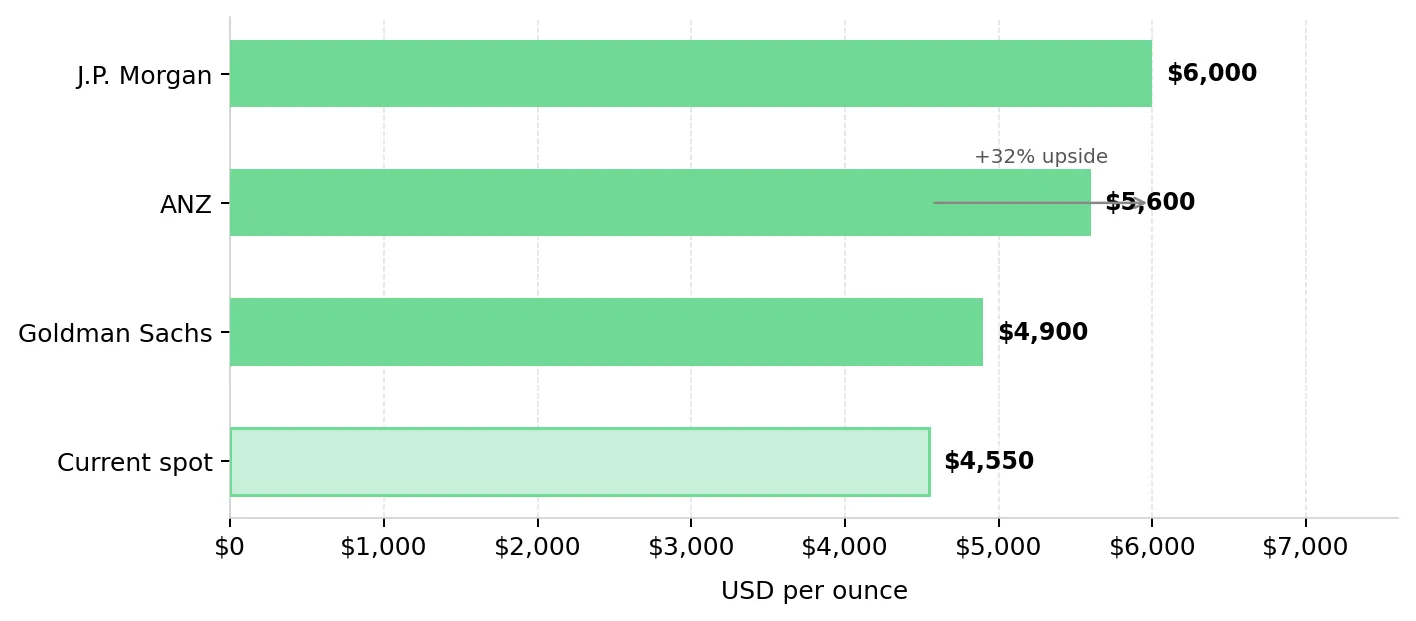

- JPMorgan lowered its average 2026 gold price forecast to $5,243 per ounce because of weaker institutional paper demand while maintaining its year-end 2026 target of $6,000 per ounce, implying 32% upside from current levels. Goldman Sachs targets $4,900 per ounce and ANZ targets $5,600 per ounce by year-end 2026, both above current spot prices.

- Production-stage gold equities remain profitable at current spot prices without requiring a near-term rebound in gold. Producers profitable at $4,550 per ounce today would see further margin expansion if the Strait of Hormuz reopens, energy inflation subsides, and Fed rate cuts resume.

Iran Oil Shock Pushes Real Rates Higher & Weakens Gold

The Strait of Hormuz carries approximately 20% of global oil supply, making any disruption immediately inflationary for energy-importing economies. Iran's blockade, now in its eleventh week, disrupted a critical export route with no near-term replacement available. The International Energy Agency described the disruption as "the largest supply disruption in the history of the global oil market," reinforcing expectations for sustained energy-driven inflation. WTI crude crossed $102 per barrel, contributing to April CPI of 3.8% year-over-year and pushing CME Group FedWatch to price a 37% probability of a Fed rate hike before year-end 2026.

Higher real-rate expectations reduced institutional demand for paper gold instruments. COMEX gold open interest fell to multi-quarter lows, ETF inflows stalled, and gold declined 16% from its January 2026 record. Production-stage gold companies continued reporting record quarterly earnings because current spot prices remain far above historical operating-cost assumptions.The Iran war weakened gold by raising energy costs, accelerating inflation, and delaying central bank rate cuts. Gold is likely to remain under pressure in paper markets until energy prices fall and rate-cut expectations return.

Energy Inflation Weakens Paper Gold Demand While Central Banks Keep Buying

WTI crude rose more than 40% from approximately $73 per barrel in late February 2026 to above $102 per barrel by mid-May. Energy accounted for more than 40% of April's monthly CPI increase, according to the Bureau of Labor Statistics. Core PPI rose 1.0% month-over-month, its sharpest increase in four years, indicating that energy inflation is spreading into services and goods. Goldman Sachs raised its December 2026 PCE inflation forecast to 3.4% from 3.1%, citing higher energy costs linked to the Iran war.

Physical gold demand remains strong even as institutional paper gold demand weakens. Central banks purchased a net 244 tonnes of gold in Q1 2026, 3% above the prior year and above the five-year quarterly average. The People's Bank of China made its largest monthly gold purchase in 17 months during the same week that Western institutional paper-gold inflows weakened. Sovereign buyers continue accumulating physical gold while institutional investors shift toward bonds offering positive real yields.

$4,550 Gold Still Supports Record Producer Margins

Gold averaged approximately $1,801 per ounce in 2022, less than half the current spot price. At $4,550 per ounce today, a producer with AISC of $2,800 per ounce generates approximately $1,750 per ounce in operating margin, a level that exceeded peak margins in prior gold cycles.

Integra Resources Expands Florida Canyon to Increase Future Gold Cash Flow

Q1 2026 earnings show that production-stage miners remain highly profitable at current gold prices. Integra Resources Corp. generated mine operating earnings of $24.9 million on revenue of $61.7 million in Q1 2026, producing a 40% operating margin versus 27% in Q1 2025 at an average realized gold price of $4,854 per ounce. Net earnings increased to $12.5 million, or $0.06 per share, from $1.0 million in Q1 2025. The DeLamar Project Feasibility Study, effective December 2025, shows after-tax NPV at a 5% discount rate increasing from approximately $774 million at $3,000 gold to approximately $1.9 billion at $4,500 gold.

With Florida Canyon reaching a record 76,800 total tonnes mined per day in Q1 2026, George Salamis, President and Chief Executive Officer of Integra Resources, explains how current capital spending is intended to increase future production and cash flow:

"2026 is about building capacity today at Florida Canyon to deliver more ounces, stronger cash flow, and lower costs tomorrow."

High-Grade Deposits & Existing Mills Increase Gold Operating Leverage

Not all gold operations respond equally to rising energy costs. The key variable is ore grade: more gold per tonne means fewer tonnes processed per ounce, directly lowering per-ounce fuel and processing costs. High-grade operations carry a structural AISC advantage that widens as energy prices stay elevated.

Serabi Gold Expands Throughput While Maintaining Low Processing Costs

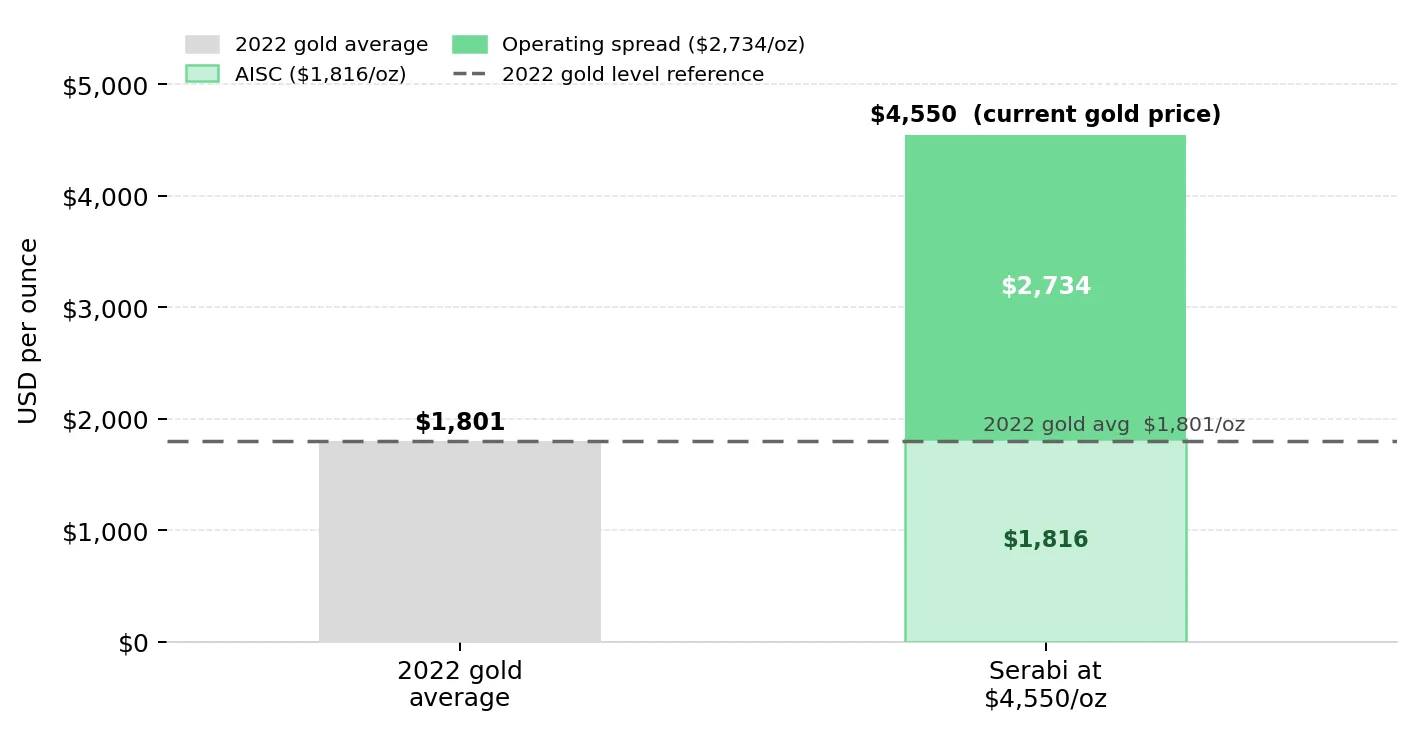

Serabi Gold produced 44,169 ounces in 2025, up 18% from 2024, at a group AISC of approximately US$1,816 per ounce. At $4,550 gold, AISC generates approximately $2,734 per ounce in operating margin, supporting an inaugural annual dividend of US$5.41 million while leaving Serabi with US$64.4 million in cash and zero debt at Q1 2026 close. The Comex ore sorter at Coringa upgrades sub-2 g/t feed to 10 g/t while rejecting more than 90% of waste mass, reducing processing costs per ounce.

Serabi's near-term production growth depends on expanding processing capacity rather than increasing ore supply. Mike Hodgson, Chief Executive Officer of Serabi Gold, explains why the company is investing in plant expansion:

"Our plant is absolutely maxed out. We're sorting all the Coringa ore, nearly all of it, and we're sorting some of the Palito ore. We can't really do anything more with that plant without expansion."

Serabi is relocating a dormant ball mill from Coringa to Palito for approximately US$5 million, targeting Q4 2026 commissioning and increasing throughput by roughly 38% without constructing a new plant.

West Red Lake Gold Mines Uses Existing Infrastructure to Expand High-Grade Production

West Red Lake Gold Mines operates in Ontario's Red Lake district, which has produced more than 20 million ounces of gold historically and supports established mining infrastructure. The Madsen mill anchors the company's hub-and-spoke strategy and carries 2026 production guidance of 35,000 to 45,000 ounces. The Rowan Deposit, located 80 road kilometres away, contains an indicated resource of 196,747 ounces at 12.78 g/t gold and an inferred resource of 118,155 ounces at 8.73 g/t. A standalone PEA for Rowan generated a $125 million NPV and 42% IRR with only $70 million in capital expenditure because the project uses the existing Madsen mill. The joint Madsen-Rowan PFS, targeting Q3 2026, values the combined asset using a gold price of US$2,600 per ounce, US$1,950 below current spot prices.

Shane Williams, President and Chief Executive Officer of West Red Lake Gold Mines, explains why near-term gold production and existing infrastructure can create more immediate cash flow value:

"I would much rather have a mine in production today producing gold for the next four years generating cash flow than have a great project that is five years out the road. And investors need to think about that."

i-80 Gold Funds Lone Tree Expansion Through Existing Nevada Processing Capacity

i-80 Gold Corp. reported record Q1 2026 gross profit of $16.1 million on revenue of $52.4 million from 10,590 ounces sold at an average realized gold price of $4,941 per ounce. Granite Creek produced 8,857 ounces at an oxide mined grade of 8.86 g/t, exceeding March 2025 PEA assumptions. More than 4,000 recoverable sulphide ounces remain unprocessed pending completion of the Lone Tree Plant, a $430 million refurbishment targeting Phase 1 production of 150,000 to 200,000 ounces annually from 2028. i-80 Gold ended Q1 2026 with $513.5 million in cash, including a $250 million NSR royalty transaction with Franco-Nevada, fully funding Phase 1 and Phase 2 development.

With Lone Tree fully funded and engineering work advancing, Paul Chawrun, Chief Operating Officer of i-80 Gold, outlines the timeline for bringing new processing capacity into production:

"We're comfortable with putting this together and we're still looking at the first pour by the end of December of 2027 with a ramp up to production in the first quarter of 2028."

Falling Energy Inflation Could Restore Fed Rate Cuts and Support Gold Prices

If the Strait of Hormuz reopens and energy prices normalize, CPI could move back toward the Fed's 2% target, giving a rate-cutting Fed Chair greater flexibility to begin an easing cycle. JPMorgan's commodity research framework attributes approximately 70% of quarter-on-quarter gold price movements to investor and central bank demand volumes. Under that relationship, a 100 basis point reduction in US policy rates would likely increase gold demand by reducing real bond yields.

Production-stage gold producers remain highly profitable at current gold prices without requiring Fed rate cuts or a renewed gold rally. JPMorgan, Goldman Sachs, and ANZ maintain year-end 2026 gold targets of $6,000, $4,900, and $5,600 per ounce respectively, implying upside of 8% to 32% from current levels.

The Investment Thesis for Gold

- Producers with mine-site AISC below $3,000 per ounce are generating $1,500 to $2,500 per ounce in gross margin at the current spot price of $4,550 per ounce, exceeding margin levels seen in prior inflation-driven gold cycles.

- The Iran-driven pressure on paper gold depends on the Strait of Hormuz remaining closed; reopening the route would reduce energy inflation, pull CPI closer to the Fed's 2% target, and restore expectations for rate cuts.

- High-grade underground operations with head grades above 8 g/t maintain lower AISC during energy inflation because higher gold content per tonne reduces fuel, processing, and haulage costs per ounce relative to lower-grade mines.

- Hub-and-spoke processing models route high-grade satellite ore to existing permitted mills, replacing standalone plant construction with transport costs and lowering the capital required for production growth without materially reducing margins.

- Producers with fully funded development programmes face construction-execution risk rather than financing risk, making them more investable for institutions that require capital certainty before deploying funds.

- JPMorgan, Goldman Sachs, and ANZ maintain year-end 2026 gold targets of $6,000, $4,900, and $5,600 per ounce respectively, implying 8% to 32% upside from current prices. Low-AISC production-stage equities would convert higher gold prices directly into additional cash flow per ounce without requiring lower operating costs.

Gold at $4,550 per ounce remains 41% above year-ago levels and more than double its 2022 annual average. The near-term bear case is driven by the Iran energy shock lifting CPI to 3.8%, keeping Fed rates elevated, and weakening institutional paper-gold demand. Those macro pressures do not change the cash-flow strength of production-stage miners that remain profitable at current gold prices. If the Iran conflict eases and energy prices normalize, the Fed would face less inflation pressure to keep rates elevated. Under that scenario, production-stage gold equities operating at today's AISC levels could benefit from gold prices $500 to $1,500 per ounce above current levels without requiring lower operating costs. Current market conditions have created a disconnect between paper-gold sentiment and the cash-flow performance of production-stage miners.

TL;DR

Gold's 16% correction to $4,550 per ounce reflects a specific macro mechanism: Iran's Strait of Hormuz blockade has driven WTI crude above $102 per barrel, pushing US CPI to 3.8% year-over-year, which has frozen Fed rate-cut expectations and suppressed institutional paper gold demand. The correction does not change the cash-flow reality for production-stage gold companies operating with AISC below $3,000 per ounce, where gross margins of $1,500 to $2,500 per ounce represent a level the sector has never seen at comparable points of macro uncertainty. When the conflict resolves, energy prices normalize, and the Fed resumes cutting rates, these producers face significant price upside with no cost improvement required to capture it.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed