Federal Reserve Credibility Shock & the Silver Repricing Cycle

Silver hits $88/oz as Fed credibility erodes, Chinese exports tighten supply, and EV/AI demand surges. Explore top silver miners across the value chain.

- Silver's advance to $88 per ounce on January 13, 2026 reflects more than momentum, signaling a repricing of monetary credibility risk as political pressure on the US Federal Reserve escalates.

- Unlike gold, silver's smaller, more industrially exposed market amplifies volatility when macro trust erodes and physical supply tightens.

- Structural supply constraints, including Chinese export restrictions and regional inventory fragmentation, are reducing liquidity at traditional pricing hubs.

- Exchange-level changes to CME margin structures introduce short-term volatility but reinforce investor preference for cash-flow-generating producers.

- Select silver miners across production, development, and advanced exploration offer differentiated exposure depending on jurisdiction, cost structure, and capital strength.

When Monetary Trust Becomes a Commodity Variable

Silver reached a record high of $88 per ounce on January 13, 2026, occurring alongside gold trading near all-time highs and underscoring divergent investor behavior within the precious metals complex. While gold has long served as the primary monetary hedge, silver's sharper trajectory reveals a market recalibrating its assessment of institutional stability.

The immediate catalyst centers on heightened political scrutiny of the US Federal Reserve, including a Department of Justice criminal investigation into Fed Chair Jerome Powell that market analysts cite as challenging long-held assumptions of central bank independence. For decades, the credibility of monetary policy rested on the presumption that rate-setting institutions operated beyond political interference. That assumption is now being tested publicly, and capital is responding accordingly.

For investors, this shift represents more than a headline risk. It constitutes a portfolio construction signal, particularly for assets tied to monetary credibility and physical scarcity. Traditional models of precious metals allocation assumed stable institutional frameworks. The current environment demands reassessment of those assumptions.

Silver's dual identity as both a monetary hedge and an industrial input positions it uniquely in this environment. Unlike gold, which responds primarily to real rate expectations and currency depreciation, silver carries exposure to manufacturing demand, energy transition requirements, and data infrastructure growth. This bifurcated demand profile creates distinct price dynamics when macro uncertainty coincides with structural supply constraints.

Political Risk & the Repricing of Central Bank Credibility

The relationship between political pressure and precious metals pricing operates through several transmission mechanisms that investors must understand to position portfolios effectively. Markets are responding not merely to interest rate policy itself, but to the erosion of institutional trust that underpins forward guidance credibility.

Political interference in central bank operations introduces uncertainty across multiple dimensions. Forward guidance loses predictive value when policy decisions become subject to external considerations. Inflation expectations become unanchored when markets question the commitment to price stability. Real rate stability, the foundation of fixed income valuation, becomes contingent on political outcomes rather than economic fundamentals. Each of these channels reinforces the case for assets that preserve purchasing power independent of policy credibility.

The investment implications extend beyond simple rate sensitivity. Precious metals benefit when policy predictability deteriorates, not merely when rates decline. Silver historically reacts more sharply than gold during such periods due to thinner liquidity and higher speculative participation. The smaller market capitalization of silver relative to gold means that comparable capital flows generate larger price movements, creating both opportunity and risk for positioned investors.

Within this environment, primary silver producers offer direct operating leverage to price movements driven by monetary stress. Americas Gold and Silver operates the Galena Complex in Idaho's Silver Valley district, where the company is executing a production ramp-up toward a target of 5 million ounces annually. Year-to-date production through the third quarter of 2025 reached 0.73 million ounces of silver, with current mill throughput at 408 tons per day against total capacity of 1,150 tons per day. The company also holds the distinction of operating the largest active antimony mine in the United States, a critical mineral designation that has prompted engagement with US Senators regarding domestic supply chain priorities.

Oliver Turner, Executive Vice President of Corporate Development at Americas Gold and Silver, frames the company's production trajectory:

"We've been out there publicly stating that our goal is to bring Galena back to 5 million ounces, and we're not going to stop there. We think Galena can do more than that."

The December 2025 acquisition of the nearby Crescent Mine provides additional feed for the existing mill infrastructure, with development expected to commence within approximately six months of closing.

From Global Pools to Regional Bottlenecks: Silver's Physical Constraint Problem

The global silver market is undergoing a structural transformation that carries significant implications for price discovery and physical availability. For decades, silver traded as a globally fungible commodity with relatively seamless arbitrage between major trading hubs. That architecture is fragmenting under pressure from trade policy and strategic resource considerations.

Chinese export restrictions are accelerating the shift away from a unified global market. As the world's largest refiner of silver, China's policy decisions directly affect supply availability in Western markets. Restrictions on refined metal exports create regional imbalances that cannot be resolved through traditional arbitrage mechanisms, introducing persistent price dispersion between trading centers.

The London-New York imbalance illustrates this dynamic in practice. Tariff concerns and hedging activity have redirected significant volumes of physical silver into US vaults, depleting London inventories and raising questions about benchmark reliability during stress events. When physical metal cannot move freely between jurisdictions, prices at different locations may diverge for extended periods, complicating hedging strategies and creating basis risk for producers and consumers alike.

Exploration-stage silver projects positioned to supply North American demand carry strategic value in this reconfigured market structure. Vizsla Silver is advancing the Panuco project in Mexico's Sinaloa state, where a November 2025 Feasibility Study established Proven and Probable Reserves of 123 million ounces silver equivalent. The company commenced test mining in the fourth quarter of 2024, with underground development now comprising 169 meters in ore and 902 meters in waste, targeting a 10,000-tonne bulk sample.

Jesus Velador, Vice President of Exploration at Vizsla Silver, describes the company's resource development progress:

"What we accomplished there is over 60,000 meters of infield drilling mostly on the central portion of Copala, with that drilling what we essentially ended up releasing is an updated mineral resource with a substantial increase in particularly the indicated and measured resources, an increase of 43 percent."

The company is targeting a construction decision in the second quarter of 2026 and first silver production in the second half of 2027, supported by total financing capacity of US$480 million including proceeds from a US$300 million convertible note offering.

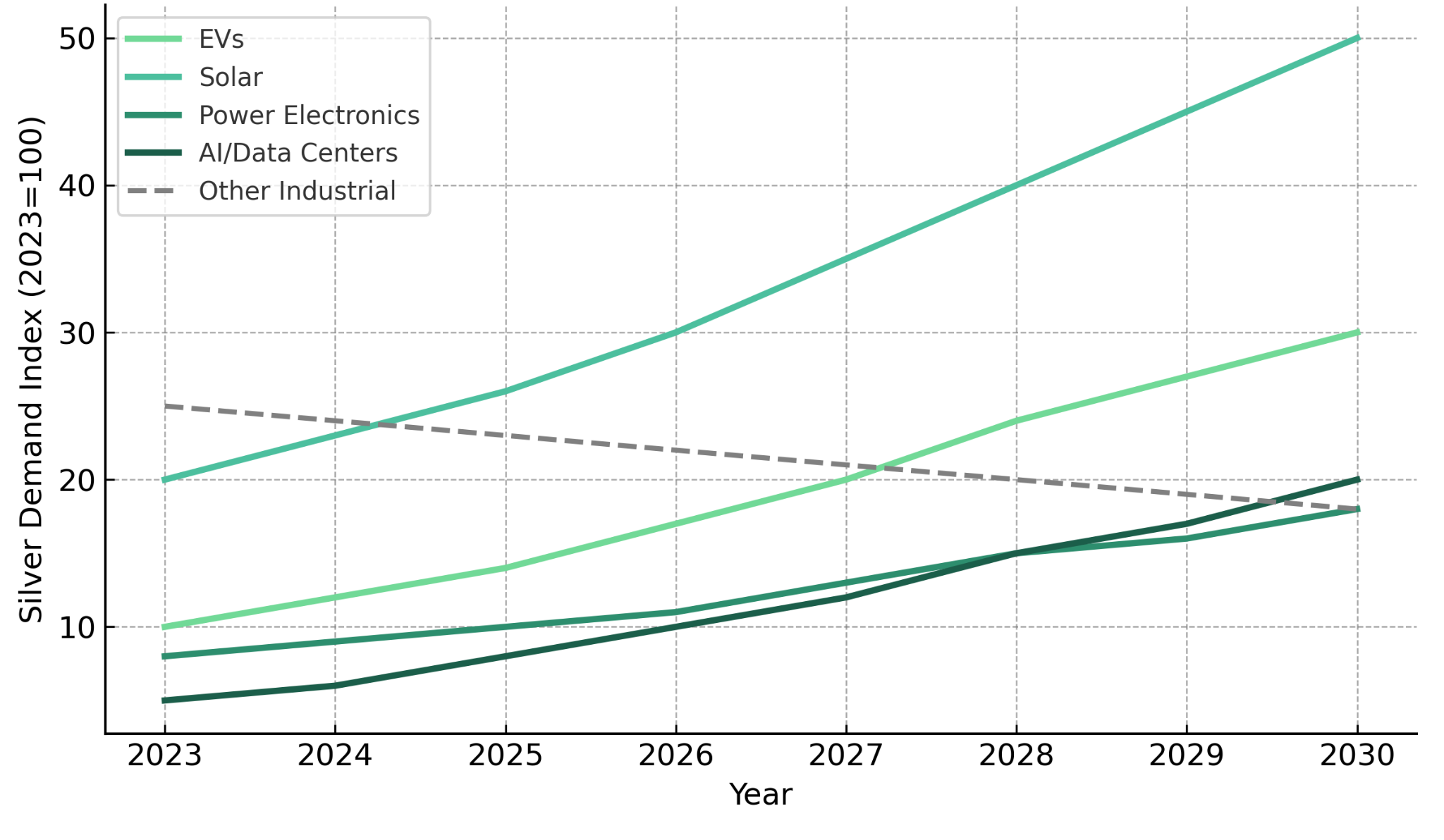

Industrial Demand Is No Longer Cyclical: Structural Consumption Drivers

The traditional framework for analyzing silver demand assumed industrial consumption would track broader economic cycles, rising during expansions and contracting during recessions. That assumption requires revision given the structural nature of current demand drivers.

Silver consumption from electric vehicles, power electronics, and AI data centers represents non-discretionary industrial demand that persists independent of GDP growth rates. These applications rely on silver's unique combination of electrical conductivity, thermal properties, and chemical stability. At current performance thresholds, substitution remains technically impractical or economically prohibitive, creating a demand floor that differs qualitatively from historical industrial patterns.

Under slower GDP growth scenarios, energy transition investments and data infrastructure requirements maintain baseline silver demand at levels that exceed historical precedent. The International Energy Agency's projections for photovoltaic capacity additions alone imply sustained industrial silver consumption growth through the end of the decade, before accounting for additional demand from transportation electrification and semiconductor manufacturing.

Projects offering exposure to sustained silver demand with favorable cost structures merit particular attention in this environment. Cerro de Pasco Resources is advancing toward a Feasibility Study, expected in the first half of 2026, for its polymetallic assets in Peru. The Quiulacocha tailings deposit contains an estimated 75 million tonnes grading to a historic estimate of 423 million ounces silver equivalent, while the Excelsior mineral pile holds an NI 43-101 compliant Inferred Resource of 30.1 million tonnes. The project's surface-based reprocessing model eliminates conventional underground mining risk while addressing legacy environmental liabilities, a factor that has helped secure local social license in the region.

Steven Zadka, Executive Chairman of Cerro de Pasco Resources, explains the cost advantages inherent to the project's configuration:

"The hardest part of mining is mining. That's where your biggest risk is, not processing."

Recent drilling has also identified critical minerals including gallium averaging 53.2 grams per tonne and indium at 19.9 grams per tonne across 40 holes, results that have prompted engagement with US government officials regarding strategic materials supply.

Volatility, Margin Rules & Capital Discipline

Market structure changes at major exchanges are reshaping the risk profile of silver exposure and influencing capital allocation across the sector. The CME Group's transition to percentage-based margin requirements raises the cost of maintaining leveraged positions during volatility spikes, with implications for both speculative activity and commercial hedging.

The short-term impact manifests as potential pressure on futures-driven price action. When margin requirements increase proportionally with price, the capital required to maintain existing positions rises precisely when volatility is highest, forcing position liquidation that can amplify price movements in either direction. Analysts note this mechanism may temporarily weigh on precious metals prices even as fundamental drivers remain supportive.

The longer-term impact favors operationally robust mining companies over purely speculative vehicles. As leveraged trading becomes more expensive, capital rotates toward equity instruments that offer silver exposure through production economics rather than financial engineering. Balance sheet strength and all-in sustaining cost resilience become increasingly valuable when margin stress periodically disrupts futures markets.

Exploration-stage companies offering discovery leverage face heightened sensitivity to capital market conditions under this regime. GR Silver Mining is advancing the Plomosas project in Mexico with a strengthened treasury position of approximately CAD$28.8 million following a private placement that closed December 15, 2025. The project hosts a combined resource of 134 million ounces silver equivalent across Indicated and Inferred categories, with existing infrastructure including a water permit and tailings facility.

Marcio Fonseca, Chief Executive Officer and President of GR Silver Mining, describes the company's capital allocation priorities:

"We are going to split this between a material aggressive step-out drilling and some exploration drilling in some new areas to really multiply the size of the resource at Plomosas. That's the core: the resource growth."

Engineering studies for bulk sampling and pilot plant assessment are targeting commencement in early 2026.

The Investment Thesis for Silver

Silver's current market conditions present a differentiated opportunity set across the value chain, supported by several structural factors that merit strategic attention.

- Political pressure on central banks, including active investigations into Federal Reserve leadership, reinforces silver's historical role as a monetary hedge during periods of institutional credibility erosion.

- Regional inventory isolation introduces structural volatility and creates upside skew when physical supply cannot arbitrage freely between major trading centers.

- Electric vehicle production and AI infrastructure development underpin long-term industrial consumption that is less cyclically sensitive than historical demand patterns.

- Producers, developers, and explorers offer distinct risk-return profiles depending on capital strength, cost structure, and development timing.

- Low all-in sustaining cost assets and fully funded development projects provide asymmetric upside exposure when price volatility compresses leveraged speculation.

- Established mining jurisdictions offer regulatory frameworks that support permitting visibility, though investors should monitor evolving policy conditions and associated timeline risks.

Silver as a Signal, Not a Speculation

Silver's advance to record highs represents more than a price event. It constitutes a macro signal reflecting trust erosion in monetary institutions, supply rigidity from trade policy fragmentation, and structural demand from industrial applications that are reshaping consumption patterns.

The opportunity lies not in chasing volatility but in selective exposure to companies positioned across the silver value chain. Production assets offer direct operating leverage to price appreciation. Development projects provide visibility on future supply in an increasingly constrained market. Exploration companies offer discovery optionality for investors with appropriate risk tolerance and time horizons.

As monetary credibility becomes increasingly politicized and physical supply remains regionally fragmented, silver's relevance as both an industrial input and financial asset is likely to persist.

TL;DR

Silver reached a record $88 per ounce on January 13, 2026, driven by three converging forces: political pressure on the Federal Reserve eroding monetary credibility, Chinese export restrictions fragmenting global supply chains, and structural industrial demand from EVs and AI infrastructure. Unlike gold, silver's smaller market amplifies volatility during institutional trust erosion. CME margin rule changes are pushing capital toward cash-generating producers over leveraged speculation. The investment opportunity spans production-stage assets offering direct price leverage, development projects with 2026-2027 production timelines, and exploration plays with resource expansion potential. As monetary trust becomes politicized and physical supply remains constrained, silver functions as both industrial input and financial hedge.

FAQs (AI-Generated)

Silver's advance to $88 per ounce reflects a repricing of monetary credibility risk as political pressure on the Federal Reserve escalates, combined with Chinese export restrictions tightening physical supply and sustained industrial demand from electric vehicles and AI data centers.

When markets question central bank independence, forward guidance loses predictive value and inflation expectations become unanchored. Silver historically reacts more sharply than gold during such periods due to thinner liquidity and higher speculative participation.

Non-discretionary consumption from EVs, power electronics, and AI data infrastructure relies on silver's unique electrical conductivity and thermal properties. These applications persist independent of GDP cycles, creating a demand floor exceeding historical patterns.

As the world's largest silver refiner, China's export restrictions create regional imbalances between London and New York that cannot be resolved through traditional arbitrage, introducing persistent price dispersion and basis risk.

Producers provide direct operating leverage to price movements; development projects offer visibility on future supply; and exploration companies offer discovery optionality. Low all-in sustaining cost assets and fully funded projects provide asymmetric upside when margin stress compresses leveraged speculation.

Analyst's Notes

Subscribe to Our Channel

Stay Informed