Fitzroy Minerals: PFS in Q1/2027 & Copper Production Targeted for Q1/2028

Fitzroy Minerals advances copper project in Chile with low-cost exploration, strong balance sheet, and near-term production pathway via oxide development.

- Strong balance sheet post-financing: Fitzroy Minerals raised C$21.1M, bringing total cash to ~C$29M, implying an enterprise value of ~C$80M (≈US$55M), providing flexibility in volatile markets.

- Unique cost-recovery exploration model: For the next 12 months, ~90% of exploration spend is expected to be reimbursed via partner clawback, effectively reducing drilling costs to only ~10 cents on the dollar.

- Near-term production pathway via oxides: Heap leach project targeting potential production by 2028, leveraging third-party processing infrastructure to reduce capex and permitting timelines.

- Large-scale copper system emerging: Drill results confirm extensive mineralisation (e.g., 384m @ 0.23% Cu), with mineralisation extending over >3.5km, suggesting district-scale potential.

- Execution and partnership risk remains: Reliance on partner agreements (e.g., electro-winning plant access, clawback execution) and pending PFS (Q1 next year) introduce uncertainty.

Copper Demand Meets Capital Discipline

The global copper market remains central to the energy transition narrative, underpinning electrification, grid expansion, and renewable infrastructure. Against this backdrop, investors are increasingly focused not just on resource size, but on capital efficiency, speed to production, and funding strategies that minimise dilution.

Fitzroy Minerals presents a case study in this evolving investment framework. The company is advancing a copper project in Chile, combining near-term oxide production potential with longer-term sulfide exploration upside. Recent announcements—including a C$21.1 million capital raise and new drill results offer a clearer view of how management intends to execute. CEO, Merlin Marr-Johnson framed the company’s positioning succinctly:

“We’re exploring for copper, and happily we’re finding copper in Chile.”

This statement, while simple, reflects a broader narrative: early validation of a potentially large system, paired with a structured approach to development and capital deployment.

Financial Position & Capital Structure

The company has put together 4 elements which position it ahead of other exploration companies:

1. Cash position with $29M.

2. Clawback deal, effectivly meaning it costs only $0.10 for every dollar sepnt on exploration.

3. Oxide processed by local producer to generate millions each year in cash from Q1/2028. No permits required, no capex.

4. Large copper assets already show large endowment from surface 30km by paved dual highway from mining town

The company’s financial position is a central component of its investment case. Following the recent capital raise, Fitzroy holds approximately C$29 million in cash. With a market capitalisation of around C$110 million, this translates into an enterprise value of approximately C$80 million, or roughly US$55 million.

This capital base provides the company with a degree of flexibility that is often lacking among junior explorers. Management has indicated that even after executing its planned work programs over the next 12 months, Fitzroy expects to retain approximately $10 million in treasury. This suggests a measured approach to capital allocation, balancing the desire to accelerate exploration with the need to preserve financial resilience.

From an investor perspective, this capital position serves multiple functions:

- Provides funding for an expanded exploration program

- Supports ongoing prefeasibility study (PFS) work

- Reduces near-term financing risk

- Enables flexibility in volatile market conditions

Management emphasised this flexibility:

“Having the stronger balance sheet gives us greater flexibility particularly in these volatile markets.”

The company expects to retain approximately $10 million in treasury after executing its planned exploration and Pre Feasibility Study programs over the next 12 months, suggesting disciplined capital allocation rather than aggressive expenditure.

Capital-Efficient Exploration Model

Perhaps the most distinctive aspect of Fitzroy’s strategy is its approach to exploration funding. Through its agreement structure, the company expects that up to 90% of exploration expenditure may be reimbursed via a partner clawback mechanism. This effectively reduces the cost of drilling to approximately 10% of actual spend for a defined period.

The CEO described this dynamic clearly:

“For every dollar that we put into exploration… we’ll get 90 cents back.”

This structure has significant implications for capital efficiency. It enables the company to undertake a more aggressive exploration program than would otherwise be possible, while limiting dilution for existing shareholders. At the same time, management has emphasised discipline. Despite the opportunity to accelerate spending, Marr-Johnson noted that the company intends to remain measured in its approach, focusing on high-quality targeting and geological understanding rather than indiscriminate drilling.

This balance between opportunity and restraint is likely to be an important factor in how investors assess the credibility of the company’s execution strategy. This structure creates several implications:

- Accelerated exploration potential: The company can expand drilling programs without proportional capital outlay

- Reduced dilution risk: Lower effective costs mean less need for equity financing

- Higher risk tolerance: More aggressive exploration can be justified economically

However, management also stressed prudence:

“That would encourage us to throw the kitchen sink at drilling… but that’s not us.”

This balance between opportunity and discipline is central to the investment case.

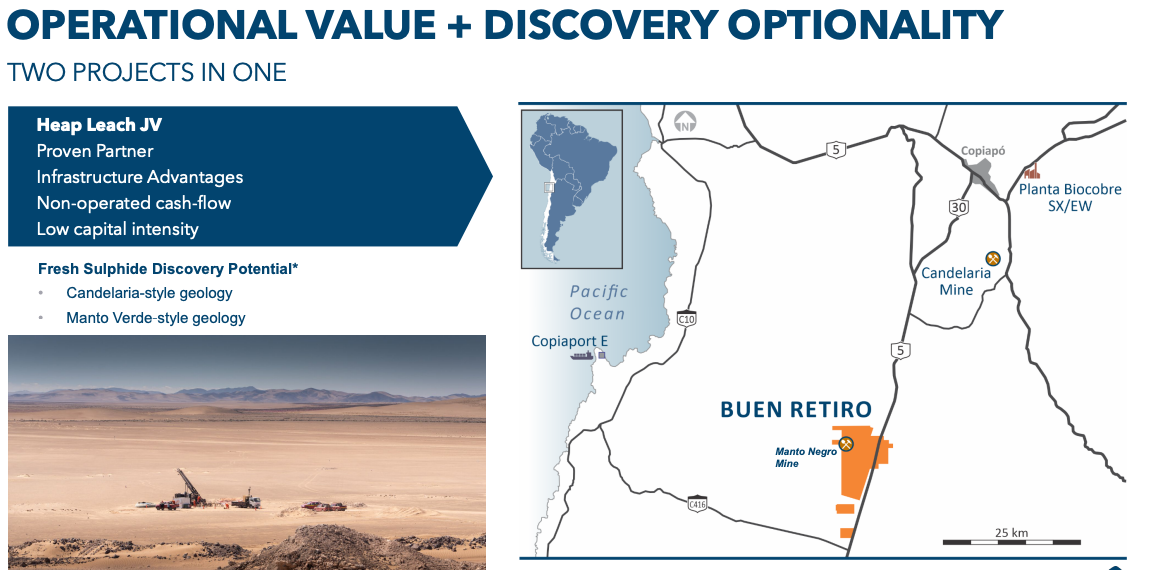

Oxides First, to Generate Cash

Fitzroy’s development strategy is anchored in a phased approach, beginning with oxide mineralisation. The company is targeting a heap leach operation, with a prefeasibility study expected in Q1 next year and potential production by 2028 A critical advantage lies in infrastructure:

- Access to a nearby electro-winning plant owned by a partner

- Avoidance of ~$60 million in capital expenditure

- Reduced permitting timelines

A key advantage lies in the availability of nearby infrastructure. Fitzroy intends to utilise an existing electro-winning plant operated by a partner, thereby avoiding the need to construct its own facility. This could save approximately $60 million in capital expenditure and significantly reduce permitting timelines.

As Marr-Johnson explained, “We can get into production without having to spend the $60 odd million… nor go through the years of permitting.” For investors, this represents a meaningful reduction in both capital intensity and execution risk. but alos the genertation of millions of dollars of exploration capital to use across the portfolio.

The oxide operation is also expected to generate early cash flow, which management intends to reinvest into further exploration. This creates the potential for a self-funded growth model, reducing reliance on external financing over time.

Then Exploration, to unlock Geological Potential

Recent drilling results provide early evidence of scale.

Key intercepts include:

110m @ 1.94% Cu

135m @ 0.75% Cu

384m @ 0.23% Cu

94m @ 0.33% Cu

108m @ 0.4% Cu

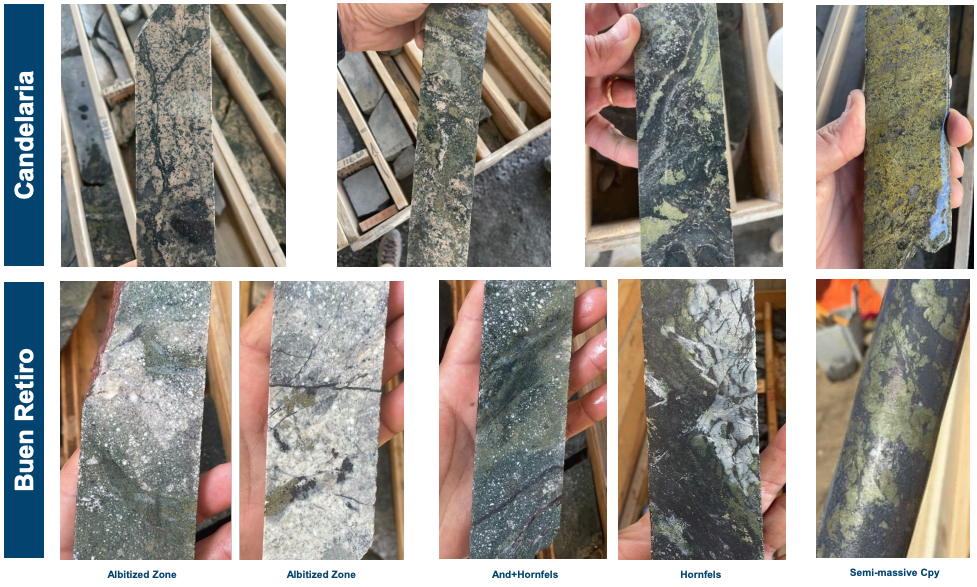

Recent drilling results provide early evidence of scale at the Buen Retiro project. One of the most notable intercepts, 384 metres at 0.23% copper, demonstrates consistent mineralisation over a significant interval. Additional results, including 94 metres at 0.33% copper and 108 metres at 0.4% copper, further support the presence of a large system.

While the grades are moderate, the continuity and extent of mineralisation are key considerations. Marr-Johnson highlighted this point, noting that the results “really confirm that we’re in a big system.”

Importantly, the project remains at an early stage of exploration. Only a limited number of drill holes have been completed across a large area, much of which is covered by sand and gravel. Mineralisation has already been identified over a distance exceeding 3.5 kilometres, suggesting significant expansion potential.

To improve targeting, the company is undertaking advanced geophysical surveys, including passive seismic work. These efforts are intended to provide greater resolution on structural controls and help guide future drilling programs.

Additional observations include:

- Mineralisation extending over more than 3.5 kilometres

- Consistent mineralisation across multiple holes

- Early-stage drilling in a largely covered (sand/gravel) area

The project remains in early exploration, with only a handful of holes drilled across a large area. This suggests substantial upside, but also highlights geological uncertainty. The company is supplementing drilling with advanced geophysics, including passive seismic surveys, to better define structures and targets.

Operational Work Program

Fitzroy is currently executing an intensive work program designed to advance both exploration and development objectives. The company is operating two drill rigs on a continuous basis, supported by double-shift core logging and geological analysis. In parallel, metallurgical testing is underway, with approximately 2.8 tonnes of material being collected for analysis. Baseline environmental studies have been ongoing for several months, while engineering and resource estimation work are progressing toward the prefeasibility study.

The company expects to drill between 15,000 and 25,000 metres over the course of the year, depending on results and market conditions. This level of activity reflects both the scale of the opportunity and the benefits of the cost-recovery structure. Management has described the prefeasibility study as being based on “real numbers,” drawing on operating data from its partner. This could enhance the credibility of the study and reduce the gap between prefeasibility and feasibility-level confidence.

Fitzroy is currently operating an intensive exploration and development program:

- Two drill rigs operating 24/7

- Double-shift core logging

- Metallurgical testing underway (2.8 tonnes of material)

- Baseline environmental studies in progress

- Resource estimation and engineering work ongoing

Ownership Structure and Partner Dynamics

The project is currently under an option structure, with full ownership expected by Q2 2027, subject to:

- Completion of technical work

- Required investment thresholds

- Payments to multiple concession holders

At that point, the partner retains a clawback option, reimbursing 90% of expenditures to date.

Management indicated a high probability of this occurring:

- Partner has underutilised processing infrastructure

- Economic incentive to secure feedstock

- Active engagement in joint venture discussions

While this creates alignment, it also introduces dependency on third-party decisions.

Risks and Challenges

Despite the positive indicators, Fitzroy’s investment case is not without risk. The company remains in the early stages of exploration, and further drilling will be required to fully define the resource and understand grade distribution. Execution risk is also present, particularly in relation to the delivery of the prefeasibility study and the transition from exploration to development. Metallurgical outcomes, engineering assumptions, and cost estimates will all need to be validated.

A further consideration is partner dependency. The company’s strategy relies on access to third-party infrastructure and the successful execution of clawback agreements. While management has expressed confidence in these arrangements, they remain outside Fitzroy’s direct control. Finally, broader market conditions, including copper price volatility and financing environments, will influence the company’s ability to advance its projects.

So despite the positive narrative, several risks remain:

Execution Risk

- Delivery of PFS on schedule

- Transition from exploration to development

- Metallurgical and engineering outcomes

Partner Risk

- Finalisation of agreements

- Reliance on third-party infrastructure

- Clawback mechanism execution

Geological Risk

- Early-stage exploration

- Grade variability across the system

- Need for further drilling to define resources

Market Risk

- Copper price volatility

- Financing conditions for development

Operational Risk

- Scaling from exploration to production

- Cost control during expansion

These risks are typical of junior mining companies but are partially mitigated by the company’s capital position and partnerships.

Investment Thesis

The Investment Thesis for Fitzroy Minerals:

- Capital-efficient exploration model (10% effective cost) enhances capital productivity

- Near-term production pathway via oxide heap leach project

- Strategic use of existing infrastructure reduces capex and permitting risk

- Evidence of a large-scale copper system with district potential

- Strong balance sheet reduces short-term financing risk

- Key risk: dependency on partner agreements and execution of PFS

- Actionable: Monitor PFS delivery (Q1 next year) and JV confirmation as key catalysts

Fitzroy Minerals presents an emerging copper story that combines early-stage exploration upside with a structured pathway to production. The company’s recent financing strengthens its balance sheet at a critical stage, allowing it to accelerate drilling and technical work without immediate reliance on additional capital markets.

The defining feature of the investment case is its capital efficiency. Through a partner clawback mechanism, Fitzroy is effectively exploring at a fraction of the typical cost, enabling a level of activity that would otherwise require significantly more funding. This, combined with access to existing processing infrastructure, positions the company to potentially move into production faster and with lower capital intensity than many peers.

However, the story remains contingent on execution. The delivery of a prefeasibility study, confirmation of joint venture arrangements, and continued drilling success will be key milestones. Investors should also be mindful of the inherent risks associated with early-stage exploration and reliance on third-party partnerships. Overall, Fitzroy offers a differentiated exposure to copper, where capital discipline and strategic structuring may prove as important as geology in driving value.

Merlin Marr-Johnson, CEO, of Fitzroy Minerals

Macro Thematic Analysis for Copper

The copper market continues to be shaped by structural supply constraints and rising demand from electrification, renewable energy, and grid expansion. Industry forecasts consistently highlight a looming supply gap, driven by declining grades, permitting challenges, and underinvestment in new projects. Within this context, junior developers with credible pathways to production are increasingly relevant. However, capital intensity remains a key barrier. Many projects require significant upfront investment, often exceeding $1 billion, which limits development in volatile markets. Fitzroy’s approach addresses this challenge directly. By leveraging existing infrastructure and structuring partnerships that reduce capital requirements, the company aligns with a broader industry shift toward capital-light development models.

The CEO’s comment captures this positioning:

“We have these incredible shortcuts in terms of permits and also in terms of capex.”

This reflects a growing recognition across the sector that speed to production and capital efficiency may be more valuable than sheer resource size.

At the same time, the ability to fund exploration internally through future oxide production introduces a self-sustaining growth model. This reduces reliance on equity markets, which have historically been cyclical and dilutive. For investors, the key thematic takeaway is clear: in a constrained capital environment, companies that can advance projects with lower upfront investment and faster timelines may command a premium.

Ptolemy Capital is a significant share holder in Fitzroy Minerals, and contunues to invest.

Analyst's Notes

Subscribe to Our Channel

Stay Informed