From Cost to Security: How the IEA's 2026 Critical Minerals Declaration Is Repricing Jurisdictional Risk Across Battery Metal Supply Chains

Critical minerals reclassified as strategic assets, jurisdiction, ESG compliance, and policy alignment now drive valuation over cost position alone.

- Governments are formally reclassifying critical minerals as strategic assets, accelerating state-directed intervention across supply chains.

- The IEA Ministerial Declaration (February 2026) signals a coordinated global shift toward stockpiling, emergency response frameworks, and supply chain diversification.

- This transition is repricing jurisdictional risk, with Western-aligned and ESG-compliant assets commanding valuation premiums over low-cost but geopolitically concentrated supply.

- Energy market shocks are transmitting directly into mining cost structures, compressing margins for high-energy-intensity producers and widening the cost curve bifurcation.

- Companies with bottom-quartile all-in sustaining costs, secure jurisdictions, and credible ESG frameworks are increasingly positioned to attract development finance institutions and sovereign capital.

From Market Efficiency to Strategic Control in Critical Minerals

For most of the past two decades, global critical minerals markets operated on cost minimization. Supply gravitated toward the lowest-cost producers regardless of geography, and capital followed. That framework is now being restructured through government policy intervention, geopolitical supply concentration, and ESG-driven financing constraints.

The energy transition has driven exponential demand growth for lithium, nickel, cobalt, graphite, and rutile, materials essential to batteries, electric vehicles, and grid-scale storage. But that demand has also exposed a systemic vulnerability: critical minerals supply chains are dangerously concentrated in jurisdictions that are either geopolitically contested or misaligned with Western industrial policy.

In February 2026, the IEA issued a Ministerial Declaration explicitly framing minerals as instruments of geopolitical leverage, a coordinated signal that state-backed institutions intend to intervene in how critical minerals are sourced, processed, and stockpiled. Meanwhile, energy market shocks from the Middle East are feeding cost inflation through mining and processing operations globally, compounding supply chain fragility. The market is transitioning from cost optimization to supply security as the dominant investment filter, with direct implications for capital allocation: assets in geopolitically stable jurisdictions with credible ESG frameworks are attracting preferential financing from development finance institutions and sovereign capital, while projects in high-concentration or geopolitically exposed geographies face a structural cost-of-capital penalty that is likely to widen as policy frameworks mature.

Governments Move to Secure Critical Minerals

The IEA Ministerial Declaration introduces national stockpiling, emergency response frameworks, mandated supply diversification, and enhanced trade transparency, marking a shift from market-driven supply management to coordinated policy architecture, with direct precedent in how Western governments treat oil reserves and defense inputs. The capital markets implications are already visible: subsidies, state-backed partnerships, and export controls are being deployed as supply policy instruments, meaning allocation decisions are now shaped by policy alignment and jurisdictional classification as much as asset economics. Assets qualifying for development finance institution support or government-backed offtake agreements carry financing advantages not yet fully reflected in market valuations.

Canada Nickel Chief Executive Officer Mark Selby has observed that European industrial nations are moving to underwrite project development as a supply security measure:

"Germany and France want those critical minerals, and they're prepared to help fund the mining projects to secure them."

The institutional architecture for state-backed critical minerals financing is being constructed in real time, and developers with projects in recognized Tier-1 jurisdictions are the primary beneficiaries. The relevant question for investors is not whether this capital will arrive, but which assets are positioned to receive it first.

Building the Ex-China Supply Chain

Energy Fuels CEO Mark Chalmers has articulated the same logic from the perspective of a fully integrated critical minerals producer building outside the Chinese supply chain:

"To really compete with China, you have to have all those steps, you can't afford to miss a single one."

This imperative, spanning mining, hydrometallurgical processing, and metal alloy production, is precisely the supply chain architecture that Western governments and offtakers are seeking to underwrite as an alternative to Chinese dominance. The relevant question for investors is not whether this capital will arrive, but which assets are positioned to receive it first.

Cost Inflation & Supply Chain Stress

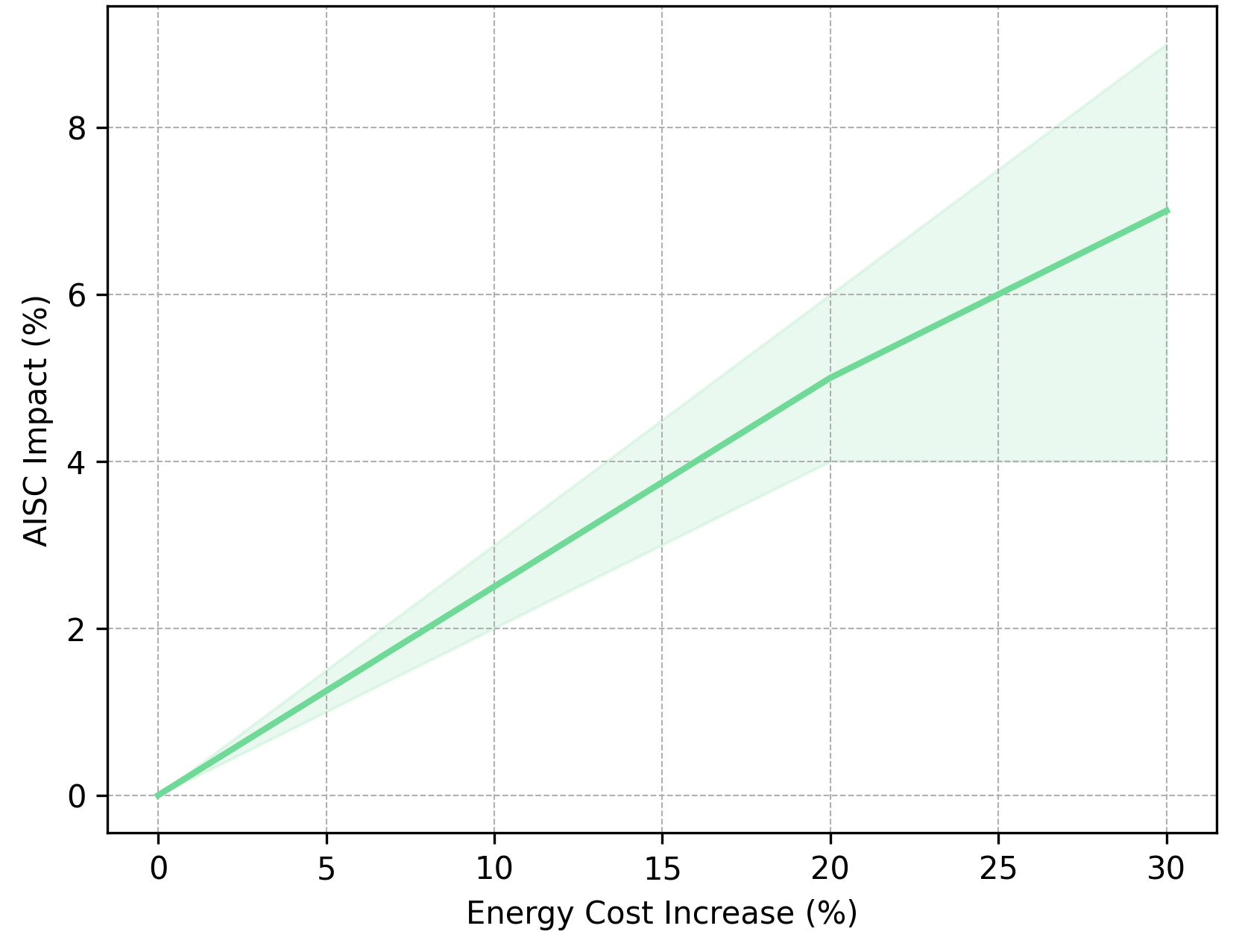

The IMF, World Bank, and IEA have jointly flagged Middle East-driven energy instability as a source of sustained cost inflation across commodity supply chains, and for critical minerals, the transmission is direct. Mining is among the most energy-intensive industrial sectors, with diesel, electricity, and natural gas embedded across extraction, haulage, and refining. When energy prices spike, operating costs follow within quarters.

High-pressure acid leach processing for nickel laterites is particularly exposed, making Indonesian operations especially vulnerable; the Philippines, while a significant laterite ore producer, faces compounding pressure from the environmental and social risks associated with nickel extraction, risks that institutional investors are increasingly scrutinizing across both jurisdictions. Broadly, a 20-30% increase in energy input costs translates to roughly 4-9% inflation in all-in sustaining costs depending on energy mix and hedging, enough to push producers near the upper quartile of the cost curve into negative cash margins.

Operations with low strip ratios, shallow deposits, or access to low-cost hydroelectric power are structurally insulated in ways thermal-powered operations are not, a distinction institutional analysts are increasingly using to differentiate assets within the same commodity category.

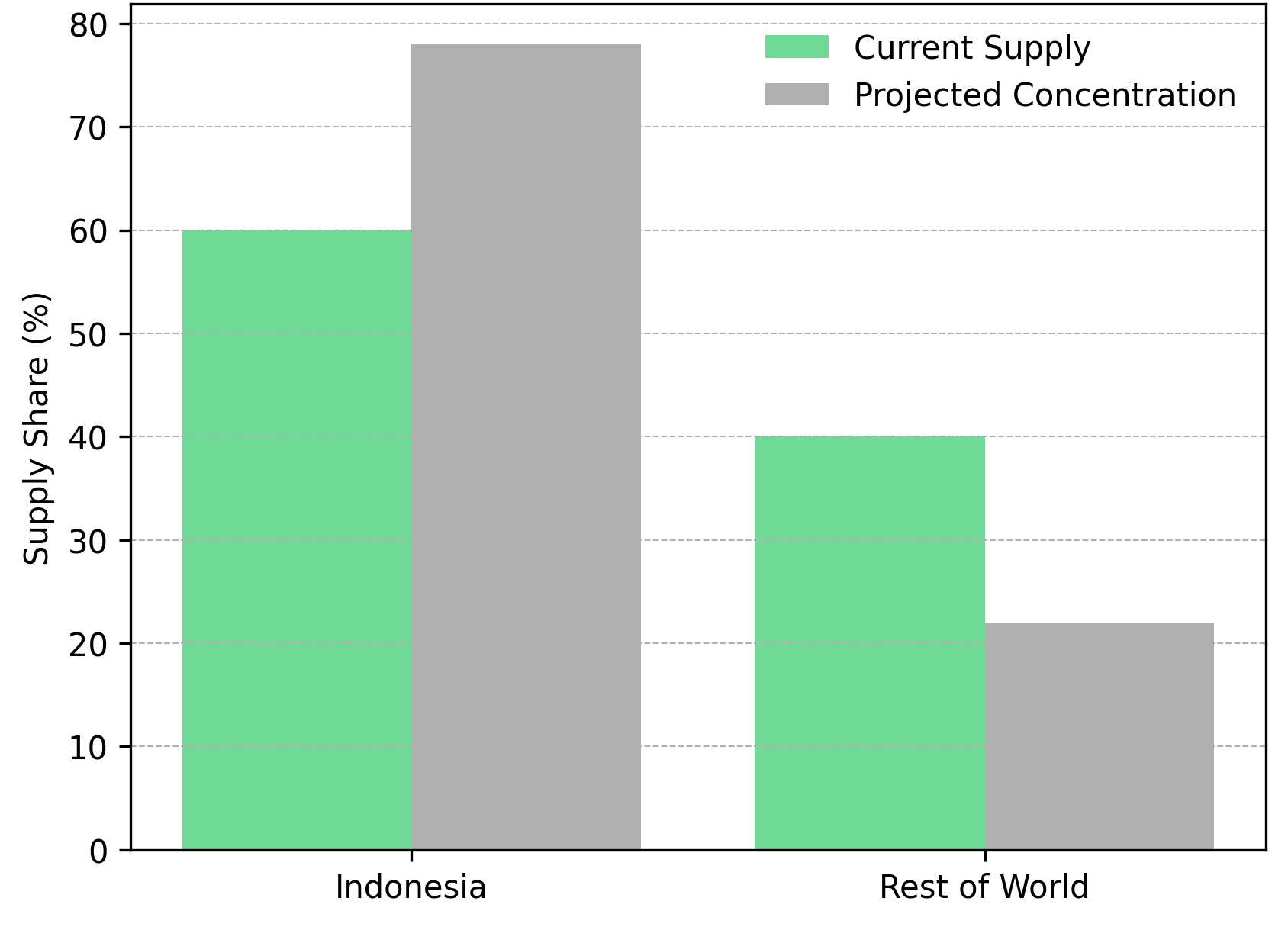

Supply Chain Fragmentation & ESG Constraints in Nickel

Indonesia accounts for over 60% of global nickel supply, the majority from high-pressure acid leach and rotary kiln electric furnace operations carrying significant environmental and social risks. A coalition of institutional investors representing approximately $4.5 trillion in AUM has placed ESG compliance at the center of procurement criteria, creating direct pressure on downstream manufacturers and offtake counterparties to source from operations meeting IFC Performance Standards.

On the risk of further concentration in Indonesian supply, Lifezone Metals Chief Financial Officer Ingo Hofmaier has articulated the threshold that Western policy is trying to avoid:

"If development continues in Indonesia, you could be looking at 75 to 80% of global supply. Western governments simply don't want to find themselves in a position where that dependency keeps growing."

This concentration is creating a bifurcation between ESG-compliant and non-compliant nickel supply. Deforestation risks, environmentally driven permitting delays, and potential export restrictions from producing governments are all introducing cost and supply interruption risk into the Indonesian supply base.

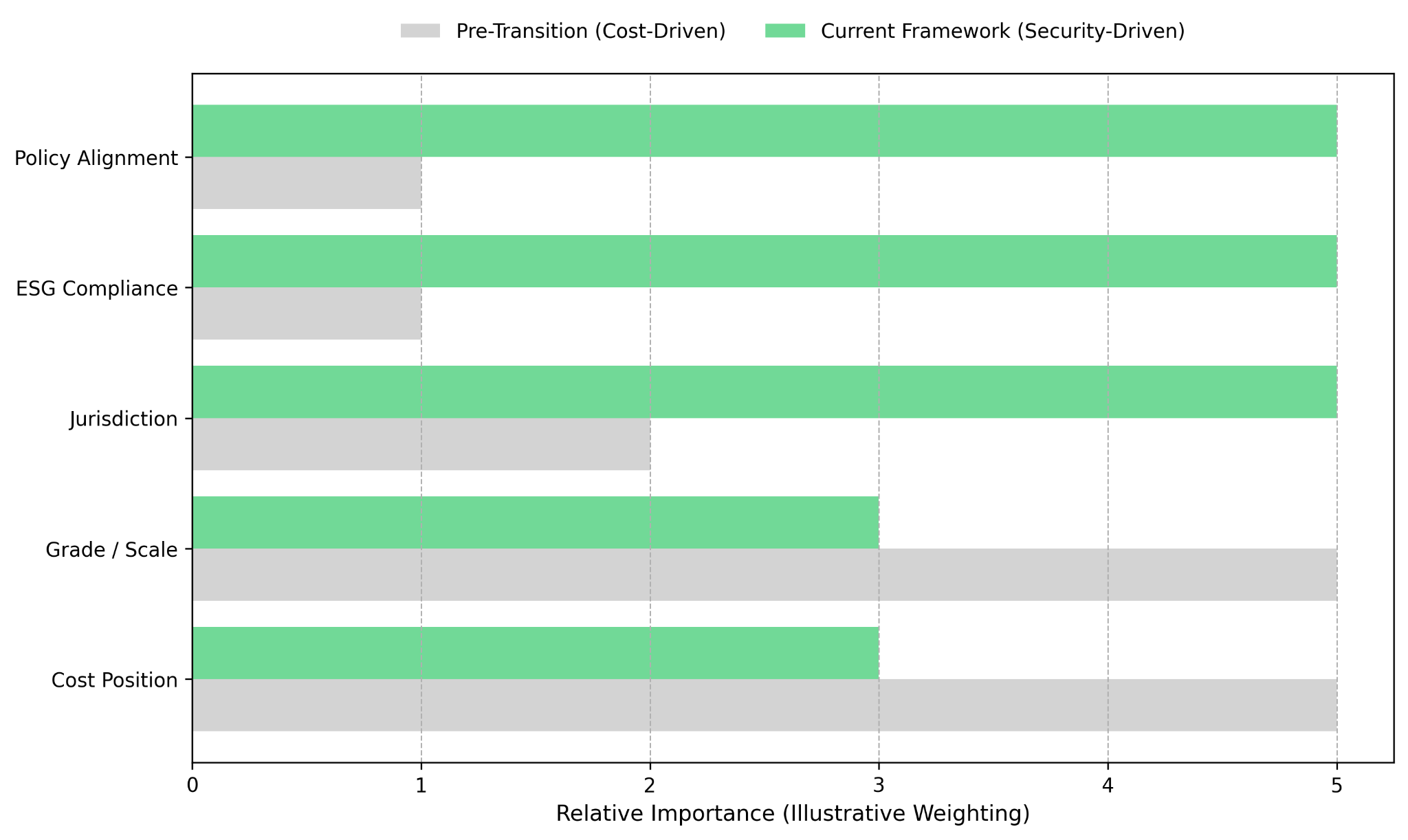

Western Assets Gain Strategic Premium

Jurisdiction has historically been a secondary valuation consideration in mining, subordinate to grade, scale, and cost position. Policy support availability, ESG compliance pathway, and supply security classification are now primary drivers of development-stage asset valuation, particularly for projects seeking development finance institution debt or government-linked equity.

Canada Nickel's Crawford Nickel-Cobalt Sulphide Project in Ontario illustrates this repricing dynamic. Situated in one of the world's most established mining jurisdictions, Crawford is progressing through federal permitting under Canada's critical minerals strategy and is positioned explicitly as an alternative to Indonesian supply for North American and European battery manufacturers. The Definitive Feasibility Study supports an NPV aligned with institutional financing requirements, with capex of approximately $2.5 billion and a targeted production timeline of 2028.

Sovereign Metals' Kasiya Rutile-Graphite Project in Malawi sits at the bottom of the global cost curve, underpinned by free-dig ore with low sulfur content producing high-value flake graphite, providing a structural margin buffer that higher-cost operations cannot replicate. Chairman Ben Stoikovich has noted that even at lower battery-grade graphite prices, Kasiya targets a 50% operating margin, a cost position that qualifies for the financing structures development finance institutions are currently deploying.

ESG, Bankability & Capital Flows

Development finance institutions, including the IFC, US Export-Import Bank, and European export credit agencies, are increasingly functioning as the primary financing conduit for critical minerals projects outside China. Their capital comes with IFC Performance Standards requirements across environmental management, community engagement, and labor practices. Projects demonstrating empirical compliance attract a meaningfully lower cost of capital and higher financing probability.

Ben Stoikovich, Chairman of Sovereign Metals, has demonstrated measurable community and environmental outcomes at Kasiya that directly address the bankability criteria required by development finance institutions:

"We'd be selling graphite at a 50% operating margin, even if we only sold into the lower-value battery graphite market."

The project's rehabilitation track record, including documented 5x agricultural yield improvement on reclaimed land and a structured community partnership model, provides the empirical ESG evidence base that development finance institutions require before committing capital. The Definitive Feasibility Study is progressing with the intent to de-risk financing assumptions through operational data rather than forward projections, a distinction that materially affects bankability. Alignment with IFC Performance Standards at this stage improves both the probability and cost of securing concessional financing relative to commercial alternatives.

Recycling & Secondary Supply Chains

Both the IEA declaration and the broader critical minerals policy architecture explicitly prioritize circular economy development and battery recycling as tools for reducing dependence on Chinese processing and primary supply from Russia and Africa. The strategic logic is straightforward: domestically sourced recycled battery material is the only supply chain entirely insulated from geopolitical risk.

Lifezone Metals' hydrometallurgical processing technology, applied to the Kabanga Nickel Project in Tanzania, targets nickel recovery rates exceeding 99%, materially above conventional smelting, while generating substantially lower emissions per tonne of output. Management has disclosed a project NPV of $1.66 billion supporting a 23.3% after-tax IRR, with Final Investment Decision targeted for Q2 2026 and Glencore holding a strategic position.

A $3.36 per pound all-in sustaining cost net of byproduct credits, combined with processing technology that produces Class 1 battery-grade nickel without Chinese refining, creates a supply chain proposition that directly addresses what North American and European off-takers require: allied-jurisdiction sourcing with verified ESG credentials.

The Investment Thesis for Battery & Critical Metals

- Structural demand growth from electric vehicle adoption, grid-scale energy storage deployment, and industrial electrification provides a multi-year demand floor independent of short-term commodity price cycles.

- Government-backed supply chain diversification mandates, formalized through the IEA declaration and bilateral critical minerals agreements, are creating subsidized financing pathways for qualifying projects, reducing development risk and cost of capital for Tier-1 jurisdiction developers.

- Supply constraints driven by ESG compliance requirements and permitting bottlenecks in high-concentration geographies are structurally limiting the volume of compliant material available to downstream manufacturers, supporting a durable premium for qualifying supply.

- Energy cost inflation is widening the spread between low-cost and high-cost producers, with bottom-quartile all-in sustaining cost assets in low-strip-ratio, energy-efficient operations benefiting from structural margin protection that high-cost incumbents cannot easily replicate.

- Projects such as Canada Nickel's Crawford, Sovereign Metals' Kasiya, and Lifezone Metals' Kabanga offer exposure to jurisdictional diversification, cost curve positioning, and ESG bankability characteristics that align directly with the investment criteria being applied by development finance institutions and sovereign wealth vehicles entering the sector.

- Development timelines targeting first production between 2027 and 2029 are aligned with the period during which battery metal demand is projected to outpace the supply additions currently under construction, supporting the probability of premium pricing conditions at the point of production ramp-up.

- Hydrometallurgical and processing technology innovations, as demonstrated at Kabanga, offer risk-adjusted growth optionality by enabling higher-margin output from the same resource base, reducing dependence on Chinese downstream processing and improving off-take commercial terms.

The critical minerals sector is transitioning from efficiency-driven globalization to security-driven regionalization. The IEA Ministerial Declaration is not the cause of this shift, it is its institutional formalization.

The practical implication is that competitive advantage is defined by three previously secondary variables: jurisdiction, ESG compliance, and policy alignment. Assets that score well on all three are positioned to attract capital on terms, cost, structure, and partnership quality, creating durable enterprise value premiums. Assets that fail on any one face a financing constraint that may be structural rather than cyclical. The repricing is underway, and the divergence between qualifying and non-qualifying assets is likely to widen as policy frameworks mature and institutional capital accelerates.

TL;DR

Governments are formally reclassifying critical minerals as strategic assets, dismantling the cost-minimization logic that organized global supply chains for two decades. The IEA Ministerial Declaration signals coordinated state intervention in how minerals are sourced, processed, and stockpiled, creating a new valuation hierarchy in which jurisdiction, ESG compliance, and policy alignment now outweigh cost position alone. For investors, this means assets in Tier-1 jurisdictions with credible ESG frameworks and development finance institution eligibility, such as Canada Nickel's Crawford, Sovereign Metals' Kasiya, and Lifezone Metals' Kabanga, are structurally positioned to attract capital at terms that lower-cost but geopolitically exposed operations cannot match.

FAQs (AI-Generated)

The convergence of energy transition demand, supply chain concentration, and geopolitical realignment has exposed a systemic vulnerability that markets previously underpriced. Lithium, nickel, cobalt, graphite, and rutile are essential to batteries, electric vehicles, and grid-scale storage, but their supply is dangerously concentrated in jurisdictions that are either geopolitically contested or misaligned with Western industrial policy. The IEA Ministerial Declaration of February 2026 formalized what capital markets had already begun pricing: that supply security, not cost efficiency, is now the dominant organizing principle for critical minerals investment.

Mining is among the most energy-intensive industrial sectors, with diesel, electricity, and natural gas embedded across extraction, haulage, and refining. Middle East-driven energy instability, flagged jointly by the IMF, World Bank, and IEA, is transmitting directly into mining operating costs, with a 20-30% increase in energy input costs translating to roughly 4-9% inflation in all-in sustaining costs. This compression is particularly acute for high-pressure acid leach nickel operations in Indonesia and the Philippines, and is widening the cost curve bifurcation between energy-efficient, low-strip-ratio operations and conventional thermal-powered producers.

Indonesia currently accounts for over 60% of global nickel supply, with projections suggesting that figure could reach 75-80% if current development trajectories continue. The majority of Indonesian production comes from processing routes carrying significant environmental and social risks that fail to meet IFC Performance Standards, the baseline requirement for institutional ESG compliance. Deforestation risks, permitting delays, and potential export restrictions are introducing supply interruption risk that the market has historically underpriced, creating structural demand for ESG-compliant alternative supply from Western-aligned jurisdictions.

Development finance institutions, including the IFC, U.S. Export-Import Bank, and European export credit agencies, require empirical rather than prospective ESG compliance across environmental management, community engagement, and labor practices. Projects that can demonstrate measurable outcomes, such as documented agricultural yield improvements on rehabilitated land or structured community partnership models, attract meaningfully lower cost of capital and higher financing probability than projects offering only forward-looking commitments. Bottom-quartile cost positioning and Tier-1 or allied jurisdiction classification are additional criteria that determine eligibility for the concessional financing structures currently being deployed.

The investment case rests on the convergence of structural demand growth, policy-backed financing, and supply constraint. Electric vehicle adoption, grid-scale energy storage, and industrial electrification provide a multi-year demand floor independent of short-term price cycles, while government-backed diversification mandates are creating subsidized financing pathways that reduce development risk for qualifying projects. Supply constraints driven by ESG requirements and permitting bottlenecks in high-concentration geographies are limiting the volume of compliant material available to downstream manufacturers, supporting a durable premium for assets that meet the new criteria. Development timelines targeting first production between 2027 and 2029 align with the period during which battery metal demand is projected to outpace supply additions currently under construction.

Analyst's Notes

Subscribe to Our Channel

Stay Informed