Gold Continues to Be Priced Toward $4,700+ in 2026 as Geopolitical and Monetary Risks Persist

Median forecasts reach $4,746.50/oz as institutional allocators reassess sovereign debt exposure and Federal Reserve independence.

- Median 2026 gold forecasts have been revised to $4,746.50/oz, marking one of the most aggressive year-on-year upgrades in recent history.

- Concerns over Federal Reserve independence, sovereign debt expansion, and trade fragmentation are driving renewed safe-haven allocations.

- Official sector demand remains a structural pillar of the gold market as reserve diversification accelerates.

- The move from $5,600 highs to $4,403 lows and back near $5,100 highlights extreme macro sensitivity to political and monetary signals.

- At $4,700+ gold, margin expansion for producers and developers with sub-$1,300/oz All-In Sustaining Cost materially reshapes Net Present Value, Internal Rate of Return, and enterprise value per ounce valuations.

Institutional Stress & Structural Gold Forecast

Escalating sovereign debt burdens across developed economies, persistent uncertainty around Federal Reserve independence, ongoing geopolitical fragmentation, and structural trade realignment have combined to drive reallocation toward hard assets.

The recent surge in gold forecasts to $4,746.50/oz reflects more than cyclical inflation hedging. It represents a reassessment of institutional credibility and monetary durability that has fundamentally altered how allocators model portfolio risk.

The metal experienced its worst two-day decline since 1983, followed by its strongest single-day rebound in over 17 years. The price action illustrates how responsive markets have become to perceived shifts in monetary policy credibility.

Central Bank Accumulation as a Structural Demand Anchor

While jewelry demand contracts at elevated prices, official sector demand remains robust. Central bank buying has shifted the marginal buyer profile of gold from consumer-led to sovereign strategic allocation, driven by reserve diversification away from dollar concentration, geopolitical hedging requirements, and reduced institutional trust in Western-led monetary frameworks.

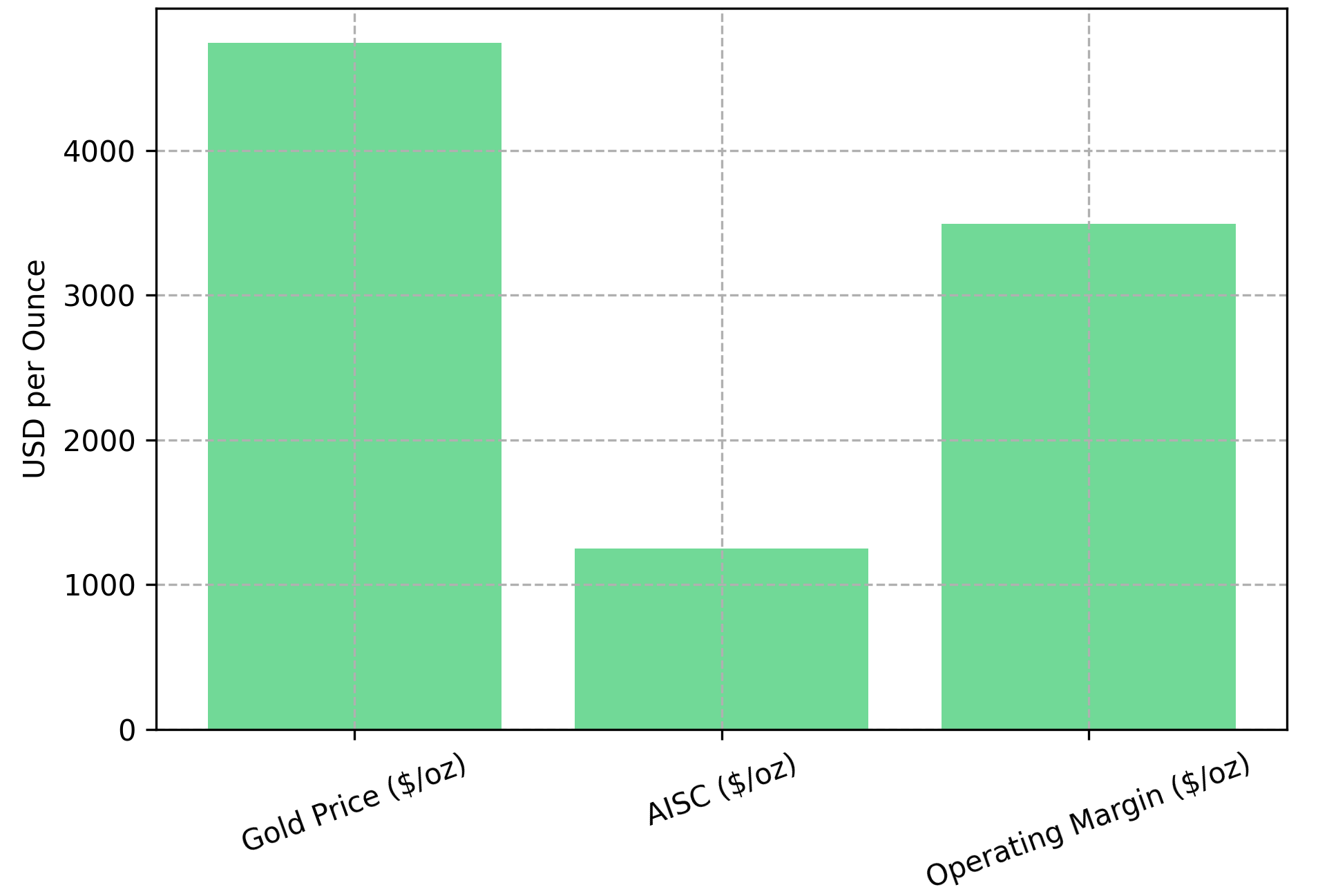

Margin Expansion Mechanics at $4,700+ Gold

With gold trading near $4,746/oz, the economics of gold production have shifted substantially. A producer running all-in sustaining costs of around $1,250/oz is capturing roughly $3,500/oz in margin. At these margin levels, projects that were borderline viable at $1,800 or $2,000 gold now generate meaningfully higher returns, and the value of an ounce still in the ground rises sharply.

Not all gold producers benefit equally at these prices. Three types of operations tend to stand out. First, high-grade underground mines - where ore quality is high enough that cost-per-ounce stays low even with expensive underground extraction - see their margins widen fastest. Second, heap leach projects processing oxide ore with minimal waste stripping offer low capital intensity and faster payback, meaning investors recover their money sooner. Third, developers sitting close to a construction decision - where permits are either in hand or expected shortly — are positioned to break ground while prices remain elevated, rather than waiting through years of approvals that could see the window close.

The Chief Executive Officer of i-80 Gold, Richard Young, quantifies the valuation disconnect emerging at current prices:

"The NAV of the five gold projects at $3,000 gold was about $5 billion US. These prices are somewhere between 8 and 10, and our market cap is maybe 1.3 billion."

i-80 Gold, currently producing from its Nevada operations, holds 6.5Moz gold-equivalent in Measured and Indicated categories with an additional 7.5Moz Inferred across its Nevada portfolio. The company's Archimedes PEA indicates 81% Internal Rate of Return at $3,000 gold, while the Cove project shows 54% Internal Rate of Return with All-In Sustaining Cost of $1,303/oz.

Perseus Mining operates three producing gold mines — Yaouré and Edikan in Côte d'Ivoire and Ghana respectively, and Sissingué in Côte d'Ivoire — while advancing the Nyanzaga development project in Tanzania. Group production guidance for FY2026 is 400,000 to 440,000 ounces, underpinned by a portfolio that balances operational cash flow generation with capital-funded organic growth.

Development Assets & NPV Leverage

Integra Resources operates a blended model combining Florida Canyon production, targeting approximately 70,000 oz gold-equivalent annually, with DeLamar development. The DeLamar Feasibility Study identifies $1.9 billion Net Present Value at a 5% discount rate and 97% Internal Rate of Return at $3,000 gold.

George Salamis, President and Chief Executive Officer of Integra Resources, describes the capital allocation discipline enabled by current market conditions:

"$60 million was the targeted raise... We’re very well subscribed, three times oversubscribed. There's 12 or so new institutions in the book including three generalist funds, it was really well accepted."

High-Grade Deposits & Capital Efficiency Considerations

Grade is one of the most important variables in gold mining economics, and at current prices its effect is amplified. A deposit running above 2.5 grams of gold per tonne of ore processes more value per tonne moved, which has a cascading effect on project economics: less rock needs to be mined and moved to produce the same ounce, processing plants can be smaller relative to output, and the capital required to build the mine is lower relative to the gold it will produce. The result is a project that can absorb cost increases - labour, energy, consumables - without seeing margins collapse the way a lower-grade operation might. This is why high-grade assets tend to attract premium valuations, particularly when investors are paying close attention to which operations can stay profitable if prices pull back.

New Found Gold's Queensway project in Newfoundland represents this high-grade development profile, with a Preliminary Economic Assessment indicating 1.39Moz at 2.40 g/t Au, All-In Sustaining Cost of $1,256/oz, and Internal Rate of Return of 56.3% at $2,500 gold base case pricing. Environmental Assessment submission is anticipated in late Q1 2026, with baseline work already complete.

The company completed its acquisition of Maritime Resources in 2025, securing the Pine Cove mill which has commenced ramp-up and is advancing toward steady-state production in 2026.

Hashim Ahmed, Chief Financial Officer of New Found Gold, explains the capital approach enabled by phased development:

"This phased approach of building Queensway enables us to be more disciplined in capital allocation. This enables us to reduce construction risk because we just acquired Maritime Resources and there's a Pine Cove mill."

Serabi Gold operates in Pará State, Brazil — ranked second in Brazil for mining investment climate — with two high-grade assets in the Tapajos region: the producing Palito Complex and the Coringa development project. The company is targeting consolidated production of approximately 60,000 oz by 2026 as Coringa advances toward full operation.

Oxide Projects & Rapid Payback Profiles

Low-capital expenditure oxide projects offer rapid payback in volatile macro environments, providing investors with exposure to gold price sensitivity while limiting construction and execution risk.

U.S. Gold Corp's CK Gold project in Wyoming demonstrates this profile, with the February 2025 Pre-Feasibility Study indicating Internal Rate of Return of 39.4%, Net Present Value of $532 million at a 5% discount rate and $2,500 gold, and All-In Sustaining Cost of $937/oz gold-equivalent. The project holds full permitting approval, having received its Mine Operating Permit in April 2024 and Industrial Siting Permit in June 2023, with no federal involvement required. Definitive Feasibility Study engineering is advancing toward completion in early 2026.

Luke Norman, Executive Chairman of U.S. Gold Corp, emphasizes the jurisdictional and permitting advantages:

"We received our final non-conditional permit to mine... We're one of the only junior mining companies with a fully permitted shovel-ready project in North America."

Cabral Gold's Cuiú Cuiú project sits in the Tapajos Gold Province of northern Brazil, the same district that hosts G Mining's Tocantinzinho operation. The project holds two main deposits approximately 5 kilometres apart, with Indicated resources of 12.29Mt at 1.14 g/t gold for 450,200 oz in primary material and an additional 216,182 oz in oxide material. Recent drilling has returned intercepts including 23.8m at 5.5 g/t gold, reinforcing the grade profile ahead of maiden resource estimates for new discoveries expected later in 2026.

Nevada Concentration & Jurisdictional Premium Dynamics

Jurisdiction risk premium remains critical in high-price cycles, with established mining jurisdictions commanding valuation premiums that reflect permitting transparency, rule of law, and infrastructure availability.

Hycroft Mining holds one of the largest gold-silver deposits in Nevada, with a Preliminary Economic Assessment and Pre-Feasibility Study targeted for Q1 2026. The company maintains approximately $175 million in cash as of December 2025, providing runway for continued exploration and development.

Diane Garrett, President and Chief Executive Officer of Hycroft Mining, describes the exploration progress and the financial position that supports continued development:

"Not only do we have one of the world's largest gold deposits but also one of the world's largest silver deposits, with two recent very significant high-grade silver discoveries... We have no need to raise capital or money for the next three plus years or more. We've got just shy of 200 million in the treasury."

P2 Gold is advancing its Gabbs project in Nevada toward Feasibility Study completion targeted for Q4 2026, with water permit approval anticipated in early 2026. The company's indicated resource of 1.16Moz gold-equivalent provides a foundation for production scenarios under evaluation.

Joseph Ovsenek, President and Chief Executive Officer, outlined P2 Gold’s development pathway:

"We're focused on advancing our Gabbs project in Nevada to production. We're currently in feasibility study and we expect to get that done this year."

Exploration Optionality in High-Price Regimes

Tudor Gold's Treaty Creek project in British Columbia's Golden Triangle hosts 24.9Moz gold indicated with an additional 4Moz inferred. The company is targeting a Preliminary Economic Assessment in early Q3 2026 while evaluating higher-grade underground zones.

West Red Lake Gold Mines reported 7,379 oz production from its Madsen mine in Q4 2025, with the company maintaining CAD$46 million in cash as of January 2026. The Rowan project represents additional resource upside within the company's portfolio.

Risk Considerations & Macro Fragility

Several scenarios have historically weighed on gold prices: a Federal Reserve that moves decisively to restore its inflation-fighting credibility, pushing real interest rates higher; an unexpected shift toward fiscal restraint that reduces deficit concerns and supports the dollar; or a sustained recovery in the dollar itself, which tends to move inversely to gold. Softer jewelry demand - particularly from large consumer markets such as India and China - can also act as a modest headwind, though its influence is generally smaller than central bank and investment flows at current price levels.

At the company level, the risks are more operational in nature. Permitting processes that run longer than projected can delay construction decisions and erode the value of a development asset. Rising costs for energy, labor, and key consumables can compress margins that look attractive on paper. Changes to royalty or taxation regimes - which governments have historically introduced during high-price cycles - can materially affect what a company actually keeps per ounce produced.

The Investment Thesis for Gold

- The $4,746.50/oz median forecast reflects structural reallocation driven by debt concerns and monetary credibility reassessment.

- Producers with sub-$1,300/oz All-In Sustaining Cost are generating significant free cash flow that supports internal capital deployment and balance sheet strengthening.

- Development projects modeled at $2,500/oz base case assumptions demonstrate nonlinear Net Present Value and Internal Rate of Return expansion at current spot prices.

- Nevada, Newfoundland, and Wyoming jurisdictions offer clearer permitting pathways relative to emerging market alternatives.

- Companies maintaining substantial cash reserves reduce dilution risk and preserve optionality during extended development timelines.

- Feasibility studies, Environmental Assessment submissions, and production ramp-ups align with the elevated price environment across multiple development-stage assets.

- High-grade deposits exceeding 2.5 g/t Au gain renewed strategic interest as producers evaluate reserve replacement through acquisition.

The implications differ across the gold sector depending on where a company sits in the development cycle. Producers with tight cost discipline are converting the price environment into free cash flow at rates that were not achievable at prior price levels. Developers with completed or advanced feasibility work are seeing their project valuations respond sharply to price assumptions, since the economics of a fully-scoped project are more directly leveraged to spot gold than an earlier-stage asset. Explorers are finding it easier to attract capital as the argument for owning gold in the ground - rather than waiting for it to be produced - gains traction with investors looking for earlier-stage exposure.

The central question has shifted from whether gold benefits from the current macro environment to which companies are structured to translate that environment into durable returns. Balance sheet quality, jurisdictional stability, and grade profile are the variables that tend to determine whether a company captures the upside or is consumed by the operational and financial risks that elevated price cycles also bring.

Gold trading above $4,700/oz reflects something more specific than a commodity cycle. Three structural pressures appear to be driving institutional demand: concern about the long-term sustainability of sovereign debt loads across major economies, questions about whether central banks can restore inflation credibility without triggering recession, and the fragmentation of the geopolitical order that underpinned decades of dollar dominance.

TL;DR

Gold's median 2026 forecast of $4,746.50/oz reflects a structural shift in institutional thinking — not merely inflation hedging, but a fundamental reassessment of sovereign debt sustainability, Federal Reserve credibility, and dollar dominance. At these price levels, producers running sub-$1,300/oz all-in sustaining costs are generating margins exceeding $3,500/oz, while development-stage assets are seeing nonlinear NPV and IRR expansion far beyond base-case modeling. High-grade deposits, fully permitted projects, and companies with strong cash reserves in stable jurisdictions like Nevada, Newfoundland, and Wyoming are best positioned to convert the macro tailwind into durable shareholder returns.

FAQs (AI-Generated)

The median 2026 gold forecast of $4,746.50/oz reflects a convergence of structural pressures: escalating sovereign debt burdens across major economies, growing questions about Federal Reserve independence, and the fragmentation of the geopolitical order that previously underpinned dollar dominance. These factors have shifted institutional allocators toward hard assets in ways that go beyond typical inflation-cycle hedging.

At $4,746/oz gold, a producer with all-in sustaining costs of $1,250/oz captures roughly $3,500/oz in margin — a level that transforms project economics, dramatically expands NPV and IRR versus base-case assumptions, and makes previously marginal development assets economically compelling. The leverage is most pronounced for high-grade deposits, low-capex oxide projects, and developers at or near a construction decision.

Official sector demand has become a structural pillar of the gold market, shifting the marginal buyer profile from consumer-driven to sovereign strategic allocation. Central banks are diversifying reserves away from dollar concentration, hedging geopolitical risk, and reducing exposure to Western-led monetary frameworks — demand characteristics that are less price-sensitive than jewelry or retail investment flows.

Nevada, Newfoundland, and Wyoming are highlighted as offering clearer permitting pathways, established rule of law, and infrastructure availability relative to emerging market alternatives. During elevated price cycles, jurisdictional stability commands a valuation premium because permitting delays and regulatory changes can materially erode the economics of development assets.

The primary macro risks include a decisive Fed pivot to restore inflation-fighting credibility — pushing real interest rates sharply higher — unexpected fiscal restraint reducing deficit concerns, and a sustained dollar recovery. At the company level, operational risks include permitting delays, rising input costs for energy and labor, and potential government-imposed royalty or taxation changes that historically emerge during high-price cycles.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed