Gold Mining Supply Constraints Drive M&A Optionality as Structural Scarcity Reprices Development Assets

Gold mining faces severe supply constraints as majors replace <50% of production reserves. M&A activity increases as developers gain strategic value in tight market.

- Structural supply constraints in gold mining, driven by underinvestment, declining reserve replacement, and rising cost curves, are reshaping the sector’s investment dynamics.

- M&A optionality is re-emerging as a central driver, with majors seeking growth through acquisition rather than greenfield exploration.

- Fed policy discord and U.S. fiscal risks sustain gold’s long-term appeal, while short-term volatility provides strategic entry points.

- Development-stage companies with high-grade, low-AISC, and jurisdictional stability stand to benefit disproportionately in this environment.

- Case studies of Cabral Gold (Brazil), New Found Gold (Canada), and i-80 Gold (Nevada) highlight how developers positioned with near-term catalysts can leverage both gold price tailwinds and sector-wide M&A appetite.

Structural Supply Constraints in the Gold Sector

The global gold mining industry faces its most severe supply constraints in decades, fundamentally altering investment dynamics across the sector. World Gold Council data reveals that major producers have consistently replaced less than 50% of annual production through reserve additions since 2016, creating a structural deficit that threatens long-term output sustainability.

This supply crisis stems directly from the capital discipline imposed during the 2010s commodity downturn. The industry's collective response to cost overruns and project failures involved slashing exploration budgets, deferring greenfield development, and prioritizing debt reduction over growth capital.

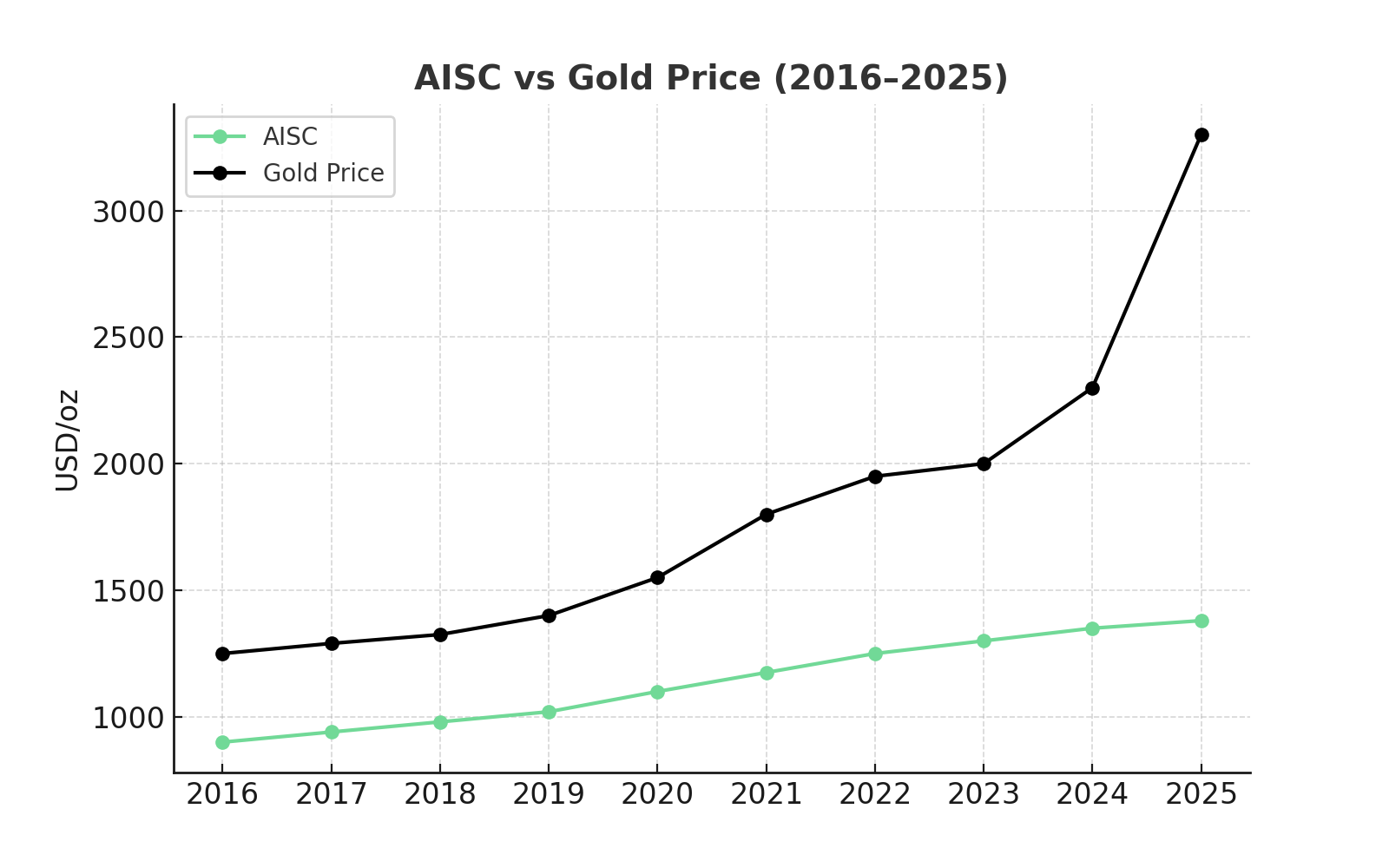

What followed was effectively a "missing decade" of discovery investment, leaving today's majors with aging asset portfolios and diminishing organic growth prospects. Industry-wide all-in sustaining costs have crept above $1,300 per ounce across most major operations, narrowing operating margins even as gold prices have reached multi-year highs.

Rising Development Complexity & Cost Pressures

This cost inflation reflects deeper structural challenges including declining ore grades, deeper mining depths, increased regulatory compliance costs, and labor shortages in key mining jurisdictions. Environmental, social, and governance requirements have introduced additional complexity to new project development.

Permitting timelines have extended significantly across major jurisdictions, while community relations and environmental impact assessments demand increasingly sophisticated approaches. Geopolitical instability in several gold-producing regions has further elevated the risk premium associated with greenfield exploration and development.

The combination of depleted pipeline inventory, rising development costs, and extended permitting cycles has created a fundamental mismatch between supply and demand dynamics. This structural imbalance forces majors to consider alternative growth strategies, with many now viewing acquisition of advanced development projects as a more viable path to production growth than organic expansion.

Investment Implications of Structural Scarcity

For institutional investors, these supply constraints translate into a scarcity premium that increasingly favors development-stage companies with proven resources, favorable jurisdictions, and clear paths to production. The era of abundant, low-cost development opportunities has effectively ended, creating a new paradigm where quality projects command premium valuations.

This scarcity dynamic creates heightened strategic interest from major producers seeking growth opportunities. Development companies with the right combination of resource quality and jurisdictional stability are increasingly viewed as strategic assets rather than speculative investments.

The implications extend beyond simple valuation effects, fundamentally altering how institutional capital approaches gold sector allocation and risk assessment in development-stage opportunities.

The Macro Environment Driving Gold Allocation

The macroeconomic backdrop supporting gold allocation has strengthened considerably, with multiple structural factors converging to sustain long-term demand despite short-term price volatility. Federal Reserve policy discord and credibility erosion create persistent uncertainty around real rate trajectories, undermining confidence in traditional monetary frameworks and reinforcing gold's role as a monetary hedge.

U.S. fiscal dynamics present perhaps the most compelling long-term catalyst for gold investment. Congressional Budget Office projections indicate cumulative deficits exceeding $21 trillion over the next decade, assuming no major policy interventions or economic disruptions.

This debt trajectory, combined with already elevated debt-to-GDP ratios, raises legitimate questions about long-term dollar stability and purchasing power preservation. Recent Federal Reserve communication has revealed significant internal discord regarding appropriate policy responses to persistent inflationary pressures.

Geopolitical Risk & Dollar Weakness Create Technical Support

The central bank's dual mandate creates inherent conflicts between employment objectives and price stability goals, particularly as demographic shifts reduce labor force participation rates. This policy uncertainty keeps real interest rate expectations volatile, supporting gold's appeal as a hedge against monetary debasement.

Persistent geopolitical tensions across multiple theaters, including the ongoing conflict in Ukraine and escalating Middle East instability, sustain safe-haven demand for gold assets. Unlike previous geopolitical episodes that generated temporary spikes in gold prices, current tensions appear more structural and long-lasting, supporting sustained allocation shifts toward alternative monetary assets.

Dollar weakness provides an additional technical floor under gold pricing, with the currency's decline against major trading partners creating favorable conditions for gold-denominated assets. Gold's year-over-year performance of approximately 40% reflects both these currency dynamics and fundamental shifts in institutional allocation patterns.

Institutional Allocation Shifts Support Sector Valuations

The implications for gold equity investors extend beyond simple price exposure. Institutional portfolios are maintaining elevated gold allocations as portfolio hedges, creating sustained demand for both physical bullion and mining equities.

This allocation discipline supports valuation multiples across the gold mining sector, particularly for companies offering leverage to sustained higher gold prices. The structural nature of current monetary challenges suggests these allocation patterns may persist longer than typical cyclical shifts.

Professional portfolio managers increasingly view gold exposure as essential rather than opportunistic, fundamentally changing the demand characteristics for gold-related investments.

Capital Discipline & the Return of M&A in Mining

The gold mining industry's renewed focus on capital discipline has paradoxically created conditions favoring increased merger and acquisition activity, as majors prioritize brownfield expansion and strategic acquisitions over high-risk greenfield exploration. This shift represents a fundamental change from the growth-at-any-cost mentality that characterized the sector during previous commodity cycles.

Major producers are increasingly viewing acquisition of advanced development projects as a more efficient path to production growth than organic expansion. The 2024-2025 period has witnessed a notable uptick in development-stage takeovers, with transactions including the Newcrest acquisition by Newmont and various mid-tier consolidation plays demonstrating renewed appetite for strategic combinations.

Acquisition premiums are being paid specifically for projects offering three critical characteristics: low all-in sustaining costs, high-grade mineralization, and operations in established mining jurisdictions. The scarcity of projects meeting these criteria has created a bidding environment where strategic buyers compete aggressively for quality assets.

Embedded Optionality Creates Value for Development Companies

This M&A environment creates embedded optionality for shareholders of quality development companies. Projects that demonstrate clear paths to low-cost production, scalable resource bases, and minimal jurisdictional risk increasingly trade with takeover premiums built into their valuations.

These premiums effectively represent "free call options" on sector consolidation trends. The strategic rationale driving this acquisition activity extends beyond simple production growth, with majors seeking to acquire projects with long mine lives, expandable resource bases, and operational synergies with existing infrastructure.

The ability to bolt-on production from proven deposits represents a more predictable growth strategy than the traditional approach of grassroots exploration and greenfield development. Current market conditions favor this consolidation trend, with many development companies trading at discounts to net asset value despite holding high-quality projects.

Multiple Value Realization Paths Enhance Risk-Adjusted Returns

This valuation disconnect creates opportunities for strategic buyers to acquire assets below replacement cost, while offering development company shareholders premium exit valuations through corporate transactions. For investors positioning in the development space, this M&A dynamic creates multiple paths to value realization.

Companies can generate returns through successful project development and production growth, or through strategic acquisition at premium valuations. This dual optionality enhances the risk-adjusted return profile of quality development investments.

The combination of scarcity dynamics and strategic buyer appetite suggests that well-positioned development companies may command premium valuations regardless of whether they pursue independent development or strategic sale opportunities.

Companies Positioned for Scarcity & M&A Themes

The intersection of structural supply constraints and renewed M&A appetite creates compelling investment opportunities for development-stage companies positioned with the right combination of resource quality, jurisdictional stability, and operational visibility. Three companies exemplify how strategic positioning can capture value from both gold price appreciation and sector consolidation trends.

Cabral Gold: Brazil's District-Scale Optionality

Cabral Gold's Cuiú Cuiú project in northern Brazil represents a compelling example of how staged development strategies can create multiple value inflection points while minimizing execution risk. The project's proximity to G Mining's Tocantinzinho operation provides critical infrastructure advantages and operational benchmarking opportunities that enhance development certainty.

The company's updated preliminary feasibility study projects a 78% internal rate of return at $2,500 per ounce gold pricing, with economics improving dramatically at current gold price levels. The two-stage development approach begins with oxide material processing requiring initial capital expenditure of approximately $37 million, creating a rapid payback scenario that funds subsequent hard rock development.

Chief Executive Officer Alan Carter emphasizes the project's scalability potential:

"This district could contain 5-10 million ounces plus. The bulk of the 1.3 million ounces inferred and indicated in our current resource base is in the hard rock material."

Exceptional Economics & Self-Funding Development Model

The oxide starter operation targets annual gold production of 25,000 to 40,000 ounces with exceptional recovery rates of 87%, generating projected annual pre-tax cash flows of $50-60 million. This cash generation capability enables self-funding of the larger hard rock development phase, which represents the project's primary value driver.

Cabral's 50+ exploration targets across the district-scale land package provide substantial resource expansion optionality. The systematic approach to target development, combined with proven mineralization systems, creates multiple avenues for resource base growth that could attract strategic interest from regional producers seeking long-term growth platforms.

Near-term catalysts include an updated prefeasibility study expected in July 2025, construction decision timing in Q3 2025, and maiden resource estimates for newly discovered zones. This catalyst sequence creates multiple opportunities for value realization through both operational progress and potential strategic transactions.

New Found Gold: Newfoundland's High-Grade Camp Potential

New Found Gold's Queensway Project in Newfoundland demonstrates how exceptional grade and jurisdictional advantages can create compelling development economics even in higher-cost mining environments. The project's 79% indicated category resource classification provides unusual development certainty for an early-stage asset.

Drill results including 42.8 grams per tonne over 14.95 meters highlight the ultra-high grade nature of the mineralization, creating significant leverage to gold price movements. The preliminary economic assessment projects a 56% internal rate of return at $2,500 per ounce gold pricing, improving to 197% at current price levels of approximately $3,300 per ounce.

Chief Executive Officer Keith Boyle outlines the phased development approach:

"The preliminary economic assessment highlights a phased approach that gets us to cash flow rapidly. Phase one will be building a 700 ton a day mine open pit mine but we'll be toll milling custom milling at a custom mill in the area."

Strategic Institutional Support & Camp-Scale Discovery Potential

The initial capital requirement of $155 million for phase one operations creates a less than two-year payback period, with subsequent phases funded through operational cash flow. This financial structure minimizes dilution risk while providing clear visibility on development funding requirements.

The property package spans 175,600 hectares with only approximately 5 kilometers drilled to date, creating substantial exploration upside potential. The combination of proven high-grade mineralization and extensive prospective ground positions New Found as a potential camp-scale discovery in one of Canada's most established mining jurisdictions.

Institutional support from Eric Sprott (19% ownership) and other strategic investors provides both financial backing and sector credibility. The bulk sampling program currently underway will provide critical metallurgical data supporting feasibility study advancement and potential strategic partnership discussions.

i-80 Gold: Nevada's Multi-Asset Growth Platform

i-80 Gold's Nevada-focused portfolio represents the most advanced example of how multi-asset strategies can create scalable production platforms attractive to strategic acquirers. The company's 14 million ounce resource base ranks as the fourth largest in Nevada, providing substantial scale and operational flexibility.

The portfolio approach enables optimization across multiple development projects, with underground operations at Archimedes (75% IRR), Granite Creek (50% IRR), and Cove (52% IRR) feeding existing processing infrastructure. Combined net present value across all projects totals $4.5 billion at $2,900 per ounce gold pricing.

The Ruby Hill carbonate replacement deposit discovery adds unique polymetallic leverage to the portfolio, with recent drilling results including 238 grams per tonne silver with significant lead and zinc credits. This discovery creates rare strategic optionality in the Nevada gold sector, where most deposits are simple gold systems.

Strategic Asset Scale Attracts Consolidation Interest

The phased growth strategy targets production exceeding 500,000 ounces annually by the early 2030s, positioning i-80 as a potential mid-tier producer in the world's premier gold mining jurisdiction. This production scale, combined with Nevada's favorable mining regulations and infrastructure, creates an attractive strategic asset for major producers seeking U.S.-based growth platforms.

Near-term development catalysts include portal development at Ruby Hill scheduled for Q3 2025 and feasibility studies across multiple projects throughout 2025-2026. This catalyst sequence provides multiple inflection points for operational progress and potential strategic interest from consolidation-focused majors.

The combination of proven resources, existing infrastructure, and Nevada jurisdiction positioning creates compelling strategic value for potential acquirers seeking established platforms for organic growth and operational synergies.

Investor Positioning in a Scarcity-Driven Cycle

The convergence of structural supply constraints and renewed strategic acquisition activity creates a fundamentally different investment environment for gold sector positioning. Institutional and retail investors are increasingly recognizing that development-stage companies offer superior leverage to both gold price appreciation and sector consolidation trends compared to established producers.

Development-stage optionality provides asymmetric upside potential that established producers cannot match due to their larger scale and more mature asset bases. While major producers trade closer to net asset value with limited exploration upside, quality developers can generate multiples of return through successful project advancement or strategic acquisition at premium valuations.

The M&A optionality embedded in quality development companies effectively functions as a "free call option" on sector consolidation trends. This optionality becomes increasingly valuable as the scarcity of quality development opportunities forces strategic buyers to compete more aggressively for available assets.

Tactical Entry Opportunities & Portfolio Construction Strategy

Current market conditions create tactical entry opportunities as near-term gold price consolidation pressures development company valuations. This temporary valuation compression allows strategic investors to establish positions in quality companies at attractive valuations before catalyst-driven rerating occurs.

Portfolio construction strategies should focus on companies demonstrating three critical characteristics: proven resource quality with low all-in sustaining cost profiles, operations in established mining jurisdictions with transparent regulatory frameworks, and management teams with demonstrated ability to advance projects through development stages.

The risk-adjusted return profile of this positioning strategy benefits from multiple value realization paths. Companies can generate returns through successful operational development, gold price appreciation leverage, or strategic acquisition premiums, reducing single-point-of-failure risks while maintaining upside exposure to sector themes.

The Investment Thesis for Gold

- Strategic allocation to gold development companies in 2025 offers exposure to multiple converging themes that create compelling risk-adjusted return opportunities for institutional and retail investors seeking leverage to structural sector changes.

- Structural supply constraints represent the foundational investment thesis, with years of underinvestment creating a situation where reserves are not being replaced at the pace of production. This supply deficit creates scarcity value for quality development projects and supports premium valuations for companies with proven resources and clear development paths.

- M&A optionality provides embedded upside potential as majors actively seek development-stage acquisitions to supplement organic growth. Premium valuations are consistently being paid for high-quality projects, creating "free call options" on consolidation activity for shareholders of well-positioned developers.

- Macro tailwinds including Federal Reserve policy discord, fiscal sustainability concerns, and persistent geopolitical instability reinforce gold's portfolio hedge characteristics. These structural factors support sustained institutional allocation to gold-related investments, providing valuation support across the sector.

- Asymmetric equity upside differentiates development companies from established producers, with companies like Cabral Gold, New Found Gold, and i-80 Gold providing significantly higher leverage to gold price movements than large-cap producers trading closer to net asset value.

- Jurisdictional stability mitigates geopolitical risk for companies operating in established mining regions with transparent regulatory frameworks. This stability premium becomes increasingly valuable as political risk rises in traditional gold-producing regions.

- Operational leverage to gold price movements creates compelling return scenarios at current price levels, with many development projects showing exceptional economics at gold prices above $3,000 per ounce compared to their original feasibility studies based on conservative pricing assumptions.

Scarcity & Optionality as the Core 2025 Theme

Gold's resilience, demonstrating 40% year-over-year gains despite tactical consolidation periods, reflects underlying structural changes in both monetary policy and mining sector fundamentals. The combination of supply constraints and renewed strategic acquisition appetite creates a uniquely favorable environment for selective development company positioning.

Structural supply limits have created genuine scarcity premiums for high-quality development projects, with M&A optionality increasingly embedded in valuations as strategic buyers compete for limited available assets. This dynamic offers multiple paths to value realization for investors positioned in quality development companies with proven resources and clear advancement catalysts.

For both institutional allocators and sophisticated retail investors, strategic positioning in select gold developers provides leveraged exposure to macro monetary themes while capturing sector-specific scarcity dynamics. The convergence of these factors suggests that 2025 may represent an inflection point where development company valuations begin reflecting true replacement cost economics rather than historical distressed metrics.

Analyst's Notes

Subscribe to Our Channel

Stay Informed