Gold's Record Rally & the Next Generation of Emerging Producers: An Investor's Guide

Gold hits $3,534/oz on tariff shocks and geopolitical tensions while emerging producers Cabral Gold, Integra Resources, and New Found Gold offer growth exposure.

- Gold has surged to record highs of $3,534 per ounce, driven by unexpected tariff shocks on Swiss gold bars, escalating geopolitical tensions, and growing stagflation fears that have pushed the precious metal's year-to-date performance to 32% versus just 8% for the S&P 500.

- A new generation of emerging gold producers across multiple jurisdictions is positioning to capitalize on this bull market, with companies like Cabral Gold in Brazil's Tapajós province, Integra Resources in Nevada's Great Basin, and New Found Gold in Newfoundland offering distinct risk-reward profiles.

- These emerging producers are demonstrating robust project economics with internal rates of return ranging from 33% to 139% at current gold prices, while established operators like Perseus Mining and Serabi Gold provide cash flow stability and proven execution in their respective markets.

- The convergence of record gold prices, streamlined permitting processes under new U.S. policies, and significant exploration upside across multiple districts creates a compelling backdrop for selective investment in the gold mining sector.

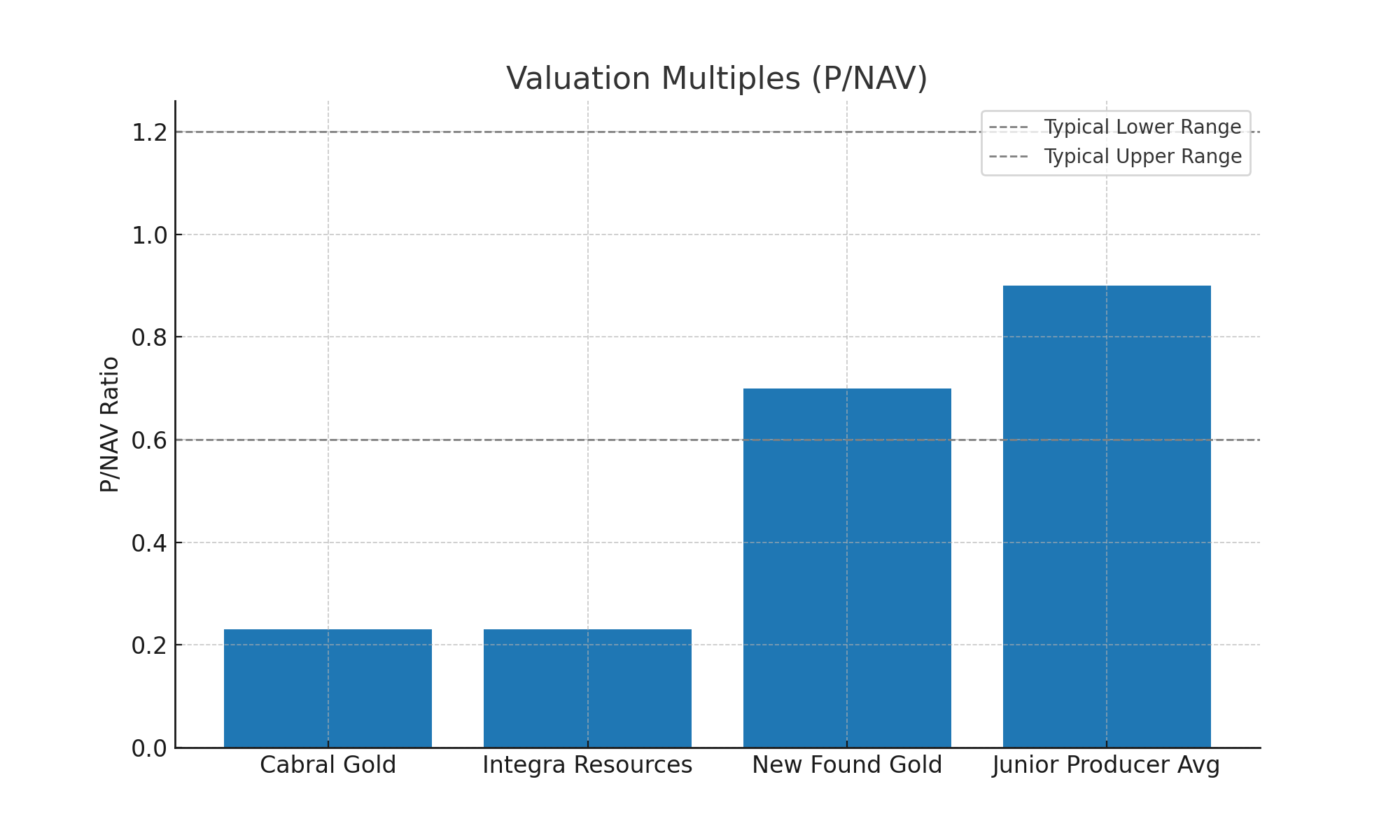

- Valuation disparities among emerging producers present opportunities for investors, with companies trading at 0.23x to 0.7x price-to-net asset value ratios compared to traditional junior producer multiples of 0.6x to 1.2x, suggesting substantial re-rating potential.

The Gold Market's Historic Breakout

Gold's ascent to record territory represents more than just another commodity rally; it reflects a fundamental shift in global economic dynamics that investors cannot ignore. The precious metal's climb to $3,534 per ounce before settling at current levels has been driven by three converging forces that underscore gold's renewed relevance in modern portfolios.

The most immediate catalyst came from an unexpected source: U.S. Customs and Border Protection's ruling that 1-kilogram and 100-ounce gold bars from Switzerland, a major bullion supplier, are subject to tariffs of up to 39%. This decision caught markets off guard, as previous guidance had suggested these products would be exempt. The irony was palpable: an asset traditionally used to hedge against inflation was itself being subjected to inflationary pressures through taxation.

Beyond the tariff shock, geopolitical tensions have elevated gold's safe-haven status. Strained U.S. relations with Russia and China, combined with ongoing uncertainties in Ukraine, have reinforced the metal's appeal as a store of value independent of any single government's policies. This dynamic has been further amplified by central bank buying, with institutions worldwide diversifying their reserves away from traditional currencies.

The third pillar supporting gold's rally stems from macroeconomic concerns about stagflation. Despite robust Q2 GDP figures, weakness in labor markets combined with persistent inflation signals have created an environment that historically favors precious metals. When traditional assets struggle to provide real returns in an inflationary environment, gold's appeal as a wealth preservation vehicle becomes paramount.

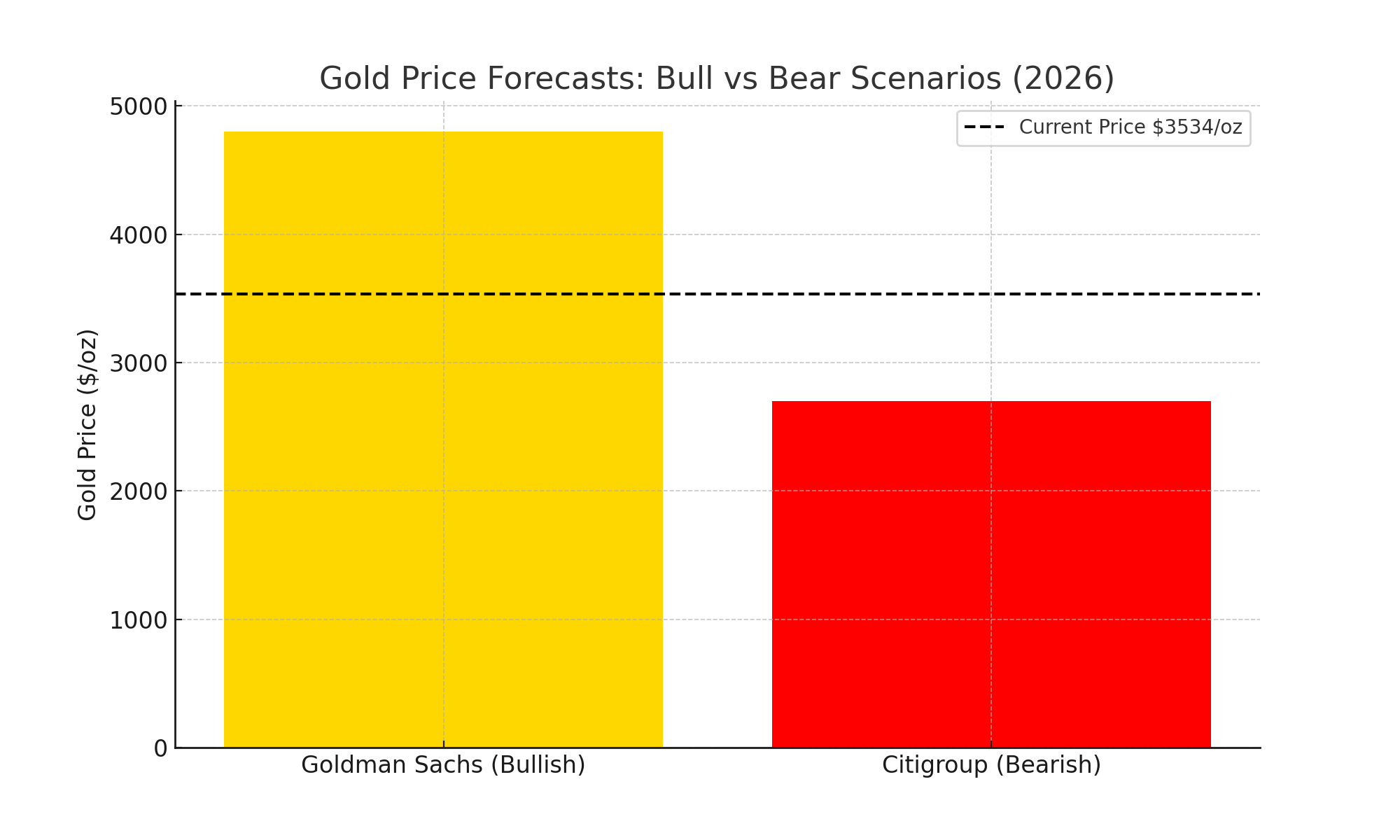

Goldman Sachs has captured this sentiment in their projections, suggesting gold could reach $3,700 or even $4,800 by mid-2026, driven by recession fears and continued central bank accumulation. However, not all analysts share this optimism. Citigroup has cautioned about potential downside, forecasting a possible correction to $2,500-$2,700 per ounce if economic conditions improve significantly.

The Emerging Producer Landscape

Against this backdrop of record gold prices and uncertain economic conditions, a new generation of gold producers is emerging across multiple jurisdictions, each offering distinct advantages and risk profiles that investors should carefully consider.

Brazil's Tapajós Province: The Next Gold Rush

Brazil's Tapajós province has emerged as one of the most compelling gold districts globally, with companies like Cabral Gold and Serabi Gold leading the charge in this historically productive region. The Tapajós gold rush from 1978 to 1995 yielded approximately 30 million ounces, establishing it as Brazil's third-largest gold district. The recent entry into production of G Mining Ventures' Tocantinzinho mine in September 2024 has validated both the region's geology and its infrastructure capabilities.

Cabral Gold's Cuiú Cuiú project exemplifies the district's potential. With over 1.2 million ounces in compliant resources and multiple high-grade discoveries including intercepts exceeding 30 grams per tonne, the company has outlined a compelling development pathway. Their July 2025 Preliminary Feasibility Study confirms exceptional economics with a 78% internal rate of return and $74 million net present value at $2,500 per ounce gold, supported by relatively modest capital expenditure of $37.7 million.

"The starter project has a very strong IRR of 77%, a 10 month payback and is expected to generate after tax cash flows averaging over $20 million annually during its initial six year mine life. All this at $2,500 an ounce. The free cash flow generated by this oxide project will be directed into the funding of stage two development of Kuyukuyu, accelerating the exploration evaluation program, focused on the primary resources of Kuyukuyu." - John Sestan, VP Project Development, Cabral Gold.

The project's phased development approach beginning with oxide heap leach operations targeting 25,000 ounces annually in the initial years provides a low-risk entry point that can self-fund expansion into much larger hard rock operations. At current spot prices near $3,340 per ounce, the project's IRR jumps to an impressive 139%, highlighting the leverage these emerging producers offer to gold price movements.

Serabi Gold represents a different model within the same province, having established itself as a sustainable producer at the Palito Complex while developing the Coringa expansion. The company's three-phase growth strategy targets expansion from current levels of 30-40,000 ounces annually to over 100,000 ounces by 2028. Their 2024 Preliminary Economic Assessment for Coringa demonstrates robust economics with all-in sustaining costs of $1,241 per ounce and strong recovery rates of 97%.

"Maintain quality, maintain quality, don't chase quantity. Tons cost, grade pays. We chase margin, we chase quality. While the gold price is like this, that's where the money comes from. We're not just going to use this gold price to chuck all kinds of rubbish in and just chase scale. It's astonishing how much money you make if you keep the grade high and the gold price is like this." - Michael Hodgson, CEO, Serabi Gold.

North American Opportunities: Stability Meets Growth

The North American gold mining landscape offers a compelling contrast to emerging markets, combining jurisdictional stability with significant growth potential. Integra Resources exemplifies this opportunity, transitioning from developer to producer with its Florida Canyon Mine in Nevada while advancing two major development projects.

Integra's Florida Canyon operation provides immediate cash flow, targeting 70-75,000 ounces annually with six years of remaining mine life. However, the real value lies in the company's development pipeline. The DeLamar project in Idaho, with its historic production of 750,000 ounces of gold and 47.6 million ounces of silver, offers exceptional economics with an internal rate of return of 33% and all-in sustaining costs of just $814 per ounce.

Recent policy changes have created additional tailwinds for U.S. gold development. Idaho's SPEED Act and federal executive orders promoting domestic mineral independence are streamlining permitting processes, potentially accelerating project timelines. Integra has also demonstrated strong stakeholder engagement, with the company noting regarding their Relationship Agreement with the Shoshone‑Paiute Tribes that:

"This Agreement is unprecedented in the Lower 48 States, in both recognizing Tribal sovereignty and collaboratively advancing sustainable, long‑term economic development for a project located on federally managed lands."

The Nevada North project adds another growth leg, with a 2023 Preliminary Economic Assessment outlining a 13-year mine life producing approximately 80,000 ounces annually.

New Found Gold in Newfoundland represents perhaps the most compelling high-grade opportunity in North America. The company's Queensway project has delivered a robust Preliminary Economic Assessment with an after-tax net present value of C$743 million and an internal rate of return of 56%.

"The PEA highlights a phased approach that gets us to cash flow rapidly. At a $2,500 gold price the net present value is $743 million, it gives us a 56.3% after-tax IRR with less than a two-year payback on a $155 million initial capital cost. Once that's in production, we'll use the cash flow to fund the build-out of the larger 7,000-tonne-a-day plant and underground, ultimately producing over 170,000 ounces a year at just under $1,100 an ounce. - Keith Boyle, CEO, New Found Gold.

The phased development strategy, beginning with 700 tonnes per day toll milling before expanding to a 7,000 tonnes per day on-site plant, provides operational flexibility while maintaining exposure to the high-grade resource base averaging 2.40 grams per tonne.

West Red Lake Gold offers a unique "restart" story in Ontario's proven Red Lake district. The company's successful restart of the Madsen Mine, combined with strong bulk sample reconciliation results, demonstrates the viability of their approach. With production targeting 65,000 ounces annually from Madsen and additional growth from the Rowan project's 35,000 ounces per year, the company is building toward becoming a 150,000-ounce annual producer.

Recent drilling results continue to validate the high-grade potential at Madsen, with the company reporting exceptional intercepts including 36.85 grams per tonne gold over 6.9 meters, 92.39 grams per tonne over 2 meters, and 8.79 grams per tonne over 15.5 meters from the South Austin Zone. Shane Williams, President & CEO, emphasized the importance of these findings:

"The high‑grade panel of gold mineralization the team is currently defining and expanding in South Austin has been delivering exceptional grades and thicknesses. Archaean lode‑gold vein systems like Madsen are well known for having pockets of mineralization that are often discrete, very high‑grade and require tight‑spaced drilling to properly define. The success we are having... underscores the importance of getting the drills deeper in the system and into high priority areas of the deposit so that additional high‑grade pockets and lenses can be discovered, drilled off and integrated into the mine plan."

These results further expand on the high-grade panel of gold mineralization within South Austin, which has been a key focus of definition drilling in 2025, according to the company's recent announcement.

Established Producers Capitalizing on Market Conditions

While emerging producers offer significant leverage to gold price movements, established operators like Perseus Mining provide stability and proven execution capabilities that appeal to risk-conscious investors. Perseus delivered 496,551 ounces in fiscal 2025 at all-in sustaining costs of $1,235 per ounce, generating substantial cash flow that has enabled significant shareholder returns.

"Once again, our operations have performed very well. We've produced something like 121,237 ounces for the quarter at an all-in site cost of $1,417 an ounce. Now, with a gold price of around $3,000 an ounce, that's giving us $1,560 per ounce margin. So very strong cash flow, very strong residual cash and bullion balances at the end of the year." - Jeff Quartermaine, CEO, Perseus Mining.

The company's multi-jurisdictional approach, spanning West Africa and East Africa, provides geographic diversification while maintaining focus on Tier-1 assets. Perseus's development of the Nyanzaga project in Tanzania, expected to become their lowest-cost operation at $1,230-$1,330 per ounce all-in sustaining costs, demonstrates their ability to advance major projects while maintaining operational excellence at existing mines.

Perseus's balance sheet strength with $827 million in cash and bullion and zero debt positions the company to weather market volatility while funding growth initiatives. The company's capital return program, including $275 million in dividends and buybacks during fiscal 2025, showcases management's commitment to shareholder value creation.

Valuation Opportunities & Investment Considerations

Current market conditions have created significant valuation disparities within the gold mining sector, presenting opportunities for discerning investors. Many emerging producers trade at substantial discounts to their net asset values, with companies like Integra Resources trading at just 0.23x price-to-net asset value compared to typical junior producer multiples of 0.6x to 1.2x.

These valuation gaps reflect several factors, including jurisdictional risk premiums, execution concerns, and the market's current preference for established producers with proven cash flows. However, for investors willing to accept development risk, these disparities offer potential for significant re-rating as projects advance through construction and into production.

The leverage these companies provide to gold price movements cannot be overstated. Each $100 per ounce increase in gold prices typically adds $89 million to New Found Gold's net present value, while Cabral Gold's internal rate of return jumps from 78% to 139% at current spot prices versus their base case assumptions.

For Investors

The current environment presents both opportunities and challenges for gold mining investors. Record gold prices provide substantial tailwinds for project economics and cash flows, but they also raise questions about sustainability and entry timing. Companies with low-cost operations and robust balance sheets are best positioned to maintain margins if gold prices moderate from current levels.

Jurisdictional considerations remain paramount. While emerging markets like Brazil offer exceptional geological potential and lower development costs, they carry additional political and operational risks. North American projects command premium valuations but benefit from stable regulatory environments and established infrastructure.

The permitting landscape has evolved favorably for U.S. projects, with recent policy changes emphasizing domestic mineral security and streamlined approval processes. These developments particularly benefit companies like Integra Resources and West Red Lake Gold, which operate in established mining jurisdictions with supportive regulatory frameworks.

Exploration upside represents another key differentiator among investment opportunities. Companies operating in district-scale environments with significant untested targets offer the potential for resource growth beyond current project economics. New Found Gold's 110-kilometer strike length with only 4.3 kilometers currently defined exemplifies this potential, as does Cabral Gold's regional exploration program across more than 50 peripheral targets.

Positioning Investors for Gold's Next Chapter

Gold's record-breaking performance reflects fundamental shifts in global economic dynamics that extend beyond short-term market movements. The convergence of trade policy uncertainty, geopolitical tensions, and macroeconomic instability has restored gold's relevance as both a portfolio hedge and a growth investment.

The emerging producer landscape offers investors multiple pathways to participate in this gold renaissance, from high-grade, low-capital projects in stable jurisdictions to district-scale opportunities in emerging markets. While each investment carries distinct risks and rewards, the current environment of record gold prices and improving project economics creates compelling opportunities for selective investors.

Success in this environment requires careful evaluation of project fundamentals, jurisdictional considerations, and management execution capabilities. Companies with strong balance sheets, proven development teams, and assets that can generate attractive returns across a range of gold price scenarios are best positioned for long-term success.

As gold continues to challenge traditional assumptions about portfolio construction and value storage, the mining companies that can efficiently convert geological resources into profitable operations will reward investors who recognize the strategic value of precious metals exposure in an increasingly uncertain global environment.

Analyst's Notes

Subscribe to Our Channel

Stay Informed