US Nuclear Fuel Investment & Global Production Cuts Accelerate Uranium Contracting as Fuel-Cycle Spending Reaches $170 Billion

Uranium contracting is accelerating as $170 billion in nuclear fuel-cycle investment and global production cuts tighten long-term supply.

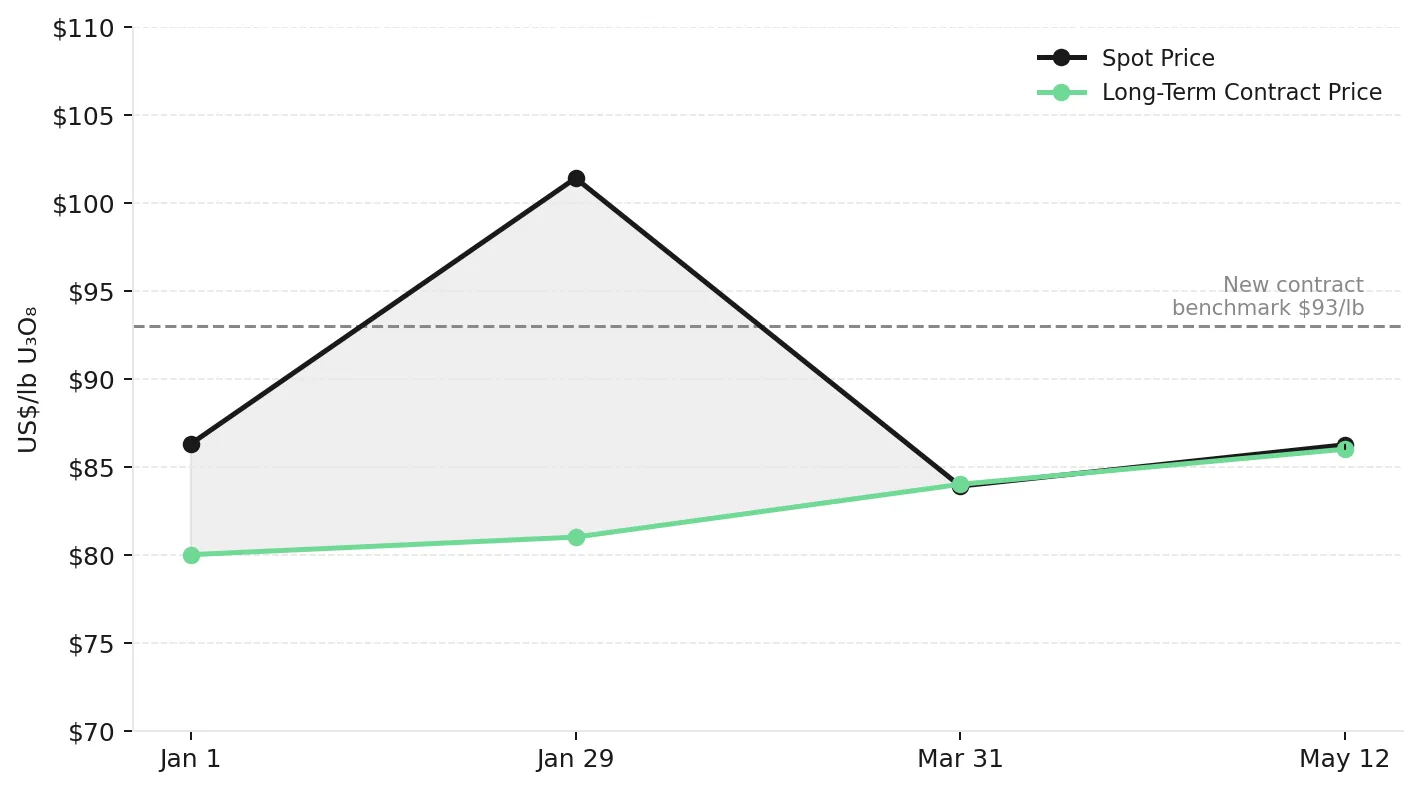

- Uranium's $86.25/lb spot price has converged with the $86/lb long-term contract price, reducing the economic incentive for utilities to defer multi-year supply agreements.

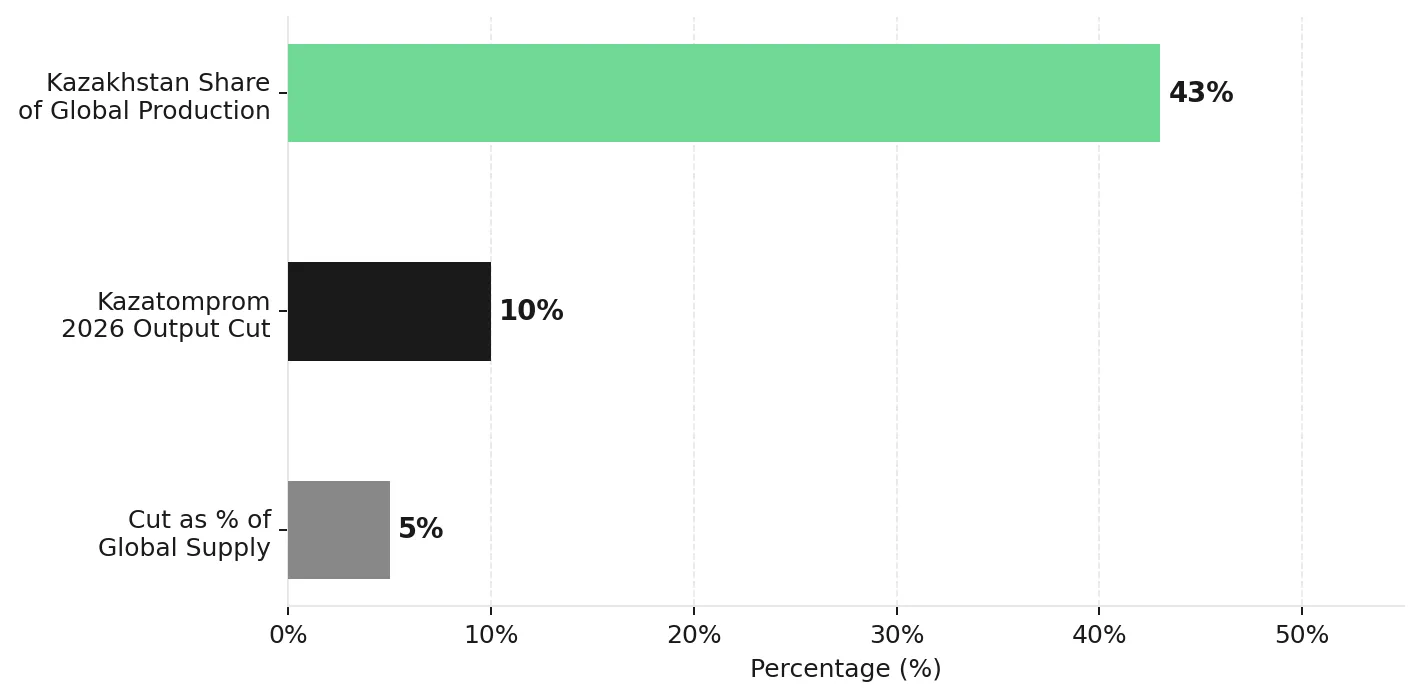

- Kazatomprom's 10% production cut removes approximately 8 million pounds of U3O8, or 5% of 2026 global primary supply, tightening available utility supply through a strategic value-over-volume decision rather than an operational disruption.

- The NextEra Energy and Dominion Energy merger combines 110 GW of generation capacity and concentrates a historically large block of uncovered uranium demand into a single utility buyer.

- Italy's nuclear enabling legislation, confirmed for summer 2026 passage, adds a seventh G7 economy to long-term reactor development planning and reinforces that European nuclear expansion is being driven by formal energy policy rather than short-term power market conditions.

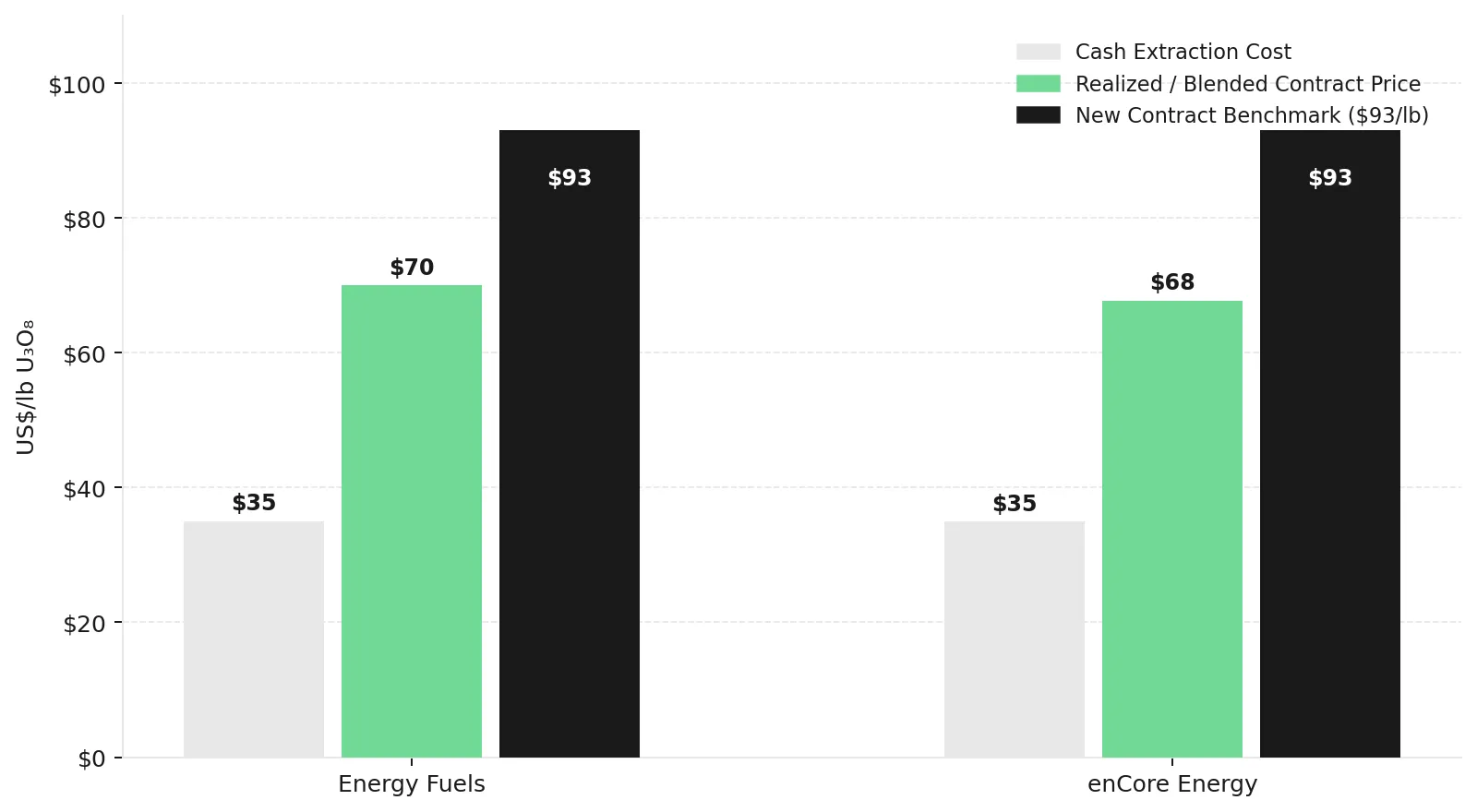

- Production-stage US uranium companies with self-extracted cash costs below $35/lb are positioned for margin expansion as legacy contracts expire and new long-term contract pricing reaches $93.00/lb, the highest benchmark in over 18 years.

On May 12, 2026, uranium traded at $86.25/lb U3O8. More important for utility procurement, long-term contract pricing has risen from $79-82/lb to $86/lb year-to-date, eliminating the spot-market discount utilities previously used to delay contracting. Equal spot and long-term uranium prices reduce the incentive for utilities to rely on short-term purchasing strategies, increasing long-term supply contracting.

The same week, McKinsey estimated that the US nuclear fuel supply chain requires $80 billion to $170 billion in investment to support 300 GW of reactor capacity by 2050. The scale of required fuel-cycle investment indicates that US nuclear expansion policy now supports sustained long-term uranium procurement rather than short-term reactor deployment targets. The key investment distinction is which producers, developers, and explorers have the jurisdiction, permitting, and balance-sheet capacity to secure new utility contracts as term contracting accelerates.

Utility Consolidation & Nuclear Policy Increase Long-Term Uranium Procurement

On May 18, 2026, NextEra Energy and Dominion Energy announced an all-stock merger combining 110 GW of generation capacity and approximately 10 million customer accounts. Pending Nuclear Regulatory Commission approval over 12 to 18 months, the merger is expected to reduce spot-market purchasing activity from two major nuclear operators as procurement is consolidated. Following close, the combined entity is expected to enter the market with one of the largest uncovered uranium procurement positions in the US utility sector, with new long-term contracts currently priced near $93.00/lb.

William Sheriff, Executive Chairman of enCore Energy, explains how production scale improves utility contracting leverage and financing flexibility:

“You've got to get some size for a number of reasons. Your credit ratings go up, so your cost of capital goes down. Your ability to deal on more favorable terms with your customers, that be at the nuclear utilities, that's going to increase as a larger scale company. We wanted to get to a million pounds a year because then you become meaningful to the utilities.”

European Nuclear Policy Reversal & Middle East Energy Disruption Strengthen Uranium Demand

Italy's President told the Senate in May 2026 that the government is targeting summer passage of nuclear enabling legislation supporting 8 GWe of capacity by 2050, potentially rising to 16 GWe or 20-22% of national electricity demand. European Commission President Ursula von der Leyen described the bloc's nuclear exit as "a strategic mistake", signaling increased political support for long-term nuclear generation within the EU (NucNet, 2026). The Q1 2026 war in Iran and the closure of the Strait of Hormuz drove uranium spot prices from $101.41/lb to $83.90/lb while increasing European policy support for domestic nuclear generation and fuel security.

Kazatomprom's 10% Reduction Tightens Global Uranium Supply

Kazatomprom reduced its 2026 nominal production from 32,777 tonnes to 29,697 tonnes of uranium, a 10% cut equivalent to approximately 8 million pounds of U3O8 or 5% of global primary supply. The company's 1H2025 financial results confirmed stable sulfuric acid supply for 2026, indicating the reduction was driven by pricing discipline rather than operational constraints. Kazatomprom controls 43% of global uranium production and has characterized the cut as an effort to support pricing rather than maximize output. Long-term contract prices have risen from $79-82/lb to $86/lb year-to-date, indicating utilities are prioritizing supply security rather than waiting for uranium prices to decline.

US-China Supply Fragmentation Increases Demand for Western Uranium Projects

The May 2026 US-China trade summit produced no durable critical minerals framework , preserving supply-chain uncertainty for Western nuclear fuel procurement. Critical minerals agreements are increasingly forming between third-party nations outside US-China negotiations, increasing utility preference for uranium supply from politically aligned jurisdictions. Uranium projects in Canadian and US basins, along with development-stage assets in mining-supportive jurisdictions such as Zambia, which carries no government free-carried interest, are positioned to benefit from increased utility demand for non-Russian and non-Chinese supply.

Spot & Term Uranium Prices Equalize as Utility Contracting Accelerates

Uranium's spot price peaked at $101.41/lb on January 29, 2026, fell to $83.90/lb by the end of Q1 2026, and recovered to $86.25/lb. Long-term contract prices have risen from $79-82/lb to $86/lb year-to-date, while new long-term contracts are being signed near $93.00/lb, the highest benchmark in more than 18 years. Similar spot and long-term uranium pricing levels preceded the 2006-2007 uranium contracting cycle, when utilities accelerated multi-year supply agreements. Producers with uncovered 2026-2028 delivery windows are positioned to secure higher realized pricing as legacy contracts expire.

US Fuel-Cycle Investment Expands Domestic Nuclear Supply Capacity

On January 5, 2026, the US Department of Energy awarded $2.7 billion to Orano Fed Services, American Centrifuge Operating, and General Matter for domestic enrichment capacity. In May 2026, the DOE selected Oklo, Terrestrial Energy, TRISO-X, and Valar Atomics for advanced nuclear fuel pilot programs supporting future reactor deployment. The investments reduce domestic enrichment and fuel-supply uncertainty that previously delayed long-term uranium contracting by US utilities. Simultaneously, TEPCO's Kashiwazaki-Kariwa Unit 6, a 1,356 MW reactor, restarted on February 9, 2026 and entered commercial operation, bringing Japan to 15 operating reactors with 33 GW of combined capacity. Each additional reactor restart increases long-term uranium procurement requirements for Japanese utilities

Uranium Investment Opportunities Across Producers, Developers and Explorers

Development stage, jurisdiction, and balance-sheet strength determine which uranium companies can secure new utility contracts as long-term contracting activity increases.

Production-Stage Uranium Companies Positioned for Higher Contract Pricing

Energy Fuels reported Q1 2026 revenue of $35.8 million from 510,000 pounds of uranium oxide sold at $70.04/lb, below the current $93.00/lb long-term contract benchmark, positioning the company for higher realized pricing as legacy contracts roll off. White Mesa Mill in Utah is the only US facility licensed to process both uranium ore and monazite into separated rare earth oxides, and achieved first US primary production of terbium oxide at 99.9% purity in March 2026, expanding Energy Fuels' exposure to domestic critical minerals supply chains.

Mark Chalmers, Chief Executive Officer of Energy Fuels, states the integration mandate anchoring both revenue streams:

"We're building a critical mineral hub that revolves around the uranium business. To compete with China, you need every step of the supply chain integrated."

enCore Energy is the only US uranium producer operating two ISR processing facilities in South Texas, increasing its ability to supply contracted volumes domestically. Q1 2026 self-extracted uranium cost $34.94/lb against the current $93.00/lb long-term contract benchmark, while production reached 90,000 pounds, up 22% year-on-year, supporting significant margin expansion potential. Repricing current volumes from the $67.78/lb blended contract price toward the $93.00/lb benchmark would add approximately $6.8 million per quarter without additional capital investment. Dewey Burdock in South Dakota has cleared all federal Nuclear Regulatory Commission permits, positioning the project for potential construction in early 2027 pending state-level approval.

Development-Stage Uranium Companies Advance Toward Commercial Scale

IsoEnergy holds the Hurricane deposit in Saskatchewan's Athabasca Basin, which contains the world's highest-grade published Indicated uranium resource at 48.6 million pounds U3O8 grading 34.5% U3O8, located 40 km from the McClean Lake mill. May 2026 drilling returned 11.61% U3O8 over 1.0 metre at the Hurricane South Trend, supporting the potential expansion of mineralization beyond the current resource boundary, with a 20-hole summer 2026 program planned.

Phil Williams, Chief Executive Officer of IsoEnergy, explains how balance-sheet strength allows the company to time development decisions around uranium market conditions:

"With the money we have, we're fully funded for that. We're in a position where we don't need to rush development decisions. We want to maximize the value of every pound that we produce, and the stronger uranium market gives us more flexibility on timing."

Atomic Eagle holds the Muntanga Uranium Project in Zambia with a JORC resource of 58.8 million pounds U3O8 grading 309 ppm across a 146 km strike length, representing one of Africa's largest undeveloped uranium resources by contained pounds. The 2026 drill campaign at Chisebuka has returned grades more than three times the current resource average at near-surface depths, supporting potential low strip-ratio open-pit mining and heap leach recoveries above 90%. On May 19, 2026, the company secured an option over the 429 square kilometer Sitwe Uranium Project in Zambia, increasing its tenement holdings by 38% at an entry cost of US$200,000.

Phil Hoskins, Chief Executive Officer of Atomic Eagle, states the 2026 resource growth target:

"We'd love to get it over 100 million pounds by the end of the year. Increasing that scale will ensure that even at $90 a pound the economics will look extremely favorable."

Exploration-Stage Uranium Companies Target Large-Scale Discoveries in Established Basins

ATHA Energy controls 100% of the Angikuni Basin in Nunavut and holds a 6.8 million-acre uranium exploration portfolio, one of the largest land positions in Canada's uranium sector. The fully funded CAD $63 million 2026 exploration program includes 20,000 meters of drilling across three rigs between May and September 2026. At RIB North, a maiden 2025 drill hole returned 34.7 meters of composite mineralization with grades up to 8.16% U3O8 over 0.5 meters, well above the 1% U3O8 high-grade threshold commonly used in uranium exploration, with follow-up drilling scheduled for the 2026 program.

Troy Boisjoli, Chief Executive Officer of ATHA Energy, describes the discovery scale supporting the expanded 2026 program:

"In the Rib area, we drilled 13 holes contiguously over about 14 km, and every hole was mineralized. The best result was more than 34 meters of mineralization, including 13 meters grading over 0.5% U3O8 with intervals above 8%."

The Investment Thesis for Uranium

- Spot and long-term uranium prices reaching $86/lb reduces the incentive for utilities to delay contracting, because equal pricing increases the risk of securing future supply at higher contract rates.

- Kazatomprom's 10% production reduction supports higher uranium contract prices because the reduction is embedded in renegotiated subsoil use agreements that limit near-term output increases.

- US investment of $2.7 billion in domestic enrichment capacity reduces fuel-supply uncertainty that previously delayed long-term uranium contracting by US utilities.

- The merger of two major US nuclear operators concentrates one of the largest uncovered uranium procurement positions in the sector, with new long-term contracts currently priced at the highest benchmark in more than 18 years.

- Producers with low cash extraction costs can increase margins as legacy uranium contracts expire and are renewed at higher market prices, generating additional revenue without new capital investment or higher spot uranium prices.

- Developers in politically aligned jurisdictions are positioned to benefit from utility demand for non-Russian and non-Kazakh uranium supply as utilities begin contracting for reactors scheduled to enter service before 2030.

- Exploration-stage uranium companies with fully funded drill programs in established basins can generate significant equity upside from new discoveries, particularly where existing mineralization remains untested and market valuations remain below the cost of acquiring equivalent uranium resources through M&A.

The uranium market saw five major developments simultaneously, including spot-term price convergence at $86/lb, an 8 million pound Kazatomprom supply reduction, a major US nuclear utility merger, nuclear enabling legislation in Italy, and a McKinsey estimate that the US nuclear fuel supply chain requires up to $170 billion in investment. Together, these developments support higher long-term uranium contracting and tighter future supply availability. The McKinsey estimate indicates that large-scale nuclear expansion will require sustained long-term investment across the uranium fuel cycle. The key investment distinction is which producers, developers, and explorers have the jurisdiction, permitting, and balance-sheet capacity to secure new utility contracts as long-term uranium contracting accelerates. The scale of projected fuel-cycle investment indicates that long-term uranium demand growth is increasingly being supported by formal energy and industrial policy.

TL;DR

Uranium markets are entering a new contracting cycle as spot and long-term prices equalize near $86/lb, removing the incentive for utilities to delay procurement. At the same time, Kazatomprom's 10% production cut is tightening global supply, while US nuclear fuel investment requirements have reached as much as $170 billion through 2050. Utility consolidation, European nuclear policy support, and growing demand for non-Russian supply are increasing long-term contracting pressure. Production-stage uranium companies with low extraction costs are positioned for margin expansion, while developers and explorers in politically aligned jurisdictions could benefit from increased utility demand and future supply deficits.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed